|

시장보고서

상품코드

1836698

양수천자침 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Amniocentesis Needle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

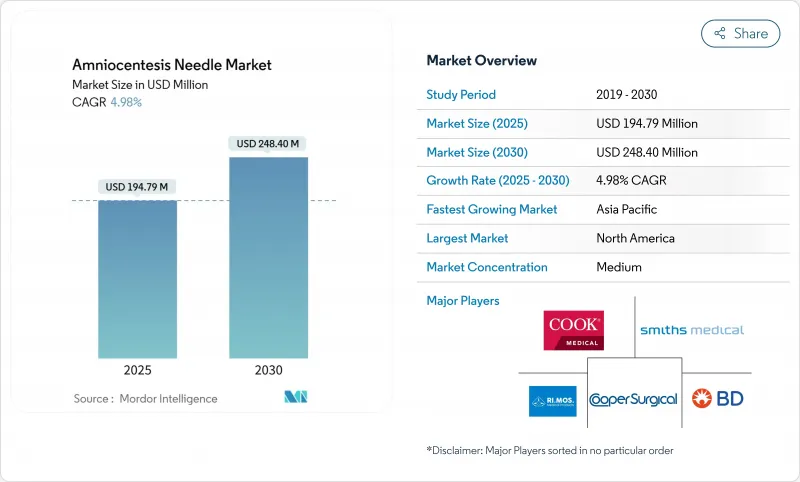

양수천자침 시장은 2025년에 1억 9,479만 달러로 추정되고, 2030년에는 2억 4,840만 3,000달러에 달할 것으로 예측되며, CAGR 4.98%로 성장할 전망입니다.

비침습적인 산전 검사가 급증하고 있음에도 불구하고, 확정적인 진단 정밀도가 요구되는 양수천자, 제대천자, 태아수혈에 있어서 이 기구가 필수적인 역할을 하고 있음을 반영하여 꾸준하고 계획적인 확대가 보입니다. 수요는 고위험 임신에 집중하고 임상의는 모체와 태아의 결과를 보호하기 위해 최고 정확도의 장비를 요구합니다. 고령 출산, 보조생식 기술의 이용 확대, 출생 전 스크리닝의 의무화 확대 등 인구 레벨의 시프트와 연동하여 초음파의 시인성을 높여 안전 정지 기능을 포함한 프리미엄 제품의 이용이 증가하고 있습니다. 새로운 보험 상환 정책은 외래 환자에 대한 치료의 전환을 촉진하는 반면, 장기적인 성장은 복잡한 태아 개입을 지원할 수 있는 병원과 3차 센터에 고정되어 있습니다.

세계의 양수천자침 시장 동향 및 인사이트

유전성 및 염색체 이상의 부담 증가

염색체 이상은 세계 출생아의 0.6%에 영향을 주며, 트리소미 21의 발생률은 어머니의 나이가 35세를 넘으면 급상승합니다. 국가의 스크리닝 프로그램이 더 넓은 네트워크를 갖고 있는 동안, 확인적 침습적 검사는 여전히 임상적 골드 표준이며 양수천자침 시장은 출생 전 경로에 확고하게 통합되어 있습니다. 유전 카운슬러는 일상적으로 스크리닝이 진단의 확실성을 대체하지 않는다는 것을 강조하고 반복 삽입 및 치료와 관련된 불안을 줄이는 고정밀 바늘에 대한 수요를 유지합니다.

모체 연령 상승 및 이에 따른 임신 위험

2025년 40세 이상 여성의 임신은 Trisomy 21의 위험이 98명 중 1명인 반면, 29세에서는 1,095명 중 1명입니다. 이러한 인구통계학적 현실은 직업적 우선순위 및 사회경제적 변화에 힘입어 첫 NIPT의 결과에 관계없이 침습적 진단이 권장되는 환자의 안정적인 풀을 형성합니다. 따라서 장비 제조업체는 다양한 모체의 해부학 구조에서 단일 경로를 성공적으로 달성하기 위해 인체 공학적 허브와 에코 소스가되는 팁을 계속 선호합니다.

cfDNA 스크리닝의 급속한 보급

전문학회의 추천으로 NIPT의 보급으로부터 2년 이내에 침습적 진단 검사는 44% 감소했습니다. 저위험 여성의 98.6%가 cfDNA 음성인 경우, 침습적 확인을 거부하고 있기 때문에 기본적인 검사 건수는 감소하고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 체외수정(IVF)과 관련된 다태 임신 증가

- 천자 정확도를 향상시키는 AI 가이드 초음파

- 태아 의학 전문의 부족

부문 분석

100-150mm 클래스는 2024년 양수천자침 시장 점유율의 54.12%를 차지했으며 일상적인 양수천자와 제대천자에 대한 적응성으로 그 지위를 획득했습니다. 사용자의 피드백은 취급의 용이성, 안정된 초음파의 시인성, 보다 낮은 모체 불쾌감 스코어가 강조되어, 대량 생산을 실시하고 있는 산과 의료 시설에서의 지지를 확고하게 하고 있습니다. 그러나 150mm를 넘는 긴 바늘은 어머니의 BMI 상승과 후기 임신 개입이 자궁에 깊게 도달할 것을 요구하기 때문에 CAGR 5.34%에서 이 범주를 웃돌고 있습니다. 바늘의 혁신자는 현재 샤프트에 마이크로 에칭을 실시하고 양막강과 제대 정맥에 들어갈 때 잠긴 스타일릿을 내장하여 과도한 천자의 위험을 최소화합니다. 임상의가 환자마다 최적의 기구를 선택할 수 있도록 많은 병원이 길이가 다른 트레이를 채용하고 있어 이 습관이 전체적인 조달량을 확대하고 이 부문의 양수천자침 시장 규모를 지지하고 있습니다.

임상의는 또한 에코 소스가 되는 첨단 형상이 실시간 AI 시각화 알고리즘에 정확하게 맞추어 높은 패스트 패스 성공률을 보고합니다. 따라서 공급업체는 바늘 길이와 자체 소프트웨어 사전 설정을 결합하여 시설이 단일 브랜드 생태계로 표준화하도록 촉구합니다. 소프트웨어 업그레이드가 공중에서 배포되면 고객은 최대한의 호환성을 위해 재고를 새로 고쳐야 합니다.

양수천자침 시장 보고서는 바늘 길이별(100mm 미만, 100-150Mm, 150mm 초과), 절차별(양수천자, 양수감소, 태아수혈, 양수수혈, 제대천자), 최종 사용자별(병원, 전문 클리닉, 외래수술센터(ASC)), 지역별(북미, 유럽, 아시아태평양, 기타)로 구분되고 있습니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

북미의 2024년 매출 점유율 37.36%는 고위험 진단의 보편적 보험 적용과 출생 전 유전학이 널리 받아들여지고 있기 때문입니다. 대형 민간지급기관이 2025년에 cfDNA의 사전 승인을 폐지함으로써 검사 경로가 합리화되었지만, 이상 증례에서 침습적 확인의 필요성은 배제되지 않고, 병원은 예측 가능한 구입 사이클에 머물고 있습니다. 지방 출산 사막은 여전히 우려 사항이지만, 원격 초음파 파트너십은 전문 지식을 더 작은 단위로 밀어 올려 양수천자침 시장 전체의 장비 판매를 간접적으로 강화합니다.

아시아태평양은 도시화, 불임 치료의 보급, 어린이 만들기 지연으로 2030년까지 연평균 복합 성장률(CAGR) 6.78%를 보일 것으로 예측됩니다. 일본이나 한국 등의 나라에서는 구미 국가와 어깨를 나란히 하는 고도 모자 연령 임신율을 기록하고 있습니다. 정부 자금을 통한 신생아 장애 이니셔티브는 이러한 교대에 부합하며 태아 의료기기의 다년간 조달 계약을 가능하게 합니다. 현지 수탁 제조업체는 스테인레스 스틸 캐뉼라를 공급하기 시작하고 비용 층을 잘라내고 고급 코팅 바늘의 채택을 확대하고 있습니다.

유럽에서는 통일된 출생 전 가이드라인과 공적 자금에 의한 스크리닝 프로그램이 있어 기본적인 수요가 보장되고 있습니다. 그러나 비용 억제에 중점을 둔 지역은 의료 제공업체를 외래 환자로 유도하고 있으며 이는 미국을 반영한 진화입니다. 의료기기 규제 조화인증 취득으로 시장 진출의 타임라인은 길어졌지만 동시에 임상의에게 제품의 안전성을 안심시켜 오래된 재고보다 AI 대응 기기로의 업그레이드를 촉구하고 있습니다. 그 결과 양수천자침 시장의 갱신주기는 초음파 진단 장치의 자본 업데이트와 동기화를 유지합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 유전성 및 염색체 이상의 부담 증가

- 모체 연령 상승 및 그에 따른 임신 위험

- 체외수정(IVF)과 관련된 다태임신 증가

- 출생 전 유전학적 검사 및 스크리닝 프로그램에 대한 의식 증가와 정부 지원

- AI 가이드 하 초음파 검사에 의한 천자 정밀도 향상

- 첨단 기술 및 다양한 제품의 가용성

- 시장 성장 억제요인

- CFDNA 스크리닝의 급속한 보급

- 모체 의료 전문의의 부족

- 침습적 처치에 있어서 소송 리스크

- 수술용 스테인레스 스틸 공급 핀치

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측 : 금액(달러)

- 바늘 길이별

- 100mm 미만

- 100-150 mm

- 150mm 이상

- 절차별

- 양수천자

- 양수감소

- 태아수혈

- 양수수혈

- 제대천자

- 최종 사용자별

- 병원

- 전문 클리닉

- 외래수술센터(ASC)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- BD

- CooperSurgical

- Cook Medical

- Smiths Medical

- RI.MOS Srl

- Laboratoire CCD

- Rocket Medical

- Sterylab Srl

- BPB Medica

- Medex Medical device

- Vigeo Srl

- GIMA Italia

- Tsumani Medical

제7장 시장 기회 및 전망

AJY 25.10.27The amniocentesis needle market stood at USD 194.79 million in 2025 and is forecast to reach USD 248.403 million by 2030, advancing at a 4.98% CAGR.

A steady yet deliberate expansion reflects the device's indispensable role in amniocentesis, cordocentesis and fetal blood transfusion-procedures that still command definitive diagnostic accuracy despite the meteoric rise of non-invasive prenatal tests. Demand concentrates in high-risk pregnancies, where clinicians insist on highest-precision instrumentation to safeguard maternal and fetal outcomes. Uptake of premium products with enhanced ultrasound visibility and built-in safety stops is rising in tandem with population-level shifts toward older motherhood, greater use of assisted reproduction and widening prenatal screening mandates. While new reimbursement policies fuel procedure migration to outpatient settings, long-term growth remains anchored to hospitals and tertiary centers that can support complex fetal interventions.

Global Amniocentesis Needle Market Trends and Insights

Rising Burden of Genetic and Chromosomal Disorders

Chromosomal abnormalities affect 0.6% of live births worldwide, with trisomy 21 incidence climbing sharply beyond maternal age 35. As national screening programs cast a wider net, confirmatory invasive tests remain the clinical gold standard, keeping the amniocentesis needle market firmly embedded in prenatal pathways. Genetic counselors routinely underscore that screening cannot replace diagnostic certainty, sustaining demand for high-precision needles that reduce repeat insertions and procedure-related anxiety.

Growing Maternal Age and Associated Pregnancy Risks

In 2025, pregnancies in women >= 40 years carry a trisomy 21 risk of 1 in 98, versus 1 in 1,095 at age 29. This demographic reality, driven by career priorities and socioeconomic shifts, anchors a steady pool of patients for whom invasive diagnostics remain recommended irrespective of initial NIPT results. Device makers therefore continue to prioritize ergonomic hubs and echogenic tips that improve single-pass success in diverse maternal anatomies.

Rapid Uptake of cfDNA Screening

Professional-society endorsements have cut invasive diagnostic testing volumes by 44% within two years of NIPT rollout. With 98.6% of low-risk women declining invasive confirmation when cfDNA is negative, base-procedure volumes retreat even as remaining interventions skew toward higher-risk pregnancies that demand premium needles.

Other drivers and restraints analyzed in the detailed report include:

- Growth in IVF-Related Multiple Pregnancies

- AI-Guided Ultrasound Improving Puncture Accuracy

- Shortage of Fetomaternal Medicine Specialists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 100 - 150 mm class captured 54.12% of the amniocentesis needle market share in 2024, a position earned through its adaptability across routine amniocentesis and cordocentesis. User feedback highlights easier handling, consistent ultrasound visibility and lower maternal-discomfort scores, solidifying loyalty among high-volume obstetric units. Longer needles above 150 mm, however, are outpacing the category at a 5.34% CAGR as rising maternal BMI and late-gestation interventions demand deeper uterine reach. Needle innovators now coat shafts with micro-etching and embed stylets that lock once the amniotic cavity or umbilical vein is entered, minimizing the risk of over-penetration. Many hospitals adopt mixed-length trays so clinicians can select the optimal device per patient, a practice that expands overall procurement volume and underpins the amniocentesis needle market size for the segment.

Clinicians also report higher first-pass success when echogenic tip geometry is mated precisely to real-time AI visualization algorithms. Vendors, therefore, pair needle length with proprietary software presets, encouraging facilities to standardize on a single brand ecosystem. As software upgrades roll out over the air, customers feel compelled to refresh inventories to ensure maximum compatibility-an aftermarket dynamic that further supports the amniocentesis needle market.

Amniocentesis Needle Market Report is Segmented by Needle Length(<100mm, 100-150 Mm and > 150 Mm), Procedure (Amniocentesis, Amnioreduction, Fetal Blood Transfusion, Amnioinfusion and Cordocentesis), End User (Hospitals, Specialty Clinics, and Ambulatory Surgical Centers), and Geography (North America, Europe, Asia-Pacific and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's 37.36% revenue share in 2024 stems from universal insurance coverage of high-risk diagnostics and broad acceptance of prenatal genetics. The 2025 removal of prior authorization for cfDNA by a leading private payer streamlines testing pathways, yet does not eliminate the need for invasive confirmation in abnormal cases, keeping hospitals on a predictable purchasing cycle. Rural maternity deserts remain a concern, but tele-ultrasound partnerships push expertise into smaller units, indirectly bolstering equipment sales across the amniocentesis needle market.

Asia-Pacific is forecast to grow at 6.78% CAGR through 2030, propelled by urbanization, fertility-treatment uptake and delayed parenthood. Nations such as Japan and South Korea now document advanced-maternal-age pregnancy rates rivaling Western peers. Government-funded newborn-disorder initiatives align with this shift, enabling multi-year procurement contracts for fetal medicine devices. Local contract manufacturers have begun to supply stainless-steel cannulae, trimming cost layers and widening adoption of premium-coated needles.

Europe enjoys uniform prenatal guidelines and public-funded screening programs that guarantee baseline demand. Regional focus on cost containment, however, nudges providers toward outpatient settings-an evolution mirroring the United States. Harmonized Medical Device Regulation certification has lengthened market-entry timelines but also reassures clinicians of product safety, encouraging them to upgrade to AI-compatible devices over older stock. Consequently, refresh cycles for the amniocentesis needle market remain synchronized with ultrasound capital refresh programs.

- Beckton Dickinson

- The Cooper Companies

- Cook Group

- Smiths Group

- RI.MOS Srl

- Laboratoire CCD

- Rocket Medical

- Sterylab Srl

- BPB Medica

- Medex Medical device

- Vigeo Srl

- GIMA Italia

- Tsumani Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Burden Of Genetic And Chromosomal Disorders

- 4.2.2 Growing Maternal Age And Associated Pregnancy Risks

- 4.2.3 Growth In Ivf-Related Multiple Pregnancies

- 4.2.4 Rising Awareness And Government Support For Prenatal Genetic Testing And Screening Programs

- 4.2.5 AI-Guided Ultrasound Improving Puncture Accuracy

- 4.2.6 Availability Of Technological Advanced And Prodcut Variety

- 4.3 Market Restraints

- 4.3.1 Rapid Uptake Of CFDNA Screening

- 4.3.2 Shortage Of Fetomaternal Medicine Specialists

- 4.3.3 Litigation Risk In Invasive Procedures

- 4.3.4 Supply Pinch In Surgical-Grade Stainless Steel

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Needle Length

- 5.1.1 < 100 mm

- 5.1.2 100 - 150 mm

- 5.1.3 > 150 mm

- 5.2 By Procedure

- 5.2.1 Amniocentesis

- 5.2.2 Amnioreduction

- 5.2.3 Fetal Blood Transfusion

- 5.2.4 Amnioinfusion

- 5.2.5 Cordocentesis

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Specialty Clinics

- 5.3.3 Ambulatory Surgical Centers

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 BD

- 6.3.2 CooperSurgical

- 6.3.3 Cook Medical

- 6.3.4 Smiths Medical

- 6.3.5 RI.MOS Srl

- 6.3.6 Laboratoire CCD

- 6.3.7 Rocket Medical

- 6.3.8 Sterylab Srl

- 6.3.9 BPB Medica

- 6.3.10 Medex Medical device

- 6.3.11 Vigeo Srl

- 6.3.12 GIMA Italia

- 6.3.13 Tsumani Medical

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment