|

시장보고서

상품코드

1836726

아스타잔틴 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Astaxanthin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

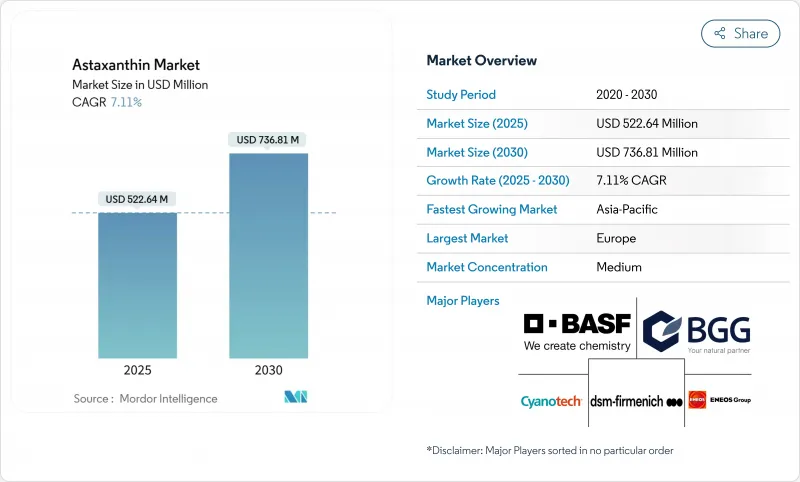

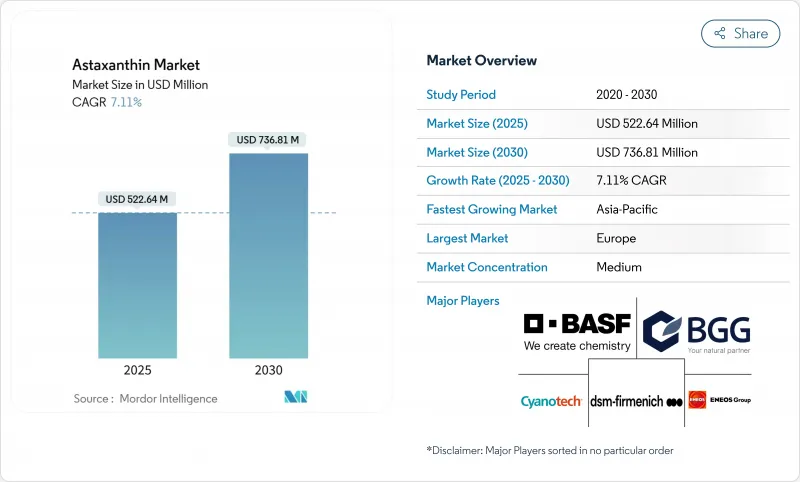

아스타잔틴 시장 규모는 2025년 5억 2,264만 달러로 추정되며, 예측 기간(2025-2030년) 동안 7.11%의 연평균 복합 성장률(CAGR)을 나타내 2030년까지 7억 3,681만 달러에 달할 것으로 예상됩니다.

세계의 아스타잔틴 시장은 그 항산화 작용, 항염증 작용, 인지 서포트 작용의 임상적 검증의 고조에 견인되어 강력한 성장 궤도를 따라가고 있습니다. 미국, 유럽, 아시아 규제기관이 식품, 보충제, 화장품에 사용하는 새로운 아스타잔틴의 형식을 계속 승인하고 있기 때문에 수요는 꾸준히 확대되고 있습니다. 주로 미세조류를 원료로 하는 천연 아스타잔틴은 그 뛰어난 생물학적 이용능력과 클린 라벨의 매력 덕분에, 신제품 발매의 견인역이 되고 있어, 오늘의 건강 지향으로 성분에 정통한 소비자의 공감을 부르고 있습니다. 비용에 민감한 동물사료 분야에서는 합성 사료가 여전히 주류를 차지하고 있지만, 혁신은 꾸준히 비용 격차를 채우고 있습니다. 미세조류 배양, 인공지능에 최적화된 광 생물반응기 시스템, 깊은 공정 용매와 같은 녹색 추출 기술의 혁신은 운영 비용을 절감할 뿐만 아니라 지속가능성과 확장성을 향상시킵니다. 이러한 진보는 천연 기능성 성분에 대한 소비자의 기호의 변화와 함께 영양 보조 식품, 기능성 식품, 프리미엄 스킨 케어에 새로운 수익원을 가져오고 있습니다. 미래성이 높고 과학적으로 뒷받침되는 웰빙 성분의 활용을 목표로 하는 기업에 있어서, 아스타잔틴은 기술 혁신, 소비자의 신뢰, 규제의 기세에 뒷받침되는 매력적인 성장 스토리를 제공합니다.

세계의 아스타잔틴 시장 동향과 인사이트

활황을 나타내는 예방 건강 관리 및 안티 에이징 동향

이 보고서는 아스타잔틴의 정기적인 섭취가 산화 스트레스 마커의 감소, 내피 기능 개선, 정신 피로 평가시 성인의 인지 능력 향상과 관련이 있음을 입증했습니다. 시장은 기업이 종합적인 웰빙 제품으로 천연 아스타크 산틴 소프트젤을 판매하고 예방 건강 솔루션에 소비자 선호도 증가를 보여줍니다. 이 포지셔닝은 아스타잔틴의 세포막을 통과하고 비타민 C에 비해 일중항 산소를 중화하는 우수한 능력에 의해 지원됩니다. 약국 및 온라인 소매업체의 판매 데이터는 소비자가 기존의 항산화제와 비교하여 프리미엄 아스타잔틴 제품에 기꺼이 더 많은 것을 지불한다는 것을 보여줍니다. 화장품 산업은 또한 광 노화의 영향을 줄이고 콜라겐 생산을 강화하도록 설계된 국소 제품에 아스타크 산틴을 통합합니다. 이러한 용도 기반의 확대는 아스타잔틴 시장에서 지속적인 연구 투자, 규제 개발 및 광범위한 소비자 채용을 촉진합니다.

천연 및 식물 유래 보충제의 인기 증가

천연 성분에 대한 수요 증가는 특히 α-리포산 보충제를 둘러싼 안전성에 대한 우려가 높아짐에 따라 유럽 전역에서 상당한 처방 변경에 대한 노력을 추진하고 있습니다. Heematococcus pluvialis(Haematococcus pluvialis)에서 추출한 아스타잔틴은 천연적이고 유전적으로 변형되지 않은 대체품이며, 합성품에 비해 혈장 농도가 높고 유지 기간이 길다는 것이 임상시험에서 나타나고 뛰어난 성능을 나타내고 있습니다. CBI(신흥 국가 수입 촉진 센터)에 따르면 천연 성분은 주로 식품 보충제, 허브 의약품, 대체 의료 치료 등 다양한 건강 용도에서 점점 대중화되고 있습니다. 이것은 아스타크 산치와 같은 천연 성분에 대한 기회입니다.

생산 비용이 천연 아스타잔틴 시장 성장을 제한

천연 아스타잔틴의 생산 비용은 여전히 높고, 다운스트림 공정은 총 생산 비용의 대부분을 차지하기 때문에 합성 대체품에 비해 가격이 높아지고 있습니다. 미세조류 바이오매스에서 아스타잔틴을 추출하고 정제하려면 복잡한 공정, 특수 장비, 관리 환경이 필요합니다. 기술적 개선으로 생산비용이 줄어들고 있지만, 가격 차이는 비용에 민감한 용도, 특히 천연 성분 수요가 증가하고 있음에도 불구하고, 합성 버전이 비용 우위를 유지하는 동물사료 시장에서 천연 아스타잔틴의 채용을 계속 제한하고 있습니다. 시장 역학은 생산 경제성과 소비자 선호도의 균형을 맞추는 지속적인 과제를 보여주며, 특히 다양한 최종 용도 부문에서 사업을 확장하고 경쟁력있는 가격 전략을 유지하는 제조업체의 능력에 영향을 미칩니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

- 조류의 양식과 추출에 있어서의 진보가 생산물의 품질 향상

- 소비자의 클린 라벨, 비유전자 재조합 성분으로의 변화

- 신흥 시장에서 소비자 의식의 한계

부문 분석

합성 아스타잔틴 부문은 2024년에 84.47%의 시장 점유율을 차지하고 양식 가공업자에게 안정적인 비용과 색상의 효력을 공급하는 확립된 화학 합성 생산 라인에 지원되었습니다. 제조 공정은 수십년동안 거의 변하지 않았으며 제조 업체에게 신뢰할 수있는 제조 방법과 표준화 된 출력 품질을 제공합니다.

헤마토코커스(Haematococcus)와 파피아(Phaffia)의 생산방법에 근거한 천연 부문은 천연 성분의 인증을 요구하는 건강·미용 제품 제조업체에 견인되어 2030년까지 연평균 복합 성장률(CAGR) 8.74%를 나타낼 것으로 예측됩니다. 조사에 따르면 천연 추출물은 항산화 활성이 높고 조직 보유력이 강화되고 안정성이 높기 때문에 고급 영양 보충제 및 스킨 케어 제품에 적합합니다.

분말 형태는 기존 캡슐, 정제, 프리믹스 생산 라인과의 호환성으로 2024년 아스타잔틴 시장의 75.55% 판매 점유율을 차지했습니다. 분말 형태는 2년간의 보존 가능 기간을 제공하며 해상 운송 시 온도 변화에도 안정성을 유지합니다. 나노에멀젼과 비드렛을 포함한 액체 부문은 냉수 분산성이 개선되어 2030년까지 연평균 복합 성장률(CAGR) 8.24%를 나타낼 것으로 예측됩니다. 제조업체는 현재 몇 초 안에 음료에 녹는 속용성 파우치를 생산하고 있으며 아스타잔틴이 기능성 미용 음료의 콜라겐과 프로바이오틱스를 보완 할 수 있습니다.

솔라비아 알가텍사는 분말의 안정성과 액체에의 응용 능력을 겸비한 2.5% 냉수 분산성 아스타잔틴 분말을 개발했습니다. 이 제형을 통해 음료 제조업체는 아스타잔틴을 제품에 배합하여 기능적 특성과 임상적 이점을 활용할 수 있습니다. 이 개발은 음료 산업에서 천연 산화 방지제에 대한 수요가 증가함에 따라 제조업체의 응용 가능성을 확대합니다. 분말의 개선된 분산 특성은 아스타잔틴의 혼입과 관련된 생산의 복잡성 및 비용을 감소시키고, 잠재적으로 다양한 음료 부문 전체에서의 채용을 증가시킵니다.

지역별 분석

유럽은 EFSA의 종합적인 안전성 평가와 유럽위원회의 아스타잔틴을 많이 포함한 성분의 신규 식품 승인 등 확립된 규제 틀에 힘입어 2024년에 32.94%의 점유율로 시장의 주도권을 유지했습니다. 이 지역의 성숙한 보충제 시장과 프리미엄 천연 건강 제품의 소비자 수용은 아스타크 산틴 채용을위한 유리한 조건을 만들고, 엄격한 품질 기준은 고순도 제형에 대한 수요를 추진하고 있습니다. 아시아태평양은 5.55%의 연평균 복합 성장률(CAGR)을 나타내 가장 급성장하는 지역으로 떠오르고 있으며, 규제 개발과 예방 의료 솔루션을 추구하는 중류 계급의 인구 확대에 힘쓰고 있습니다.

아시아태평양의 가속 성장 궤도는 아스타잔틴의 채택에 유리한 인구 동태와 규제 동향의 수렴에 기인합니다. 새로운 식품소재로서 미세조류유의 인가를 포함한 중국의 규제 근대화는 기능성 식품에의 응용에 대한 장벽을 없애는 한편, 이 나라의 확대하는 중간층은 프리미엄 건강 제품을 요구하고 있습니다. 일본의 기능성표시 식품제도는 건강강조표시의 입증을 간소화하고, 제조업체가 아스타잔틴의 이점을 소비자에 의해 간단하게 전달할 수 있기 때문에 시장의 대폭적인 성장을 견인하고 있습니다. 이 지역에서는 고령화가 진행되고 있기 때문에 인지 건강이나 안티 에이징의 용도에 대한 큰 수요가 생기는 한편, 확립된 양식 산업이 복수의 용도로 아스타잔틴을 채용하는 기반을 제공합니다.

북미는 성숙시장으로, FDA에 의한 아스타잔틴 제제의 GRAS 승인이 시장 진입을 가능하게 하고 있지만, 기존의 항산화 성분과의 경쟁이 성장을 제한하고 있습니다. 임상 검증에 중점을 둔 이 지역은 아스타잔틴의 연구 증거 확대를 지원합니다. 깨끗한 라벨로 지속 가능한 성분에 대한 소비자의 선호도는 비용이 높음에도 불구하고 천연 아스타크 산틴 수요를 촉진합니다. 남미, 중동 및 아프리카는 아스타잔틴의 건강상의 이점에 대한 의식 증가로 보충 및 양식 응용 분야에서 점차 채용을 촉진하고 신흥 시장의 잠재력을 보여줍니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 예방의료와 안티에이징 동향의 활황

- 천연 및 식물 유래 보충제의 인기 증가

- 조류의 양식과 추출의 진보에 의한 생산 품질의 향상

- 클린 라벨, 비유전자 재조합 성분으로의 소비자 변화

- 지속 가능하고 환경 친화적인 영양 성분에 주목

- 건강 강조 표시를 부가한 기능성 식음료의 확대

- 시장 성장 억제요인

- 생산 비용의 한계

- 신흥 시장에서의 한정된 소비자 의식

- 식품 혼입에 대한 우려 증가

- 시장 성장을 억제하는 엄격한 정부 규제

- 공급망 분석

- 규제의 전망

- Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모·성장 예측(금액)

- 유래별

- 천연

- 합성

- 형태별

- 분말

- 액체

- 생산 방법별

- 미세조류 배양

- 화학 합성

- 발효

- 용도별

- 식음료

- 영양보조식품

- 동물사료

- 퍼스널케어 및 화장품

- 의약품

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미

- 유럽

- 영국

- 독일

- 스페인

- 프랑스

- 이탈리아

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 랭킹 분석

- 기업 프로파일

- BASF SE

- dsm-firmenich

- Fuji Chemical Industry/AstaReal

- Cyanotech Corporation

- Beijing Gingko Group(BGG)

- Algatech Ltd.

- Algalif Iceland ehf.

- Divi's Laboratories Ltd.

- ENEOS Holdings Inc.

- Biogenic Co. Ltd.

- Otsuka Holdings Co. Ltd.

- INNOBIO Ltd.

- Yunnan Alphy Biotech Co.

- NOW Health Group Inc.

- Archer-Daniels-Midland Company

- Givaudan Active Beauty

- Kemin Industries

- Evonik Nutrition & Care

- Valensa International

- Atacama Bio(Northeastern Biotech)

제7장 시장 기회와 전망

KTH 25.10.28The Astaxanthin Market size is estimated at USD 522.64 million in 2025, and is expected to reach USD 736.81 million by 2030, at a CAGR of 7.11% during the forecast period (2025-2030).

The global astaxanthin market is witnessing a powerful growth trajectory, driven by increasing clinical validation of its antioxidant, anti-inflammatory, and cognitive-support properties. As regulatory bodies across the U.S., Europe, and Asia continue approving new astaxanthin formats for use in food, supplements, and cosmetics, demand is steadily expanding. Natural astaxanthin, sourced primarily from microalgae, is gaining traction in new product launches, thanks to its superior bioavailability and clean-label appeal, which resonates well with today's health-conscious and ingredient-savvy consumers. While synthetic variants continue to dominate the cost-sensitive animal feed segment, technological innovations are steadily bridging the cost gap. Breakthroughs in microalgae cultivation, AI-optimised photobioreactor systems, and green extraction technologies like deep eutectic solvents are not only reducing operational costs but also enhancing sustainability and scalability. These advances, combined with shifting consumer preferences toward natural, functional ingredients, are opening new revenue streams across dietary supplements, functional foods, and premium skincare. For businesses looking to tap into a high-potential, science-backed wellness ingredient, astaxanthin offers a compelling growth story anchored in innovation, consumer trust, and regulatory momentum.

Global Astaxanthin Market Trends and Insights

Booming Preventive Healthcare and Anti-Aging Trends

Research demonstrates that regular astaxanthin consumption correlates with reduced oxidative-stress markers, improved endothelial function, and enhanced cognitive performance in adults during mental-fatigue assessments. The market shows increasing consumer preference for preventive health solutions, with companies marketing natural astaxanthin softgels as comprehensive wellness products. This positioning is supported by astaxanthin's superior ability to cross cell membranes and neutralize singlet oxygen compared to vitamin C. Sales data from pharmacies and online retailers indicates consumers willingly pay more for premium astaxanthin products compared to conventional antioxidants. The cosmetics industry has also incorporated astaxanthin in topical products designed to reduce photo-aging effects and enhance collagen production. This expanding application base drives continued research investment, regulatory development, and broader consumer adoption in the astaxanthin market.

Growing Popularity of Natural and Plant-Based Supplements

The growing demand for natural ingredients has driven significant reformulation efforts across Europe, particularly following heightened safety concerns surrounding alpha-lipoic acid supplements. Astaxanthin extracted from Haematococcus pluvialis offers a natural, non-GMO alternative that demonstrates superior performance, with clinical studies showing higher plasma concentration and longer retention periods compared to synthetic versions. According to the CBI (Centre for the Promotion of Imports from developing countries), natural ingredients have become increasingly prevalent in various health applications, primarily in food supplements, herbal medicinal products, and alternative medicine treatments . This translates into opportunities for natural ingredients like astaxanthin

Production Costs Limit Natural Astaxanthin Market Growth

Natural astaxanthin production costs remain high, with downstream processing representing a significant majority of total production expenses, resulting in higher prices compared to synthetic alternatives. The extraction and purification of astaxanthin from microalgae biomass requires complex processes, specialized equipment, and controlled environments. Although technological improvements are reducing production costs, the price difference continues to restrict natural astaxanthin adoption in cost-sensitive applications, especially in animal feed markets where synthetic versions maintain their cost advantage despite increasing demand for natural ingredients. The market dynamics indicate a persistent challenge in balancing production economics with growing consumer preferences, particularly affecting manufacturers' ability to scale operations and maintain competitive pricing strategies in various end-use segments.

Other drivers and restraints analyzed in the detailed report include:

- Advancement in Algae Farming and Extraction Boosting Output Quality

- Consumer Shift Towards Clean-Label, Non-GMO Ingredients

- Limited Consumer Awareness in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Synthetic astaxanthin segment held a 84.47% market share in 2024, supported by established chemical synthesis production lines that supply aquaculture processors with consistent costs and color potency. The manufacturing process has remained largely unchanged for decades, providing manufacturers with reliable production methods and standardized output quality.

The natural segment, based on Haematococcus and Phaffia production methods, is expected to grow at a CAGR of 8.74% through 2030, driven by wellness and beauty product manufacturers seeking natural ingredient certifications. Research shows that natural extracts offer higher antioxidant activity, enhanced tissue retention, and greater stability, making them suitable for premium dietary supplements and skincare products.

Powder formats accounted for 75.55% revenue share of the Astaxanthin market in 2024, driven by their compatibility with existing capsule, tablet, and premix production lines. The powder form offers a two-year shelf life and maintains stability during maritime shipping temperature variations. The liquid segment, including nano-emulsions and beadlets, is projected to grow at an 8.24% CAGR through 2030, following improvements in cold-water dispersibility. Manufacturers now produce quick-dissolving sachets that integrate into beverages within seconds, enabling astaxanthin to complement collagen and probiotics in functional beauty drinks.

Solabia-Algatech developed a 2.5% cold-water-dispersible astaxanthin powder that combines powder stability with liquid application capabilities. This formulation enables beverage manufacturers to incorporate astaxanthin into their products, leveraging its functional properties and clinical benefits. The development addresses the growing demand for natural antioxidants in the beverage industry and expands the application possibilities for manufacturers. The improved dispersibility characteristics of the powder reduce production complexities and costs associated with astaxanthin incorporation, potentially increasing its adoption across various beverage segments.

The Astaxanthin Market Report is Segmented by Nature (Natural and Synthetic), Form (Powder and Liquid), Production Method (Microalgae Cultivation, Chemical Synthesis, and Fermentation), Application (Food and Beverage, Dietary Supplement, Animal Feed, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe maintains market leadership with 32.94% share in 2024, supported by established regulatory frameworks including EFSA's comprehensive safety assessments and the European Commission's novel food approvals for astaxanthin-rich ingredients. The region's mature supplement market and consumer acceptance of premium natural health products create favorable conditions for astaxanthin adoption, while stringent quality standards drive demand for high-purity formulations. Asia-Pacific emerges as the fastest-growing region at 5.55% CAGR, propelled by regulatory developments and expanding middle-class populations seeking preventive healthcare solutions.

Asia-Pacific's accelerated growth trajectory stems from converging demographic and regulatory trends that favor astaxanthin adoption. China's regulatory modernization, including the approval of microalgae oil as a new food material, removes barriers to functional food applications while the country's expanding middle class seeks premium health products. Japan's Foods with Function Claims system has simplified health claim substantiation, driving significant market growth as manufacturers can more easily communicate astaxanthin's benefits to consumers. The region's aging population creates substantial demand for cognitive health and anti-aging applications, while established aquaculture industries provide a foundation for astaxanthin adoption across multiple applications.

North America represents a mature market where FDA GRAS approvals for astaxanthin formulations enable market access, though competition from established antioxidant ingredients limits growth. The region's focus on clinical validation supports astaxanthin's expanding research evidence. Consumer preferences for clean-label and sustainable ingredients drive demand for natural astaxanthin, despite higher costs. South America, Middle East, and Africa show emerging market potential, with increasing awareness of astaxanthin's health benefits driving gradual adoption in supplements and aquaculture applications.

- BASF SE

- dsm-firmenich

- Fuji Chemical Industry / AstaReal

- Cyanotech Corporation

- Beijing Gingko Group (BGG)

- Algatech Ltd.

- Algalif Iceland ehf.

- Divi's Laboratories Ltd.

- ENEOS Holdings Inc.

- Biogenic Co. Ltd.

- Otsuka Holdings Co. Ltd.

- INNOBIO Ltd.

- Yunnan Alphy Biotech Co.

- NOW Health Group Inc.

- Archer-Daniels-Midland Company

- Givaudan Active Beauty

- Kemin Industries

- Evonik Nutrition & Care

- Valensa International

- Atacama Bio (Northeastern Biotech)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Booming in Preventive Heathcare and Ant-Aging Trends

- 4.2.2 Growing Popularity of Natural and Plant-Based Supplements

- 4.2.3 Advancement in Algae Farming and Extraction Boosting Output Quality

- 4.2.4 Consumer Shift Towards Clean-Label, Non-GMO Ingredients

- 4.2.5 Focus on Sustaniable and Eco-Friendly Nutritional Ingredients

- 4.2.6 Expansion of Functional Food and Beverage with Added Health Claims

- 4.3 Market Restraints

- 4.3.1 Production Costs Limit

- 4.3.2 Limited Consumer Awareness in Emerging Markets

- 4.3.3 Growing Concerns Over Food Adulteration

- 4.3.4 Stringent Government Regulation to Retrain the Market Growth

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE & GROWTH FORECASTS (VALUE)

- 5.1 By Nature

- 5.1.1 Natural

- 5.1.2 Synthetic

- 5.2 By Form

- 5.2.1 Powder

- 5.2.2 Liquid

- 5.3 By Production Method

- 5.3.1 Microalgae Cultivation

- 5.3.2 Chemical Synthesis

- 5.3.3 Fermentation

- 5.4 By Application

- 5.4.1 Food and Beverage

- 5.4.2 Dietary Supplement

- 5.4.3 Animal Feed

- 5.4.4 Personal Care and Cosmetics

- 5.4.5 Pharmaceuticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 Spain

- 5.5.2.4 France

- 5.5.2.5 Italy

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 dsm-firmenich

- 6.4.3 Fuji Chemical Industry / AstaReal

- 6.4.4 Cyanotech Corporation

- 6.4.5 Beijing Gingko Group (BGG)

- 6.4.6 Algatech Ltd.

- 6.4.7 Algalif Iceland ehf.

- 6.4.8 Divi's Laboratories Ltd.

- 6.4.9 ENEOS Holdings Inc.

- 6.4.10 Biogenic Co. Ltd.

- 6.4.11 Otsuka Holdings Co. Ltd.

- 6.4.12 INNOBIO Ltd.

- 6.4.13 Yunnan Alphy Biotech Co.

- 6.4.14 NOW Health Group Inc.

- 6.4.15 Archer-Daniels-Midland Company

- 6.4.16 Givaudan Active Beauty

- 6.4.17 Kemin Industries

- 6.4.18 Evonik Nutrition & Care

- 6.4.19 Valensa International

- 6.4.20 Atacama Bio (Northeastern Biotech)