|

시장보고서

상품코드

1842420

정형외과 소프트웨어 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Orthopedic Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

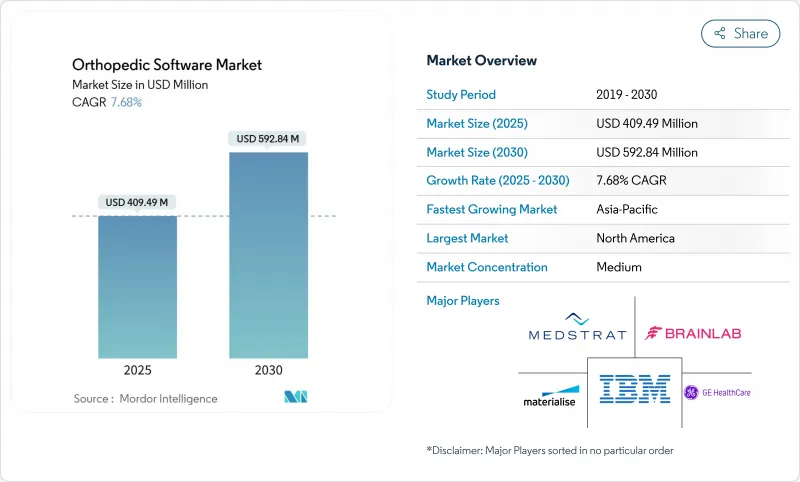

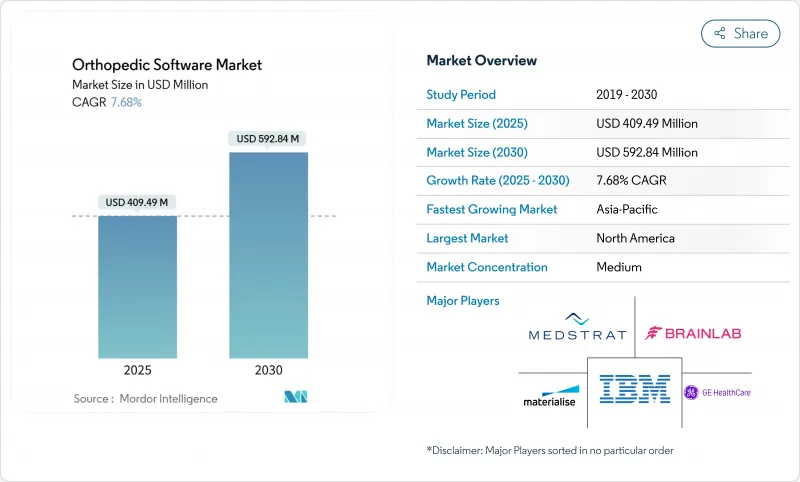

정형외과 소프트웨어 시장 규모는 2025년에 4억 949만 달러로 추정되며, 예측기간(2025-2030년)의 CAGR은 7.68%를 나타내, 2030년에는 5억 9,284만 달러에 달할 것으로 예상됩니다.

정형외과 의료의 광범위한 디지털화, 인공지능(AI)의 급속한 성숙, 상호 운용성 규칙의 시행에 의해 전문 클리닉이나 대규모 병원 시스템은 화상 처리, 수술 계획, 수익 사이클 업무를 관리하는 통합 소프트웨어 에코시스템으로 향하고 있습니다. AI 주도의 의사결정 지원과 안전한 클라우드 구축을 제공하는 벤더는 수술실의 시간 단축, 재수술률의 저하, 새로운 가치에 근거한 상환 흐름의 획득을 목표로 하는 클리닉에서의 수요를 계속 획득하고 있습니다. 고소득국가의 고령화, 외래 수술 센터(ASC)의 급증, 로봇 지침의 이용 확대가 주요 하위 부문의 2자리 성장을 더욱 지원하고 있습니다. 하드웨어 메이저가 소프트웨어 틈새 분야에 진입함에 따라 경쟁이 심화되고 있지만 시장이 단편화되어 중견 개발자는 틈새 혁신과 지역 제휴를 통해 점유율을 확대하고 있습니다.

세계의 정형외과 소프트웨어 시장 동향과 인사이트

고령화가 골관절염과 골절의 사례 수를 밀어 올립니다.

세계의 65세 이상의 인구는 계속 확대되고 있으며, 수작업 워크플로우에 부담을 주는 변성 관절 질환과 골절 발생률을 밀어 올리고 있습니다. 디지털 템플리팅은 수술 시간을 15-20% 단축하여 임플란트의 매립 정밀도를 향상시켜 외과의사가 결과를 손상시키지 않고 더 많은 경우에 대응할 수 있도록 합니다. AI를 활용한 영상 진단을 통해 골 병변의 조기 발견이 90% 이상의 진단 정확도를 달성하고 장기적인 비용 압박을 완화하는 예방적 개입이 가능합니다. 통합 수익주기 모듈은 복잡한 노인 의료 청구를 간소화하고 지불자의 조사에 직면하는 클리닉의 마진 확보를 개선합니다.

외래 및 저침습 성형 수술로의 급속한 이동

ASC의 수술 건수는 매년 6.9% 증가하고 있으며, 정형외과의 외래 수술 건수는 지난 10년간 13% 증가할 것으로 예측되고 있습니다. 이러한 환경에서는 신속한 회전, 소규모 수술실 및 엄격한 자본 예산을 지원하는 클라우드 네이티브 소프트웨어가 필요합니다. CMS에 의한 어깨 관절 치환술 외래 환자에 대한 상환 승인은 고급 계획 도구의 도입을 가속화하고 있습니다. 현재 ASC의 54.6%만이 인증 EHR을 운용하고 있으며 전문 벤더에게 대응할 수 있는 시장이 큰 것을 보여주고 있습니다.

정형외과 정보학 및 이미지 IT 전문가 부족

고급 EHR 도입을 위해서는 세계 15만 3,114명의 IT 전임자를 추가해야 하지만, 연수 파이프라인은 수요를 따라잡지 못하고 있습니다. 현지 전문 클리닉은 공급업체의 서비스에 의존하기 때문에 도입 비용이 상승하고 일정이 장기화되고 있습니다. 따라서 도입, 교육 및 관리 서비스를 번들하는 공급업체가 전략적 이점을 얻고 있습니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

- EHR/PACS 상호운용성의 의무화

- 3D 디지털 템플릿의 임플란트 수정율 저감에의 효과의 증명

- 랜섬웨어 사건 이후 사이버 보험료 상승

부문 분석

디지털 템플리팅은 재수술률을 낮추고 수술실에서의 작업 시간을 단축하는 능력이 입증된 것을 반영했으며, 2024년 정형외과 소프트웨어 시장 점유율은 35.83%였습니다. 이 하위 부문은 과거의 사례에서 학습한 AI 이미지 세분화 모듈이 표준화된 임플란트 플랜을 제공하여 외과의사 간의 편차를 줄일 수 있다는 장점이 있습니다. 정형외과 PACS의 CAGR은 9.71%를 나타낼 것으로 예측되고 있으며, 이는 MRI와 CT의 증례 수 증가와 필름 폐지를 위한 규제의 움직임에 의한 것입니다. 통합 EHR은 운동기 워크플로우에 맞는 전문적인 의사결정 지원을 통합합니다. 재활의 이정표를 임상 기록과 동기화하는 환자 관리 앱은 피드백 루프를 닫고 일괄 지불 규정 준수를 지원합니다.

보완적인 모듈은 스케줄링, 이미지 처리 및 OR 재고 관리를 통합하는 개방형 API 백본에 집계됩니다. 공급업체는 현재 3D 렌더링을 위한 클라우드 기능을 배포하고 로컬 서버에서 계산 워크로드를 오프로드하고 있습니다. 디지털 템플릿이 구조화된 데이터를 로봇 콘솔로 내보내면 수술 중 조정이 줄어들고 수술 후 정렬 점수가 향상됩니다. 템플릿화 및 PACS와 관련된 정형외과 소프트웨어 시장 규모는 유행기에 연기된 선택 사례의 백로그에 지지되어 8-9%의 페이스로 안정적으로 확대될 것으로 예측됩니다.

클라우드 도입은 2024년에는 정형외과 소프트웨어 시장의 59.32%를 차지했고, 2030년까지의 CAGR은 11.95%를 나타낼 전망입니다. 구독 가격은 ASC의 현금 흐름과 일치하며 소규모 클리닉은 많은 자본 지출에서 벗어날 수 있습니다. 공급업체는 다운타임 없는 업그레이드와 암호화된 에지 간 동기화를 강조하고 대기 시간과 데이터 주권에 대한 이전 우려를 극복합니다. 하이브리드 모델은 AI 모델을 교육하기 위해 클라우드 분석을 사용하면서 기밀성이 높은 연구 이미지를 현장에서 보관하는 학술 센터에 계속 적합한 모델입니다.

광역 대역폭이 제한되거나 데이터 보호 규칙이 오프사이트 스토리지를 금지하는 경우 On-Premise 시스템이 유지됩니다. 이러한 경우에도 공급업체는 데이터 세트를 재해 복구 클라우드로 미러링하는 모듈식 게이트웨이를 제공합니다. 퍼블릭 클라우드 제공업체가 HIPAA 및 GDPR(EU 개인정보보호규정) 인증을 획득함에 따라 마이그레이션을 보류한 기업도 마이그레이션할 것으로 예측됩니다. 클라우드 소프트웨어로 인한 정형외과 소프트웨어 시장 규모는 현재의 채용 곡선이 유지되면 2030년까지 3억 5,000만 달러를 초과할 가능성이 높습니다.

지역별 분석

북미는 확립된 상환경로와 성숙한 클라우드 인프라로 2024년 총 매출의 39.85%를 차지했습니다. 미국 메디케어 정책은 품질 지표를 지원하는 디지털 문서에 보답하는 것으로, 클리닉에 통합 솔루션을 도입하도록 촉구하고 있습니다. 캐나다에서는 전자 데이터 공유가 주에 의해 의무화되고 수요가 더욱 높아지고 있습니다.

아시아태평양의 CAGR은 13.15%를 나타낼 전망입니다. 중국의 건강한 중국 청사진은 디지털 건강의 조종사 사업에 자금을 제공하고 지방 병원을 조기 도입자에게 자리 매김하고 있습니다. 일본에서는 외과 수술의 노동력 부족을 보완하기 위해 로봇 공학과 AI가 활용되고 인도에서는 관민 파트너십이 제3차 외상 센터의 클라우드 EHR에 자금을 제공합니다. 지역마다 다른 다양성은 다양한 개인정보보호법에 따라 모듈화되고 언어로 현지화된 플랫폼을 선호합니다.

유럽의 꾸준한 도입은 독일이 견인하고 있으며 연방 정부의 보조금은 GDPR(EU 개인정보보호규정)의 엄격한 규정을 준수하는 클리닉에서 정형외과 디지털화를 지원합니다. 미국의 NHS 상호 운용성 프로그램에서는 정형외과 소개에 FHIR 메시징이 지정되어 있으며 입증된 데이터 교환 워크플로가 있는 공급업체가 선행합니다. 프랑스는 외래 방사선과에서 정형외과 병동으로 실시간 이미지 라우팅을 필요로하는 협력 관리 네트워크에 혁신 예산을 돌리고 있습니다. 이 블록 전체에서 재수술률이 낮다는 증거는 투자 사인 오프에 매우 중요하며 데이터가 풍부한 공급업체는 유리한 입장에 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 고령화에 의한 변형성 관절증 및 골절 증례 증가

- 외래 및 저침습 정형외과 수술로의 급속한 변화

- EHR/PACS 상호운용성의 의무화

- 임플란트의 재치환율을 삭감하는 것이 증명된 3D 디지털 템플리팅

- AI 자동 템플릿화에 의해 멸균 트레이의 재고를 삭감

- 클리닉의 새로운 SaaS 수익을 이끌어내는 정형외과 소프트웨어 API 마켓플레이스

- 시장 성장 억제요인

- 정형외과 정보학 및 이미지 IT 전문가 부족

- 높은 자본 비용과 시스템 이행시의 워크플로우 중단

- 클라우드 데이터 호스팅의 복잡한 HIPAA/GDPR(EU 개인정보보호규정) 규정 준수

- 랜섬웨어 사건 후 사이버 보험료 상승

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모·성장 예측(단위 : 달러)

- 제품 유형별

- 디지털 템플릿/수술 전 계획

- 정형외과 EHR

- 정형외과 진료 관리

- 정형외과 PACS

- 수익 주기 관리

- 기타 소프트웨어

- 배포 모드별

- 클라우드/웹 기반

- On-Premise

- 용도별

- 정형외과 수술

- 골절 관리

- 관절 치환술

- 소아 평가

- 기타 용도

- 최종 사용자별

- 병원

- 외래 수술 센터(ASC)

- 정형외과 클리닉

- 학술 및 연구 기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Athenahealth

- Brainlab

- CureMD Healthcare

- GE Healthcare

- Greenway Health

- IBM(Merge Healthcare)

- Materialise

- Medstrat

- NextGen Healthcare

- Breg

- mediCAD Hectec

- Rayence

- Stryker

- Zimmer Biomet

- Smith & Nephew

- McKesson

- HealthFusion

- Allscripts

- Medhost

- Touch Surgery

제7장 시장 기회와 전망

KTH 25.10.28The Orthopedic Software Market size is estimated at USD 409.49 million in 2025, and is expected to reach USD 592.84 million by 2030, at a CAGR of 7.68% during the forecast period (2025-2030).

Widespread digitization of orthopedic care, the rapid maturation of artificial intelligence (AI), and the enforcement of interoperability rules are pushing specialty clinics and large hospital systems toward integrated software ecosystems that manage imaging, surgical planning, and revenue-cycle tasks. Vendors that provide AI-driven decision support and secure cloud deployment continue to capture demand from practices looking to shorten operating-room time, lower revision rates, and tap new value-based reimbursement streams. Aging populations in high-income countries, surging ambulatory surgery center (ASC) volumes, and expanding use of robotic guidance further sustain double-digit growth in key sub-segments. Competitive intensity is rising as hardware majors enter software niches, yet the market remains fragmented, allowing mid-tier developers to gain share through niche innovations and regional partnerships.

Global Orthopedic Software Market Trends and Insights

Aging Population Boosting Osteoarthritis & Fracture Case-Load

Global populations aged 65+ continue to expand, driving up degenerative joint disease and fracture incidence that strain manual workflows. Digital templating decreases surgical time by 15-20% and improves implant placement accuracy, helping surgeons handle higher caseloads without compromising outcomes. AI-driven imaging reaches over 90% diagnostic accuracy for early bone pathology detection, enabling proactive interventions that ease long-term cost pressures. Integrated revenue-cycle modules streamline complex geriatric billing, improving margin security for practices facing payer scrutiny.

Rapid Shift to Ambulatory & Minimally-Invasive Orthopedic Surgery

ASC volumes are climbing at 6.9% annually, with orthopedic outpatient procedures projected to grow 13% this decade. These settings require cloud-native software that supports rapid turnover, small operating suites, and tight capital budgets. CMS approval of shoulder replacements for outpatient reimbursement accelerates adoption of advanced planning tools. Only 54.6% of ASCs presently operate certified EHRs, signaling a sizable addressable market for specialty vendors.

Shortage of Orthopedic Informatics & Imaging IT Specialists

Advanced EHR rollouts require up to 153,114 additional IT full-time equivalents worldwide, yet training pipelines lag demand. Specialty clinics in rural settings depend on vendor services, elevating deployment cost and elongating timelines. Vendors that bundle implementation, training, and managed services thus gain a strategic edge.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory EHR / PACS Interoperability

- 3-D Digital Templating Proven to Cut Implant Revision Rates

- Soaring Cyber-Insurance Premiums after Ransomware Incidents

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digital templating held a 35.83% orthopedic software market share in 2024, reflecting its proven ability to lower revision rates and trim operating-room minutes. The sub-segment benefits from AI image-segmentation modules that learn from prior cases, yielding standardized implant plans and reducing inter-surgeon variability. Orthopedic PACS is projected to post a 9.71% CAGR, fueled by climbing MRI and CT volumes and regulatory moves to eliminate film. Revenue-cycle tools remain essential as value-based contracts rise, while integrated EHRs embed specialty decision support tailored to musculoskeletal workflows. Patient-engagement apps that sync rehab milestones into the clinical record close the feedback loop, supporting bundled-payment compliance.

Complementary modules converge around an open-API backbone that unifies scheduling, imaging, and OR inventory control. Vendors now deploy cloud functions for 3-D rendering, offloading compute workload from local servers. As digital templating exports structured data to robotics consoles, intra-operative adjustments shrink and post-operative alignment scores improve. The Orthopedic software market size tied to templating and PACS is forecast to expand at a steady 8-9% pace, underpinned by a backlog of elective cases deferred during pandemic years.

Cloud deployments comprised 59.32% of the orthopedic software market in 2024 and are tracking an 11.95% CAGR to 2030. Subscription pricing aligns with ASC cashflows and shields smaller clinics from large capital outlays. Vendors emphasize zero-downtime upgrades and encrypted edge-to-cloud sync, overcoming earlier fears of latency and data sovereignty. Hybrid models remain relevant for academic centers that house sensitive research images onsite while using cloud analytics for AI model-training.

On-premise systems persist where wide-area bandwidth is limited or data guardianship rules forbid offsite storage. Even here, suppliers offer modular gateways that mirror datasets to disaster-recovery clouds. As public cloud providers win HIPAA and GDPR attestations, holdouts are expected to convert. The Orthopedic software market size attributed to cloud software will likely exceed USD 350 million by 2030 if current adoption curves hold.

The Orthopedic Software Market Segments the Industry Into by Product Type (Digital Templating / Pre-Operative Planning, Orthopedic EHR, and More), Mode of Delivery (Cloud/Web Based, and More), Application (Orthopedic Surgery, and More), End User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 39.85% of total revenue in 2024 thanks to established reimbursement pathways and mature cloud infrastructure. U.S. Medicare policies reward digital documentation that supports quality metrics, encouraging practices to adopt integrated solutions. Canada's provincial mandates for electronic data sharing further entrench demand, and cross-border vendor relationships ease technology transfers.

Asia-Pacific is registering the strongest 13.15% CAGR. China's Healthy China blueprint funds digital health pilots, positioning provincial hospitals as early adopters. Japan utilizes robotics and AI to offset surgical labor shortages, while India's public-private partnerships finance cloud EHRs in tertiary trauma centers. Regional heterogeneity favors modular, language-localised platforms that comply with divergent privacy statutes.

Europe's steady adoption is led by Germany, where federal grants subsidize orthopedic digitization in clinics complying with stringent GDPR controls. The U.K.'s NHS Interoperability program specifies FHIR messaging for orthopedic referrals, giving vendors with proven data-exchange workflows a head start. France channels innovation budgets toward coordinated care networks that require real-time image routing from outpatient radiology to orthopedic wards. Across the bloc, evidence of lower revision rates is pivotal to investment sign-off, placing data-rich suppliers in an advantageous position.

- Athenahealth

- Brain Lab

- CureMD Healthcare

- GE Healthcare

- Greenway Health

- IBM (Merge Healthcare)

- Materialise

- Medstrat

- NextGen Healthcare

- Breg

- mediCAD Hectec

- Rayence

- Stryker

- Zimmer Biomet

- Smiths Group

- Mckesson

- HealthFusion

- Allscripts

- Medhost

- Touch Surgery

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Population Boosting Osteoarthritis & Fracture Case-Load

- 4.2.2 Rapid Shift to Ambulatory & Minimally-Invasive Orthopedic Surgery

- 4.2.3 Mandatory EHR / PACS Interoperability

- 4.2.4 3-D Digital Templating Proven to Cut Implant Revision Rates

- 4.2.5 AI Auto-Templating Reduces Sterile Tray Inventory

- 4.2.6 Ortho-Software API Marketplaces Unlocking New Saas Revenue for Clinics

- 4.3 Market Restraints

- 4.3.1 Shortage of Orthopedic Informatics & Imaging IT Specialists

- 4.3.2 High Capital Cost and Workflow Disruption During System Migration

- 4.3.3 Complex HIPAA / GDPR Compliance for Cloud Data Hosting

- 4.3.4 Soaring Cyber-Insurance Premiums after Ransomware Incidents

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Digital Templating / Pre-operative Planning

- 5.1.2 Orthopedic EHR

- 5.1.3 Orthopedic Practice Management

- 5.1.4 Orthopedic PACS

- 5.1.5 Revenue Cycle Management

- 5.1.6 Other Software

- 5.2 By Mode of Delivery

- 5.2.1 Cloud / Web-based

- 5.2.2 On-premise

- 5.3 By Application

- 5.3.1 Orthopedic Surgery

- 5.3.2 Fracture Management

- 5.3.3 Joint Replacement

- 5.3.4 Pediatric Assessment

- 5.3.5 Other Applications

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Orthopedic Clinics

- 5.4.4 Academic & Research Institutes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 Athenahealth

- 6.3.2 Brainlab

- 6.3.3 CureMD Healthcare

- 6.3.4 GE Healthcare

- 6.3.5 Greenway Health

- 6.3.6 IBM (Merge Healthcare)

- 6.3.7 Materialise

- 6.3.8 Medstrat

- 6.3.9 NextGen Healthcare

- 6.3.10 Breg

- 6.3.11 mediCAD Hectec

- 6.3.12 Rayence

- 6.3.13 Stryker

- 6.3.14 Zimmer Biomet

- 6.3.15 Smith & Nephew

- 6.3.16 McKesson

- 6.3.17 HealthFusion

- 6.3.18 Allscripts

- 6.3.19 Medhost

- 6.3.20 Touch Surgery

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment