|

시장보고서

상품코드

1842441

실험실 정보 관리 시스템 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Laboratory Information Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

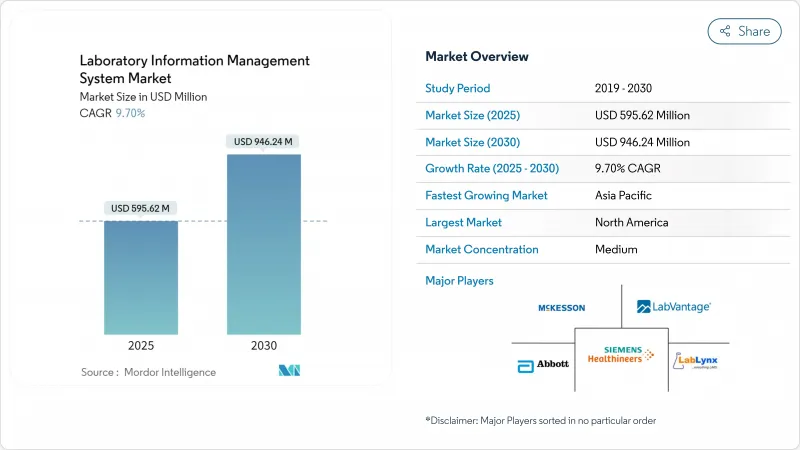

실험실 정보 관리 시스템 시장 규모는 2025년에 5억 9,562만 달러에 이르고, CAGR 9.7%를 나타내 2030년에는 9억 4,624만 달러에 달할 것으로 예상됩니다.

이 기세는 엔드 투 엔드 데이터 추적성이 규제 검사의 핵심을 차지하게 된 연구 및 품질 중심의 실험실에서 지속적인 디지털화로 탄생했습니다. 원시 분석 데이터를 의사 결정 가능한 인사이트으로 변환하고 과학자를 반복적인 큐레이션 작업으로부터 해방하는 인공지능 워크플로우도 성장의 혜택을 누리고 있습니다. 유행 시대의 비중앙 집권화로 인한 원격 샘플 모니터링에 대한 수요 증가는 모바일 액세스, 자동 CoC 및 실시간 분석을 제공하는 플랫폼에 투자를 집중시키고 있습니다. LIMS, 과학 데이터 관리, 전자연구노트(ELN) 등을 통합 클라우드 제품에 번들하는 공급자는 사일로에 묶인 워크플로우를 제거하여 채택을 계속 확대하고 있습니다. 마지막으로, 유전체, 바이오뱅크, 세포 치료 시료의 양이 급속히 증가함에 따라 수집부터 장기 보존까지 데이터 무결성을 보장하는 시스템의 가치 제안이 강화되었습니다.

세계의 실험실 정보 관리 시스템 시장 동향 및 인사이트

의약품 및 바이오테크놀러지 R&D 파이프라인의 급성장

세계의 의약품 개발 프로그램은 현재 20,000을 넘어 2020년에 비해 38% 증가하고 있습니다. 새로운 분자가 생성될 때마다 실험실의 데이터 양이 증가하고 컨텍스트화 및 감사 추적을 자동화하는 확장 가능한 LIMS의 필요성이 증가하고 있습니다. AI에 의한 이상치 검출 기능을 갖춘 플랫폼은 품질 관리 실험실의 데이터 검토 사이클을 43% 단축하고, 분석가의 능력을 해방하고 배치 릴리스를 가속화하고 있습니다. LIMS와 전자 노트북 및 과학 데이터 허브와의 완벽한 통합은 정보 장벽을 제거하여 학제 간 팀이 발견에서 확장까지 데이터 세트를 수동으로 내보내지 않고도 쿼리할 수 있도록 합니다. 이 기능은 GO/NO GO의 의사결정을 가속화하고 전반적인 개발 기간을 단축하는 적응형 테스트 설계를 지원합니다.

바이오뱅킹에 대한 수요 증가

정밀의료 프로그램의 70% 이상은 동의한 샘플을 수십년동안 보호하는 바이오 리포지토리에 의존합니다. 최신 시스템은 IoT 지원 냉동고 모니터링과 온도 상승을 피하는 이벤트 중심 경보를 결합합니다. 블록체인에 지지된 체인 오브 캐스트디는 생산 환경에 들어가고 있으며 사용권이 기증자의 동의에 직접 링크하는 유전자 치료 샘플에 있어서 중요한 불변의 증명 로그를 제공합니다. 이러한 고급 기능은 LIMS를 수동 기록 관리자로부터 시료 무결성을 보호하는 적극적인 보호자로 향상시킵니다.

높은 총 소유 비용과 장기적인 검증

기업 도입은 라이선스 수수료가 100만 달러를 초과할 수 있으며 6-9개월의 검증 기간이 필요하기 때문에 투자 회수가 지연됩니다. 버몬트가 있는 공중보건연구소는 사용자 정의와 유지보수에 170만 달러를 지출했다고 기록하고 있습니다. 구독 가격 SaaS 옵션은 자본 지출을 줄이는 것, 인프라 아웃소싱에 소극적인 보수적 품질 보증 팀에 직면하고 있습니다. 벤더는 자격 증명주기를 단축하는 템플릿과 평생 비용에 상한을 제공하는 관리 서비스 계약의 번들로 대응하고 있습니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

- AI를 활용한 유전체 검사 워크플로우

- 분산형 임상시험의 급속한 확대

- 정밀농업 토양 마이크로바이옴 분석

- 데이터 보안 및 주권에 대한 우려

- 생물 정보학 인력 부족으로 인한 고급 LIMS 확산 지연

부문 분석

실험실 정보 관리 시스템 시장은 2024년에 52%의 수익을 차지하는 서비스를 기록했고 실험실이 검증, 통합 및 지속적인 개선을 위해 외부 전문 지식에 의존하고 있음을 강조했습니다. 이러한 계약은 수년에 걸친 경우가 많으며, 규제 업데이트 및 새로운 장비로 워크플로우가 진화할 수 있도록 보장합니다. 이와 병행하여 클라우드 네이티브 구독 수요도 CAGR 10.8%를 나타내 가속화되고 있습니다. 이는 유연한 스케일링과 자동 기능 롤아웃으로 실험실 업무 중단을 피할 수 있기 때문입니다. 서비스 제공업체는 밸리데이션 아즈 어 서비스 및 AI 모델 스튜어드십을 포함한 포트폴리오를 확대하여 인력 부족에 제한 없이 고객에게 턴키 액세스를 제공합니다. 이 패턴은 시스템 구성을 진화하는 과학적 목적과 일치하는 전략적 도메인 지침과 함께 처음으로 소프트웨어의 유용성이 극대화됨을 보여줍니다.

2세대 매니지드 서비스 모델은 알고리즘 트레이닝과 성능 모니터링에 대한 책임을 지고 있으며, software-as-a-service의 사고 방식을 반영한 경상적인 수익 흐름을 창출하고 있습니다. 특히 단일 셀 시퀀싱과 같은 새로운 모달리티를 다루는 경우 실험실은 예측 가능한 지출과 신속한 시간 대 가치를 높이 평가합니다. 현재 일부 공급업체는 서비스 수수료와 정량화된 효율성 향상을 연결하는 성과 기반 가격 설정을 도입했으며 일시적인 도입 이정표가 아닌 지속적인 최적화를 장려하는 메커니즘이 되었습니다. 이를 위해 실험실 정보 관리 시스템 시장은 구성 가능한 플랫폼과 기술 및 규정 준수 측면을 탐색하는 컨설팅 깊이를 결합할 수 있는 공급업체에 보답하고 있습니다.

On-Premise 시스템은 2024년 매출의 55%를 차지했는데, 이는 엄격한 규제 시설이 인프라, 검증 스크립트 및 데이터 액세스 정책을 직접 관리하는 것을 선호하기 때문입니다. 그러나 실험실이 원격 액세스와 IT 오버헤드를 줄일 수 있기 때문에 클라우드 유형은 CAGR 10.2%를 나타낼 전망입니다. 익숙한 워크스테이션의 UI를 반영하면서 데이터를 소블린 클라우드에 저장하는 하이브리드 디자인은 감사관을 만족시키면서 분석에 필요한 탄력적인 계산을 가능하게 하고 받아들일 수 있는 교량을 합니다. 소규모 실험실에서는 클라우드 구독을 활용하여 자본 지출을 줄이고 배포를 몇 주 동안 압축할 수 있습니다.

유행성(세계적 유행)을 잠그면 얻은 운영 경험은 브라우저 기반 액세스의 탄력성을 입증했으며 보수적인 품질 관리 리더조차도 비 GxP 기능을 위한 SaaS 샌드박스를 시험적으로 도입하도록 촉구했습니다. 신뢰가 높아짐에 따라 생산 워크로드는 마이그레이션되고, 종종 안정성 테스트 및 환경 모니터링 모듈로 시작하여 중요한 릴리스 분석으로 이동합니다. 시간이 지남에 따라 실험실 정보 관리 시스템 시장은 에지 어플라이언스가 장비 캡처를 처리하면서 규제 등급 사본이 지역 클라우드 저장소에 존재하고 대기 시간 제어와 컴플라이언스를 모두 보장하는 통합 아키텍처를 보여줄 것으로 예측됩니다.

지역별 분석

북미는 2024년 실험실 정보 관리 시스템 시장의 매출에서 35%를 나타내 가장 큰 점유율을 차지하며 광범위한 제약 R&D 투자 및 정보학 공급업체 및 통합업체의 성숙한 생태계에 지지를 받았습니다. FDA와 같은 규제 당국에 의한 모니터링은 데이터 무결성을 우선시하고, 검사 시설은 LIMS가 제공하는 종합적인 감사 추적 및 전자 서명의 유지를 강요합니다. 프로액티브 품질 모니터링을 위한 AI 통합은 급속히 진행되고 있으며, 주요 제조업체는 출시를 방해하는 사건이 발생하기 전에 잠재적인 편차를 신고하는 예측 분석을 도입하고 있습니다. 유전체 검사에 대한 상환 경로와 함께 정밀의료의 채용이 진행되고 있으며, 시퀀싱 데이터와 환자의 동의를 통일 기록 내에 도입하는 플랫폼에 대한 수요가 더욱 높아지고 있습니다.

2030년까지 연평균 복합 성장률(CAGR)은 11.3%를 나타낼 것으로 예측되어 아시아태평양이 가장 빠른 속도로 추이하고 있습니다. 중국과 인도에서의 백신과 생물제제 제조의 지역적 확대는 연구소 인프라의 디지털화를 장려하는 정부 인센티브와 쌍을 이루고 있습니다. 싱가포르와 한국에서 사업을 전개하는 개발업무 수탁기관은 GLP(Good Laboratory Practice : 의약품안전성시험기준)를 준수하기 위해 LIMS를 도입하여 비용효과가 높고 품질이 보장된 파트너를 요구하는 다국적 스폰서로부터 계약을 획득하고 있습니다. 일본의 국가적 유전체 연구 이니셔티브는 프라이버시를 중시하는 동의 워크플로우를 통합하고 LIMS를 윤리적인 데이터 스튜어드십의 중심으로 삼고 있습니다. 반면 호주 농업기술 이해관계자들은 지속가능한 농업을 지원하기 위해 토양 마이크로바이옴 정보학을 채택하고 LIMS의 보급을 헬스케어 이외에도 확대하고 있습니다.

유럽은 엄격한 데이터 보호 규정과 견고한 바이오 의약품 제조거점으로 큰 발자국을 남깁니다. GDPR(EU 개인정보보호규정)은 시스템 설계에 영향을 주며 지역 잠긴 데이터 레지던시와 섬세한 동의 관리를 의무화합니다. 제약 연구소는 LIMS를 적격자 릴리스 시스템과 통합하여 원료 수락부터 최종 제품 인증까지 추적성을 보장합니다. 유럽 대륙의 광범위한 바이오 뱅킹 네트워크는 범유럽 연구 컨소시엄 내에서 종단적 샘플 추적과 국경을 넘어 데이터 교환에 특화된 모듈을 활용하고 있습니다. 영국 규제 코드의 브레그지트 후의 괴리는 의약품 및 헬스케어 제품 규제청의 가이드라인을 충족하기 위한 설정 프로젝트를 유발하여 도입 파트너에게 새로운 서비스 수익을 가져옵니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 의약품 및 바이오테크놀러지 연구개발 파이프라인의 급성장

- 바이오뱅크 수요 증가

- AI를 활용한 유전체 검사 워크플로가 정밀의료 실험실의 LIMS 수요 촉진

- 수탁 연구 및 제조 아웃소싱의 채용 증가

- 원격 시료 물류를 필요로 하는 분산형 임상시험의 급속한 확대

- LIMS를 도입하는 정밀 농업 토양 마이크로 바이옴 분석 실험실

- 시장 성장 억제요인

- 높은 총소유비용과 검증기간의 장기화

- 레거시 실험실 정보 시스템 및 이종 장치 인터페이스와의 상호 운용성의 과제

- 데이터 보안 및 주권에 대한 우려

- 바이오인포매틱스의 인재 부족이 선진적 LIMS의 보급 저지

- 가치/공급망 분석

- 규제와 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모·성장 예측(금액)

- 구성 요소별

- 소프트웨어

- 서비스

- 제품 유형별

- 광범위/다목적 LIMS

- 의약품 전용 LIMS

- 배포 모델별

- On-Premise

- 웹 호스팅

- 클라우드 기반

- 기업 규모별

- 대규모 실험실 네트워크

- 중소규모 실험실

- 용도별

- 신약 개발 및 전임상

- 임상시험 및 바이오 분석

- 제조 품질 관리(QC)

- 바이오 뱅킹 및 샘플 추적

- 최종 사용자별

- 제약 및 바이오테크놀러지 기업

- 계약 연구/개발 및 제조 기관(CRO/CDMO)

- 학술의료 및 연구기관

- 병원 및 임상 진단 실험실

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동

- GCC

- 남아프리카

- 기타 중동

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Thermo Fisher Scientific Inc.

- LabWare Inc.

- LabVantage Solutions Inc.

- Abbott Informatics(STARLIMS)

- Autoscribe Informatics

- Accelerated Technology Laboratories Inc.

- Genologics(Illumina Inc.)

- LabLynx Inc.

- Siemens Healthineers AG

- Dassault Systemes SE(BIOVIA)

- Agilent Technologies Inc.

- Waters Corporation(NuGenesis)

- PerkinElmer Inc.(Signals Notebook)

- Cerner Corp.(Oracle Health)

- Clinisys Group Ltd.

- Sunquest Information Systems Inc.

- Blomesystem GmbH

- Sapio Sciences LLC

- Benchling Inc.

- Ocimum Biosolutions Ltd.

- Computing Solutions Inc.

- Labworks LLC

제7장 시장 기회와 전망

KTH 25.10.28The laboratory information management system market size reached USD 595.62 million in 2025 and is projected to climb to USD 946.24 million by 2030, reflecting a 9.7% CAGR.

This momentum springs from sustained digitalization across research and quality-driven laboratories, where end-to-end data traceability now sits at the core of regulatory inspections. Growth also benefits from artificial-intelligence workflows that convert raw assay data into decision-ready insights, freeing scientists from repetitive curation tasks. Heightened demand for remote sample oversight, born out of pandemic-era decentralization, keeps investment focused on platforms that offer mobile accessioning, automated chain-of-custody, and real-time analytics. Providers that bundle LIMS, scientific data management, and electronic laboratory notebooks into unified cloud offerings continue to widen adoption by removing silo-bound workflows. Finally, the fast-rising volume of genomic, biobanking, and cell-therapy samples reinforces the value proposition of systems that secure data integrity from collection to long-term archival.

Global Laboratory Information Management System Market Trends and Insights

Rapid Growth of Pharmaceutical & Biotech R&D Pipeline

Global drug-development programs now exceed 20,000 active candidates, a figure 38% higher than in 2020. Each new molecule multiplies laboratory data volumes, intensifying the need for scalable LIMS that automate contextualization and audit trails. Platforms equipped with AI-driven outlier detection are shortening data-review cycles by 43% in quality-control labs, freeing analyst capacity and accelerating batch release . Seamless integration of LIMS with electronic notebooks and scientific data hubs breaks down informational barriers, letting multidisciplinary teams interrogate datasets from discovery through scale-up without manual exports. This capability speeds go/no-go decisions and supports adaptive trial designs that cut overall development timelines.

Growing Demand for Biobanking

More than 70% of precision-medicine programs depend on biorepositories that safeguard consented samples across decades. Modern systems pair IoT-enabled freezer monitoring with event-driven alerts that avert temperature excursions. Barcode-centred inventory in leading institutions has trimmed retrieval times by 67% while eliminating count discrepancies .Blockchain-anchored chain-of-custody is entering production environments, providing immutable provenance logs critical for gene-therapy samples whose usage rights link directly to donor consent. These advanced features elevate LIMS from passive record-keepers to proactive guardians of specimen integrity.

High Total Cost of Ownership and Prolonged Validation

Enterprise deployments may exceed USD 1 million in license fees and require validation periods that stretch 6-9 months, delaying return on investment. A Vermont public-health lab documented a USD 1.7 million spend covering customization and maintenance. Subscription-priced SaaS options mitigate capital outlay yet still confront conservative quality-assurance teams reluctant to outsource infrastructure. Vendors are countering with prevalidated templates that shorten qualification cycles and bundled managed-services contracts that cap lifetime costs.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Genomic-Testing Workflows

- Rapid Expansion of Decentralized Clinical Trials

- Precision-Agriculture Soil-Microbiome Analysis

- Data Security and Sovereignty Concerns

- Scarce Bioinformatics Talent Slowing Advanced LIMS Uptake

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The laboratory information management system market recorded services commanding 52% revenue in 2024, underscoring laboratories' reliance on external expertise for validation, integration, and continuous refinement. These engagements often extend for multiple years, ensuring workflows evolve with regulatory updates and new instrumentation. In parallel, demand for cloud-native subscriptions is accelerating at 10.8% CAGR, encouraged by elastic scaling and automatic feature rollouts that avoid interruption to bench activities. Service providers are broadening portfolios to include validation-as-a-service and AI-model stewardship, giving clients turnkey access to capabilities otherwise constrained by talent gaps. This pattern illustrates how software utility is maximized only when paired with strategic domain guidance that aligns system configuration with evolving scientific aims.

Second-generation managed-service models increasingly assume responsibility for algorithm training and performance monitoring, creating recurring revenue streams that mirror the software-as-a-service mindset. Laboratories appreciate predictable expenditure and quicker time-to-value, especially when tackling novel modalities such as single-cell sequencing. Several vendors now embed outcome-based pricing that links service fees to quantified efficiency gains, a structure that encourages ongoing optimization rather than one-off implementation milestones. The laboratory information management system market therefore rewards suppliers able to combine configurable platforms with consultative depth that navigates both technology and compliance landscapes.

On-premise systems retained 55% of 2024 revenue because heavily regulated facilities favour direct control over infrastructure, validation scripts, and data-access policies. However, the cloud cohort is forecast to grow 10.2% CAGR as laboratories seek remote accessibility and lighter IT overhead. Hybrid designs that mirror familiar workstation UIs while storing data in sovereign clouds provide an acceptable bridge, satisfying auditors yet permitting elastic compute for analytics bursts. For smaller labs, cloud subscriptions slash capital outlay and compress deployment into weeks, democratizing best-practice workflows once confined to big-pharma budgets.

Operational experience gained during pandemic lockdowns demonstrated the resilience of browser-based access, prompting even conservative quality leaders to pilot SaaS sandboxes for non-GxP functions. As confidence builds, production workloads migrate, often beginning with stability studies or environmental monitoring modules before moving critical release assays. Over time, the laboratory information management system market is expected to show a converged architecture in which edge appliances handle instrument ingestion while regulatory-grade copies reside in regional cloud vaults, ensuring both latency control and compliance.

The Report Covers LIMS Vendors and the Market is Segmented by Component (Software and Services), Product Type (Broad-Based / Multi-Purpose LIMS, and More), Deployment Model (On-Premise, Web-Hosted, and Cloud-Based), Enterprise Size (Large Laboratory Networks, and More, Application (Drug Discovery & Pre-Clinical, Clinical Trials & Bioanalysis, and More), End User (Pharmaceutical & Biotech Companies, and More), and Geography

Geography Analysis

North America generated the largest share of laboratory information management system market revenue in 2024 at 35%, underpinned by extensive pharmaceutical R&D investment and a mature ecosystem of informatics vendors and integrators. Regulatory scrutiny from agencies such as the FDA prioritizes data integrity, pressing laboratories to maintain comprehensive audit trails and electronic signatures that LIMS deliver. Integration of AI for proactive quality monitoring is progressing rapidly, with leading manufacturers deploying predictive analytics that flag potential deviations before release-blocking events occur. High adoption of precision medicine, coupled with reimbursement pathways for genomic testing, further stimulates demand for platforms that capture sequencing data and patient consents within unified records.

Asia-Pacific registers the fastest trajectory, with an 11.3% CAGR projected through 2030. Regional expansion of vaccine and biologics manufacturing in China and India is paired with government incentives encouraging digital transformation of laboratory infrastructure. Contract research organizations operating in Singapore and South Korea deploy LIMS to demonstrate Good Laboratory Practice compliance, winning contracts from multinational sponsors seeking cost-effective yet quality-assured partners. Japan's national genomics initiatives integrate privacy-centric consent workflows, making LIMS central to ethical data stewardship. Meanwhile, Australian agri-tech stakeholders adopt soil-microbiome informatics in support of sustainable-farming imperatives, extending LIMS penetration beyond healthcare.

Europe maintains a sizable footprint driven by stringent data-protection regulations and a robust biopharma manufacturing base. GDPR influences system design, mandating region-locked data residency and granular consent management. Pharmaceutical laboratories integrate LIMS with Qualified Person release systems, ensuring traceability from raw material intake through final product certification. The continent's extensive biobanking network leverages specialized modules for longitudinal sample tracking and cross-border data exchange within pan-European research consortia. Post-Brexit divergence of U.K. regulatory codes triggers configuration projects to meet Medicines and Healthcare products Regulatory Agency guidelines, generating fresh service revenue for implementation partners.

- Thermo Fisher Scientific

- LabWare

- LabVantage Solutions

- Abbott Informatics (STARLIMS)

- Autoscribe Informatics

- Accelerated Technology Laboratories

- Genologics (Illumina Inc.)

- LabLynx

- Siemens Healthineers

- Dassault Systemes SE (BIOVIA)

- Agilent Technologies

- Waters Corporation (NuGenesis)

- PerkinElmer Inc. (Signals Notebook)

- Cerner Corp. (Oracle Health)

- Clinisys Group Ltd.

- Sunquest Information Systems Inc.

- Blomesystem GmbH

- Sapio Sciences LLC

- Benchling Inc.

- Ocimum Biosolutions Ltd.

- Computing Solutions Inc.

- Labworks

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Growth of Pharmaceutical & Biotech R&D Pipeline

- 4.2.2 Growing Demand for Biobanking

- 4.2.3 AI-Enabled Genomic-Testing Workflows Boosting LIMS Demand in Precision Medicine Labs

- 4.2.4 Rising adoption of contract research and manufacturing outsourcing

- 4.2.5 Rapid Expansion of Decentralized Clinical Trials Requiring Remote Sample Logistics

- 4.2.6 Precision-Agriculture Soil-Microbiome Analysis Labs Deploying LIMS

- 4.3 Market Restraints

- 4.3.1 High Total Cost of Ownership and Prolonged Validation

- 4.3.2 Interoperability challenges with legacy laboratory information systems and heterogeneous instrument interfaces.

- 4.3.3 Data Security and Sovereignty Concerns

- 4.3.4 Scarce Bioinformatics Talent Slowing Advanced LIMS Uptake

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory & Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Product Type

- 5.2.1 Broad-based / Multi-purpose LIMS

- 5.2.2 Pharma-specific LIMS

- 5.3 By Deployment Model

- 5.3.1 On-premise

- 5.3.2 Web-hosted

- 5.3.3 Cloud-based

- 5.4 By Enterprise Size

- 5.4.1 Large Laboratory Networks

- 5.4.2 Small & Medium-sized Laboratories

- 5.5 By Application

- 5.5.1 Drug Discovery & Pre-clinical

- 5.5.2 Clinical Trials & Bioanalysis

- 5.5.3 Manufacturing Quality Control (QC)

- 5.5.4 Biobanking & Sample Tracking

- 5.6 By End User

- 5.6.1 Pharmaceutical & Biotech Companies

- 5.6.2 Contract Research / Development & Manufacturing Orgs (CROs / CDMOs)

- 5.6.3 Academic Medical & Research Institutes

- 5.6.4 Hospital & Clinical Diagnostic Labs

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 South Korea

- 5.7.3.5 Australia

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company profiles ((includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Thermo Fisher Scientific Inc.

- 6.4.2 LabWare Inc.

- 6.4.3 LabVantage Solutions Inc.

- 6.4.4 Abbott Informatics (STARLIMS)

- 6.4.5 Autoscribe Informatics

- 6.4.6 Accelerated Technology Laboratories Inc.

- 6.4.7 Genologics (Illumina Inc.)

- 6.4.8 LabLynx Inc.

- 6.4.9 Siemens Healthineers AG

- 6.4.10 Dassault Systemes SE (BIOVIA)

- 6.4.11 Agilent Technologies Inc.

- 6.4.12 Waters Corporation (NuGenesis)

- 6.4.13 PerkinElmer Inc. (Signals Notebook)

- 6.4.14 Cerner Corp. (Oracle Health)

- 6.4.15 Clinisys Group Ltd.

- 6.4.16 Sunquest Information Systems Inc.

- 6.4.17 Blomesystem GmbH

- 6.4.18 Sapio Sciences LLC

- 6.4.19 Benchling Inc.

- 6.4.20 Ocimum Biosolutions Ltd.

- 6.4.21 Computing Solutions Inc.

- 6.4.22 Labworks LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment