|

시장보고서

상품코드

1842446

혈관성형술용 풍선 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Angioplasty Balloons - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

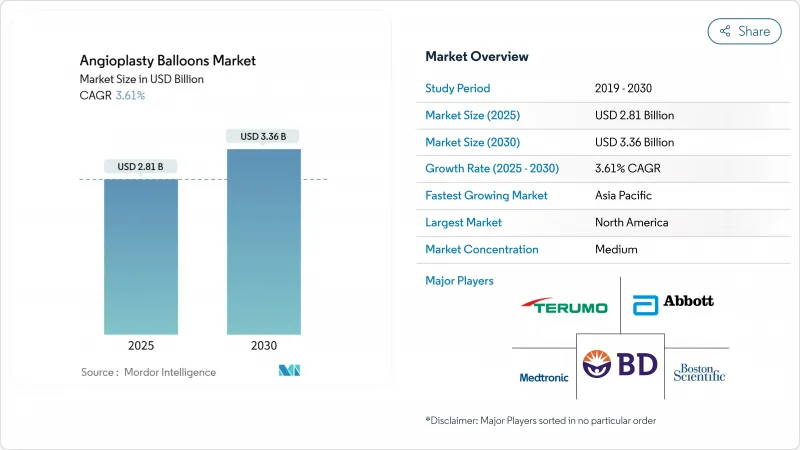

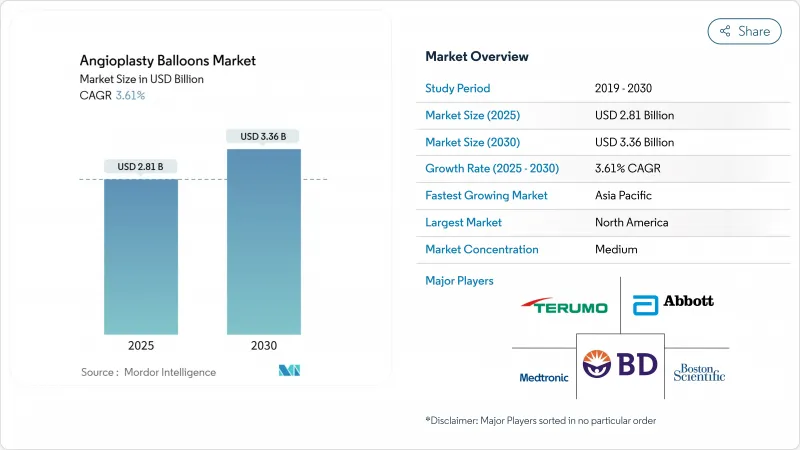

혈관성형술용 풍선 시장은 2025년에 28억 1,000만 달러, 2030년에는 33억 6,000만 달러에 이를 것으로 예측되며, CAGR은 3.61%로 예상됩니다.

이러한 전망에 의하면 혈관성형술용 풍선 시장은 선진지역에서의 수술의 완만한 성장과 기기의 고도화로 인해 심혈관 의료환경 속에서 계속 성숙하고 있는 것을 확인할 수 있습니다. 20세 이상의 미국인 중 1억 2,790만명이 심장병을 앓고 있으며, 관상동맥 질환의 유병률은 4.6%에서 4.9%에 가깝습니다. 저침습적 경피적 관상동맥 인터벤션(PCI)에 대한 임상 선호도 증가가 주요 치료 건수를 유지하는 반면, 최근 약물 코팅 풍선(DCB)의 승인을 통해 영구적인 금속 임플란트에 대한 의존성을 줄이는 "leave-nothing-behind"치료 전략이 검증되었습니다. 일반적인 풍선이 여전히 루틴 PCI를 지배하고 있지만, 병변의 복잡성이 증가하고 결과 보상 모델이 내구성있는 결과에 보답함에 따라 특수 스코어링 및 약물 기술이 점유율을 확대하고 있습니다.

경쟁과 지역의 주요 변화가 중기 상승을 뒷받침하고 있습니다. 북미는 2024년 혈관성형술용 풍선 시장의 39.68%를 차지하였으며, 선진적인 인프라와 외래수술센터(ASC)에서 PCI를 커버하는 환급으로 지역별로 최고 실적을 유지하고 있습니다. 아시아태평양은 CAGR 4.53%로 급성장하고 있으며, 인구동태의 고령화와 심혈관조영실의 설비투자에 의한 급속한 PCI 도입에 의해 뒷받침되고 있습니다. 의료 제공 수준에서 혈관성형술용 풍선 시장의 성장은 외래 센터로 기울고 있습니다. ASC 기반 PCI 건수는 2018년부터 2022년 사이에 메디케어 수급자 1만명당 0.01건에서 0.87건으로 증가했으며, 이 환경에서의 CAGR은 4.67%로 예상됩니다. 제품별로는 일반 풍선이 2024년에 41.54%의 점유율을 차지했지만 임상의가 플라크 제거 효율을 추구함에 따라 스코어링 풍선이 4.32%의 연평균 복합 성장률(CAGR)을 기록하고 있습니다. 한편 보스턴 사이언티픽이 2024년 FDA로부터 인가를 취득한 AGENT 관동맥 DCB는 표적 병변의 재관류 위험을 일반 풍선에 비해 50% 감소시켜 약물 코팅 플랫폼에 대한 규제 당국의 결정적인 청신호를 보여주고 있습니다.

세계의 혈관성형술용 풍선 시장의 동향과 인사이트

심혈관 질환의 유병률 상승

임상적 심혈관 질환을 앓고 있는 성인의 수는 2050년까지 미국에서만 4,500만 명을 넘을 것으로 예측됩니다. 고혈압, 당뇨병, 비만의 비율은 모두 지속적으로 상승하고 있으며, 카테터를 이용한 혈액 순환 재건술의 장기적인 필요성이 높아지고 있습니다. 관상동맥 사망률은 2000년부터 2020년까지 현저하게 떨어졌으나 최근에는 두드러졌으며 풍선 혈관성형술 수요는 안정적입니다. 심장병에 의한 입원으로 2021년에 1,080억 달러의 지출이 발생하였고, 2030년에는 1,313억 달러에 이를 것으로 예측되며, 비용효율적인 저침습 솔루션이 경제적으로 필수적인 솔루션으로 부각되고 있습니다.

저침습 PCI로의 이동과 기술 진보

임상 현장에서는 현재 회복 기간을 단축하고 시설 비용을 억제하는 경피적 카테터 접근법이 선호되고 있습니다. 2025년에 발표된 관상동맥 DCB 시험의 표준화된 엔드포인트는 약제 코팅 풍선을 뒷받침하였고, 발병 1년 후의 표적 병변부전율은 일반 풍선이 28.6%인 반면 17.9%였습니다. 혈관 내 결석 파쇄술은 풍선 내의 음향 압력파를 사용하여 칼슘을 파쇄하고 루멘의 확장을 개선하는 것으로 기세를 늘리고 있습니다. 이러한 기술은 영구적인 금속을 남기지 않고 치료 결과를 향상시켜 혈관성형술용 풍선 시장의 전망을 강화하고 있습니다.

스텐트 삽입에 비해 높은 수기 및 기기 비용

의료비 지급자는 후속 영상 진단 및 투약 계획을 포함한 번들 스텐트 패키지보다 풍선 전용 전략이 더 높은 비용을 필요로 한다고 의식하고 있습니다. 메디케어의 승인에도 불구하고, ASC는 미국 외래 PCI의 1.8%만을 실시하고 있으며, 경제적인 이유로 도입이 지연되고 있음을 보여줍니다. 의약품 코팅 풍선의 프리미엄 가격은 특히 공급망 인플레이션에 의해 투입 비용이 장비 수익의 20%로 상승할 경우 구매 결정을 저해하는 것으로 나타났습니다.

부문 분석

2030년까지의 연평균 복합 성장률(CAGR)은 4.32%로 스코어링 풍선이 가장 빠른 성장 궤도를 보일 것으로 예상되고 있습니다. 이는 석회화 병변과 섬유화 병변에 대한 플라크 제거 전략의 역할을 반영한 속도입니다. 스코어링 시스템의 혈관성형술용 풍선 시장 규모는 Naviscore사의 first-in-man 시리즈 등의 연구에 의해 중등도에서 중증의 석회화 병변에서의 수술 성공률이 94%인 것으로 보고되어 상승 경향에 있습니다. 일상적인 PCI에서는 확장 전후의 루틴에 일반 풍선이 필수적이기 때문에 2024년의 점유율은 41.54%로 여전히 일반 풍선이 우세하였습니다.

약물 코팅 풍선은 보스턴 사이언티픽의 AGENT 승인 후 기존의 혈관성형술과 비교하여 혈행재건술의 재시행을 50% 감소시켰기 때문에 큰 인기를 얻었습니다. 커팅 풍선은 스텐트 내 재협착 및 소혈관에 대한 틈새 치료법이며, 메타분석은 표적 병변의 재관류 위험을 33% 감소시키는 것으로 나타났습니다. 40 기압을 넘는 초고압 풍선은 딱딱한 섬유 석회화 플라크에 대한 경피 치료를 확대하고 혈관성형술용 풍선 시장을 수술적 및 기술적으로 확대하고 있습니다.

지역별 분석

2024년 혈관성형술용 풍선 시장의 점유율은 북미가 39.68%로 최고이며, 폭넓은 보험 적용, 확립된 심혈관조영실 네트워크, 프리미엄 디바이스의 조기 도입이 이를 지원하고 있습니다. 이 지역의 규제 환경은 혁신에 유리하며, 2024년 관상동맥 DCB AGENT의 인가가 이를 증명합니다. ASC 기반 PCI를 허용하는 CMS의 정책 변경으로 PCI 시행 건수의 분포가 재구성되기 시작했지만, 복잡한 절차의 대부분은 병원이 담당하고 있습니다. 지속적인 공급망의 혼란은 현지 제조업체들이 두 자릿수의 물류와 원재료 인플레이션을 흡수하도록 강요하여 디지털 재고 관리에 대한 관심을 높이고 있습니다. Teleflex가 BIOTRONIK의 혈관 부문을 7억 6,000만 유로로 인수하여 약물 코팅 풍선과 스텐트 제품 라인업을 충실히 함으로써 통합은 계속 활발해지고 있습니다.

아시아태평양은 CAGR 4.53%로 가장 급속히 확대했습니다. 인구의 고령화, 도시화, 인프라 정비가 심혈관조영실 수요를 자극하고 있습니다. 의료기기 인가의 조화와 국내 제조의 장려를 향한 정부의 움직임에 의해 신형 풍선 시장 투입까지의 시간이 계속 단축되고 있습니다. 지역별 임상 지침은 소혈관 질환 및 스텐트 내 재협착에 대해 DCB를 권장하며, 치료법의 선택은 세계 표준을 따릅니다. 그러나 하이엔드 스코어링 풍선과 약물 코팅 풍선에 대한 수요가 높아지는 가운데 가격 민감성이 구매자를 비용효율적인 플랫폼으로 향하게 하여 일반 풍선의 현지 생산을 가속화하고 있습니다.

유럽에서는 경제적 압력으로 일부 공공 의료 시스템에서 프리미엄 풍선 도입이 억제되어 꾸준하지만 완만한 상승에 머물고 있습니다. 의료기기 규제(MDR)의 틀은 엄격하지만, Terumo는 2024년에 여러 혈관 폐쇄 솔루션의 CE 마크를 획득하여 수술 생태계를 유지하는 데 기여하였습니다. Cordis의 SELUTION SLR 시롤리무스 용출 풍선은 일본에서 81.5%의 3년 개방율을 기록했으며, 유럽의 임상시험에서는 91.1%의 표적 병변의 재관류를 방지했습니다. Drug-Coated Balloon Academic Research Consortium과 같은 그룹을 통한 임상 협력은 유럽 전역에서 증거 기반 채용을 촉진하고 차세대 풍선의 선구자 시장으로서 유럽의 역할을 유지하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 심혈관 질환의 유병률의 상승

- 저침습 PCI로의 시프트와 기술의 진보

- 신흥국의 고령자 PAD 환자 확대

- 병원의 주력 제품으로 유지되는 통상 압력 풍선

- 생체 흡수성 및 초고압 폴리머의 혁신

- 혈관성형술 외래 심혈관조영실로의 전환

- 시장 성장 억제요인

- 스텐트 삽입 대비 높은 수기 비용과 기기 비용

- 수술 전후의 합병증

- 고급 나일론 및 PET 필름공급 체인의 혼란

- 파클리탁셀 DCB의 안전성에 대한 규제 상의 신중함

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측(단위 : 달러)

- 제품 유형별

- 일반 풍선

- 커팅 풍선

- 스코어링 풍선

- 약제 용출 풍선

- 용도별

- 관상동맥성형술

- 말초혈관성형술

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 튀르키예

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Abbott Laboratories

- AngioDynamics

- Becton, Dickinson & Co.

- BIOTRONIK

- Boston Scientific Corp.

- B. Braun Melsungen AG

- Cook Medical

- Terumo Corp.

- INFINITY Angioplasty Balloon

- Johnson & Johnson

- Koninklijke Philips NV

- Medtronic plc

- Merit Medical Systems

- Integer Holdings Corp.

- Shockwave Medical Inc.

- Teleflex Inc.

- Cardionovum GmbH

- Biosensors International

- LEPU Medical Technology

제7장 시장 기회와 전망

CSM 25.11.03The angioplasty balloons market stands at USD 2.81 billion in 2025 and is projected to reach USD 3.36 billion by 2030, translating into a 3.61% CAGR.

This outlook confirms that the angioplasty balloons market continues to mature in a cardiovascular care environment where device sophistication must counterbalance modest procedure growth in developed regions. Demand remains firmly rooted in a large and aging cardiovascular patient pool-127.9 million Americans aged 20 and older live with heart disease today, and coronary artery disease prevalence remains close to 4.6%-4.9%. Growing clinician preference for minimally invasive percutaneous coronary intervention (PCI) sustains core procedure volumes, while recent approvals for drug-coated balloons (DCBs) validate a "leave-nothing-behind" treatment strategy that reduces reliance on permanent metallic implants. Normal balloons still dominate routine PCI, yet specialized scoring and drug technologies are gaining share as lesion complexity rises and pay-for-performance models reward durable outcomes.

Key competitive and regional shifts underpin medium-term upside. North America retains the largest regional position with 39.68% of the angioplasty balloons market in 2024 thanks to advanced infrastructure and reimbursement that now covers PCI in ambulatory surgical centers (ASCs). Asia-Pacific is the fastest-growing territory, expanding at 4.53% CAGR, supported by rapid procedure adoption amid demographic aging and investments in cath-lab capacity. At the care-delivery level, angioplasty balloons market growth tilts toward outpatient centers; ASC-based PCI volumes climbed from 0.01 to 0.87 per 10,000 Medicare beneficiaries between 2018 and 2022, pointing to 4.67% CAGR for this setting. On the product front, normal balloons held 41.54% share in 2024, but scoring balloons are pacing 4.32% CAGR as clinicians seek plaque-modification efficiency. Meanwhile, Boston Scientific's 2024 FDA clearance for the AGENT coronary DCB, which cut target-lesion revascularization risk by 50% versus plain balloons, signals a decisive regulatory green light for drug-coated platforms.

Global Angioplasty Balloons Market Trends and Insights

Rising Cardiovascular Disease Prevalence

The number of adults living with clinical cardiovascular disease is projected to top 45 million in the United States alone by 2050. Hypertension, diabetes, and obesity rates all continue to climb, reinforcing a long-run need for catheter-based revascularization. Although coronary mortality dropped markedly between 2000 and 2020, it has plateaued in recent years, keeping demand for balloon angioplasty stable. Hospitalizations linked to heart disease cost USD 108 billion in 2021, and forecasts point to USD 131.3 billion by 2030, highlighting the economic imperative for cost-effective minimally invasive solutions.

Shift toward Minimally-invasive PCI & Technology Advances

Clinical practice now favors percutaneous catheter approaches that shorten recovery and curb facility costs. Standardized endpoints for coronary DCB trials released in 2025 have legitimized drug-coated balloons, which posted 17.9% target-lesion failure at 1 year versus 28.6% with plain balloons. Intravascular lithotripsy is gaining momentum, using acoustic pressure waves inside the balloon to fracture calcium and improve luminal gain. These technologies collectively strengthen the angioplasty balloons market outlook by enhancing outcomes without leaving permanent metal behind.

High Procedure & Device Cost versus Stenting Bundles

Healthcare payers remain cautious when balloon-only strategies appear more expensive than bundled stent packages that include follow-up imaging and medication plans. Despite Medicare approval, ASCs still perform only 1.8% of outpatient PCIs in the United States, signaling persistent economic hesitation. Premium pricing on drug-coated balloons tightens purchasing decisions, especially where supply-chain inflation has lifted input costs to 20% of device revenues.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Geriatric PAD Pool in Emerging Economies

- Breakthroughs in Bio-resorbable & Ultra-high-pressure Polymers

- Regulatory Scrutiny on Paclitaxel DCB Safety Signals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Scoring balloons held the fastest growth trajectory at 4.32% CAGR through 2030, a pace that reflects their role in plaque-modification strategies for calcified or fibrotic lesions. The angioplasty balloons market size for scoring systems is rising as studies such as Naviscore's first-in-man series reported 94% procedural success in moderate-to-severe calcification. Normal balloons still dominate everyday PCI with 41.54% 2024 share because they remain indispensable for routine pre- and post-dilation steps.

Drug-coated balloons gained decisive momentum after Boston Scientific's AGENT approval, which showed a 50% reduction in repeat revascularization compared with conventional angioplasty. Cutting balloons preserve a niche for in-stent restenosis and small-vessel work, with meta-analysis indicating a 33% reduction in target-lesion revascularization risk. Ultra-high-pressure variants, now exceeding 40 atm, extend percutaneous treatment to hard fibro-calcific plaques, expanding the angioplasty balloons market both procedurally and technologically.

The Angioplasty Balloons Market Report Segments the Industry Into by Product Type (Normal Balloons, Cutting Balloons, Scoring Balloons, and Drug-Eluting Balloons), by Application (Coronary Angioplasty, Peripheral Angioplasty), by End User (Hospitals, Ambulatory Surgical Centers, Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 39.68% angioplasty balloons market share in 2024, supported by broad insurance coverage, established cath-lab networks, and early adoption of premium devices. The region's regulatory environment favors innovation, evidenced by the 2024 clearance of the AGENT coronary DCB. CMS policy changes permitting ASC-based PCI have begun to reshape volume distribution, yet hospitals keep the bulk of complex procedures. Persistent supply-chain turbulence has forced local manufacturers to absorb double-digit logistics and raw-material inflation, heightening focus on digital inventory control. Consolidation remained active, highlighted by Teleflex's EUR 760 million acquisition of BIOTRONIK's vascular unit, which enriched its drug-coated balloon and stent offerings.

Asia-Pacific registers the swiftest expansion at 4.53% CAGR. Population aging, urbanization, and infrastructure build-out are unlocking cath-lab demand. Government moves to harmonize device approvals and encourage domestic manufacturing continue to reduce time-to-market for new balloons. Regional clinical guidelines now recommend DCBs for small-vessel disease and in-stent restenosis, aligning therapy choices with global standards. Growth, however, is tempered by price sensitivity, which pushes buyers toward cost-effective platforms and accelerates local production of basic balloons even as demand for high-end scoring and drug-coated variants climbs.

Europe delivers steady but measured gains as economic pressures constrain premium device uptake in some public-health systems. The Medical Device Regulation (MDR) framework, while rigorous, provides clarity that helped Terumo secure CE marks for several vascular-closure solutions in 2024, sustaining procedural ecosystems. Cordis's SELUTION SLR sirolimus-eluting balloon posted 81.5% three-year patency in Japan and 91.1% freedom from target-lesion revascularization in European trials, reinforcing drug-coated platforms. Clinical collaboration through groups such as the Drug-Coated Balloon Academic Research Consortium promotes evidence-based adoption across the continent, maintaining Europe's role as a bellwether market for next-generation balloons.

- Abbott Laboratories

- AngioDynamics

- Beckton Dickinson

- BIOTRONIK

- Boston Scientific

- B. Braun

- Cook Group

- Terumo Corp.

- INFINITY Angioplasty Balloon

- Johnson & Johnson

- Koninklijke Philips

- Medtronic

- Merit Medical Systems

- Integer Holdings Corp.

- Shockwave Medical Inc.

- Teleflex

- Cardionovum

- Biosensors International

- LEPU Medical Technology

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Cardiovascular Disease Prevalence

- 4.2.2 Shift toward Minimally-invasive PCI & Tech Advances

- 4.2.3 Expanding Geriatric PAD Pool in Emerging Economies

- 4.2.4 Normal-pressure Balloons Remain Hospital Workhorse

- 4.2.5 Breakthroughs in Bio-resorbable & Ultra-high-pressure Polymers

- 4.2.6 Migration of Angioplasty to Outpatient Cath-lab Settings

- 4.3 Market Restraints

- 4.3.1 High Procedure & Device Cost vs. Stenting Bundles

- 4.3.2 Periprocedural Complications

- 4.3.3 Supply-chain Tightness for High-grade Nylon & PET Films

- 4.3.4 Regulatory Scrutiny on Paclitaxel DCB Safety Signals

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Normal Balloons

- 5.1.2 Cutting Balloons

- 5.1.3 Scoring Balloons

- 5.1.4 Drug-Eluting Balloons

- 5.2 By Application

- 5.2.1 Coronary Angioplasty

- 5.2.2 Peripheral Angioplasty

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Others

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 Turkey

- 5.4.4.3 South Africa

- 5.4.4.4 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Abbott Laboratories

- 6.3.2 AngioDynamics

- 6.3.3 Becton, Dickinson & Co.

- 6.3.4 BIOTRONIK

- 6.3.5 Boston Scientific Corp.

- 6.3.6 B. Braun Melsungen AG

- 6.3.7 Cook Medical

- 6.3.8 Terumo Corp.

- 6.3.9 INFINITY Angioplasty Balloon

- 6.3.10 Johnson & Johnson

- 6.3.11 Koninklijke Philips N.V.

- 6.3.12 Medtronic plc

- 6.3.13 Merit Medical Systems

- 6.3.14 Integer Holdings Corp.

- 6.3.15 Shockwave Medical Inc.

- 6.3.16 Teleflex Inc.

- 6.3.17 Cardionovum GmbH

- 6.3.18 Biosensors International

- 6.3.19 LEPU Medical Technology

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment