|

시장보고서

상품코드

1842451

미생물 식별 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Microbial Identification - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

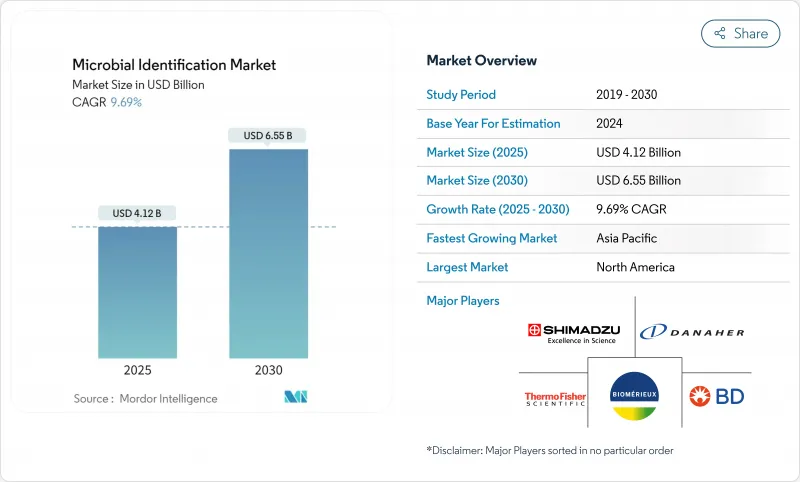

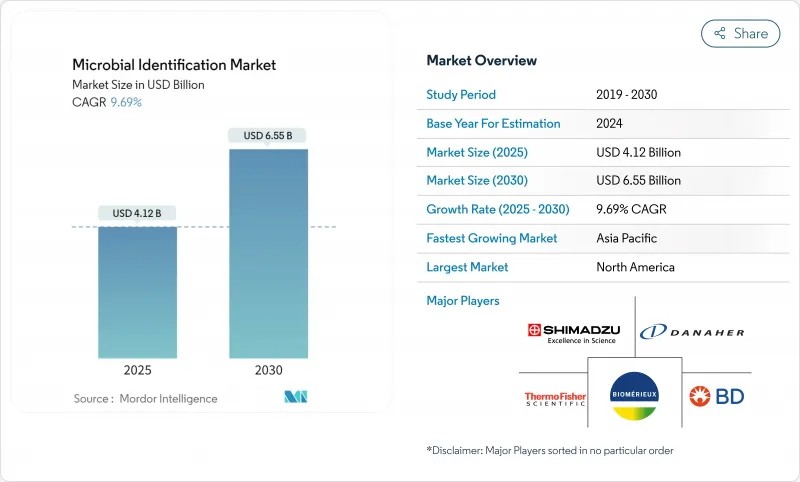

미생물 식별 시장은 2025년에 41억 2,000만 달러로 평가되고, 2030년에는 65억 5,000만 달러에 도달할 것으로 예측되며, CAGR 9.69%를 나타낼 전망입니다.

배양 기반 분석에서 분자 플랫폼으로의 전환, 항균제 내성 감시 강화, 신속한 턴어라운드에 대한 기대가 기세를 유지하는 주요 힘이 되고 있습니다. 공급업체는 기술 포트폴리오를 확장하고, 규제 당국은 승인 경로를 명확히 하고, 헬스케어 시스템은 실시간 데이터 통합에 투자하고 있습니다. 동시에 인력 부족과 높은 자본 요건은 자원에 제약이 있는 환경에서의 채용을 억제하고 있습니다. 인공지능도구가 병원체 도서관을 확장하고 신흥국 전체에서 식품안전규칙이 강화됨에 따라 장기적인 성장 전망은 지속적으로 강해지고 있습니다.

세계의 미생물 식별 시장 동향과 인사이트

일상 진단에서 MALDI-TOF MS의 신속한 채용

연구실은 현재 시간당 최대 600개 샘플을 처리하는 고처리량 MALDI-TOF 플랫폼을 사용하여 몇 시간이 아닌 몇 분 안에 종 수준을 확인하고, 낮은 시약 비용으로 16S rRNA 시퀀싱의 정확도에 필적하는 결과를 얻고 있습니다. 4,300종 이상을 다루는 확장된 참조 데이터베이스를 통해 동일한 장비에서 식품, 의약품 및 임상 워크플로우를 지원할 수 있습니다. 미국 식품의약국은 2025년 6월 이러한 시스템을 특별한 관리를 수반하는 Class II로 분류하였으며, 제조업체에게 안전 기준을 유지하면서 더욱 명확하고 신속한 클리어런스 경로를 제공했습니다.

항균제 내성 감시 프로그램의 성장

미국에서는 연간 280만 건 이상의 AMR 감염이 발생해 3만 5,000명이 사망하고 있기 때문에 전체 유전체 시퀀싱이 서베이란스 네트워크에 채용되게 되었습니다. 중국의 전국 CHINET 프로그램은 2021년까지 분리된 엔테로박터 균주의 10%에 카바페넴 내성이 보고되어 신속한 동정에 대한 세계적인 압력이 집중하고 있는 것으로 밝혀졌습니다. 적시 균프로파일 링은 약사가 효과적인 치료를 조정하고 입원 기간을 단축하는 데 도움이 됩니다.

고가의 장비와 유지보수 비용

선진적인 MALDI-TOF 시스템의 자본 지출은 20만 달러를 넘어서 서비스 계약은 매년 구입 가격의 10-15%를 올리기 때문에 중견 병원에서의 도입은 제한됩니다. 2024년에 채택된 새로운 임상검사 개선법의 성과 목표는 보다 엄격한 시그마 지표를 요구하고 있으며, 소규모 실험실은 계획보다 빨리 장비를 업그레이드하거나 교체해야 할 수 있습니다.

분석되는 기타 성장 촉진요인 및 억제요인

- 신흥국에서의 식품안전규제의 고조

- AI 탑재 스펙트럼 라이브러리의 통합

- 질량 분석 숙련 기술자 부족

부문 분석

소모품은 2024년 매출의 47.15%를 차지했습니다. 이는 실험실이 매번 검사에 필요한 대량의 시약과 배지에 의존하고 있기 때문에 미생물 식별 시장에 경상적인 현금 흐름의 탄력성을 부여하고 있습니다. 소프트웨어 및 서비스는 규모가 작고 실험실이 데이터 마이그레이션 및 분석을 자동화하는 클라우드 검사 정보 시스템으로 업그레이드됨에 따라 CAGR 11.78%를 나타내 가장 빠르게 성장하고 있습니다. 로봇 공학과 AI를 도입한 차세대 '다크라보'는 소프트웨어 레이어가 처리량을 향상시키면서 인력 부족을 완화한다는 것을 보여줍니다.

이 변화는 또한 애널리틱스 대시보드의 구독 라이선싱을 위한 광범위한 움직임을 돋보이게 하며, 공급업체는 예측 가능한 마진을 제공하고 사용자에게 신속한 투자 회수를 제공합니다. 품질 관리 규제가 강화됨에 따라 장비 성능을 기록하고 편차에 실시간으로 플래그를 지정하는 클라우드 호스팅 플랫폼이 중요해지고 있습니다. 이 소프트웨어의 보급은 2030년까지 2자리 성장을 유지해 미생물 식별 시장 전체의 경쟁 차별화의 핵심으로서 디지털 프로세스를 확고하게 할 것으로 예측됩니다.

MALDI-TOF MS는 2024년 57.50%의 매출 점유율을 유지하면서 비교할 수 없는 속도-투-리저트, 낮은 검사 단가, 지속적으로 확대되는 생물 라이브러리를 강점했습니다. MALDI-TOF 플랫폼의 미생물 식별 시장 규모는 여전히 확대되고 있지만, 북미와 유럽에서 보급이 진행됨에 따라 성장은 완만해지고 있습니다. 이와는 대조적으로 PCR과 실시간 PCR은 멀티플렉스 패널과 POC(Point-of-Care) 형식이 기본 케어 클리닉에 보급됨에 따라 2030년까지 연평균 복합 성장률(CAGR)이 12.73%를 나타내 가장 급상승할 전망입니다. 2024년, 주요 신드로믹 PCR 분석기에 대한 4개의 FDA 인가는 규제 기세를 보여주었습니다.

검사실이 우선 MALDI-TOF에서 스크리닝을 실시하고, 그 후 PCR이나 내성 유전자의 시퀀싱로 이행하는 하이브리드 워크플로우가 출현하고 있어 폭의 넓이와 깊이를 겸비하고 있습니다. 크로스 플랫폼 데이터 컨버전스는 새로운 소모품 및 서비스 번들에 박차를 가하여 제조업체가 보완적인 분자 분석으로부터 증가를 활용하면서 점유율을 보호 할 수 있게 합니다.

지역 분석

북미는 2024년에 있어서도 최대의 매출 공헌국이며, 세계 전체의 39.56%를 차지했습니다. 이것은 충분한 자금이 투입된 건강 관리 시스템, 상환되는 신속 검사, 강력한 AMR 감시 보조금을 반영합니다. 미국 내 검사실은 CDC의 항균제 내성 검사실 네트워크를 활용하여 국가 대시보드에 실시간 데이터를 제공하는 연결형 식별 플랫폼을 채용하고 있습니다. 캐나다도 비슷한 궤도를 따르고 있지만 기술자 부족에 직면하고 있으며 소규모 주에서 장비 도입이 지연되었습니다.

아시아태평양은 CAGR 11.45%를 나타낼 것으로 예측되며, 중국과 인도의 공립 병원 확대, ASEAN 이니셔티브에 의한 품질 기준의 조화, 활기찬 지역의 바이오 제조거점에 의해 추진됩니다. CHINET 프로그램의 다기능 데이터 세트는 이 지역의 데이터 성숙도와 그 결과 항생제 처방에 대한 지침이 되는 생물학적 프로파일링의 가속화를 보여줍니다. 정부는 또한 지방질환관리센터를 위한 장비구입에 보조금을 내고 지방의 접근성을 넓히고 있습니다.

유럽은 엄격한 체외 진단용 의약품 규제 기한에 따라 검사 시설이 예정보다 빨리 플랫폼의 검증을 실시하게 되어 적합 키트의 안정된 수요가 확보되어 완만한 성장을 유지하고 있습니다. 영국의 ESPAUR 보고서는 2019년 이후 AMR 부담의 3.5% 상승을 꼽고 있으며, 신속한 동정을 정책 과제로 삼고 있습니다. Brexit의 세관 변경으로 인해 공급망에 지연이 발생할 수 있지만 대륙의 조달 프레임 워크는 최종 사용자를 부족으로부터 크게 보호합니다.

중동 및 아프리카은 도입 초기 단계에 있지만, 걸프 국가에 의한 3차 의료시설에 대한 투자나 기증자 자금에 의한 수병원체 프로젝트에 의한 혜택을 받고 있습니다. 라틴아메리카에서는 브라질과 멕시코가 주요 무역 상대국 간의 수출 요건을 정합시키고 농산업 실험실 이용을 뒷받침하기 때문에 식품 안전 검사량이 증가하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 루틴 진단에 있어서의 MALDI-TOF MS의 급속한 채용

- 항균제 내성(AMR) 감시 프로그램의 성장

- 신흥국에서의 식품안전규제의 고조

- AI를 활용한 스펙트럼 라이브러리의 통합(과소보고)

- 분산형 POCT 미생물 ID 시스템의 확대(보고 부족)

- 시장 성장 억제요인

- 높은 장비 및 유지 보수 비용

- 숙련된 질량 분석 기술자의 부족

- 환경분리주의 표준화 부족(보고 부족)

- 클라우드 기반 ID 플랫폼의 사이버 보안 위험(과소보고)

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Five Forces 분석

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측

- 제품 및 서비스별

- 기구

- 소모품

- 소프트웨어 및 서비스

- 기술별

- MALDI-TOF MS

- PCR 및 실시간 PCR

- 시퀀싱(NGS, Sanger)

- 기타(생화학, 현미경 등)

- 최종 사용자별

- 병원 및 임상 실험실

- 제약 및 바이오테크놀러지 기업

- 식음료 검사실

- 환경 및 산업 시험소

- 용도별

- 임상 진단

- 제약 제조 품질 관리(QC)

- 식품안전 및 품질

- 환경 모니터링

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- bioMerieux SA

- Bruker Corporation

- Becton, Dickinson and Company

- Thermo Fisher Scientific Inc.

- Danaher Corporation(Beckman Coulter)

- Shimadzu Corporation

- Charles River Laboratories

- Biolog Inc.

- Qiagen NV

- Merck KGaA(MilliporeSigma)

- Liofilchem Srl

- bioNote Inc.

- MIDI Labs

- Eppendorf AG

- Hologic Inc.

- Roche Diagnostics

- Siemens Healthineers

- Revvity(PerkinElmer)

- Abbott Laboratories

- Agilent Technologies

제7장 시장 기회와 전망

KTH 25.10.28The microbial identification market was valued at USD 4.12 billion in 2025 and is forecast to reach USD 6.55 billion by 2030, advancing at a 9.69% CAGR.

The transition from culture-based assays to molecular platforms, intensified antimicrobial-resistance surveillance, and quicker turnaround expectations are the key forces sustaining momentum. Vendors are broadening technology portfolios, regulators are clarifying approval pathways, and healthcare systems are investing in real-time data integration. At the same time, staffing shortages and high capital requirements temper adoption in resource-constrained settings. Long-term growth prospects remain strong as artificial-intelligence tools extend pathogen libraries and as food-safety rules tighten across emerging economies.

Global Microbial Identification Market Trends and Insights

Rapid Adoption of MALDI-TOF MS in Routine Diagnostics

Laboratories now generate species-level identification within minutes rather than hours by using high-throughput MALDI-TOF platforms that process up to 600 samples per hour, matching the accuracy of 16S rRNA sequencing at lower reagent cost. Expanded reference databases covering more than 4,300 species enable the same instrument to support food, pharmaceutical, and clinical workflows. The United States Food and Drug Administration placed these systems in Class II with special controls in June 2025, giving manufacturers a clearer, faster clearance route while preserving safety standards .

Growth of Antimicrobial-Resistance Surveillance Programs

More than 2.8 million AMR infections occurred annually in the United States, resulting in 35,000 deaths, which prompted whole-genome sequencing adoption across surveillance networks. China's national CHINET program reported carbapenem resistance in 10% of Enterobacter isolates by 2021, highlighting convergent global pressure for rapid identification. Timely organism profiling helps pharmacists tailor effective therapy and shorten hospital stays.

High Instrument and Maintenance Costs

Capital expenditure for an advanced MALDI-TOF system can exceed USD 200,000, while service contracts add 10-15% of purchase price each year, restricting uptake in mid-tier hospitals. New Clinical Laboratory Improvement Amendments performance goals adopted in 2024 require tighter sigma metrics, which may oblige smaller labs to upgrade or replace equipment sooner than planned.

Other drivers and restraints analyzed in the detailed report include:

- Rising Food-Safety Regulations in Emerging Economies

- Integration of AI-Powered Spectral Libraries

- Shortage of Skilled Mass-Spectrometry Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Consumables generated 47.15% of 2024 revenues as labs relied on high-volume reagents and media needed for every run, giving the microbial identification market recurring cash flow resilience. Software and services, though smaller, are growing the fastest at 11.78% CAGR as laboratories upgrade to cloud laboratory-information systems that automate data movement and analytics. Next-generation "dark labs" showcasing robotics and AI illustrate how software layers mitigate staffing gaps while boosting throughput .

The shift also highlights a broader move toward subscription licensing for analytics dashboards, offering predictable margins to vendors and quicker payback for users. As quality-control regulations tighten, cloud-hosted platforms that log instrument performance and flag deviations in real time are becoming critical. This software uptake is expected to maintain double-digit growth through 2030, cementing digital processes as a core competitive differentiator across the microbial identification market.

MALDI-TOF MS retained a 57.50% revenue share in 2024 on the strength of unmatched speed-to-result, low per-test cost, and a continuously expanding organism library. The microbial identification market size for MALDI-TOF platforms is still expanding, yet growth is moderating as penetration rises in North America and Europe. PCR and real-time PCR, by contrast, will post the sharpest 12.73% CAGR through 2030 as multiplex panels and point-of-care formats reach primary-care clinics. Four separate FDA clearances for a flagship syndromic PCR analyzer in 2024 illustrate regulatory momentum.

Hybrid workflows are emerging in which laboratories first screen with MALDI-TOF, then reflex to PCR or sequencing for resistance genes, combining breadth with depth. Cross-platform data convergence is spurring new consumable and service bundles, allowing manufacturers to defend share while tapping incremental revenue from complementary molecular assays.

The Microbial Identification Market Report Segments by Products and Services (Instruments, Consumables and More), by Technology (MALDI-TOF, MSPCR & Real-Time and More ), by End User (Hospitals & Clinical Laboratories and More), by Application (Clinical Diagnostics, Pharmaceutical Manufacturing QC and More) and Geography (North America and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America remained the largest revenue contributor in 2024, claiming 39.56% of global spend, reflecting well-funded healthcare systems, reimbursed rapid tests, and robust AMR surveillance grants. Laboratories across the United States leverage the CDC's Antimicrobial Resistance Laboratory Network to adopt connected identification platforms that feed real-time data into national dashboards. Canada follows similar trajectories but faces greater technician shortages, delaying instrument rollouts in smaller provinces.

Asia-Pacific, forecast to rise at 11.45% CAGR, is propelled by public hospital expansion in China and India, harmonized quality standards under ASEAN initiatives, and a vibrant local biomanufacturing base. The CHINET program's multicenter datasets illustrate the region's data maturity and the resulting push for faster organism profiling to guide antibiotic formularies. Governments are also subsidizing instrument purchases for provincial disease-control centers, widening rural access.

Europe maintains moderate growth as stringent In-Vitro Diagnostic Regulation deadlines drive labs to validate platforms earlier than scheduled, ensuring steady demand for compliant kits. The United Kingdom's ESPAUR report cites a 3.5% rise in AMR burden since 2019, keeping rapid identification on policy agendas. Brexit customs changes create occasional supply chain delays, yet continental procurement frameworks largely shield end users from shortages.

The Middle East and Africa region is at an earlier adoption stage but benefits from Gulf state investment in tertiary care facilities and from donor-funded water-pathogen projects. Latin America sees rising food-safety testing volumes as Brazil and Mexico align export requirements with major trade partners, boosting uptake among agro-industry labs.

- bioMerieux

- Bruker

- Beckton Dickinson

- Thermo Fisher Scientific

- Danaher

- Shimadzu

- Charles River

- Biolog

- QIAGEN

- Merck KGaA (MilliporeSigma)

- Liofilchem Srl

- bioNote Inc.

- MIDI Labs

- Eppendorf

- Hologic

- Roche

- Siemens Healthineers

- Revvity (PerkinElmer)

- Abbott Laboratories

- Agilent Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid adoption of MALDI-TOF MS in routine diagnostics

- 4.2.2 Growth of antimicrobial-resistance (AMR) surveillance programs

- 4.2.3 Rising food-safety regulations in emerging economies

- 4.2.4 Integration of AI-powered spectral libraries (under-reported)

- 4.2.5 Expansion of decentralized POCT microbial ID systems (under-reported)

- 4.3 Market Restraints

- 4.3.1 High instrument & maintenance costs

- 4.3.2 Shortage of skilled mass-spectrometry technicians

- 4.3.3 Lack of standardization for environmental isolates (under-reported)

- 4.3.4 Cyber-security risks in cloud-based ID platforms (under-reported)

- 4.4 Value/ Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product & Service

- 5.1.1 Instruments

- 5.1.2 Consumables

- 5.1.3 Software & Services

- 5.2 By Technology

- 5.2.1 MALDI-TOF MS

- 5.2.2 PCR & Real-time PCR

- 5.2.3 Sequencing (NGS, Sanger)

- 5.2.4 Others (Biochemical, Microscopy, etc.)

- 5.3 By End-User

- 5.3.1 Hospitals & Clinical Laboratories

- 5.3.2 Pharmaceutical & Biotechnology Companies

- 5.3.3 Food & Beverage Testing Labs

- 5.3.4 Environmental & Industrial Labs

- 5.4 By Application

- 5.4.1 Clinical Diagnostics

- 5.4.2 Pharmaceutical Manufacturing QC

- 5.4.3 Food Safety & Quality

- 5.4.4 Environmental Monitoring

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 bioMerieux SA

- 6.3.2 Bruker Corporation

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 Thermo Fisher Scientific Inc.

- 6.3.5 Danaher Corporation (Beckman Coulter)

- 6.3.6 Shimadzu Corporation

- 6.3.7 Charles River Laboratories

- 6.3.8 Biolog Inc.

- 6.3.9 Qiagen N.V.

- 6.3.10 Merck KGaA (MilliporeSigma)

- 6.3.11 Liofilchem Srl

- 6.3.12 bioNote Inc.

- 6.3.13 MIDI Labs

- 6.3.14 Eppendorf AG

- 6.3.15 Hologic Inc.

- 6.3.16 Roche Diagnostics

- 6.3.17 Siemens Healthineers

- 6.3.18 Revvity (PerkinElmer)

- 6.3.19 Abbott Laboratories

- 6.3.20 Agilent Technologies

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment