|

시장보고서

상품코드

1842464

외과용 봉합사 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Surgical Sutures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

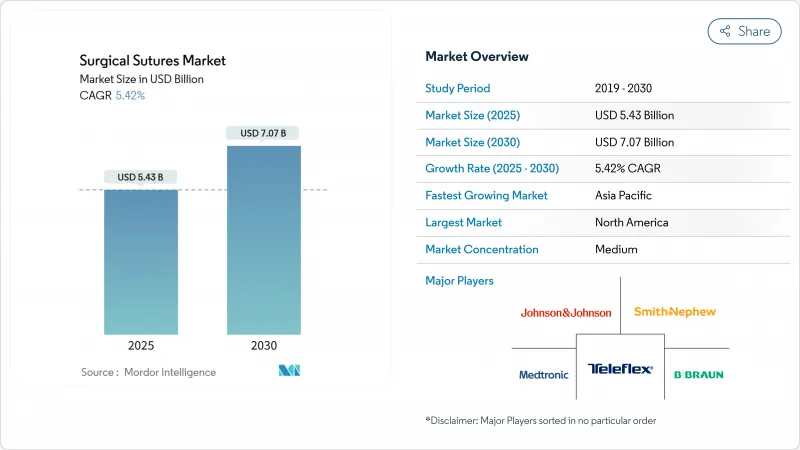

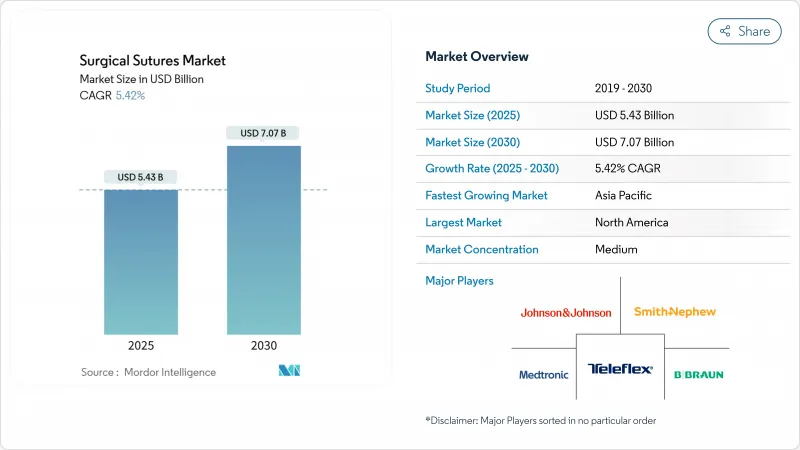

외과용 봉합사 시장 규모는 2025년에 54억 3,000만 달러, 2030년에는 70억 7,000만 달러에 이를 것으로 예상되며, CAGR은 5.42%를 나타낼 전망입니다.

세계 수술 건수 증가, 외래 수술 센터(ASC) 증가, 매듭이 없는 가시 봉합사의 급속한 보급에 의해 각 전문 분야에서 수요가 강화되고 있습니다. 제품 혁신은 항균제를 포함한 합성 흡수성 물질로 이동하고 있으며, 건강 관리 4.0 개념은 결함 및 리콜 위험을 피하기 위해 디지털 공급망 추적을 통합합니다. 고소득 국가에서는 이제 흔한 로봇 지원 수술을 통해 제조업체는 최소한의 촉각 피드백으로 조직을 고정할 수 있는 구조를 만들어야 합니다. 아시아태평양이 가장 빠르게 성장하고 있지만, 북미는 선진 상처 폐쇄 기구에 대한 지속적인 상환 지원으로 여전히 유일한 최대 수익원이 되고 있습니다.

세계의 외과용 봉합사 시장 동향과 인사이트

고령화와 만성질환 부담으로 세계 수술 건수 급증

2024년 메디케어 수급자가 받은 외래 수술 건수는 340만 건으로 전년 대비 5.7% 증가하여 선진국 전체 증가를 반영했습니다. 인구의 고령화와 심혈관계 및 종양의 증례 수가 증가함에 따라 많은 치료가 최종 수단에서 첫 번째 선택 치료로 이동하고 있습니다. 심혈관 외과용 봉합사만으로도 CAGR 5.81%를 나타낼 것으로 예측되며, 지혈을 손상시키지 않고 박동성 스트레스를 견디는 봉합사가 필요합니다. 아시아 신흥국의 생산 능력 증강이 접근을 확대하고 외과용 봉합사 시장에 새로운 수술을 유입시키고 있습니다.

특수 가시 봉합사가 필요한 로봇 지원 수술의 상승

가시철선 봉합사는 CAGR 7.23%를 나타내 성장을 지속하고 있는데, 이는 자기고정 설계에 의해 촉각 피드백이 제한되는 로봇 환경에서의 매듭을 경감할 수 있기 때문입니다. 존슨 엔드 존슨의 STRATAFIX 시리즈의 임상 평가는 출혈량 감소와 함께 수술실의 시간 단축을 확인했습니다. 마이크로서젤리 로봇 시스템에 대한 FDA의 지속적인 인가는 대응가능한 분야를 넓히고 조직을 균일하게 고정하는 보다 얇은 게이지와 양방향 미늘 모양의 설계를 공급자에게 촉구하고 있습니다.

스테이플러, 실란트, MIS 절차 사용 증가로 봉합사 수 감소

스테이플링 플랫폼에는 섬세한 조직을 그립하여 몇 초 안에 폐쇄를 완료하는 텍스처드 가공된 조가 포함되어 기존 봉합사의 양이 줄어듭니다. 반월판과 폐 절개에 적합한 탄성 실란트도 마찬가지로, 특히 트로커 포트가 바늘의 조작성을 제한하는 낮은 침습 수술에서 단일 폐쇄에 필요한 경로 수를 줄입니다.

분석되는 기타 성장 촉진요인 및 억제요인

- 재료 과학의 급속한 진보에 의해 보다 강력한 합성 흡수성 봉합사가 가능하게

- SSI 삭감이 의무화되는 가운데, 항균·약제 용출 봉합사에 대한 수요가 높아진다

- 침침 감염과 직장 안전에 대한 우려

부문 분석

흡수성 봉합사는 2024년 외과용 봉합사 시장 규모의 60.46%를 차지했고, CAGR 5.67%를 나타낼 전망입니다. 폴리글락틴 및 폴리디옥사논으로 대표되는 합성 섬유의 하위 부문은 균일한 흡수 프로파일에 의해 예측 가능한 치유 곡선을 얻을 수 있다는 장점이 있습니다. 이 제품의 대부분은 SSI 위험을 줄이는 항균성 트리클로산 코팅을 실시합니다. 비 흡수성 제품은 심장혈관과 정형외과 수술에서 여전히 필수적이지만, 이전에는 영구적인 지원에 유보되었던 용도가 실란트에 침식되었기 때문에 확장은 완만합니다. 캣갓의 가용성은 윤리적인 조달의 조사에 의해 엄격해지고 있으며, 실험실은 염증을 유발하지 않고 깨끗하게 분해되는 알부민 기반 단백질의 탐구를 촉구하고 있습니다.

개발 파이프라인은 항생제와 성장 인자 저장소를 통합한 전기 방사 흡수체로 붐비고 있습니다. 이러한 섬유는 최소한의 매듭 강도를 최대 4주 동안 유지하면서 국소 치료 페이로드를 제공하고 신속한 퇴원을 중시하는 외래 센터에 매력적인 사양입니다. 천연 실크는 현재도 일부 치과 사례에서 사용되고 있지만, 세균 부착성이 높기 때문에 보급이 늦어지고 있습니다. 따라서 프리미엄 합성 라인은 감염 감소, 직원 편의성 및 환자의 편안함을 중시함으로써 외과용 봉합사 시장에서 더 큰 점유율을 얻고 있습니다.

멀티필라멘트 편조는 뛰어난 유연성과 매듭 안전성으로 인해 2024년 외과용 봉합사 시장 규모의 59.38%를 차지했습니다. 그러나, 가시 봉합사는 셀프 그립 텍스처에 의해 매듭의 스텝이 불필요하게 되어, 복강경하 수술이나 로봇 지원 분야에서의 수술 시간이 단축되기 때문에 CAGR 7.23%를 나타내 성장을 리드하고 있습니다. 초기 임상 프로그램에서 가시 봉합사는 성형 외과 수술에서 효과적이었지만 현재는 부인과 수술과 소화기계 수술에도 적용되어 단위 당 수요를 밀어 올리고 있습니다. 중점에서 외부로 조직을 고정하고 장력을 균등하게 넓히고 이물질 부하를 줄이는 양방향 바브에 대한 투자가 계속되고 있습니다.

모노필라멘트는 저항력과 부드러운 통과성이 결정수가 되는 혈관이식술로 계속 지지되고 있습니다. 새로운 표면 처리 모노 필라멘트는 나노 스케일 텍스처링과 항균 이온을 결합하여 유연성을 희생하지 않고 미생물 내성을 보장합니다. 이러한 개선을 총칭하여 외과용 봉합사 시장은 수술 효율과 수술 후 성적을 극대화하는 프리미엄 구조의 매력을 높여주고 있습니다.

지역 분석

북미는 2024년 세계 수익의 42.53%를 차지했으며, 2030년까지 8억 2,000만 달러 증가가 예상됩니다. 메디케어에 의한 ASC 서비스에 대한 68억 달러의 지출은 수요 수요 회복을 입증하는 반면, 소아과 의사의 부족에 대한 FDA의 경계는 공급을 안정시키는 이중 조달 계약을 촉구하고 있습니다. 존슨 엔드 존슨 등 국산 대기업은 2025년 중 13억 달러를 수술 기구의 연구 개발에 쏟아 부어 이 지역의 기술 혁신에 있어서의 리더십을 확고히 하고 있습니다.

인구동태의 고령화와 CE마크 취득 경로의 조화를 배경으로 유럽은 CAGR 5.28%를 나타낼 전망입니다. 지속가능성 목표로 인해 구매위원회는 환경에 대한 부하를 최소화하는 생분해성 합성수지에 조타를 하고 있습니다. 동유럽의 확대 프로그램은 독일과 프랑스에서 볼 수 있는 프리미엄 혁신과 균형을 맞추면서 중급 제품의 섭취를 창출하고 있습니다.

아시아태평양은 중국과 인도에서 건강 보험 적용 범위가 확대되고 수술 건수가 급증했기 때문에 CAGR이 6.19%를 나타낼 전망입니다. 현지 제조업체는 수입 의존도를 낮추기 위해 폴리프로필렌과 폴리그랙틴의 생산 라인을 확대해, 지역 공급자가 대응 가능한 외과용 봉합사 시장 규모를 확대하고 있습니다. 중동 및 아프리카의 CAGR은 5.74%를 나타내 다과목 병원 프로젝트에 밀려 왔고, 남미의 CAGR은 5.65%를 나타내 브라질과 아르헨티나의 의료 접근 개선을 반영하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 도입

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 고령화와 만성질환에 의한 세계 수술건수 급증

- 신흥국에서의 의료시설의 확대가, 대량의 당일치기 수술을 촉진

- 특수 가시 봉합사를 필요로 하는 로봇 지원/이미지 유도 수술의 대두

- 재료 과학의 급속한 진보에 의해 합성 흡수성 봉합사의 강도가 향상

- SSI 삭감의 의무화에 수반하는 항균 및 약제 용출 봉합사에 대한 수요

- 주요 시장에서 유리한 상환 제도와 의료기기 승인 경로

- 시장 성장 억제요인

- 스테이플러, 실란트, MIS 기술의 사용 증가에 의한 봉합사 수의 감소

- ESG에 의한 카트구트/실크 및 특수 폴리머의 부족

- 리콜과 품질 시스템 감사의 엄격화에 의한 컴플라이언스 비용의 상승

- 침침 감염과 직장의 안전성에 대한 우려

- 공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측

- 제품 유형별

- 흡수성 봉합사

- 천연

- 캐트컷

- 콜라겐

- 합성

- 비크릴

- 폴리글리콜산(PGA)

- 기타 흡수성 합성 봉합사

- 비흡수성 봉합사

- 나일론

- 폴리프로필렌

- 폴리에스터

- 실크

- 기타 비흡수성 봉합사

- 흡수성 봉합사

- 구조별

- 모노필라멘트

- 멀티필라멘트

- 가시형 봉합사

- 용도별

- 일반 외과

- 심혈관 외과

- 정형외과

- 안과 수술

- 신경외과

- 산부인과

- 치과 및 구강외과

- 성형 및 미용 수술

- 기타 용도

- 유통 채널별

- 직접 입찰/GPO

- 오프라인

- 온라인

- 코팅별

- 무코팅

- 코팅

- 최종 사용자별

- 병원

- 외래 수술 센터(ASC)

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 경쟁 벤치마킹

- 시장 점유율 분석

- 기업 프로파일

- Alfresa Holdings Corporation

- Assut Medical SA

- B. Braun Melsungen AG

- Boston Scientific Corp.

- CONMED Corp.

- DemeTECH Corp.

- Dolphin Sutures

- Gunze Limited

- Healthium Medtech Ltd

- Integra LifeSciences Corporation

- International Fiber Corporation

- Johnson & Johnson Services, Inc.

- Kono Seisakusho Co. Ltd.

- Lotus Surgicals Pvt Ltd

- Mani Inc.

- Medtronic plc

- Mellon Medical BV

- Orion Sutures India Pvt Ltd

- Peters Surgical

- Shanghai Pudong Jinhuan Medical Products Co., Ltd.

- Smith & Nephew plc

- Surgical Specialties Corp.

- Teleflex Incorporated

- Unisur Lifecare Pvt. Ltd.

- Weigao Meidcal international Co., Ltd

제7장 시장 기회와 전망

KTH 25.10.28The surgical sutures market size stands at USD 5.43 billion in 2025 and is on track to reach USD 7.07 billion by 2030, advancing at a 5.42% CAGR.

Rising global surgical volumes, the growing footprint of ambulatory surgical centers and rapid uptake of knotless barbed sutures are reinforcing demand across specialties. Product innovation is shifting toward synthetic absorbable materials with embedded antimicrobials, while Healthcare 4.0 initiatives are integrating digital supply-chain tracking to head off shortages and recall risks. Robot-assisted procedures, now commonplace in high-income countries, are pushing manufacturers to tailor constructions that secure tissue under minimal tactile feedback. Asia-Pacific is accelerating fastest, yet North America remains the single-largest revenue pool thanks to sustained reimbursement support for advanced wound-closure devices.

Global Surgical Sutures Market Trends and Insights

Surging global surgical volumes driven by ageing and chronic-disease burden

Medicare beneficiaries underwent 3.4 million outpatient surgeries in 2024, a 5.7% year-over-year rise that mirrors a wider uptick across advanced economies. Population ageing and rising cardiovascular and oncological case loads are shifting many interventions from last resort to first-line treatment. Sutures for cardiovascular surgery alone is forecast to expand at 5.81% CAGR, requiring sutures that withstand pulsatile stress without compromising hemostasis. Capacity buildouts in emerging Asia are broadening access, channeling additional procedures into the surgical sutures market.

Rise of robot-assisted surgery requiring specialized barbed sutures

Barbed sutures record 7.23% CAGR because their self-anchoring design mitigates knot-tying in robotic environments where tactile feedback is limited. Clinical evaluations of Johnson & Johnson's STRATAFIX line found measurable operating-room time savings alongside reduced blood loss. Continued FDA clearances for microsurgical robotic systems are widening the addressable field, encouraging suppliers to engineer finer gauges and bidirectional barb geometries that anchor tissue evenly.

Growing use of staplers, sealants and MIS techniques reducing suture counts

Stapling platforms now incorporate textured jaws that grip delicate tissue and finish closures in seconds, chipping away at traditional suture volumes. Elastic sealants suitable for meniscus and lung incisions are likewise cutting the number of passes required per closure, particularly in minimally invasive surgery where trocar ports limit needle maneuverability.

Other drivers and restraints analyzed in the detailed report include:

- Rapid material-science advances enabling stronger synthetic absorbable sutures

- Demand for antimicrobial and drug-eluting sutures amid SSI-reduction mandates

- Needle-stick infection and workplace-safety concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Absorbable formats generated 60.46% of surgical sutures market size in 2024, advancing at 5.67% CAGR as hospitals seek products that dissolve post-healing and spare patients follow-up removal. The synthetic sub-segment, led by polyglactin and polydioxanone, benefits from uniform absorption profiles that translate to predictable healing curves. Many of these lines carry antimicrobial triclosan coatings that reduce SSI risk. Non-absorbables remain indispensable in cardiovascular and orthopedic procedures but show slower expansion as sealants encroach on applications once reserved for permanent support. Catgut availability is tightening because of ethical sourcing scrutiny, prompting laboratories to explore albumin-based proteins that break down cleanly without triggering inflammation.

The development pipeline is crowded with electrospun absorbables that integrate antibiotic or growth-factor reservoirs. These fibers deliver a local therapeutic payload while retaining minimum knot-pull strength for up to four weeks, a specification attractive to outpatient centers focused on fast discharge. Though natural silk still finds use in select dentistry cases, its higher bacterial adherence is slowing wider uptake. Premium synthetic lines therefore capture a greater share of the surgical sutures market by positioning on infection reduction, staff convenience and patient comfort.

Multifilament braids controlled 59.38% of the surgical sutures market size in 2024, thanks to superior pliability and knot security. However, barbed formats lead growth at 7.23% CAGR because their self-gripping texture removes the knotting step, lowering operation time in laparoscopic and robot-assisted fields. Early clinical programs validated barbed sutures in plastic surgery, but expanded clearances now cover gynecology and digestive procedures, boosting unit demand. Investment continues in bidirectional barbs that lock tissue from the mid-point outward, spreading tension evenly and cutting foreign-body load.

Monofilaments persist in vascular grafting where low drag and smooth passage are decisive. New surface-treated monofilaments combine nano-scale texturing with antibacterial ions, ensuring microbial resistance without sacrificing flexibility. Collectively these refinements heighten the surgical sutures market appeal of premium constructions that maximize theater efficiency and postoperative outcomes.

The Surgical Sutures Market Report is Segmented by Product Type (Absorbable Sutures [Natural and Synthetic] and More), Construction (Monofilament and More), Application (General Surgery and More), Distribution Channel (Offline and More), Coating (Uncoated and Coated), End-User (Hospitals and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 42.53% of global revenue in 2024 and is forecast to add USD 0.82 billion in incremental value by 2030. Medicare's USD 6.8 billion outlay on ASC services evidences resilient procedural demand, while FDA vigilance over pediatric shortages is prompting dual-sourcing agreements that stabilize supplies. Home-grown giants such as Johnson & Johnson funneled USD 1.3 billion into surgical-instrument R&D during 2025, cementing the region's innovation leadership.

Europe advances at 5.28% CAGR on the back of aging demographics and harmonized CE-mark pathways. Sustainability targets are steering purchasing committees toward biodegradable synthetics that minimize environmental burden. Eastern European expansion programs create uptake for mid-tier products, balancing premium innovation seen in Germany and France.

Asia-Pacific records the highest 6.19% CAGR as health-insurance coverage widens and procedure volumes surge in China and India. Local manufacturers are scaling polypropylene and polyglactin lines to cut import reliance, thereby expanding the addressable surgical sutures market size for regional suppliers. Middle East & Africa's 5.74% CAGR is buoyed by multi-specialty hospital projects, while South America's 5.65% trajectory reflects improving healthcare access in Brazil and Argentina.

- Alfresa Holdings Corporation

- Assut Medical SA

- B. Braun

- Boston Scientific

- CONMED Corp.

- DemeTECH Corp.

- Dolphin Sutures

- Gunze Limited

- Healthium Medtech Ltd

- Integra LifeSciences

- International Fiber Corporation

- Johnson & Johnson

- Kono Seisakusho Co. Ltd.

- Lotus Surgicals Pvt Ltd

- Mani Inc.

- Medtronic

- Mellon Medical

- Orion Sutures India Pvt Ltd

- Peters Surgical

- Shanghai Pudong Jinhuan Medical Products Co., Ltd.

- Smiths Group

- Surgical Specialties Corp.

- Teleflex

- Unisur Lifecare

- Weigao Meidcal international Co., Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging global surgical volumes driven by ageing & chronic-disease burden

- 4.2.2 Expansion of healthcare facilities in emerging economies is driving high-volume day surgeries

- 4.2.3 Rise of robot-assisted / image-guided surgery requiring specialized barbed sutures

- 4.2.4 Rapid material science advances enabling stronger synthetic absorbable sutures

- 4.2.5 Demand for antimicrobial & drug-eluting sutures amid SSI-reduction mandates

- 4.2.6 Favorable reimbursement & device-approval pathways in key markets

- 4.3 Market Restraints

- 4.3.1 Growing use of staplers, sealants & MIS techniques reducing suture counts

- 4.3.2 ESG-driven shortages of catgut/silk & specialty polymers

- 4.3.3 Recalls & stricter quality-system audits raising compliance costs

- 4.3.4 Needle-stick infection & workplace-safety concerns

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Absorbable Sutures

- 5.1.1.1 Natural

- 5.1.1.1.1 Catgut

- 5.1.1.1.2 Collagen

- 5.1.1.2 Synthetic

- 5.1.1.2.1 Vicryl

- 5.1.1.2.2 Polyglycolic acid (PGA)

- 5.1.1.2.3 Other Absorbable Synthetic Sutures

- 5.1.2 Non-absorbable Sutures

- 5.1.2.1 Nylon

- 5.1.2.2 Polypropylene

- 5.1.2.3 Polyester

- 5.1.2.4 Silk

- 5.1.2.5 Other Non-absorbable Sutures

- 5.1.1 Absorbable Sutures

- 5.2 By Construction

- 5.2.1 Monofilament

- 5.2.2 Multifilament

- 5.2.3 Barbed Sutures

- 5.3 By Application

- 5.3.1 General Surgery

- 5.3.2 Cardiovascular Surgery

- 5.3.3 Orthopedic Surgery

- 5.3.4 Ophthalmic Surgery

- 5.3.5 Neurological Surgery

- 5.3.6 Obstetrics & Gynecology

- 5.3.7 Dental & Oral Surgery

- 5.3.8 Plastic & Cosmetic Surgery

- 5.3.9 Other Applications

- 5.4 By Distribution Channel

- 5.4.1 Direct Tender / GPO

- 5.4.2 Offline

- 5.4.3 Online

- 5.5 By Coating

- 5.5.1 Uncoated

- 5.5.2 Coated

- 5.6 By End-User

- 5.6.1 Hospitals

- 5.6.2 Ambulatory Surgical Centers

- 5.6.3 Other End-Users

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 Australia

- 5.7.3.5 South Korea

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East and Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East and Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Competitive Benchmarking

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Alfresa Holdings Corporation

- 6.4.2 Assut Medical SA

- 6.4.3 B. Braun Melsungen AG

- 6.4.4 Boston Scientific Corp.

- 6.4.5 CONMED Corp.

- 6.4.6 DemeTECH Corp.

- 6.4.7 Dolphin Sutures

- 6.4.8 Gunze Limited

- 6.4.9 Healthium Medtech Ltd

- 6.4.10 Integra LifeSciences Corporation

- 6.4.11 International Fiber Corporation

- 6.4.12 Johnson & Johnson Services, Inc.

- 6.4.13 Kono Seisakusho Co. Ltd.

- 6.4.14 Lotus Surgicals Pvt Ltd

- 6.4.15 Mani Inc.

- 6.4.16 Medtronic plc

- 6.4.17 Mellon Medical BV

- 6.4.18 Orion Sutures India Pvt Ltd

- 6.4.19 Peters Surgical

- 6.4.20 Shanghai Pudong Jinhuan Medical Products Co., Ltd.

- 6.4.21 Smith & Nephew plc

- 6.4.22 Surgical Specialties Corp.

- 6.4.23 Teleflex Incorporated

- 6.4.24 Unisur Lifecare Pvt. Ltd.

- 6.4.25 Weigao Meidcal international Co., Ltd

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment