|

시장보고서

상품코드

1842477

자동차용 전기 드라이브 액슬 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Automotive Electric Drive Axle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

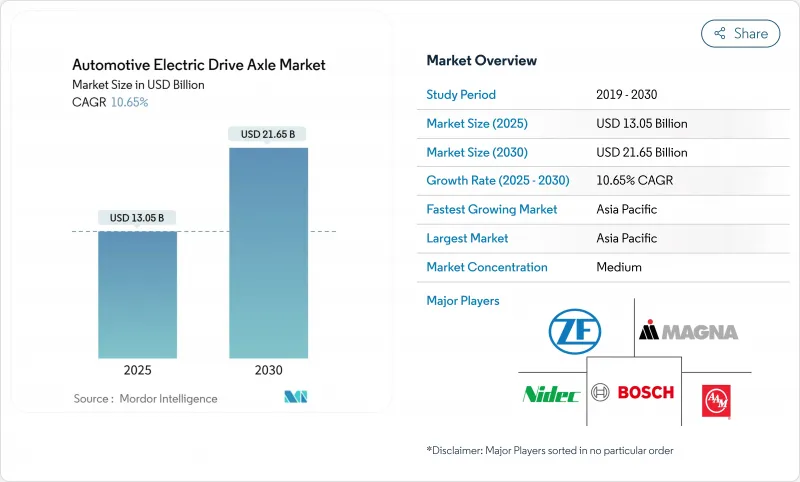

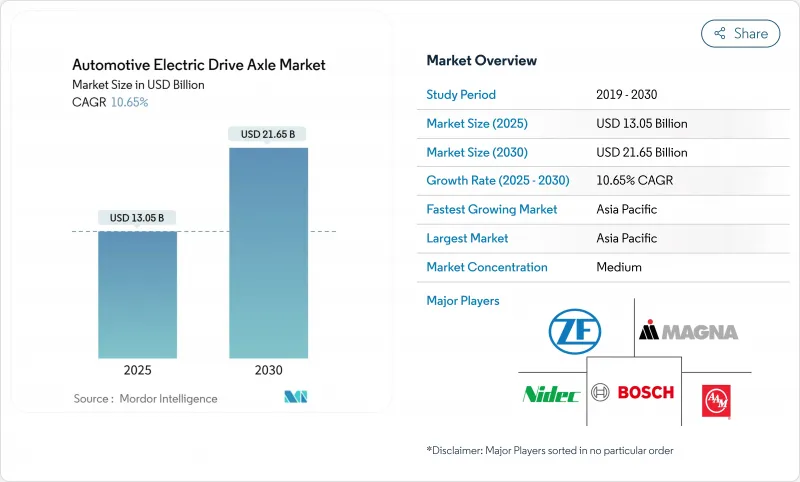

자동차용 전기 드라이브 액슬 시장 규모는 2025년에 130억 5,000만 달러가 되고, 2030년에는 216억 5,000만 달러에 달할 것으로 예측되며, CAGR은 10.65%를 나타낼 전망입니다.

제로 방출 이동성으로의 전환이 가속화되고 차량의 CO2 목표가 의무화되고 배터리 비용 저하가 가속화됨에 따라 E-액슬 공급업체는 꾸준한 대수 전망을 세우고 있습니다. 800V 시스템, 통합형 4-in-1 솔루션의 상승, 아시아태평양의 생산 기지 확대로 비용 곡선이 압축되어 대응 가능한 수요가 확대되고 있습니다. 경쟁적 위치는 열 관리 노하우, 희토류 자석 대체품, 소프트웨어 정의 토크 벡터링 기능을 패키징할 수 있는지 여부에 달려 있습니다. 사용 중 차량용 전환 키트, SUV 및 픽업용 이익률이 높은 듀얼 모터 레이아웃, 국산 드라이브 트레인 컨텐츠에 대한 공적 보조금으로 자동차용 전기 드라이브 액슬 시장 전체에 새로운 수익 풀이 탄생하고 있습니다.

세계의 자동차용 전기 드라이브 액슬 시장 동향 및 인사이트

OEM의 전동화 로드맵이 E 액슬 수요를 가속

세계의 자동차 제조업체의 다년생 생산 목표가 굳어지면서 Tier-1 공급업체는 주문량에 대한 명확한 전망을 가질 수 있게 되어 E-액슬 전용 라인과 현지에서 부품 조달을 위한 대규모 설비 투자를 촉구하고 있습니다. BMW의 노이에 클래스용 6세대 eDrive는 세단, SUV 및 컴팩트 크로스오버의 후륜과 전륜의 레이아웃을 지원하면서 드라이브 트레인의 효율을 20% 향상시킵니다. 제트 에프는 이미 310억 유로의 고전압 e-모빌리티 오더를 획득했으며, 로크인된 로드맵이 어떻게 공급업체에게 구속력 있는 은행 계약에 직결되는지를 입증하고 있습니다.

정부의 제로 배출 의무와 구매 장려금

구속력 있는 판매 할당과 엄격한 위반 처벌로 인해 전자 액슬 채택은 자유 재량에 따른 선택에서 규제 의무로 바뀌고 있습니다. 영국의 ZEV 의무화는 2024년 전기자동차 판매 22%에서 시작되어 2035년까지 100%로 인상되어 드라이브 트레인 비용 프리미엄을 크게 웃도는 위반 차량 1대당 1만 5,000파운드의 벌금이 부과됩니다. 캘리포니아의 선진 클린카 II 규칙은 2035년까지 소형차의 100% 제로 방출 판매를, 2036년까지 중대형 차량의 완전 전환을 의무화하고 있으며, 단기적인 연료 가격 변동에 관계없이 수요를 강화하고 있습니다.

희토류 자석 가격 변동

네오디뮴과 디스프로슘의 가격 변동이 심해 마진 예측 가능성이 저하되어 제조업체는 대체 자석 화학물질과 여자 기술로 향하고 있습니다. 닛산 자동차는 사마륨 철자석으로 대체하여 모터 비용을 30% 절감하는 것을 목표로 하고 있으며, 한 지역에 집중된 공급망에 노출되는 기회를 줄이고 있습니다. GE 에어로스페이스의 23kW 2상 자석 모터는 디스프로슘을 제거하면서도 출력 밀도를 향상시키고, 희토류 재료에서 이행할 때 성능의 타협은 더 이상 불가피하다는 것을 증명합니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

- 배터리 팩의 비용이 80달러/kWh를 밑돌고, E 액슬의 저렴한 가격이 확대

- 전지 구동의 SUV와 픽업의 발매가 급증

- 기존 드라이브 라인에 대한 초기 비용 차이

부문 분석

배터리식 전동 액슬은 2024년 판매 대수의 74.05%를 차지해 자동차용 전기 드라이브 액슬 시장에서 중심적인 존재임이 밝혀졌습니다. 대량 생산 규모, 급속 충전기의 전개, 제로 테일 파이프 배출을 선호하는 정책이 이 리드를 지원하고 있습니다. 하이브리드 E-액슬은 과도적인 듀티 사이클에 대응하고, 연료전지 액슬은 아직 막 시작되었지만, 대형 트럭의 시험 주행이나 버스의 시험 주행을 배경으로 CAGR 11.24%를 나타낼 전망입니다. 연료전지 플랫폼용 자동차용 전기 드라이브 액슬 시장 규모는 Symbio Class 8 트럭용 400kW StackPack 등의 프로젝트에 밀려 수소 인프라와 함께 확대될 것으로 예측됩니다. 캘리포니아의 버스 배치 지원은 장거리 운송의 유망성을 입증합니다.

연료전지 레인지 익스텐더와 국가수소 전략에 대한 OEM의 관심이 높아짐에 따라 파워트레인의 다양성이 점차 퍼져 나가고 있음을 시사하고 있습니다. 모듈형 하우징을 배터리 전기 스택과 연료전지 스택에 모두 적용할 수 있는 공급업체는 함대 운영자가 두 기술을 모두 테스트하는 동안 대수 위험을 헤지할 수 있습니다.

모터, 기어, 인버터를 일체화한 3-in-1 유닛의 점유율은 여전히 42.85%를 차지하고 있으며, 현재의 냉각 범위 내에서 비용 효율적인 패키징을 실현하고 있습니다. 그러나 고객의 RFQ에서는 열 루프도 통합된 4-in-1 레이아웃이 선호되고 있으며, 이 부문의 CAGR은 11.50%를 나타낼 전망입니다. 와이드밴드 갭 반도체가 배열을 줄이고 냉각 회로의 소형화를 가능하게 하기 때문에 4-in-1 설계에 수반되는 자동차용 전기 드라이브 액슬 시장 규모는 더욱 확대될 것으로 예측되고 있습니다. 셰플러 솔루션은 모든 요소를 70kg 모듈로 결합하여 컴팩트한 C-부문 차량에 적합합니다.

지속적인 전력 부하가 필요한 고성능 EV에서는 열의 복잡성이 여전히 채용을 방해하고 있습니다. 공급업체는 상변화물질와 분할 루프 아키텍처에 투자하여 질량을 올리지 않고 피크 전력 창을 확장합니다.

지역 분석

아시아태평양은 2024년 매출의 45.11%를 차지했고 CAGR 12.33%를 나타내며 자동차용 전기 드라이브 액슬 시장의 중심이 되고 있습니다. 중국은 2024년 세계 EV의 70% 이상을 생산해 현지 E 액슬 제조업체에 비교할 수 없는 규모의 우위성을 부여했습니다. 국가 보조금, 배터리 재료의 국내 채굴, 적극적인 할당 목표가 높은 공장 가동률을 유지하고 있습니다. HSBC는 이 지역이 2030년까지 EV 신차 판매의 60% 이상을 차지할 것으로 예측했습니다. 일본의 Tier-1 기업은 신속하게 방향을 바꾸고 있습니다.일본 전산은 저비용의 초소형 EV용으로 소형 E 모터를 최적화하고 있으며, 중견 공급업체는 기술 갭을 메우기 위해 연구 개발력을 결집하고 있습니다.

북미에서는 전동 픽업과 정책 주도의 현지 조달 규칙을 중심으로 기세가 증가하고 있습니다. 인플레이션 삭감법은 소비자 리베이트를 지역 조달의 드라이브 트레인에 연결하고 차축 조립 라인에 대한 새로운 투자를 했습니다. 볼그워너는 미국 OEM 공장에서의 강력한 출시를 반영해 2025년 1분기 e-product 매출이 전년 동기 대비 47% 증가했다고 보고했습니다. 아메리칸 액슬의 e-Beam은 보디온 프레임 플랫폼용 150kW 출력으로 이 트랙의 파도를 타겟으로 하고 있습니다.

유럽은 까다로운 차량 CO2 규정을 뒷받침하는 프리미엄 EV 엔지니어링으로 리드를 유지하고 있습니다. 영국 제로배출차량(ZEV) 의무제도는 2024년 전기차 판매 비중 22%로 시작해 2035년까지 100%로 점진적으로 확대되며, 이를 위반할 경우 차량당 15,000파운드의 벌금이 부과됩니다. 이는 구동계 추가 비용을 실질적으로 상회하는 수준입니다. ZF는 통합 드라이브 라인 솔루션으로 IVECO BUS와 제휴하는 한편, 디지털 섀시 시스템에서 Foxconn을 유치하고 있습니다. 독일 고속도로에서 항속거리 연장을 목표로 하는 브랜드는 열관리 혁신과 800V 채용으로 입찰을 형성하고 있습니다. 한편 신흥의 ASEAN 시장에서는 2035년까지 EV의 CAGR이 16-39%를 나타낼 것으로 보이지만 대규모 차축 조립이 남쪽으로 이동하기 전에 자금조달과 충전 인프라가 성숙해야 합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 도입

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- OEM의 전동화 로드맵이 전기 액슬 수요를 가속

- 정부에 의한 제로 에미션 의무화와 구입 인센티브

- 배터리 팩의 비용이 kWh당 80달러 아래로 하락하며 전기 액슬 접근성 확대

- 배터리 전기자동차 SUV와 픽업 발매 급증

- 차세대 액슬 설계가 필요한 800V 아키텍처로의 전환

- 전기 액슬 데이터 서비스에 의한 소프트웨어 정의 토크 벡터링의 수익화

- 시장 성장 억제요인

- 희토류 자석의 가격 변동

- 기존 드라이브 라인과의 선행 비용차

- OEM의 인소싱에 의한 Tier-1 시장의 축소

- 4-in-1 통합 레벨에서의 열 관리의 한계

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모·성장 예측 : 금액(USD)

- 추진력 유형별

- 배터리 전기 액슬

- 하이브리드 액슬

- 연료전지 전기 액슬

- 통합 레벨별

- 2-in-1(모터, 기어)

- 3-in-1(모터, 기어, 인버터)

- 4-in-1(모터, 기어, 인버터, 열관리)

- 차량 유형별

- 승용차

- 소형 상용차

- 중대형 상용차

- 비도로용 및 특수차(건설 및 농업)

- 판매 채널별

- OEM 장착형

- 애프터마켓 개조 키트

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- ZF Friedrichshafen AG

- Robert Bosch GmbH

- Magna International Inc.

- Nidec Corporation

- American Axle & Manufacturing

- Dana Inc.

- GKN Automotive

- Schaeffler AG

- BorgWarner Inc.

- Aisin Corporation

- Cummins Inc.

- Valeo SA

- Hitachi Astemo

- BYD Co. Ltd.

- Hyundai Mobis

제7장 시장 기회와 전망

KTH 25.10.28The automotive electric drive axle market size is valued at USD 13.05 billion in 2025 and is forecast to reach USD 21.65 billion by 2030, advancing at a 10.65% CAGR.

The accelerating move to zero-emission mobility, mandated fleet CO2 targets, and faster battery cost declines are anchoring steady volume visibility for e-axle suppliers. Model launches built on 800 V systems, the rise of integrated 4-in-1 solutions, and expanded production footprints in Asia-Pacific are compressing cost curves and widening addressable demand. Competitive positioning now hinges on thermal-management know-how, rare-earth magnet alternatives, and the ability to package software-defined torque-vectoring features. Conversion kits for in-service vehicles, higher-margin dual-motor layouts for SUVs and pickups, and public subsidies for domestic drivetrain content are opening additional revenue pools across the automotive electric drive axle market.

Global Automotive Electric Drive Axle Market Trends and Insights

OEM Electrification Road-maps Accelerate E-axle Demand

Firm multi-year production targets from global automakers are giving Tier-1 suppliers unusually clear visibility into order volumes, encouraging larger capital outlays for dedicated e-axle lines and localized component sourcing. BMW's sixth-generation eDrive for the Neue Klasse raises drivetrain efficiency by 20% while supporting both rear- and all-wheel layouts across sedans, SUVs, and compact crossovers. ZF has already booked EUR 31 billion in high-voltage e-mobility orders, demonstrating how locked-in road maps convert directly into binding, bankable contracts for suppliers.

Government Zero-emission Mandates and Purchase Incentives

Binding sales quotas and steep non-compliance penalties are turning e-axle adoption from a discretionary choice into a regulatory requirement. The UK ZEV mandate starts with 22% electric sales in 2024 and climbs to 100% by 2035, backed by GBP 15,000 fines per non-compliant vehicle that materially exceed drivetrain cost premiums. California's Advanced Clean Cars II rule compels 100% zero-emission light-duty sales by 2035 and full medium- and heavy-duty fleet conversion by 2036, cementing demand irrespective of short-term fuel-price swings .

Rare-earth Magnet Price Volatility

Sharp swings in neodymium and dysprosium pricing are eroding margin predictability and pushing manufacturers toward alternative magnet chemistries or excitation technologies. Nissan targets a 30% motor-cost cut by substituting samarium-iron magnets, reducing exposure to supply chains concentrated in one geography. GE Aerospace's 23 kW dual-phase magnetic motor eliminates dysprosium yet improves power density, proving that performance compromises are no longer inevitable when moving away from rare-earth materials .

Other drivers and restraints analyzed in the detailed report include:

- Battery-pack Cost Falls Below USD 80/kWh, Widening E-axle Affordability

- Surge in Battery-electric SUV and Pickup Launches

- Up-front Cost Gap vs. Conventional Drivelines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Battery-electric axles delivered 74.05% of 2024 volumes, underscoring their centrality in the automotive electric drive axle market. Mass-production scale, rapid charger rollouts, and policy preference for zero-tailpipe emissions anchor this lead. Hybrid e-axles address transitional duty cycles, while fuel-cell axles, though nascent, are pacing at an 11.24% CAGR on the back of heavy-duty truck pilots and bus trials. The automotive electric drive axle market size for fuel-cell platforms is projected to rise alongside hydrogen infrastructure, aided by projects such as Symbio's 400 kW StackPack for Class 8 trucks. California's support for bus deployments validates long-haul promise.

Growing OEM interest in fuel-cell range extenders and national hydrogen strategies suggests a gradual broadening of powertrain diversity. Suppliers that can tailor modular housings to either battery-electric or fuel-cell stacks will hedge volume risk as fleet operators experiment with both technologies.

A 42.85% share still resides with 3-in-1 units that merge motor, gear, and inverter, offering cost-effective packaging within current cooling envelopes. Yet customer RFQs now favor 4-in-1 layouts that also integrate thermal loops, lifting that segment at an 11.50% CAGR. The automotive electric drive axle market size attached to 4-in-1 designs is forecast to compound as wide-bandgap semiconductors reduce heat rejection and enable smaller cooling circuits. Schaeffler's solution combines all elements into a 70 kg module that fits compact C-segment vehicles.

Thermal complexity still caps adoption in high-performance EVs where sustained power loads demand separate chillers. Suppliers are investing in phase-change materials and split-loop architectures to extend peak-power windows without raising mass.

The Automotive Electric Drive Axle Market Report is Segmented by Propulsion Type (Battery-Electric Axle, Hybrid Axle, and More), Integration Level (2-In-1 (Motor, and Gear), 3-In-1 (Motor, Gear, and Inverter), and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Sales Channel (OEM-Fitted and Aftermarket Retrofit Kits), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific captured 45.11% of 2024 revenue and is expanding at a 12.33% CAGR, making it the gravitational center of the automotive electric drive axle market. China produced more than 70% of global EVs in 2024, giving local e-axle makers unmatched scale advantages. State subsidies, domestic mining of battery materials, and aggressive quota targets sustain high plant-utilization rates. HSBC forecasts the region will represent over 60% of new EV sales by 2030. Japanese Tier-1s are pivoting quickly: Nidec is optimizing smaller e-motors tailored to low-cost micro EVs, while midsize suppliers are pooling R&D to close technology gaps.

North America is building momentum around electric pickups and policy-driven local content rules. The Inflation Reduction Act ties consumer rebates to regionally sourced drivetrains, steering fresh investment into axle assembly lines. BorgWarner reported a 47% year-on-year rise in e-product sales for Q1 2025, reflecting strong ramp-ups at US OEM plants. American Axle's e-Beam targets this truck wave with 150 kW output for body-on-frame platforms.

Europe maintains a lead in premium EV engineering underpinned by stringent fleet CO2 rules. The 22% electric sales mandate in 2024, moving to 100% by 2035, ensures steady axle demand despite a softer macro backdrop. ZF is partnering with IVECO BUS for integrated driveline solutions while courting Foxconn for digital chassis systems. Thermal-management innovation and 800 V adoption shape tenders as brands strive for extended range on high-speed German motorways. Meanwhile, emerging ASEAN markets eye a 16-39% EV CAGR through 2035, though financing and charging infrastructure must mature before large-scale axle assembly shifts south.

- ZF Friedrichshafen AG

- Robert Bosch GmbH

- Magna International Inc.

- Nidec Corporation

- American Axle & Manufacturing

- Dana Inc.

- GKN Automotive

- Schaeffler AG

- BorgWarner Inc.

- Aisin Corporation

- Cummins Inc.

- Valeo SA

- Hitachi Astemo

- BYD Co. Ltd.

- Hyundai Mobis

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 OEM electrification road-maps accelerate e-axle demand

- 4.2.2 Government zero-emission mandates and purchase incentives

- 4.2.3 Battery-pack cost falls below USD 80/kWh, widening e-axle affordability

- 4.2.4 Surge in battery-electric SUV and pickup launches

- 4.2.5 Shift to 800 V architectures requiring next-gen axle designs

- 4.2.6 Monetization of software-defined torque-vectoring via e-axle data services

- 4.3 Market Restraints

- 4.3.1 Rare-earth magnet price volatility

- 4.3.2 Up-front cost gap vs. conventional drivelines

- 4.3.3 OEM insourcing squeezing Tier-1 addressable market

- 4.3.4 Thermal-management limits at 4-in-1 integration level

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Propulsion Type

- 5.1.1 Battery-Electric Axle

- 5.1.2 Hybrid Axle

- 5.1.3 Fuel-Cell Electric Axle

- 5.2 By Integration Level

- 5.2.1 2-in-1 (Motor, and Gear)

- 5.2.2 3-in-1 (Motor, Gear, and Inverter)

- 5.2.3 4-in-1 (Motor, Gear, Inverter, and Thermal)

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Medium and Heavy Commercial Vehicles

- 5.3.4 Off-Highway and Specialty (Construction and Agriculture)

- 5.4 By Sales Channel

- 5.4.1 OEM-Fitted

- 5.4.2 Aftermarket Retrofit Kits

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 ZF Friedrichshafen AG

- 6.4.2 Robert Bosch GmbH

- 6.4.3 Magna International Inc.

- 6.4.4 Nidec Corporation

- 6.4.5 American Axle & Manufacturing

- 6.4.6 Dana Inc.

- 6.4.7 GKN Automotive

- 6.4.8 Schaeffler AG

- 6.4.9 BorgWarner Inc.

- 6.4.10 Aisin Corporation

- 6.4.11 Cummins Inc.

- 6.4.12 Valeo SA

- 6.4.13 Hitachi Astemo

- 6.4.14 BYD Co. Ltd.

- 6.4.15 Hyundai Mobis

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment