|

시장보고서

상품코드

1842493

콜레라 백신 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Cholera Vaccines - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

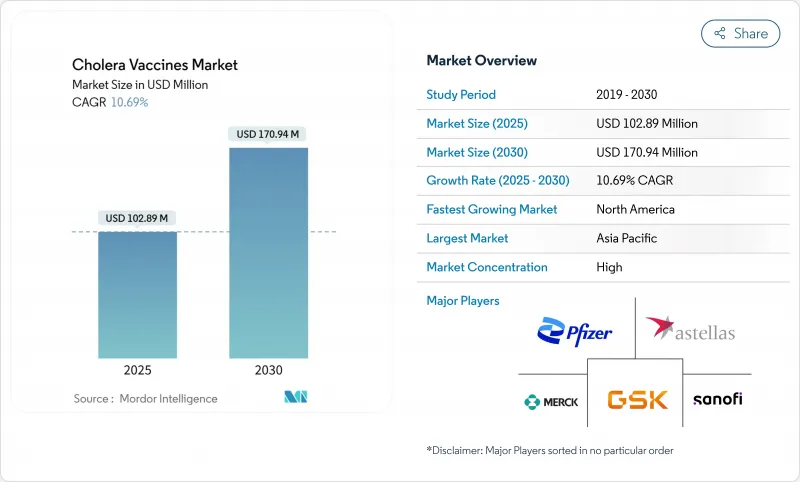

콜레라 백신 시장은 2025년에 1억 289만 달러로 평가되었고, 2030년에 1억 7,094만 달러에 이를 것으로 예측되며, CAGR 10.69%로 성장할 전망입니다.

이러한 전망은 전 세계적으로 전염이 가속화됨에 따라, 사후 대응적인 발병 통제에서 체계적인 예방 접종 프로그램으로의 급격한 전환을 반영합니다. 아시아태평양 지역에서 수요가 급증하고 있으며, 인도, 중국 및 여러 동남아시아 국가들은 기후 관련 홍수와 해수면 온도 상승에 대응하여 계절별 캠페인을 확대하고 있습니다. 공급 측면의 모멘텀도 마찬가지로 강력합니다 : EuBiologics의 단순화된 불활성화 백신 제형과 Gavi의 12억 달러 규모의 아프리카 백신 제조 가속화 프로그램은 생산 능력을 확대하는 동시에 지역적 집중 위험을 완화하고 있습니다. 동시에 단회 접종 생백신과 mRNA 플랫폼은 더 빠른 보호 효과와 신속한 균주 적응을 약속하며, 여행의학과 긴급 대응 분야에서 새로운 상업적 틈새 시장을 창출하고 있습니다. 이러한 요소들이 복합적으로 작용하여, 주기적인 비축량 부족에도 불구하고 콜레라 백신 시장은 가파른 성장 궤도를 유지하고 있습니다.

세계의 콜레라 백신 시장 동향 및 인사이트

다중 대륙에서 아웃브레이크 확대

2024년 12월 기준 33개국이 콜레라 유행을 보고했으며, 이는 역사적 평균의 두 배 이상으로 극한 기후와 인구 이동에 따른 역학 변화가 두드러집니다. 취약한 보건 체계에서 치명률이 상승함에 따라 정부는 순수 대응형 캠페인보다 선제적 예방접종을 추진하고 있어 콜레라 백신 시장의 기본 수요를 끌어올리고 있습니다. 기존 콜레라 비발생 지역으로의 확산은 비축량 요구를 더욱 확대시켜 주문량을 증가시키고 상업적 성장을 지속시키고 있습니다. 보건 기관들은 이제 다년간의 백신 수요를 예측하고 있어, 제조사들에게 생산 능력 투자를 뒷받침하는 강력한 수요 가시성을 제공하고 있습니다. 따라서 유행 빈도 증가는 시장 전망에 가장 큰 긍정적 영향을 미치는 단일 요인입니다.

Gavi OCV 비축 자금 확대

Gavi는 31개국에 2억 3,000만 회분을 공급할 것을 약속했으며 지난 2년간 9,600만 회분의 출하를 기록했습니다. 아프리카 백신 제조 가속화 프로그램은 지역 생산에 12억 달러를 배정하며, 프랑스가 1,000만 유로를 기여함으로써 생산자들의 장기적 조달 안정성을 시사합니다. 예방 캠페인은 사후 대응 캠페인보다 3-4배 많은 백신이 필요해 콜레라 백신 시장을 직접 확대합니다. 보장된 구매 계약은 자본 지출의 위험을 줄이고, 생산 라인 확장을 가속화하며, 아프리카와 아시아로의 기술 이전을 촉진해 궁극적으로 공급 탄력성을 넓힙니다. 이러한 자금 조달 메커니즘은 예측 기간 동안 꾸준한 물량 증가를 가져옵니다.

2회 접종 준수율 격차

대규모 캠페인에서 2차 접종 완료율은 64-73%로 하락하여 인구 면역력을 제한하고 더 단순한 접종 일정에 대한 요구를 촉발합니다. 이주, 생계 활동 간 경쟁, 부적절한 지역사회 메시지 전달 등이 장벽으로 작용합니다. 자가 투여나 연장된 접종 간격과 같은 대체 전달 모델이 접종률을 개선하지만 각각 물류적 복잡성을 가중시킵니다. 이러한 제약은 효과적 커버리지를 감소시키고 단기 성장 전망을 완화시키며, 준수 격차를 해소할 수 있는 단회 접종 방식에 대한 투자를 촉진합니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 기후 연계 해안 홍수 발생 지역 내 메가시티

- 여행 클리닉에서의 생백신 단회 접종 승인

- OMV 컴포넌트 병목 현상

부문 분석

2024년 콜레라 백신 시장의 74.54%를 점유한 경구용 O1 및 O139 불활성화 백신은 수십 년간의 현장 증거와 WHO 사전 인증을 통해 입지를 공고히 했습니다. 해당 부문는 2025년 7,700만 달러로 콜레라 백신 시장 규모에서 가장 큰 비중을 차지했습니다. EuBiologics의 Euvichol-S 라인에서만 생산 능력 증대로 연간 5,000만 회분이 추가되어 공급 탄력성이 강화될 전망입니다. 그러나 재조합 B-서브유닛 개선은 소아 대상 효능 향상을 이끌며, 2030년까지 연평균 복합 성장률(CAGR) 11.34%로 가장 빠르게 성장하는 하위 부문입니다.

생체 내 약독화 후보 약물은 아직 틈새 시장이지만 단회 접종의 편의성을 추구하는 업계 흐름과 부합합니다. Vaxchora는 상업적 잠재력을 보여주는 사례로, 90.3%의 단기 효능과 3개월 후 79.5%의 효능으로 여행자용 백신으로 선호됩니다. 개발 파이프라인에는 냉장 유통망이 필요 없는 식용 쌀 기반 제형과 mRNA 프로토타입이 포함되어 있어, 2027년 이후 경쟁 구도를 재편할 혁신 경쟁이 예상됩니다.

지역 분석

북미는 2024년 매출의 37.67%를 차지했으며, 이는 Vaxchora의 프리미엄 가격 정책과 글로벌 공급 부족 상황에서도 꾸준한 수요를 보장하는 성숙한 여행 건강 인프라에 힘입은 결과입니다. 기업의 의무적 보호 정책은 수요를 더욱 제도화하여 민간 부문의 물량 규모가 인도적 비축 물량 동향으로부터 영향을 받지 않도록 합니다.

아시아태평양 지역은 가장 빠르게 성장하는 지역으로, 인도, 방글라데시, 베트남이 정기적인 우기 전 예방접종으로 전환함에 따라 2030년까지 연평균 11.89%의 성장률을 보일 전망입니다. 국가 시범 사업들은 비용 효율성을 입증하여 다년간 조달을 보장하는 다자간 자금 조달을 유치했습니다. 인도의 신흥 제조 허브는 공급망을 단축하고 운송비를 절감하여 지역 자급자족을 강화할 것입니다.

유럽은 구매자이자 제조업체라는 이중 역할을 유지합니다. 강력한 규제 체계와 사노피의 유연한 바이오생산 시설에 대한 10억 유로 투자로 향후 mRNA 기반 콜레라 백신 후보물질 개발이 지원될 전망입니다. 한편 프랑스와 EU의 개발 원조는 기술 이전을 아프리카로 유도하며, 백신 자립을 글로벌 보건 안보의 핵심 축으로 보는 정책적 입장을 반영하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 다중 대륙 콜레라 발생 증가

- Gavi 2.0에 의한 글로벌 OCV 비축 자금 확대

- 기후변화로 인한 유행 지역 대도시의 해안 홍수

- 여행 클리닉 승인을 획득한 생약독화 단회 투여 제형

- mRNA 기반 신속 항원 전환 백신 플랫폼

- WHO 인도주의 신속 대응 키트에 OCV 통합

- 시장 성장 억제요인

- 대규모 캠페인에서의 2회 접종 준수 문제

- OMV 컴포넌트 제조 병목 현상

- 비유행 고소득 국가에서의 낮은 상업적 유인

- 기존 백신 효능을 약화시키는 하이브리드 O139-O1 균주

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자 및 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 백신 유형별

- 재조합 B 서브유닛의 전체 세포 V. cholerae O1

- 불활성화화 경구 O1 및 O139

- 제품별

- 듀코랄

- 유비콜 플러스

- 박스콜라

- 기타

- 유통 채널별

- 공공

- 민간

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- EuBiologics Co., Ltd.

- Valneva SE

- Emergent BioSolutions Inc.(PaxVax)

- Sanofi(Shantha Biotechnics)

- Incepta Vaccine Ltd.

- GlaxoSmithKline plc

- Merck & Co., Inc.

- Takeda Pharmaceutical Co. Ltd.

- Astellas Pharma Inc.

- Mitsubishi Tanabe Pharma Corporation

- Pfizer Inc.

- Hilleman Laboratories

- Bharat Biotech International Ltd.

- Johnson & Johnson(Janssen Vaccines)

- Serum Institute of India Pvt. Ltd.

- Medigen Vaccine Biologics

- Vabiotech

- Vaxient Inc.

- Vaxarto Inc.

- SK Bioscience Co., Ltd.

- Biological E. Limited

제7장 시장 기회와 전망

HBR 25.10.29The cholera vaccines market stood at USD 102.89 million in 2025 and is forecast to reach USD 170.94 million by 2030, advancing at a 10.69% CAGR.

This outlook reflects a hard pivot from reactive outbreak control toward systematic, preventive immunization programs as global transmission accelerates. Demand is intensifying in Asia-Pacific, where India, China, and several Southeast Asian nations are scaling seasonal campaigns in response to climate-related flooding and rising sea-surface temperatures. Supply-side momentum is equally strong: EuBiologics' simplified killed-vaccine formulation and Gavi's USD 1.2 billion African Vaccine Manufacturing Accelerator are expanding capacity while de-risking geographic concentration. At the same time, single-dose live vaccines and mRNA platforms promise faster protection and rapid strain adaptation, creating new commercial niches in travel medicine and emergency response. Together, these factors keep the cholera vaccines market on a steep growth trajectory despite periodic stockpile shortfalls.

Global Cholera Vaccines Market Trends and Insights

Escalating Multi-Continent Outbreaks

Thirty-three countries reported active cholera outbreaks in December 2024, more than double the historical norm, underscoring shifting epidemiology driven by extreme weather and population displacement . Rising case-fatality ratios in fragile health systems are propelling governments toward pre-emptive vaccination rather than purely reactive campaigns, thereby lifting baseline demand across the cholera vaccines market. Expanded geographic spread into previously cholera-free zones further stretches stockpile requirements, increasing order volumes and sustaining commercial growth. Health agencies are now forecasting vaccine needs on a multi-year basis, giving manufacturers stronger demand visibility that underpins capacity investments. Elevated outbreak frequency therefore exerts the single largest positive influence on the market outlook.

Expanded Gavi OCV Stockpile Funding

Gavi's pledge to supply 230 million doses to 31 countries-and its record 96 million-dose shipment over the past two years-marks the largest coordinated cholera vaccination effort to date. The African Vaccine Manufacturing Accelerator allocates USD 1.2 billion to regional production, with France contributing EUR 10 million, signaling long-term procurement security for producers . Preventive campaigns need three to four times more doses than reactive drives, directly scaling the cholera vaccines market. Guaranteed offtake contracts de-risk capital spending, accelerate line expansions, and encourage technology transfer to Africa and Asia, ultimately broadening supply resilience. Together these funding mechanisms inject consistent volume growth into the forecast period.

Two-Dose Compliance Gaps

Second-dose completion rates dip to 64-73% in mass campaigns, limiting population immunity and prompting calls for simpler schedules. Barriers include migration, competing livelihoods, and inadequate community messaging. Although alternative delivery models-such as self-administration or extended intervals-improve uptake, each adds logistical complexity. The constraint reduces effective coverage and tempers near-term growth projections, catalyzing investment in single-dose approaches that can close the compliance gap.

Other drivers and restraints analyzed in the detailed report include:

- Climate-Linked Coastal Flooding in Endemic Megacities

- Live Single-Dose Approvals in Travel Clinics

- OMV Component Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Killed Oral O1 and O139 vaccines generated 74.54% of the cholera vaccines market in 2024, a position secured by decades of field evidence and WHO prequalification. The segment accounted for the largest cholera vaccines market size portion at USD 77 million in 2025. Capacity gains from EuBiologics' Euvichol-S line alone will add 50 million doses annually, strengthening supply resilience. However, recombinant B-subunit enhancements are unlocking higher pediatric efficacy and, at 11.34% CAGR, are the fastest-advancing sub-segment through 2030.

Live-attenuated candidates, though still niche, match the industry's pivot toward single-dose ease. Vaxchora exemplifies the commercial potential: its 90.3% short-term efficacy and 79.5% at three months position it as the traveler's vaccine of choice. Development pipelines include edible rice-based formulations and mRNA prototypes that could bypass cold chains, underscoring an innovation race likely to re-shape competitive dynamics after 2027.

The Cholera Vaccines Market is Segmented by Vaccine Type (Whole Cell V. Cholerae O1 With Recombinant B-Subunit and Killed Oral O1, and O139), Product (Vaxchora, Dukoral, Euvichol-Plus, and Others), Distribution Channel (Public and Private), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 37.67% of 2024 revenue, propelled by Vaxchora's premium pricing and a mature travel-health infrastructure that guarantees consistent uptake even during global shortages. Corporate duty-of-care policies further institutionalize demand, ensuring that private-sector volumes remain insulated from humanitarian stockpile dynamics.

Asia-Pacific is the fastest-growing territory, advancing at an 11.89% CAGR through 2030 as India, Bangladesh, and Vietnam shift to routine pre-monsoon vaccination. National demonstration projects have validated cost-effectiveness, attracting multilateral financing that secures multiyear procurement. Emerging manufacturing hubs in India will shorten supply chains and curb freight costs, reinforcing regional self-sufficiency.

Europe maintains a dual role as both buyer and manufacturer. Robust regulatory frameworks, coupled with Sanofi's EUR 1 billion investment in flexible bioproduction, support future mRNA-based cholera candidates. Meanwhile, development assistance from France and the EU is channeling technology transfer to Africa, reflecting a policy stance that sees vaccine self-reliance as a pillar of global health security.

- EuBiologics Co., Ltd.

- Valneva

- Emergent BioSolutions Inc. (PaxVax)

- Sanofi (Shantha Biotechnics)

- Incepta Vaccine Ltd.

- GlaxoSmithKline

- Merck

- Takeda Pharmaceuticals

- Astellas Pharma

- Mitsubishi Tanabe Pharma

- Pfizer

- Hilleman Laboratories

- Bharat Biotech International Ltd.

- Johnson & Johnson (Janssen Vaccines)

- Serum Institute of India

- Medigen Vaccine Biologics

- Vabiotech

- Vaxient Inc.

- Vaxarto Inc.

- SK Bioscience Co., Ltd.

- Biological E. Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Incidence of Multi-Continent Cholera Outbreaks

- 4.2.2 Expansion of Global OCV Stockpile Funding by Gavi 2.0

- 4.2.3 Climate-Change Driven Coastal Flooding in Endemic Megacities

- 4.2.4 Live-Attenuated Single-Dose Formulations Winning Travel-Clinic Approvals

- 4.2.5 mRNA-Enabled Rapid Antigen-Switch Vaccine Platforms

- 4.2.6 Integration of OCV in WHO Humanitarian Rapid-Response Kits

- 4.3 Market Restraints

- 4.3.1 Two-Dose Compliance Challenges in Mass Campaigns

- 4.3.2 Manufacturing Bottlenecks for OMV Components

- 4.3.3 Low Commercial Incentive in Non-Endemic High-Income Countries

- 4.3.4 Hybrid O139-O1 Strains Eroding Current Vaccine Efficacy

- 4.4 Regulatory Landscape

- 4.5 Porters Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Vaccine Type

- 5.1.1 Whole cell V. cholerae O1 with Recombinant B-subunit

- 5.1.2 Killed Oral O1 and O139

- 5.2 By Product

- 5.2.1 Dukoral

- 5.2.2 Euvichol-Plus

- 5.2.3 Vaxchora

- 5.2.4 Others

- 5.3 By Distribution Channel

- 5.3.1 Public

- 5.3.2 Private

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 EuBiologics Co., Ltd.

- 6.3.2 Valneva SE

- 6.3.3 Emergent BioSolutions Inc. (PaxVax)

- 6.3.4 Sanofi (Shantha Biotechnics)

- 6.3.5 Incepta Vaccine Ltd.

- 6.3.6 GlaxoSmithKline plc

- 6.3.7 Merck & Co., Inc.

- 6.3.8 Takeda Pharmaceutical Co. Ltd.

- 6.3.9 Astellas Pharma Inc.

- 6.3.10 Mitsubishi Tanabe Pharma Corporation

- 6.3.11 Pfizer Inc.

- 6.3.12 Hilleman Laboratories

- 6.3.13 Bharat Biotech International Ltd.

- 6.3.14 Johnson & Johnson (Janssen Vaccines)

- 6.3.15 Serum Institute of India Pvt. Ltd.

- 6.3.16 Medigen Vaccine Biologics

- 6.3.17 Vabiotech

- 6.3.18 Vaxient Inc.

- 6.3.19 Vaxarto Inc.

- 6.3.20 SK Bioscience Co., Ltd.

- 6.3.21 Biological E. Limited

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment