|

시장보고서

상품코드

1842499

화염 감지기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Flame Detectors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

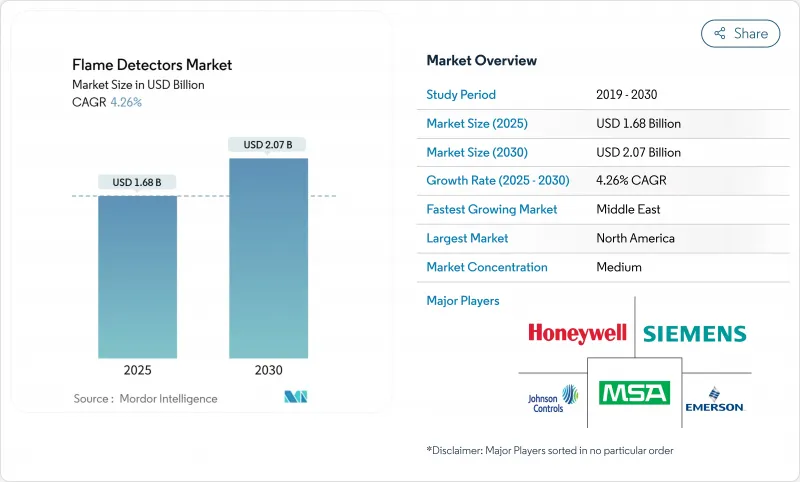

화염 감지기 시장 규모는 2025년에 16억 8,000만 달러, 2030년에는 20억 7,000만 달러에 이를 것으로 예상되며, CAGR은 4.26%에 달할 전망입니다.

탄화수소 시설에 설치된 대규모 베이스가 교환 수요를 안정시키는 한편, 신규 설치는 리튬 이온 전지 창고, 데이터센터, 수소염이 새로운 검출 과제를 낳는 그린 수소 전해조 플랜트로 변화하고 있습니다. 세계적인 안전 규칙의 엄격화, 특히 SIL-2 인증이 기본 요건으로 승격한 ATEX Zone-0의 최신 업데이트는 불쾌한 알람과 다운타임을 최소화하는 멀티스펙트럼 적외선(IR)과 AI를 탑재한 시각 이미지 검출기에 구매자를 유도하고 있습니다. 카타르와 사우디아라비아에서의 LNG 메가트레인 건설은 프로젝트 파이프라인을 확장하고 프리미엄 솔루션에 유리한 고성능 벤치마크를 설정합니다. 이와 병행하여 북미의 보험사는 보험 적용 조건과 초저오보 경보 사양을 연결하여 운영 리스크와 총소유비용을 모두 절감하는 고도로 진단 기능이 풍부한 디바이스 조달에 효과적으로 방향타를 자릅니다.

세계의 화염 감지기 시장 동향과 인사이트

LNG 메가트레인 건설이 멀티스펙트럼 IR 채용을 뒷받침

노스필드 확장 및 재프라가스 개발과 같은 중동 LNG 프로젝트에는 넓은 분리기 및 저장 탱크 전체에서 탄화수소 화재를 추적할 수 있는 검출기가 필요합니다. 플랜트의 소유자는 태양 복사 간섭을 극복하기 위해 다중 스펙트럼 IR 유닛을 지정하고 있으며, 멀티밴드 광학 어레이와 내장 진단 기능을 갖춘 고급 공급업체가 요구에 부응합니다. 무인화된 프로세스 영역에서는 99.9%의 디바이스 가용성에 대한 필요성이 향상되었으며, 자산 무결성 팀은 시간 기반 유지보수 모델에서 임베디드 상태 모니터링에 의존하는 상태 기반 유지보수 모델로 전환하고 있습니다.

FM 5560의 리튬 이온 배터리 데이터센터 수요

FM 5560은 에너지 저장 어레이의 검출 규칙을 규정하고 있으며, 하이퍼스케일 오퍼레이터는 열 폭주가 확대되기 전에 전해질 오프 가스 시그니처를 인식하는 다기준 화염 검출기를 기존 사이트로 개조하도록 촉구하고 있습니다. 2024년 국제소방법에서는 NFPA855의 의무가 추가되어 설치된 축전량이 50kWh를 초과하는 시설의 컴플라이언스 타임라인이 엄격화되었습니다. 시스템 통합자는 성공적인 배터리 모듈의 열 프로파일을 학습하는 AI 분류기를 통합하여 수익이 중요한 컴퓨팅 클러스터를 방관하는 스퓨리어스 트립을 피합니다.

저가의 중국제 적외선 카메라가 프리미엄 수익을 침식

중국의 서멀 이미징 벤더는 구미의 동등 제품보다 40-60% 싼 가격의 적외선 화염 감지기를 출시하고 있으며, SIL-2 평가를 의무화하지 않은 중견 산업 현장에서 인기를 끌고 있습니다. 유럽과 미국의 제조업체는 오 경보 감소 및 서비스 간격 연장을 수익화하는 수명주기 비용 모델로 대응하고 있습니다.

부문 분석

적외선 기기는 2024년 매출의 41.8%를 차지하고 탄화수소 화재의 신뢰성과 긴 실적을 가진 화염 감지기 시장을 지지했습니다. 정유소, 터미널, 석유화학 플랜트에서의 채용이 계속되고 있으며, 유저는 입증된 싱글 채널 광학계를 평가했습니다. 그러나 다중 스펙트럼 IR 하위 카테고리는 3개 이상의 파장 대역을 혼합하고 태양 눈부심과 고온 표면의 반사를 제거하기 때문에 CAGR 5.2%를 나타낼 것으로 예측됩니다. 무인 LNG 트레인 운영자는 고액의 자본 지출을 비용이 많이 드는 프로세스 종료에 대한 합법적인 보험으로 간주합니다. 알고리즘이 성숙하고 가격대가 낮아지고 감지와 근본 원인을 동시에 분석할 수 있어 시각적 화염 영상이 급성장하고 있습니다. UV 검출기는 수소 및 금속 연소의 위험에 대한 틈새 솔루션입니다. UV/IR을 결합한 유닛은 혼합 연료 설비의 성능과 비용의 균형을 유지합니다.

동시에 AI 지원 센서 펌웨어는 검출기를 엣지 컴퓨팅 노드로 전환하여 렌즈의 흐림과 광학적 열화를 자체 진단합니다. 원격 펌웨어 업그레이드는 유지 보수주기를 더욱 단축합니다. 이러한 추세는 사이버 보안에 대한 우려에도 불구하고 설계, 조달 및 건설(EPC) 팀이 클라우드 연결 장치를 지정하도록 촉구하고 있습니다. 화염 감지기 시장이 혜택을 받는 이유는 예측 분석이 보증 기간을 초과하는 부가가치 서비스 계약을 지원하고 통합 소프트웨어 로드맵이 있는 제조업체의 애프터마켓 마진을 밀어 올리기 때문입니다.

고정식 검출기는 2024년 매출의 86.7%를 차지하며 공정 영역, 부두의 적재 지점, 컴프레서 스테이션에서 연속 존 커버리지의 핵심 제품으로 계속되었습니다. 자산의 라이프사이클에 걸쳐 레이아웃이 거의 변경되지 않기 때문에 수요는 그린필드 프로젝트보다는 교체 및 규제 업그레이드에 연결됩니다. 그러나 휴대용 감지기는 운영자가 테스트 바이 터치의 안전 절차를 채택함에 따라 CAGR 6.1%로 가속화되고 있습니다. 검사팀은 생산을 중단하지 않고 턴어라운드 중에 고정 시스템의 무결성을 검증하고, 응급대원은 미지의 현장을 신속하게 평가하기 위해 핸드헬드 유닛을 휴대하고 있습니다.

배터리 밀도의 향상으로 고정 플랫폼과 동등한 감도를 유지하면서 휴대용 디바이스의 미션 시간은 2배가 되었습니다. 튼튼한 케이스와 본질안전방폭규격으로 Zone-1의 장소에서도 안전하게 사용할 수 있게 되었습니다. 그 결과 경쟁 관계가 아닌 보완 관계가 탄생했습니다. 휴대형 기기의 보급이 고정형 기기 수요를 카니버리화하는 것이 아니라, 유지관리 사이클마다 추가 수익이 가져오게 되었습니다. 따라서, 화염 감지기 시장은 동일한 설치 기지에서 두 개의 수익원을 얻을 수 있습니다. 즉, 고정 포인트에 대한 자본 지출과 휴대용 검증 장비에 대한 운영 지출입니다.

지역 분석

북미는 2024년 매출의 32.4%를 차지하며, 화염 감지기 시장을 선도했습니다. 이는 보험료와 초저오보율을 연결시키는 보험의 의무화에 뒷받침되었습니다. 성숙한 정제·화학자산이 꾸준한 교환주기를 촉진하고 FM 5560에 따른 새로운 규칙이 시설당 검출기 수를 확대하고 있습니다. 이 지역은 또한 어드레싱 가능한 스마트 루프의 선구자이며 네트워크의 탄력성을 보험 인수자와 규제 당국에 보장하는 사이버 보안 프레임 워크에 지원됩니다.

중동은 2030년까지 연평균 복합 성장률(CAGR) 예측이 6.2%를 나타낼 전망입니다. 이는 트레인, 저장 및 부두의 각 지역에서 엄격한 화염 모니터링이 필요한 2,000억 달러의 LNG 확장으로 인한 것입니다. 사막의 가혹한 조건에서 스테인레스 스틸 하우징, 창문 히터 및 모래 마모를 예측하는 광학 진단이 선호됩니다. 카타르에서 성공적인 배치는 인근 GCC 국가들로 퍼져 세계적인 사양을 형성하는 기술의 등대 효과를 창출하고 있습니다.

유럽에서는 ATEX Zone-0 및 SIL-2 지침 업데이트에 대응하기 위해 검출기 리노베이션에 대한 투자가 계속되고 있습니다. 다국적 석유화학 사업자들은 세계 기지에서 동일한 인증 모델을 표준화하고 대륙을 넘어 교환 수요를 확대하고 있습니다. 기타 아시아태평양의 성장은 산업전화의 과제에 달려 있으며, 특히 일본과 한국의 수소 로드맵은 전해조 홀의 UV/IR 검출기 수를 증가시키고 있습니다. 남미의 해양 프레솔트 광구에서는 심해 생산 덱에서 플레어 번들을 식별하기 위해 AI를 활용한 시각적 이미징이 필요합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 중동에서의 LNG 메가트레인 건설이 멀티 스펙트럼 적외선 검출기 수요를 가속

- FM 5560에 대응하기 위한 리튬 이온 배터리 데이터센터에의 화염 검출기의 급속한 도입

- ATEX 및 IECex Zone-0 개정에 의한 SIL-2 인증 검출기의 의무화(유럽)

- 오프쇼어 FPSO 레트로 피트에 AI를 활용한 비주얼 화염 이미징을 채용(브라질, 북해)

- 그린 수소 전해조의 설치가 UV/IR 검출기의 판매를 촉진(아시아)

- 초저오경보 사양을 요구하는 보험 인수 업자(미국과 캐나다)

- 시장 성장 억제요인

- 저가의 중국제 IR 카메라가 프리미엄 검출기의 수익 억제

- 갱내 채광에서의 채용을 제한하는 더러운 광학계 유지관리의 다운타임

- FM과 EN54-10의 인증 사이클의 길이가 제품 발매 지연

- 중요 인프라에서 네트워크화된 검출기에 대한 사이버 보안 문제

- 업계 생태계 분석

- 규제와 기술의 전망

- Porter's Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측(금액)

- 제품 유형별

- 자외선(UV)

- 적외선(IR)

- 자외선/적외선(UV/IR)

- 다중 스펙트럼 적외선(트리플/쿼드)

- 가시광선 화염 영상

- 가스 및 화염 복합 감지기

- 설치 유형별

- 고정형 화염 감지기

- 휴대용/핸드헬드 화염 감지기

- 서비스별

- 설계, 설치 및 시운전

- 검사, 시험 및 유지보수

- 개조 및 교체

- 통신/루프별

- 주소 지정 가능(스마트) 감지기

- 기존 감지기

- 최종 사용자 산업별

- 석유 및 가스(업스트림, 중류, 하류)

- 화학 및 석유화학

- 에너지 및 발전

- 제조 및 공정 산업

- 광업 및 금속

- 항공우주 및 방위

- 창고, 물류 및 데이터센터

- 해양 및 해양 플랫폼

- 상업 및 공공 인프라

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 북유럽

- 기타 유럽

- 남미

- 브라질

- 기타 남미

- 아시아태평양

- 중국

- 일본

- 인도

- 동남아시아

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 걸프 협력 회의 회원국

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장의 집중

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- Honeywell International Inc.

- Emerson Electric Co.(Det-Tronics, Spectrex)

- Johnson Controls plc(Tyco)

- MSA Safety Inc.

- Siemens AG

- Bosch Security Systems BV

- Dragerwerk AG and Co. KGaA

- Teledyne Gas and Flame(Simtronics, Oldham)

- 3M Co.(Scott Safety)

- Micropack Engineering Ltd.

- FLIR Systems(Teledyne)

- Hochiki Corporation

- Crowcon Detection Instruments Ltd.

- Fike Corporation

- Minimax Viking GmbH

- Firefly AB

- Sense-WARE Fire and Gas Detection BV

- Omniguard Flame Detectors

- General Monitors(now part of MSA)

- Kidde Fire Safety(Carrier)

제7장 시장 기회와 전망

KTH 25.11.05The flame detector market size stood at USD 1.68 billion in 2025 and is expected to reach USD 2.07 billion by 2030, translating into a 4.26% CAGR.

A sizable installed base across hydrocarbon facilities will keep replacement demand steady, while new installations are shifting toward lithium-ion battery warehouses, data centers and green-hydrogen electrolyser plants where hydrogen flames create novel sensing challenges. Stricter global safety rules-most notably the latest ATEX Zone-0 update that elevates SIL-2 certification to a baseline requirement-are nudging buyers toward multi-spectrum infrared (IR) and AI-equipped visual imaging detectors that minimise nuisance alarms and downtime. LNG mega-train construction in Qatar and Saudi Arabia is broadening project pipelines and setting higher performance benchmarks that favour premium solutions. In parallel, North American insurance carriers are linking coverage terms to ultra-low false-alarm specifications, effectively steering procurement toward advanced, diagnostics-rich devices that lower both operational risk and total cost of ownership.

Global Flame Detectors Market Trends and Insights

LNG mega-train construction boosting multi-spectrum IR adoption

Middle Eastern LNG projects such as the North Field expansion and Jafurah gas development require detectors that can track hydrocarbon fires across wide separators and storage tanks. Plant owners are specifying multi-spectrum IR units to overcome solar radiation interference, a mandate that is elevating premium vendors with multi-band optical arrays and built-in diagnostics. Unmanned process areas reinforce the need for 99.9% device availability, and asset-integrity teams are migrating from time-based to condition-based maintenance models that rely on embedded health monitoring.

Lithium-ion battery data-center demand under FM 5560

FM 5560 now sets detection rules for energy-storage arrays, prompting hyperscale operators to retrofit existing sites with multi-criteria flame detectors that recognise electrolyte off-gas signatures before thermal runaway escalates. The 2024 International Fire Code adds NFPA 855 obligations, tightening compliance timelines for facilities exceeding 50 kWh of installed storage. System integrators are embedding AI classifiers that learn normal battery-module heat profiles to avoid spurious trips that may sideline revenue-critical compute clusters.

Low-cost Chinese IR cameras eroding premium revenue

Thermal-imaging vendors from China are releasing IR flame detectors priced 40-60% lower than Western equivalents, gaining traction in mid-tier industrial sites that do not mandate SIL-2 ratings . Western manufacturers are countering with lifecycle cost models that monetise false-alarm reductions and longer service intervals.

Other drivers and restraints analyzed in the detailed report include:

- ATEX and IECEx Zone-0 revisions mandating SIL-2 detectors

- Offshore FPSO retrofits adopting AI-enabled visual imaging

- Dirty-optics downtime limiting underground-mining uptake

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Infrared devices captured 41.8% of 2024 revenue, underpinning the flame detector market with a long record of hydrocarbon-fire reliability. Adoption persists in refineries, terminals and petrochemical plants where users value proven single-channel optics. Yet the multi-spectrum IR sub-category is forecast to expand at 5.2% CAGR because it blends three or more wavelength bands to reject solar glare and hot-surface reflections. Operators in unmanned LNG trains see the higher capital spend as justifiable insurance against costly process shutdowns. Visual flame imaging is growing fastest as algorithms mature and price points fall, allowing simultaneous detection and root-cause analytics. UV detectors remain the niche solution for hydrogen or metal-combustion risks, while combined UV/IR units balance performance and cost in mixed-fuel installations.

In tandem, AI-ready sensor firmware is turning detectors into edge-computing nodes that self-diagnose lens obscuration and optical degradation. Remote firmware upgrades further shorten maintenance cycles. This trend is nudging engineering, procurement and construction (EPC) teams to specify cloud-connected devices despite cybersecurity reservations. The flame detector market benefits because predictive analytics underpin value-added service agreements that stretch beyond warranty periods, boosting aftermarket margins for manufacturers with integrated software roadmaps.

Fixed detectors delivered 86.7% of 2024 billings and remain the backbone for continuous zone coverage in process areas, jetty off-loading points and compressor stations. Layouts rarely change over asset lifecycles, keeping demand tied to replacement and regulatory upgrades rather than greenfield projects. Portable detectors, however, are accelerating at a 6.1% CAGR as operators adopt test-before-touch safety procedures. Inspection teams validate fixed-system integrity during turnarounds without halting production, and first responders carry handheld units to quickly assess unknown scenes.

Battery density improvements have doubled mission time for portable devices while maintaining sensitivity parity with fixed platforms. Rugged enclosures and intrinsically safe ratings now enable safe use in Zone-1 locations. The result is a complementary relationship rather than a competitive one: rising portable uptake does not cannibalise fixed demand but instead banks additional revenue on every maintenance cycle. The flame detector market therefore gains two revenue streams from the same installed base: capital expenditure on fixed points and operational expenditure on portable verification equipment.

The Flame Detectors Market Report is Segmented by Product Type (Ultraviolet (UV), Infrared (IR), and More), Mounting Type (Fixed Flame Detectors, and More), Service (Design, Installation and Commissioning, and More), Communication/Loop (Addressable (Smart) Detectors, and More), End-User Industry (Oil and Gas, Manufacturing and Process Industries, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the flame detector market with 32.4% of 2024 revenue, supported by insurance mandates that link policy premiums to ultra-low false-alarm rates. Mature refining and chemical assets drive steady replacement cycles, and new rules under FM 5560 are expanding detector counts per facility. The region also pioneers addressable smart loops, backed by cybersecurity frameworks that assure underwriters and regulators of network resilience.

The Middle East shows the highest 6.2% CAGR forecast to 2030 thanks to USD 200 billion in LNG expansions that require stringent flame supervision across train, storage and jetty areas. Harsh desert conditions favour stainless-steel housings, window heaters and optical diagnostics that predict sand abrasion. Successful deployments in Qatar are migrating to neighbouring GCC states, creating a technology lighthouse effect that shapes global specifications.

Europe continues to invest in detector retrofits to comply with the updated ATEX Zone-0 and SIL-2 mandates. Multinational petrochemical operators are standardising on the same certified model across global sites, amplifying replacement demand beyond the continent. Asia-Pacific's growth rests on industrial electrification agendas, notably Japan and South Korea's hydrogen roadmaps that elevate UV/IR detector counts in electrolyser halls.. South America's offshore pre-salt finds need AI-enabled visual imaging to discriminate flare bundles from deep-sea production decks.

- Honeywell International Inc.

- Emerson Electric Co. (Det-Tronics, Spectrex)

- Johnson Controls plc (Tyco)

- MSA Safety Inc.

- Siemens AG

- Bosch Security Systems B.V.

- Dragerwerk AG and Co. KGaA

- Teledyne Gas and Flame (Simtronics, Oldham)

- 3M Co. (Scott Safety)

- Micropack Engineering Ltd.

- FLIR Systems (Teledyne)

- Hochiki Corporation

- Crowcon Detection Instruments Ltd.

- Fike Corporation

- Minimax Viking GmbH

- Firefly AB

- Sense-WARE Fire and Gas Detection B.V.

- Omniguard Flame Detectors

- General Monitors (now part of MSA)

- Kidde Fire Safety (Carrier)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 LNG Mega-train Construction in Middle East Accelerating Multi-Spectrum IR Detector Demand

- 4.2.2 Rapid Deployment of Flame Detectors in Lithium-ion Battery Data-Centers to Meet FM 5560

- 4.2.3 ATEX and IECEx Zone-0 Revisions Mandating SIL-2 Certified Detectors (Europe)

- 4.2.4 Offshore FPSO Retrofits Adopting AI-Enabled Visual Flame Imaging (Brazil and North Sea)

- 4.2.5 Green-Hydrogen Electrolyser Installations Driving UV/IR Detector Sales (Asia)

- 4.2.6 Insurance Underwriters Requiring Ultra-Low False-Alarm Specifications (United States and Canada)

- 4.3 Market Restraints

- 4.3.1 Low-Cost Chinese IR Cameras Cannibalising Premium Detector Revenue

- 4.3.2 Dirty-Optics Maintenance Downtime Limiting Uptake in Underground Mining

- 4.3.3 Lengthy FM and EN54-10 Certification Cycles Delaying Product Launch

- 4.3.4 Cybersecurity Concerns over Networked Detectors in Critical Infrastructure

- 4.4 Industry Ecosystem Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Product Type

- 5.1.1 Ultraviolet (UV)

- 5.1.2 Infrared (IR)

- 5.1.3 Ultraviolet/Infrared (UV/IR)

- 5.1.4 Multi-Spectrum IR (Triple/Quad)

- 5.1.5 Visual Flame Imaging

- 5.1.6 Combined Gas and Flame Detectors

- 5.2 By Mounting Type

- 5.2.1 Fixed Flame Detectors

- 5.2.2 Portable/Hand-held Flame Detectors

- 5.3 By Service

- 5.3.1 Design, Installation and Commissioning

- 5.3.2 Inspection, Testing and Maintenance

- 5.3.3 Retrofit and Replacement

- 5.4 By Communication/Loop

- 5.4.1 Addressable (Smart) Detectors

- 5.4.2 Conventional Detectors

- 5.5 By End-User Industry

- 5.5.1 Oil and Gas (Up-, Mid-, Down-stream)

- 5.5.2 Chemicals and Petrochemicals

- 5.5.3 Energy and Power Generation

- 5.5.4 Manufacturing and Process Industries

- 5.5.5 Mining and Metals

- 5.5.6 Aerospace and Defense

- 5.5.7 Warehousing, Logistics and Data-Centers

- 5.5.8 Marine and Offshore

- 5.5.9 Commercial and Public Infrastructure

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Nordics

- 5.6.2.5 Rest of Europe

- 5.6.3 South America

- 5.6.3.1 Brazil

- 5.6.3.2 Rest of South America

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South-East Asia

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Gulf Cooperation Council Countries

- 5.6.5.1.2 Turkey

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Honeywell International Inc.

- 6.4.2 Emerson Electric Co. (Det-Tronics, Spectrex)

- 6.4.3 Johnson Controls plc (Tyco)

- 6.4.4 MSA Safety Inc.

- 6.4.5 Siemens AG

- 6.4.6 Bosch Security Systems B.V.

- 6.4.7 Dragerwerk AG and Co. KGaA

- 6.4.8 Teledyne Gas and Flame (Simtronics, Oldham)

- 6.4.9 3M Co. (Scott Safety)

- 6.4.10 Micropack Engineering Ltd.

- 6.4.11 FLIR Systems (Teledyne)

- 6.4.12 Hochiki Corporation

- 6.4.13 Crowcon Detection Instruments Ltd.

- 6.4.14 Fike Corporation

- 6.4.15 Minimax Viking GmbH

- 6.4.16 Firefly AB

- 6.4.17 Sense-WARE Fire and Gas Detection B.V.

- 6.4.18 Omniguard Flame Detectors

- 6.4.19 General Monitors (now part of MSA)

- 6.4.20 Kidde Fire Safety (Carrier)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment