|

시장보고서

상품코드

1842506

음향 광학 장치 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Acousto Optic Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

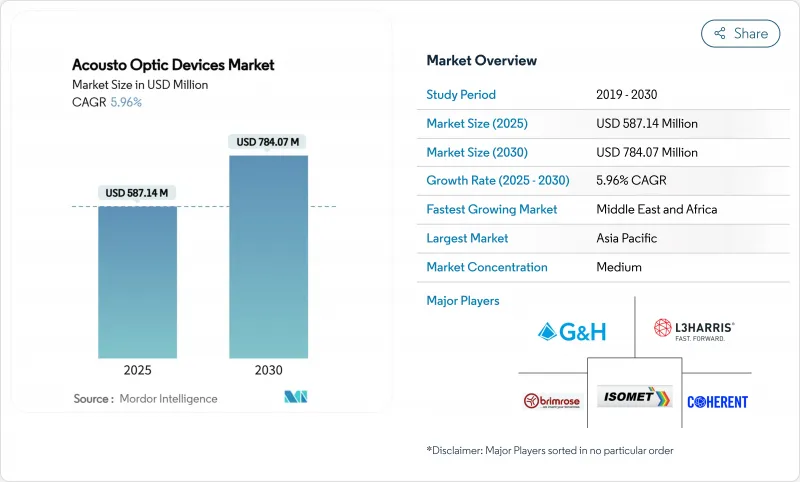

음향 광학 장치 시장은 2025년에 5억 8,714만 달러로 평가되었고, 2030년에 7억 8,407만 달러에 이를 것으로 예측됩니다.

이 같은 성장은 5G 네트워크 노드, 반도체 리소그래피 라인, 차세대 레이저 시스템 내 고정밀 광학 제어 기술의 활용 확대에서 비롯됩니다. 제조사들은 수직 통합을 통해 원자재 부족에 대비하고 리드 타임을 단축하는 한편, 가변 필터에 대한 지속적인 연구개발로 하이퍼스펙트럼 이미징 및 양자 광학 분야에서 새로운 수익원을 창출하고 있습니다. 서브마이크론 레이저 가공 수요, 의료 기기에서 TeO2 기반 Q-스위치 채택 증가, 항공우주 분야의 소형 빔 스티어링 솔루션 수요가 경쟁 전략을 형성하고 있습니다. 음향광학 장치 시장은 방위 등급 LiDAR 및 위성 탑재 분광기에 대한 공공 부문 지출의 혜택도 받고 있어, 방사선 내성 설계 전문 공급업체에게 유리한 환경을 조성하고 있습니다.

세계의 음향 광학 장치 시장 동향 및 인사이트

아시아 반도체 공장에서 초고속 레이저 미세 가공 능력 확대

주요 아시아 파운드리 전반에 걸쳐 초고속 레이저 워크스테이션의 채택이 급증하면서 나노초 단위 펄스 게이팅을 제공하는 변조기 및 Q-스위치 수요가 증가하고 있습니다. 중국 장비 제조사들은 2024년 고급 패키징 라인이 더 정밀한 재분배 층으로 전환되면서 TeO2 변조기 출하량이 27% 증가했습니다.고 보고했습니다. 음향광학 소자가 제공하는 서브마이크론 빔 제어는 실리콘 관통 전극(TSV) 드릴링 및 웨이퍼 다이싱 공정에서 수율 향상을 가능케 하여, 해당 지역 전반에 걸쳐 음향광학 소자 시장의 지속적인 수요 견인을 이끌고 있습니다.

급속한 5G/400G 광 네트워크 전개가 AO 변조기 수요 주도

북미 통신사들은 기존 100G 링크를 400G 코히어런트 광학 장치로 교체 중이며, 이 전환에는 멀티기가헤르츠 심볼 속도에서 높은 소멸비(extinction)를 구현할 수 있는 변조기가 필요합니다. 음향광학 위상 변조기는 낮은 처프(chirp)와 안정적인 열 성능을 제공하여 신규 메트로 및 장거리 네트워크 구축에 선호되는 부품입니다. 데이터센터 상호연결 업체들도 트래픽 밀도 증가 시 신호 무결성 유지를 위해 음향광학 기술을 선호하며, 이는 2027년까지 음향광학 장치 시장의 점진적 성장을 뒷받침합니다.

광학 등급 이산화 텔루륨(TeO₂) 결정의 지속적인 부족

TeO2는 구리 제련의 부산물로 생산되므로, 공급 가능성은 광학 수요보다는 채굴 주기에 좌우됩니다. 정제 능력의 느린 증설과 결정 인출 과정에서의 수율 손실로 인해 납품 기간이 길어지고 가격이 변동성이 큽니다. 장치 제조업체들은 니오븀산리튬 또는 칼코겐화물 유리 대체재를 모색하여 위험을 분산시키지만, 이러한 전환은 종종 재설계를 필요로 하여 음향광학 장치 시장의 단기 마진을 희석시킵니다.

분석되는 기타 촉진요인 및 억제요인

- 초음속 위협 탐지를 위한 방위 등급 LiDAR 채택

- 우주용 AOTF 판매를 촉진하는 하이퍼스펙트럼 이미징 큐브샛 성장

- 10kHz 초과 빔 스티어링 시스템의 복잡한 RF 드라이버 통합

부문 분석

음향 광학 장치 시장은 2024년 변조기 부문에서 34.6%의 매출을 기록했으며, 이는 레이저 가공 도구 및 광 스위치에서의 보편적 사용을 반영합니다. 최근 설계는 83% 회절 효율에 도달하여 레이저 마이크로 가공 및 광섬유 통신 허브의 처리량을 향상시킵니다. 두 번째 단락: 연평균 6.2% 성장률을 보이는 AOTF는 고정된 파장 선택으로 유지보수를 최소화하는 하이퍼스펙트럼 페이로드 및 체외진단 분야의 부상으로 혜택을 받고 있습니다. 편향기, 주파수 변환기, Q-스위치는 탄탄한 수요를 창출하며, 특히 플루언스 균일성이 필수적인 의료용 펄스 분야에서 Q-스위치가 선호됩니다.

TeO2는 우수한 성능 지수와 넓은 투과 창 덕분에 2024년 매출의 48.3%를 차지했으나, 공급 제약으로 인해 통합업체들은 대체재로 눈을 돌리고 있습니다. 리튬 니오베이트 솔루션의 음향광학 소자 시장 규모는 박막 증착 기술이 칩 내장형 음향광학 변조기에 적합한 저손실 도파관을 생산함에 따라 급속히 확대될 전망입니다. 융합 실리카는 자외선 포토리소그래피 분야에서 입지를 유지하고 있으며, 실험 데이터에서 음향광학 응답이 석영 대비 270배 향상된 것으로 나타나 게르마늄-안티몬-셀레늄 칼코겐화물 유리에 대한 관심이 고조되고 있습니다.

지역 분석

아시아태평양 지역은 2024년 글로벌 매출의 36.2%를 차지했으며, 이는 전자제품 생산의 우위와 웨이퍼 팹 생산 능력 확장을 반영합니다. 정책 입안자들은 국내 광전자 공급망에 보조금을 지원하여 절단, 드릴링 및 검사 도구에서의 음향광학 부품 소비를 촉진하고 있습니다. 5G 백홀 링크의 단기적 확장과 양자 보안 통신 연구는 음향광학 장치 시장에서의 지역적 리더십을 더욱 공고히 합니다.

북미는 통신사들의 광섬유 고밀도화 및 클라우드 제공업체들의 장거리 대역폭 업그레이드로 2위를 차지했습니다. 지향성 에너지 및 라입니다(LiDAR) 시스템에 대한 국방 계약이 안정적인 물량을 추가하는 한편, 연방 자금 지원은 가변형 AO 요소에 의존하는 양자 광학 프로젝트를 가속화하고 있습니다. 수직 통합 공급업체와 대학 연구 클러스터의 존재는 음향 광학 장치 시장 규모를 더욱 공고히 합니다.

유럽은 고정밀 제조 및 의료 기술 도입을 기반으로 견고한 점유율을 확보하고 있습니다. 독일, 영국, 프랑스는 초음속 모니터링를 위한 고속 음향광학 편향기 연구개발을 주도하고 있습니다. 우주 기반 지구 관측 임무에 대한 규제 지원은 방사선 내성 AOTF 수요를 지속적으로 창출하여 음향광학 장치 시장에 고부가가치 특수 주문을 풍부하게 합니다.

중동 및 아프리카는 현재 규모는 작지만 2030년까지 6.1%의 선도적인 연평균 성장률(CAGR)을 기록할 전망입니다. 광학 제조 및 5G 인프라로 경제 다각화를 추진하는 국가적 계획은 AO 변조기와 Q-스위치에 대한 꾸준한 공급망을 창출합니다. 이스라엘과 남아프리카공화국의 신흥 연구 허브는 물과 토양 모니터링을 위한 AO 기반 분광법을 탐구하며 과학적 수요 계층을 추가하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 아시아의 반도체 공장에서 초고속 레이저 미세 가공 능력 확대

- 북미 지역 5G/400G 광 네트워크 신속 구축으로 인한 AO 변조기 수요 증가

- 유럽 초음속 위협 탐지를 위한 방위 등급 LiDAR 도

- 하이퍼스펙트럼 이미징 큐브샛 성장으로 우주용 AOTF 판매 촉진

- 고에너지 의료용 레이저에서 TeO₂ 기반 AO Q-스위치 수요 급증

- 양자 광학 연구개발을 위한 AO 지원 가변 광원 채택 증가

- 시장 성장 억제요인

- 광학 등급 이산화 텔루륨 결정의 지속적인 부족

- 10kHz 이상 빔 스티어링 시스템에서의 복잡한 RF 드라이버 통합

- 고출력 중적외선 AO 장치의 제한된 열 관리 범위

- 이중용도 AO 부품에 대한 분산된 수출 통제 체제

- 생태계 분석

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모와 성장 예측

- 장치 유형별

- 음향 광학 변조기

- 편향기

- 주파수 변환기

- Q-스위치

- 가변 필터(AOTF)

- 모드 잠금기

- 펄스 피커/캐비티 댐퍼

- RF 드라이버

- 기타 장치 유형

- 재료별

- 이산화 텔루륨(TeO₂)

- 니오븀산 리튬(LiNbO₂)

- 용융 실리카

- 수정

- 몰리브덴산칼슘 등

- 파장 범위별

- 자외선(200-400nm)

- 가시광선(400-700nm)

- 근적외선(700-1500nm)

- 중간 적외(1500-3000nm)

- 원적외선(3000nm 이상)

- 재구성 속도별

- 저(1kHz 미만)

- 중(1-10kHz)

- 고(10kHz 이상)

- 용도별

- 재료 가공

- 레이저 매크로 가공

- 레이저 마이크로 가공

- 분광학 및 하이퍼스펙트럼 이미징

- 광학 신호 처리

- 생체 의학 이미징 및 진단

- 기타 신흥 분야(LiDAR, 양자 광학)

- 재료 가공

- 업계별

- 항공우주 및 방위

- 통신 분야

- 반도체 및 전자기기 제조

- 산업용 제조

- 생명과학 및 과학연구

- 의료

- 석유 및 가스

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽(덴마크, 스웨덴, 노르웨이, 핀란드)

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 동남아시아

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동

- 걸프 협력 회의 회원국

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장의 집중

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- Gooch and Housego PLC

- Brimrose Corporation of America

- Isomet Corporation

- Coherent Corp.

- L3Harris Technologies Inc.

- AA Opto Electronics Ltd.

- Lightcomm Technology Co., Ltd.

- IntraAction Corporation

- AMS Technologies AG

- APE Angewandte Physik and Elektronik GmbH

- CASTECH Inc.

- Sintec Optronics Pte Ltd.

- Hamamatsu Photonics KK

- Ushio Inc.

- Excelitas Technologies Corp.

- Holo/Or Ltd.

- PhotonTec Berlin GmbH

- Neos Technologies

- A*P*E China

- Glen Optics

- MPB Communications Inc.

- OptoSigma Corporation

제7장 시장 기회와 전망

HBR 25.10.29The Acousto optic devices market is valued at USD 587.14 million in 2025 and is forecast to touch USD 784.07 million by 2030 on a steady 5.96% CAGR.

Growth stems from widening use of high-precision optical control inside 5G network nodes, semiconductor lithography lines, and next-generation laser systems. Manufacturers are leveraging vertical integration to guard against material shortages and shorten lead times, while sustained RandD in tunable filters is unlocking new revenue in hyperspectral imaging and quantum photonics. Sub-micron laser machining needs, rising adoption of TeO2-based Q-switches in medical devices, and demand for compact beam-steering solutions in aerospace are shaping competitive strategy. The acousto optic devices market is also benefiting from public-sector spending on defense-grade LiDAR and satellite-borne spectroscopy, creating fertile ground for specialized suppliers with radiation-hardened designs.

Global Acousto Optic Devices Market Trends and Insights

Expanding Ultrafast-Laser Micro-Machining Capacity in Asian Semiconductor Fabs

Surging adoption of ultrafast-laser workstations across leading Asian foundries is feeding demand for modulators and Q-switches that supply nanosecond-scale pulse gating. Chinese tool builders reported a 27% rise in TeO2 modulator shipments during 2024 as advanced packaging lines shifted to finer redistribution layers. Sub-micron beam control delivered by acousto-optic devices enables higher yield in through-silicon-via drilling and wafer dicing, positioning the acousto optic devices market for sustained pull-through across the region.

Rapid 5G/400G Optical Network Roll-outs Driving AO Modulator Demand

North American carriers are replacing legacy 100 G links with 400 G coherent optics, a migration that requires modulators capable of high extinctions at multi-gigahertz symbol rates. Acousto-optic phase modulators offer low chirp and reliable thermal performance, making them the component of choice for new metro and long-haul builds. Data-center interconnect providers also favor AO technology to maintain signal integrity as traffic density rises, supporting incremental growth for the acousto optic devices market through 2027.

Persistent Shortage of Optical-Grade Tellurium Dioxide Crystals

TeO2 is grown as a by-product of copper smelting, linking availability to mining cycles rather than photonics demand. Slow ramp-ups in purification capacity and yield losses during crystal pull keep lead times extended and prices volatile. Device makers hedge by pursuing lithium niobate or chalcogenide glass alternatives, but such shifts often require redesigns that dilute near-term margins within the acousto optic devices market.

Other drivers and restraints analyzed in the detailed report include:

- Defense-Grade LiDAR Adoption for Hypersonic Threat Detection

- Growth of Hyperspectral Imaging Cubesats Fueling Space-Qualified AOTF Sales

- Complex RF-Driver Integration in Above 10 kHz Beam-Steering Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The acousto optic devices market recorded 34.6% revenue from modulators in 2024, reflecting their ubiquity in laser processing tools and optical switches. Recent designs reach 83% diffraction efficiency, boosting throughput in laser micromachining and fiber communication hubs. The second paragraph: AOTFs, advancing at 6.2% CAGR, benefit from the rise of hyperspectral payloads and in-vitro diagnostics where motionless wavelength selection minimizes maintenance. Deflectors, frequency shifters, and Q-switches contribute resilient demand, with Q-switches favored for medical pulses where fluence uniformity is mandatory.

TeO2 delivered 48.3% of 2024 sales thanks to its superior figure-of-merit and broad transmission window, yet constrained supply pushes integrators toward substitutes. The acousto optic devices market size for lithium niobate solutions is projected to expand swiftly as thin-film deposition methods produce low-loss waveguides suitable for on-chip AO modulators. Fused silica keeps a foothold in UV photolithography, and interest in Ge-Sb-Se chalcogenide glass is stirring after lab data showed a 270-fold gain over quartz in acousto-optic response.

The Acousto Optic Devices Market Report is Segmented by Device Type (Acousto-Optic Modulators, Deflectors, and More), Material (Tellurium Dioxide Lithium Niobate, and More), Wavelength Range (Ultraviolet, Visible, and More), Reconfiguration Speed (Low, Medium, High), Application (Material Processing, and More), Vertical (Aerospace and Defense, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific generated 36.2% of global revenue in 2024, reflecting dominant electronics production and expanded wafer-fab capacity. Policymakers channel subsidies toward domestic photonics supply chains, lifting consumption of AO components in cutting, drilling, and inspection tools. Near-term expansion of 5G backhaul links and research into quantum secure communication further cements regional leadership in the acousto optic devices market.

North America ranks second as telecom carriers densify fiber and cloud providers upgrade long-haul bandwidth. Defense contracts for directed-energy and LiDAR systems add dependable volume, while federal funding accelerates quantum photonics projects that depend on tunable AO elements. The acousto optic devices market size is reinforced by the presence of vertically integrated suppliers and university research clusters.

Europe commands a solid share built on high-precision manufacturing and medical technology adoption. Germany, the UK, and France spearhead R&D into high-speed AO deflectors for hypersonic surveillance. Regulatory support for space-based Earth-observation missions keeps demand flowing for radiation-hardened AOTFs, enriching the acousto optic devices market with specialized high-margin orders.

The Middle East and Africa hold a smaller base today yet post a leading 6.1% CAGR through 2030. National initiatives to diversify economies into photonics fabrication and 5G infrastructure create steady pipelines for AO modulators and Q-switches. Emerging research hubs in Israel and South Africa explore AO-driven spectroscopy for water and soil monitoring, adding scientific demand layers.

- Gooch and Housego PLC

- Brimrose Corporation of America

- Isomet Corporation

- Coherent Corp.

- L3Harris Technologies Inc.

- AA Opto Electronics Ltd.

- Lightcomm Technology Co., Ltd.

- IntraAction Corporation

- AMS Technologies AG

- APE Angewandte Physik and Elektronik GmbH

- CASTECH Inc.

- Sintec Optronics Pte Ltd.

- Hamamatsu Photonics K.K.

- Ushio Inc.

- Excelitas Technologies Corp.

- Holo/Or Ltd.

- PhotonTec Berlin GmbH

- Neos Technologies

- A*P*E China

- Glen Optics

- MPB Communications Inc.

- OptoSigma Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Ultrafast-Laser Micro-Machining capacity in Asian Semiconductor Fabs

- 4.2.2 Rapid 5G/ 400 G Optical Network Roll-outs Driving AO Modulator Demand in North America

- 4.2.3 Defense-Grade LiDAR Adoption for Hypersonic Threat Detection in Europe

- 4.2.4 Growth of Hyperspectral Imaging Cubesats Fueling Space-Qualified AOTF Sales

- 4.2.5 Demand Surge for TeO?-Based AO Q-Switches in High-Energy Medical Lasers

- 4.2.6 Increasing Adoption of AO-Enabled Tunable Light Sources for Quantum Photonics R&D

- 4.3 Market Restraints

- 4.3.1 Persistent Shortage of Optical-Grade Tellurium Dioxide Crystals

- 4.3.2 Complex RF-Driver Integration in Above 10 kHz Beam-Steering Systems

- 4.3.3 Limited Thermal-Management Window in High-Power Mid-IR AO Devices

- 4.3.4 Fragmented Export-Control Regimes for Dual-Use AO Components

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Type

- 5.1.1 Acousto-Optic Modulators

- 5.1.2 Deflectors

- 5.1.3 Frequency Shifters

- 5.1.4 Q-Switches

- 5.1.5 Tunable Filters (AOTF)

- 5.1.6 Mode Lockers

- 5.1.7 Pulse Pickers/Cavity Dumpers

- 5.1.8 RF Drivers

- 5.1.9 Other Device Types

- 5.2 By Material

- 5.2.1 Tellurium Dioxide (TeO?)

- 5.2.2 Lithium Niobate (LiNbO?)

- 5.2.3 Fused Silica

- 5.2.4 Crystal Quartz

- 5.2.5 Calcium Molybdate and Others

- 5.3 By Wavelength Range

- 5.3.1 Ultraviolet (200-400 nm)

- 5.3.2 Visible (400-700 nm)

- 5.3.3 Near-Infrared (700-1500 nm)

- 5.3.4 Mid-Infrared (1500-3000 nm)

- 5.3.5 Far-Infrared (Above 3000 nm)

- 5.4 By Reconfiguration Speed

- 5.4.1 Low (Less than 1 kHz)

- 5.4.2 Medium (1-10 kHz)

- 5.4.3 High (Above 10 kHz)

- 5.5 By Application

- 5.5.1 Material Processing

- 5.5.1.1 Laser Macro-Processing

- 5.5.1.2 Laser Micro-Processing

- 5.5.2 Spectroscopy and Hyperspectral Imaging

- 5.5.3 Optical Signal Processing

- 5.5.4 Biomedical Imaging and Diagnostics

- 5.5.5 Other Emerging (LiDAR, Quantum Photonics)

- 5.5.1 Material Processing

- 5.6 By Vertical

- 5.6.1 Aerospace and Defense

- 5.6.2 Telecommunications

- 5.6.3 Semiconductor and Electronics Manufacturing

- 5.6.4 Industrial Manufacturing

- 5.6.5 Life Sciences and Scientific Research

- 5.6.6 Medical

- 5.6.7 Oil and Gas

- 5.6.8 Others

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Nordics (Denmark, Sweden, Norway, Finland)

- 5.7.2.7 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 South Korea

- 5.7.3.4 India

- 5.7.3.5 Southeast Asia

- 5.7.3.6 Australia

- 5.7.3.7 Rest of Asia-Pacific-Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Argentina

- 5.7.4.3 Rest of South America

- 5.7.5 Middle East

- 5.7.5.1 Gulf Cooperation Council Countries

- 5.7.5.2 Turkey

- 5.7.5.3 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Nigeria

- 5.7.6.3 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Gooch and Housego PLC

- 6.4.2 Brimrose Corporation of America

- 6.4.3 Isomet Corporation

- 6.4.4 Coherent Corp.

- 6.4.5 L3Harris Technologies Inc.

- 6.4.6 AA Opto Electronics Ltd.

- 6.4.7 Lightcomm Technology Co., Ltd.

- 6.4.8 IntraAction Corporation

- 6.4.9 AMS Technologies AG

- 6.4.10 APE Angewandte Physik and Elektronik GmbH

- 6.4.11 CASTECH Inc.

- 6.4.12 Sintec Optronics Pte Ltd.

- 6.4.13 Hamamatsu Photonics K.K.

- 6.4.14 Ushio Inc.

- 6.4.15 Excelitas Technologies Corp.

- 6.4.16 Holo/Or Ltd.

- 6.4.17 PhotonTec Berlin GmbH

- 6.4.18 Neos Technologies

- 6.4.19 A*P*E China

- 6.4.20 Glen Optics

- 6.4.21 MPB Communications Inc.

- 6.4.22 OptoSigma Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment