|

시장보고서

상품코드

1842508

항공기 어레스팅 시스템 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Aircraft Arresting System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

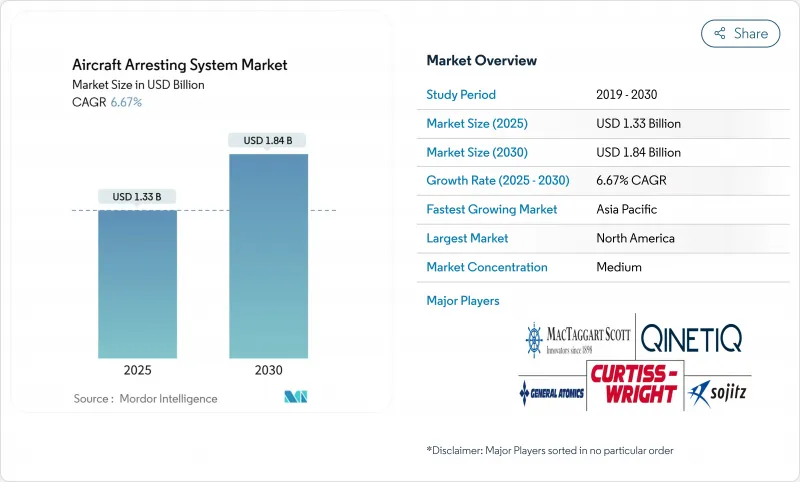

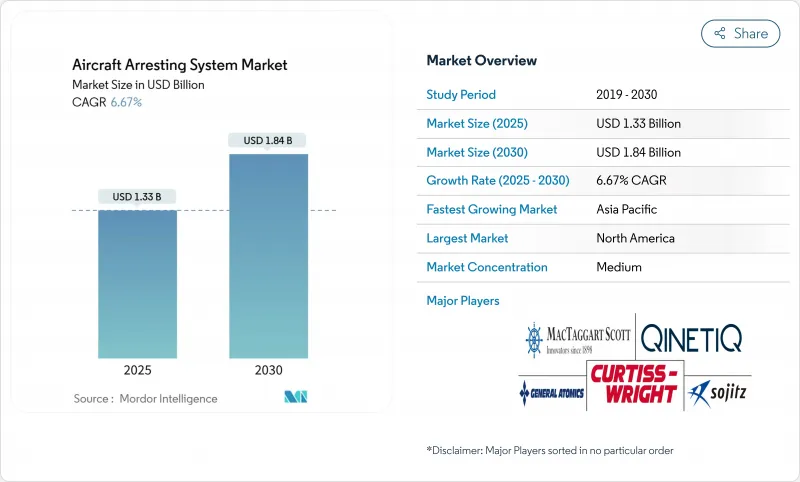

항공기 어레스팅 시스템 시장 규모는 2025년에 13억 3,000만 달러로 평가되었고, 2030년에 18억 4,000만 달러에 이를 것으로 예측되며, CAGR 6.67%로 성장할 전망입니다.

수요는 5세대 전투기 함대 확대, 항공모함 현대화 추진, 그리고 많은 상업 공항에서 활주로 이탈 방지 장치를 의무화하는 글로벌 안전 규제의 통합으로 촉진되고 있습니다. 기술은 유압식 어레스터에서 전자기 시스템으로 전환되고 있으며, 이는 CVN 78 함상에서 23,000회 이상의 회수 기록을 보유한 미 해군의 첨단 어레스터 기어(AAG)에서 입증되었습니다. 지상 기반 플랫폼이 최대 매출을 차지하지만, 아시아태평양 지역 해군들의 신형 항공모함 도입으로 해상 기반 응용 분야가 가장 빠르게 성장하고 있습니다. 미국 연방항공청(FAA)이 표준 안전 구역 구축이 불가능한 공항들에 설치 의무화를 시행함에 따라 상업 항공 분야에서도 공학적 재료 계류 시스템(EMAS) 도입이 가속화되고 있습니다. 특수 합금 및 스프링의 공급망 제약이 단기적 위험 요인으로 작용하지만, 예측 유지보수를 제공하는 디지털 제어 장치가 수명 주기 비용 절감을 통해 이러한 저항 요인의 일부를 상쇄하고 있습니다.

세계의 항공기 어레스팅 시스템 시장 동향 및 인사이트

5세대 전투기 확대

F-35 변종들은 어레스트 훅에 전례 없는 하중을 가해, 15회 접촉 수명 요건을 충족하기 위한 신속한 재료 업그레이드와 훅 포인트 재설계를 촉발했습니다. 항공모함 탑재형 F-35C 시험에서 초기 마모가 발견되어 한 자릿수 사이클 후 교체가 불가피해졌으며, 이는 고강도 합금 분야의 혁신을 주도했습니다. 완전 탑재 시 18,000파운드에 달하는 증가된 접근 중량은 더 큰 에너지 흡수 장치 용량을 요구하며, 감속을 정밀하게 조절할 수 있는 전자기 시스템 조달을 촉진하고 있습니다. 해병대의 트웬티나인팜스 기지 M-31 기어 시험은 원정 전진 기지 작전(EABO)에 대한 항공기의 유연성을 입증했습니다. 미국 2025 회계연도 항공 예산 612억 달러는 항공기 및 관련 어레스트 장치 업그레이드를 지원합니다.

단거리 활주로 및 원정 비행장 작전의 성장

분산 작전 교리는 어레스트 장치를 열악한 지역으로 확대합니다. 공군의 이동식 항공기 어레스트장치(MAAS)는 6명의 공군 병사가 자갈이나 아스팔트 위에 2시간 만에 설치할 수 있습니다. 작전 BEEFY와 같은 훈련은 악천후 속 F-16용 MAAS 배치를 검증했습니다. 원정 작전 관심사는 해안 기지용 전자기 항공기 발사 시스템(EMALS) 적용까지 확대되며, 전체 활주로 없이도 캐터펄트급 유연성을 제공합니다. 이러한 배치는 국가들이 분산 작전 기지를 강화함에 따라 항공기 어레스트 시스템 시장을 확대합니다.

높은 초기 자본 지출과 긴 인증 주기

완전한 EMAS 설치 비용은 활주로 끝당 1,000만 달러를 초과할 수 있어 소규모 공항은 최대 95%를 지원하는 FAA 보조금에 의존해야 하지만, 경쟁력 확보가 여전히 어렵습니다. 국방 프로그램도 유사한 부담에 직면합니다. 설계 변경 후 AAG 단위 비용이 조달 기준을 초과하여 신기술 인증의 복잡성을 부각시켰습니다. 독점 시스템은 공급업체 경쟁을 제한하여 획득 및 수명 주기 비용을 상승시켜 항공기 계류 장치 산업의 광범위한 채택을 저해합니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 활주로 끝 이탈 방지 보호를 향한 글로벌 안전 규제 통합

- 유압식에서 전자기식 및 회전 마찰 시스템으로의 기술 전환

- 특수 합금 및 고주기 스프링에 대한 공급망 의존도

부문 분석

해상 기반 플랫폼은 2024년 항공기 어레스트 장치 시장 점유율 64.55%로 우세한 육상 설비와의 격차를 좁히며 8.35% CAGR로 성장할 것으로 전망됩니다. 중국 푸젠(福建)과 한국 CVX를 포함한 아시아태평양 지역의 함대 확장은 더 무거운 제트기와 미래 무인 시스템을 처리하기 위해 전자기식 어레스트 장치가 필요합니다. 미국과 프랑스의 차세대 항공모함 협력은 유럽으로의 유사한 기술 이전을 시사합니다.

분산 작전에는 지상 시스템이 여전히 필수적입니다. MAAS(지상 기반 항공기 어레스트 시스템)는 도로와 다져진 땅에서 2시간 내 배치 가능하여 기존 인프라 없이도 전투기 분대를 지원합니다. 상업 공항은 지형으로 인해 활주로 확장이 불가능한 경우 EMAS(전자기식 항공기 어레스트 시스템)를 채택하며, 2024년까지 500개 이상의 설치가 기록될 전망입니다. 두 추세 모두 항공기 어레스트 시스템 시장의 다양성을 유지합니다.

공학적 재료 계류 시스템(EMAS) 매출은 연평균 9.24% 성장률로 증가하며, 케이블 및 릴 설계가 차지하던 37.24% 점유율을 잠식하고 있습니다. 차세대 재료에 대한 FAA 연구는 수명 종료 교체 물결을 예상하며, 압축 특성을 유지하면서도 더 가볍고 재활용 가능한 블록의 시장 진입 기회를 열어주고 있습니다. 투수 콘크리트의 유한 요소 시험은 배수 기능을 간소화하면서도 항공기를 신속히 감속시키는 능력을 입증하여 미래 저탄소 옵션을 제시합니다.

케이블 및 릴 방식은 후크 호환성과 낮은 구매 비용으로 기존 기지에 여전히 확고히 자리 잡고 있습니다. 회전 마찰 장치는 전자기적 복잡성 없이 신뢰할 수 있는 성능이 필요한 지역 공항을 위한 중간 지점 솔루션을 제공합니다. 전자기식 설계는 높은 출격률과 간소화된 유지보수 주기로 인해 주요 항공사의 관심을 확보하며, 항공기 어레스트 장치 시장 내 프리미엄 등급으로 자리매김하고 있습니다.

지역 분석

북미는 미 해군의 AAG 프로그램과 500개 이상의 EMAS 활주로 종단 설치를 의무화한 FAA 규정 덕분에 항공기 어레스트 장치 시스템 시장의 40.45% 점유율을 유지하고 있습니다. 캐나다의 150m 안전 구역 규정은 특히 내륙 공항에서 민간 수요를 더욱 확대하고 있으며, 커티스-라이트의 헬리콥터 취급 협력은 특수한 틈새 시장을 구축하고 있습니다. FAA의 2026년 40억 달러 규모 공항 지원 예산 항목은 안전 인프라에 대한 자본 유입을 지속시키고 있습니다.

아시아태평양 지역은 중국의 다수 항공사 보유 기단과 인도의 차세대 전자기 회수 시스템 협력에 힘입어 8.25%의 연평균 성장률(CAGR)로 가장 빠르게 확장되는 지역입니다. 한국의 CVX 프로그램은 해당 지역의 첨단 솔루션에 대한 수요를 부각시킨다. ICAO 아시아태평양 비행장 설계 태스크포스는 활주로 종단 안전 기준을 법제화하여 민간 항공 수요를 안정적으로 유지합니다.

유럽은 NATO 표준화로 점진적 성장을 지속합니다. 프랑스와 벨기에의 업그레이드는 공통 공급망 기반을 강화하여 배치 작전의 물류 부담을 완화합니다(Air Force Technology). 아프리카 신흥 시장들은 ICAO 지침을 수용하고 있습니다. 지형적 제약으로 넓은 안전 구역 확보가 어려운 시에라리온의 안전 계획은 특히 어레스트 장치 시스템을 명시하고 있습니다. 중동은 항공모함 및 지상 기반 장비를 위해 미국과 유럽의 해외 군사 판매 채널을 활용하며 글로벌 항공기 어레스트 장치 시스템 시장을 다각화하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 5세대 전투기 함대 확장

- 단거리 활주로 및 원정 비행장 운영 증가

- 활주로 끝 이탈 방지 장치에 대한 글로벌 안전 규정 통합

- 유압식에서 전자기식 및 회전 마찰 시스템으로의 기술 전환

- 민간 공항 개조를 촉진하는 보험 및 책임 부담 증가

- 전 세계 항공모함 및 LHD/LHA 배치 증가

- 시장 성장 억제요인

- 높은 초기 자본 지출 및 긴 인증 주기

- 특수 합금 및 고주기 스프링에 대한 공급망 의존도

- 경쟁적 투자 우선순위 : 자동 브레이크 및 활주로 표면 개선

- 항공기 유형 간 제한된 표준화

- 밸류체인 분석

- 규제와 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 플랫폼별

- 해상 기반

- 육상 기반

- 기술 유형별

- 케이블 및 릴

- 넷 배리어

- 공학 재료 어레스트 시스템(EMAS)

- 회전 마찰/유압식

- 전자기/자기식

- 최종 사용자별

- 군용 비행장

- 상업용 공항

- 항공모함

- 컴포넌트별

- 에너지 흡수 장치

- 후크 및 케이블

- 지지 구조물 및 기초

- 제어 및 모니터링 장치

- 설치 방법별

- 신규 설치

- 개조

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 남미

- 브라질

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장의 집중

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- Curtiss-Wright Corporation

- General Atomics

- MacTaggart, Scott and Company Limited

- Runway Safe Group AB

- SCAMA AB

- A-tech Inc.

- QinetiQ Group

- The Boeing Company

- Sojitz Aerospace Corporation

- John Galt International Engineering Limited

- SDT Space & Defence Technologies Inc.

- TEKJET AS

- Neometrix

- SIR-BA Technology and Defense Industry Inc.

제7장 시장 기회와 전망

HBR 25.10.29The aircraft arresting system market size is valued at USD 1.33 billion in 2025 and is projected to rise to USD 1.84 billion by 2030, advancing at a 6.67% CAGR.

Demand is propelled by expanding fifth-generation fighter fleets, robust aircraft-carrier modernization, and converging global safety regulations that make over-run mitigation mandatory at many commercial airports. Technology is shifting from hydraulic arrestors to electromagnetic systems, as demonstrated by the US Navy's Advanced Arresting Gear, which has logged more than 23,000 recoveries aboard CVN 78. Land-based platforms capture the largest revenue, yet sea-based applications show the fastest growth as Asia-Pacific navies field new carriers. Engineered Material Arresting Systems (EMAS) are accelerating in commercial aviation because the FAA mandates installations at airports that cannot build standard safety areas. Supply-chain constraints in specialty alloys and springs introduce near-term risk, but digital control units offering predictive maintenance offset part of this drag through life-cycle cost savings.

Global Aircraft Arresting System Market Trends and Insights

Expansion of Fifth-Generation Combat Aircraft Fleets

F-35 variants place unprecedented loads on arresting hooks, prompting rapid material upgrades and hook-point redesigns to meet 15-engagement life requirements. Carrier-borne F-35C testing revealed early wear that forced replacement after single-digit cycles, driving innovation in high-strength alloys. Elevated approach weights, 18,000 lbs with full payload, require larger energy-absorber capacity, fueling procurement of electromagnetic systems able to modulate deceleration precisely. Marine Corps trials with M-31 gear at Twentynine Palms proved the aircraft's flexibility for Expeditionary Advanced Base Operations. The US FY 2025 aviation budget of USD 61.2 billion underwrites aircraft and corresponding arresting upgrades.

Growth in Short-Runway and Expeditionary Airfield Operations

Distributed-operations doctrine pushes arresting systems into austere zones. The Air Force's Mobile Aircraft Arresting System (MAAS) can be installed on gravel or asphalt in two hours by six airmen. Exercises such as Operation BEEFY validated the MAAS deployment for F-16s under challenging weather. Expeditionary interest extends to adapting Electromagnetic Aircraft Launch System (EMALS) for shore bases, offering catapult-like flexibility without full-length runways. These deployments enlarge the aircraft arresting system market as nations harden dispersed operating bases.

High Up-Front Capital Expenditure and Lengthy Certification Cycles

Full EMAS installation can exceed USD 10 million per runway end, forcing smaller airports to rely on FAA grants that cover up to 95%, yet remain competitive to secure. Defense programs face similar burdens; AAG unit costs breached procurement thresholds after design changes, underscoring certification complexity in new technology. Proprietary systems limit vendor competition, elevating acquisition and lifecycle costs, which restrains broader adoption in the aircraft arresting system industry.

Other drivers and restraints analyzed in the detailed report include:

- Global Safety-Regulation Convergence toward Runway-End Over-Run Protection

- Technological Shift from Hydraulic to Electromagnetic and Rotary-Friction Systems

- Supply-Chain Dependence on Specialty Alloys and High-Cycle Springs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sea-based platforms are forecast to grow at an 8.35% CAGR, closing the gap with dominant land installations with a 64.55% aircraft arresting system market share in 2024. Fleet expansion in Asia-Pacific-including China's Fujian and South Korea's CVX-requires electromagnetic arrestors to handle heavier jets and future unmanned systems. US-French collaboration on next-generation carriers signals similar technology migration to Europe.

Land systems remain essential for dispersed operations. MAAS enables two-hour deployment on roads and packed earth, supporting fighter detachments without traditional infrastructure. Commercial airports adopt EMAS, where terrain blocks runway extensions, with more than 500 installations recorded by 2024. Both trends sustain a diversified aircraft arresting system market.

Engineered Material Arresting System (EMAS) revenue grows at a 9.24% CAGR, eroding the 37.24% share held by Cable and Reel designs. FAA studies on next-generation materials anticipate end-of-life replacement waves, opening space for lighter, recyclable blocks that maintain crush characteristics. Finite-element tests of pervious concrete confirm its capacity to decelerate aircraft rapidly while simplifying drainage, demonstrating future low-carbon options.

Cable and Reel remains entrenched in legacy bases because of hook compatibility and lower purchase cost. Rotary-friction units offer middle-ground solutions for regional airports needing reliable performance without electromagnetic complexity. Electromagnetic designs secure flag-carrier interest due to higher sortie rates and simplified maintenance cycles, positioning them as the premium tier in the aircraft arresting system market.

The Aircraft Arresting System Market Report is Segmented by Platform (Sea-Based and Land-Based), Technology Type (Cable and Reel, Net Barrier, and More), End User (Military Airbase, Commercial Airport, and More), Component (Energy Absorber, Hook and Cable, and More), Fit (New Installation and Retrofit), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retains a 40.45% share of the aircraft arresting system market, anchored by the US Navy's AAG program and an FAA mandate that has delivered more than 500 EMAS runway ends. Canada's 150 m safety-area rule further expands civil demand, especially at land-locked airports, while Curtiss-Wright's collaboration on helicopter handling builds specialized niches. The FAA's USD 4.0 billion airport-grant line item for 2026 sustains capital flows into safety infrastructure.

Asia-Pacific is the fastest-expanding region, with an 8.25% CAGR, propelled by China's multi-carrier fleet and India's collaboration on next-generation electromagnetic recovery. South Korea's CVX program underscores the region's appetite for advanced solutions. ICAO's Asia-Pacific Aerodrome Design Task Force has codified runway-end safety, ensuring steady civil aviation demand.

Europe maintains incremental growth driven by NATO standardization. French and Belgian upgrades reinforce a shared supplier base, easing logistics for deployed operations, Air Force Technology. Emerging markets in Africa embrace ICAO guidance; Sierra Leone's safety plan specifies arresting systems where terrain prevents wider safety areas. The Middle East leverages US and European foreign military sales channels for carrier and land-based gear, diversifying the global aircraft arresting system market.

- Curtiss-Wright Corporation

- General Atomics

- MacTaggart, Scott and Company Limited

- Runway Safe Group AB

- SCAMA AB

- A-tech Inc.

- QinetiQ Group

- The Boeing Company

- Sojitz Aerospace Corporation

- John Galt International Engineering Limited

- SDT Space & Defence Technologies Inc.

- TEKJET A.S.

- Neometrix

- SIR-BA Technology and Defense Industry Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of fifth-generation combat aircraft fleets

- 4.2.2 Growth in short-runway and expeditionary airfield operations

- 4.2.3 Global safety-regulation convergence toward runway-end over-run protection

- 4.2.4 Technological shift from hydraulic to electromagnetic and rotary-friction systems

- 4.2.5 Insurance and liability pressures driving civil-airport retrofits

- 4.2.6 Increase in worldwide aircraft-carrier and LHD/LHA deployments

- 4.3 Market Restraints

- 4.3.1 High up-front capital expenditure and lengthy certification cycles

- 4.3.2 Supply-chain dependence on specialty alloys and high-cycle springs

- 4.3.3 Competing investment priorities: autobrake and runway-surface enhancements

- 4.3.4 Limited standardization across aircraft types

- 4.4 Value Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Platform

- 5.1.1 Sea-based

- 5.1.2 Land-based

- 5.2 By Technology Type

- 5.2.1 Cable and Reel

- 5.2.2 Net Barrier

- 5.2.3 Engineered Material Arresting System (EMAS)

- 5.2.4 Rotary-Friction/Hydraulic

- 5.2.5 Electromagnetic/Magnetic

- 5.3 By End User

- 5.3.1 Military Airbase

- 5.3.2 Commercial Airport

- 5.3.3 Aircraft Carrier

- 5.4 By Component

- 5.4.1 Energy Absorber

- 5.4.2 Hook and Cable

- 5.4.3 Support Structure and Foundations

- 5.4.4 Control and Monitoring Unit

- 5.5 By Fit

- 5.5.1 New Installation

- 5.5.2 Retrofit

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Curtiss-Wright Corporation

- 6.4.2 General Atomics

- 6.4.3 MacTaggart, Scott and Company Limited

- 6.4.4 Runway Safe Group AB

- 6.4.5 SCAMA AB

- 6.4.6 A-tech Inc.

- 6.4.7 QinetiQ Group

- 6.4.8 The Boeing Company

- 6.4.9 Sojitz Aerospace Corporation

- 6.4.10 John Galt International Engineering Limited

- 6.4.11 SDT Space & Defence Technologies Inc.

- 6.4.12 TEKJET A.S.

- 6.4.13 Neometrix

- 6.4.14 SIR-BA Technology and Defense Industry Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment