|

시장보고서

상품코드

1842513

고속도강(HSS) 절삭 공구 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)High Speed Steel Cutting Tools - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

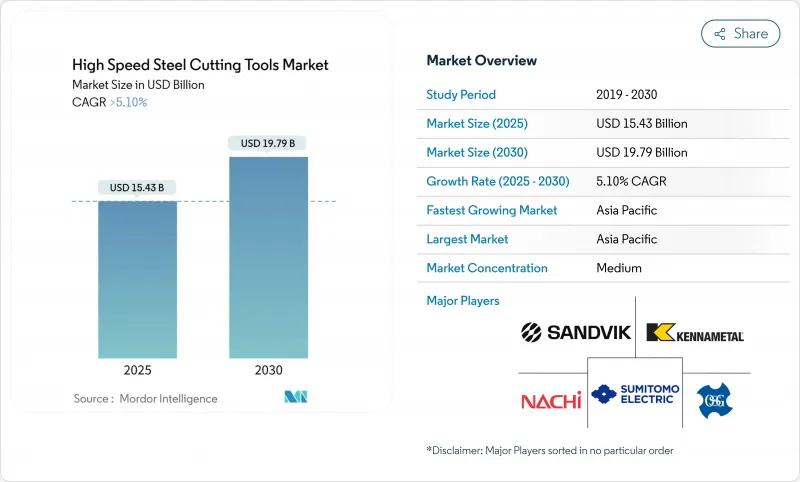

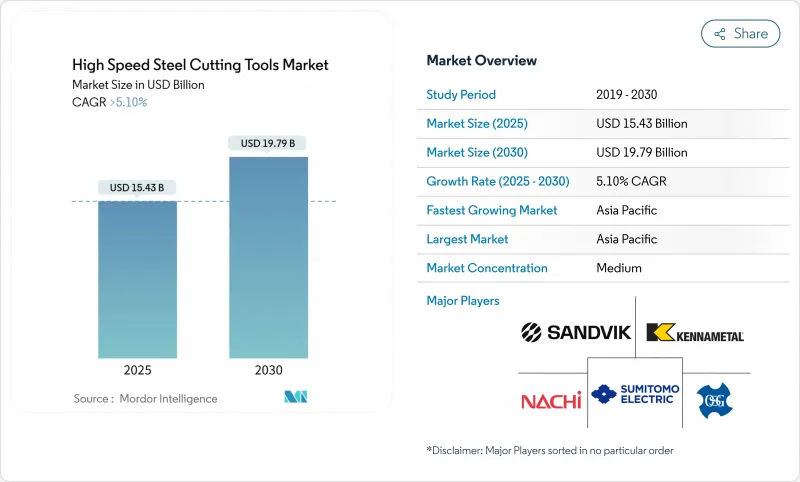

고속도강(HSS) 절삭 공구 시장 규모는 2025년에 154억 3,000만 달러로 추정되고, 2030년에는 CAGR 5.1%로 성장할 전망이며, 197억 9,000만 달러에 이를 전망입니다.

중량 가공의 부활, 아시아의 급속한 산업화, 분말 야금의 폭넓은 사용이 주요 성장 엔진입니다. 제조업체는 항공우주 합금에 코발트 강화 등급을 채택하고, DIY 구매자를 위한 전자상거래 채널을 확장하며, 공구 수명을 연장하는 적응형 CNC 전략을 정교하게 하고 있습니다. 불안정한 몰리브덴 및 코발트 가격, 자동차 부문의 초경 공구 및 PCD 공구로의 단계적 전환 등 공급측 압력은 여전히 남아 있습니다. 경쟁 구도는 타겟 인수, 디지털 공구 관리, 탄소 중립 생산에 대한 노력이 중심이 되고 있습니다.

세계의 고속도강(HSS) 절삭 공구 시장 동향 및 인사이트

아시아 신흥 가공 공장에서 저비용 공구 수요

중국, 인도, ASEAN 시장에서는 Tier2 및 Tier3 작업점의 수가 증가하고 있으며 초기 공구 비용이 낮은 것이 선호되고 있습니다. 특히, 기본 CNC를 채용하여 이송과 속도를 최적화하여 공구 수명을 연장할 수 있기 때문에 기존의 고속도강 공구는 우선순위에 적합합니다. 중국의 지방은 자국의 공작기계 제조업체를 지원함으로써 국내 조달을 정착시켜 반복적인 수요 사이클을 고정화하고 있습니다. 같은 동향이 인도의 자동차 부품 클러스터와 베트남의 전자기기 공급기지에도 퍼져 표준 고속도강 밀링 커터 및 드릴의 견조한 소비를 지원하고 있습니다.

북미의 DIY 및 주택 설비 소매 붐

북미의 가정 소유자, 취미 애호가, '프로슈머'가 소비자 등급의 HSS 비트, 탭, 홀소 온라인 판매를 2자리 성장으로 견인하고 있습니다. 공구 제조업체는 현재 디지털 선반에서 눈에 띄게 모양, 코팅 및 패키지를 조정하고 전동 공구 브랜드는 무선 드릴과 소형 선반과 스타터 세트를 번들로 제공합니다. 저렴한 가격대에서 공업적인 성능을 요구하는 숙련된 애호가가 대응 가능한 부문을 확대해 이 채널의 CAGR 전망 11.4%를 보강하고 있습니다.

자동차용 초경 및 PCD 공구로의 급속한 시프트

전기자동차 플랫폼은 얇은 알루미늄 하우징, 복합 브래킷, 고강도 강철 보강재에 의존합니다. 초경 및 PCD 커터는 이러한 재료로 높은 가공면 품위 및 처리량을 실현하고 파워트레인, 배터리, 섀시의 각 라인에서 서서히 고속도강으로 대체됩니다. 자동차 공구의 결정은 업스트림 티어 공급업체와 강철 서비스 센터에 영향을 미치며, 특히 유럽의 대량 생산 공장에서 고속도강 수요의 발을 끌어 당길 것입니다.

부문 분석

밀링 커터는 2024년 세계 매출의 32.4%를 차지했으며, 페이스, 슬롯, 프로파일 가공의 유연성으로 고속도강(HSS) 절삭 공구 시장을 지원하고 있습니다. 이 부문은 마무리를 손상시키지 않으면서 금속 제거율을 향상시키는 반경 방향 칩의 얇은 두께와 고효율 황삭 방법의 지속적인 개선으로 이익을 얻습니다. 이와는 대조적으로, 탭은 2030년까지 연평균 복합 성장률(CAGR)이 가장 빨리 6.8%를 확보하기 위해 스크류 형성 형식이 사이클 시간을 단축하고 칩 배출 문제를 방지합니다. 칩이 없는 나사 가공은 자동차 전자 기기의 하우징 및 얇은 다이 캐스팅 부품에 적합하며 아시아 및 동유럽에서의 채용을 뒷받침하고 있습니다.

비용 중시의 가공 공장에서는 구멍 가공 및 마무리 가공에 고속도강 드릴, 리머, 브로치가 편리하게 되어, 톱이나 접시판은 보수 및 수리의 틈새 요구에 응하고 있습니다. 디지털 설계 플랫폼은 현재 칩 흐르기, 헹굼 각, 냉각수 공급을 시뮬레이션하고 각 기판에 대한 절단 블레이드를 사용자 정의할 수 있습니다. 이러한 소프트웨어를 활용함으로써 공구 제조업체는 표준 고속도강 강종이라도 새로운 수명을 끌어내고 고속도강(HSS) 절삭 공구 시장에서 밀링 커터의 핵심 역할을 강화하고 있습니다.

기존의 M 시리즈 재종은 중간 정도의 인성 가공에 폭넓게 이용할 수 있으며 가격 경쟁력도 있기 때문에 2024년의 매출 점유율은 48%에 달했습니다. 분말 야금 강종은 현재 생산고의 14.5%에 불과하지만 CAGR 8.3%라는 불균형한 성장을 이루고 있습니다. 균일한 탄화물 분산, 미세화된 입계, 편석의 저감에 의해 치핑의 최소화가 중요한 항공우주용 패스너나 의료용 임플란트의 가공에 있어서, PM-HSS는 우위성을 발휘합니다. 코발트 리치 M42와 M35는 내열 합금의 전략적 틈새를 유지하고 PM과 표준 유형 사이의 비용 홈을 채 웁니다.

PM-HSS와 관련된 고속도강(HSS) 절삭 공구 시장 규모는 유럽의 생산 능력 격차 해소 및 아시아 국가의 원자화 라인의 고급화에 따라 확대될 전망입니다. Additive Manufacturing의 시험에서도 경도 구배를 조정한 고속도강 분말의 블렌드가 검토되고 있어, 장래의 설계 가능성을 넓혀 고속도강(HSS) 절삭 공구 시장에 있어서 장기적인 재료 등급의 다양화를 지원하고 있습니다.

고속도강(HSS) 절삭 공구 시장 보고서는 공구 유형별(드릴 등), 재료 등급별(종래의 고속도강(M시리즈) 등), 제조 공정별(분말 야금 등), 유통 채널별(직접 OEM 판매 등), 최종 사용자 산업별(석유 및 가스 등), 지역별(북미 등)로 분류되어 있습니다. 이 보고서는 위의 모든 부문에 대해 시장 규모 및 예측(달러)을 제공합니다.

지역 분석

아시아는 수익 점유율 46.2%, CAGR 예측 6.3%로 고속도강(HSS) 절삭 공구 시장을 선도하고 있습니다. 이것은 중국 전자 및 공작기계 건설, 인도 자동차 클러스터, 베트남 조립 수출 덕분입니다. 국내 공구 제조업체는 현재 밸류체인을 상승시키고 TiN 및 AlCrN 코팅을 채택하고 PM 채용을 추진함으로써 수입 의존도를 줄이고 지역 자급 자족을 강화하고 있습니다.

북미는 2위로, 리쇼어링 프로그램, 국방 오프셋, 활발한 DIY 문화에 의해 활성화되고 있습니다. 항공우주 및 에너지 공장의 하이브리드 가공 셀은 적응성이 높은 CNC 환경에서 활약하는 다목적 커터가 필요합니다. 또한 전자상거래의 보급으로 소규모 가공 현장에서도 특수한 탭이나 리머에 직접 액세스할 수 있게 되어 고속도강(HSS) 절삭 공구 시장의 진출 기업이 확산되고 있습니다.

유럽은 기술적으로 진행되고 있지만 생산 능력에 제약이 있습니다. PM-HSS 공급이 제한되어 프리미엄 커터의 리드 타임이 길어지고 있습니다. 그럼에도 불구하고 독일, 프랑스, 영국 공장은 이산화탄소 감소 목표를 달성하기 위해 지속 가능한 재조정과 폐쇄 루프 재활용을 강조합니다. 공구 수명 모니터링 및 ISO 14001 프로그램은 자동차 드라이브 트레인 라인에서 초경의 침식에도 불구하고 데이터 풍부한 고속도강 솔루션에 대한 수요를 높이고 있습니다.

중남미는 브라질의 산업 기반에 의존하고 중동은 에너지 설비의 개조와 지속적인 인프라 정비에 의존하고 있습니다. 아프리카 수요 클러스터는 남아프리카의 광산 공급 및 이집트 부품 공장에 있습니다. 이러한 신흥 지역은 일반적으로 고속도강(HSS) 절삭 공구 시장의 다양화와 지역화된 부가가치의 가능성을 반영합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 도입

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트 및 역학

- 시장 개요

- 시장 성장 촉진요인

- 아시아 신흥 가공 공장에서의 저비용 공구 수요

- 북미 및 유럽에서 재쉐어링 주도의 범용 고속도강 채용

- 항공우주 합금용 코발트 강화 M42 고속도강의 보급

- 북미의 DIY 및 홈 센터 붐

- CNC 기반의 적응 가공에 의한 고속도강 공구 수명의 연장

- 시장 성장 억제요인

- 몰리브덴 및 코발트 가격 변동

- 자동차 업계의 초경 공구 및 PCD 공구로의 급속한 시프트

- 탄소 중립에 의한 공구 수명의 의무화

- 유럽의 PM-HSS 생산 능력의 한계 및 공급의 병목

- 밸류체인 및 공급망 분석

- 규제 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자 및 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

- 세계의 제조업의 전망

- 기계 가공 산업에 영향을 미치는 정부 규제

- 철강 업계의 스냅샷

- 기술 스냅샷(첨가제 MFG, 나노코팅)

- 분말 야금 고속도강 스포트라이트

- 툴 포스트 및 툴 홀더에 대한 인사이트

- 지속가능성 및 순환 경제의 전망

- 세계의 혼란 및 공급망의 회복력

제5장 시장 규모 및 성장 예측

- 공구 유형별

- 밀링 커터

- 드릴

- 탭

- 리머 및 브로치

- 기타(톱니, 카운터싱크)

- 재료 등급별

- 종래 고속도강(M시리즈)

- 고코발트 고속도강(T시리즈/M42/M35)

- 분말 야금 고속도강(PM-HSS)

- 제조 공정별

- 기존 단조

- 분말 야금

- 판매 채널별

- OEM 직접 판매

- 산업용 유통업체

- 전자상거래 및 DIY 소매

- 최종 사용자 산업별

- 제조 및 자동차

- 석유 및 가스

- 광업 및 채석업

- 농업, 어업, 임업

- 건설업

- 헬스케어 및 제약

- 에너지 생성(터빈 및 원자력)

- 기타 최종 사용자(유통업 등)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 노르딕스(덴마크, 핀란드, 아이슬란드, 노르웨이, 스웨덴)

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN(인도네시아, 태국, 필리핀, 말레이시아, 베트남)

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 남아프리카

- 이집트

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 업계 주요 기업의 전략적 움직임

- 시장 점유율 분석(주요 기업)

- 기업 프로파일

- Sandvik AB

- Kennametal Inc.

- OSG Corporation

- Sumitomo Electric Industries Ltd.

- Nachi-Fujikoshi Corp.

- Walter AG

- Erasteel SAS

- YG-1 Co. Ltd.

- Tiangong International Co. Ltd.

- Mitsubishi Materials Corp.

- Guhring KG

- Dormer Pramet

- Somta Tools(Pty) Ltd.

- Niagara Cutter LLC

- Arch Cutting Tools

- DeWALT(Stanley Black & Decker)

- Addison & Co. Ltd.

- Morse Cutting Tools

- Union Tool Co.

- Chongqing Zhengtai Tools

제7장 시장 기회 및 전망

AJY 25.10.29The High Speed Steel Cutting Tools market size stands at USD 15.43 billion in 2025 and is on track to reach USD 19.79 billion by 2030, advancing at a 5.1% CAGR.

A resurgence of mid-volume machining, rapid industrialization in Asia, and wider use of powder metallurgy are the primary growth engines. Manufacturers are adopting cobalt-enriched grades for aerospace alloys, expanding e-commerce channels for DIY buyers, and refining adaptive CNC strategies that stretch tool life. Supply-side pressures remain, including volatile molybdenum and cobalt prices and the automotive sector's gradual pivot to carbide and PCD tools. Competitive moves center on targeted acquisitions, digital tool management, and carbon-neutral production commitments.

Global High Speed Steel Cutting Tools Market Trends and Insights

Demand for Low-cost Tooling in Emerging Asian Job Shops

Mounting numbers of tier-2 and tier-3 job shops across China, India, and ASEAN markets favor low initial tooling outlays. Conventional HSS tools meet that priority, especially as basic CNC adoption lets operators extend tool life by optimizing feeds and speeds. Chinese provincial support for indigenous machine-tool makers entrenches domestic sourcing, locking in repetitive demand cycles. The same trend spreads through India's automotive component clusters and Vietnam's electronics supply base, anchoring robust consumption for standard HSS milling cutters and drills.

DIY & Home-Improvement Retail Boom in North America

North American home-owners, hobbyists, and "prosumers" are driving double-digit online growth for consumer-grade HSS bits, taps, and hole saws. Tool makers now tailor geometries, coatings, and packaging to stand out on digital shelves, while power-tool brands bundle starter sets with cordless drills and compact lathes. Upskilled enthusiasts demanding industrial-style performance at modest price points have expanded the addressable segment, reinforcing the channel's 11.4% CAGR outlook.

Rapid Shift Toward Carbide & PCD Tools in Automotive

Electric vehicle platforms rely on thin-walled aluminum housings, composite brackets, and high-strength steel reinforcements. Carbide and PCD cutters deliver higher surface integrity and throughput on such materials, gradually displacing HSS in power-train, battery, and chassis lines. Automotive tooling decisions influence upstream tier suppliers and steel service centers, amplifying the drag on HSS demand, especially in Europe's high-volume plants.

Other drivers and restraints analyzed in the detailed report include:

- Re-shoring-led Adoption of Versatile HSS in North America & Europe

- Uptake of Cobalt-enriched M42 HSS for Aerospace Alloys

- Volatility in Molybdenum & Cobalt Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Milling cutters generated 32.4% of global 2024 revenue and anchor the High Speed Steel Cutting Tools market by virtue of their flexibility in face, slot, and profile machining. The segment benefits from continual refinement of radial chip thinning and high-efficiency roughing methods that raise metal-removal rates without compromising finish. Taps, in contrast, secure the quickest 6.8% CAGR through 2030 as thread-forming formats cut cycle times and avoid chip evacuation challenges. Chip-free threading aligns with automotive electronics housings and thin-section die-cast parts, pushing adoption across Asia and Eastern Europe.

Cost-sensitive job shops still prize HSS drills, reamers, and broaches for hole-making and finishing, while saws and countersinks meet niche needs in maintenance and repair. Digital design platforms now simulate chip flow, rake angle, and coolant delivery to customize cutting edges for each substrate. By leveraging such software, toolmakers unlock new shelf life even within standard HSS chemistries, reinforcing milling cutters' central role in the High Speed Steel Cutting Tools market.

Conventional M-series grades held 48% revenue share in 2024 thanks to broad availability and competitive pricing for mid-toughness jobs. Powder metallurgy variants command only 14.5% of output today, yet they capture disproportionate growth at 8.3% CAGR. Uniform carbide dispersion, refined grain boundaries, and reduced segregation give PM-HSS an edge when machining aerospace fasteners or medical implants where minimal chipping is critical. Cobalt-rich M42 and M35 maintain a strategic niche for heat-resistant alloys, bridging the cost gulf between PM and standard types.

The High Speed Steel Cutting Tools market size attached to PM-HSS is poised to expand as Europe resolves capacity gaps and as Asian players upscale domestic atomizing lines. Additive manufacturing trials also explore HSS powder blends with tailored hardness gradients, broadening future design possibilities and supporting long-term material-grade diversification across the High Speed Steel Cutting Tools market.

The High-Speed Steel Cutting Tools Market Report is Segmented by Tool Type (Drills and More), by Material Grade (Conventional HSS (M-Series) and More), by Production Process (Powder Metallurgy and More), by Distribution Channel (Direct OEM Sales and More), by End-User Industry (Oil & Gas and More) and by Geography (North America and More). The Report Offers Market Size and Forecasts in Value (USD) for all the Above Segments.

Geography Analysis

Asia leads the High Speed Steel Cutting Tools market with a 46.2% revenue share and a 6.3% CAGR forecast, thanks to China's electronics and machine-tool build-outs, India's automotive clusters, and Vietnamese assembly exports. Domestic tool makers now climb the value chain, adopting TiN and AlCrN coatings and pushing PM adoption, thereby reducing reliance on imports and cementing regional self-sufficiency.

North America ranks second and is revitalized by reshoring programs, defense offsets, and a thriving DIY culture. Hybrid machining cells in aerospace and energy plants require versatile cutters that thrive in adaptive CNC environments. E-commerce penetration also gives small workshops direct access to specialty taps and reamers, broadening High Speed Steel Cutting Tools market participation.

Europe sustains a technologically advanced yet capacity-constrained scenario. Limited PM-HSS supply elongates lead times for premium cutters. Nevertheless, German, French, and UK plants emphasize sustainable reconditioning and closed-loop recycling to hit carbon-reduction targets. Tool life monitoring and ISO 14001 programs elevate demand for data-rich HSS solutions despite carbide encroachment in automotive drivetrain lines.

South & Central America depend on Brazil's industrial base, while the Middle East leans on energy equipment refurbishment and ongoing infrastructure builds. Africa's demand cluster arises in South African mining supply and Egyptian component plants. Collectively, these emerging territories reflect the High Speed Steel Cutting Tools market's potential for diversification and localized value-add.

- Sandvik AB

- Kennametal Inc.

- OSG Corporation

- Sumitomo Electric Industries Ltd.

- Nachi-Fujikoshi Corp.

- Walter AG

- Erasteel SAS

- YG-1 Co. Ltd.

- Tiangong International Co. Ltd.

- Mitsubishi Materials Corp.

- Guhring KG

- Dormer Pramet

- Somta Tools (Pty) Ltd.

- Niagara Cutter LLC

- Arch Cutting Tools

- DeWALT (Stanley Black & Decker)

- Addison & Co. Ltd.

- Morse Cutting Tools

- Union Tool Co.

- Chongqing Zhengtai Tools

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for Low-cost Tooling in Emerging Asian Job Shops

- 4.2.2 Re-shoring-led Adoption of Versatile HSS in North America & Europe

- 4.2.3 Uptake of Cobalt-enriched M42 HSS for Aerospace Alloys

- 4.2.4 DIY & Home-Improvement Retail Boom in North America

- 4.2.5 CNC-based Adaptive Machining Extending HSS Tool Life

- 4.3 Market Restraints

- 4.3.1 Volatility in Molybdenum & Cobalt Prices

- 4.3.2 Rapid Shift Toward Carbide & PCD Tools in Automotive

- 4.3.3 Carbon-neutrality-driven Tool-life Mandates

- 4.3.4 Limited European PM-HSS Capacity & Supply Bottlenecks

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Global Manufacturing Sector Outlook

- 4.8 Government Regulations Impacting Machining Industry

- 4.9 Steel Industry Snapshot

- 4.10 Technology Snapshot (Additive MFG, Nanocoatings)

- 4.11 Spotlight on Powder Metallurgy HSS

- 4.12 Insights on Tool Posts & Tool Holders

- 4.13 Sustainability & Circular-Economy Outlook

- 4.14 Global Disruptions and Supply Chain Resilience

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Tool Type

- 5.1.1 Milling Cutters

- 5.1.2 Drills

- 5.1.3 Taps

- 5.1.4 Reamers & Broaches

- 5.1.5 Others (Saws, Countersinks)

- 5.2 By Material Grade

- 5.2.1 Conventional HSS (M-Series)

- 5.2.2 High-Cobalt HSS (T-Series/M42/M35)

- 5.2.3 Powder-Metallurgy HSS (PM-HSS)

- 5.3 By Production Process

- 5.3.1 Conventional Forged

- 5.3.2 Powder Metallurgy

- 5.4 By Distribution Channel

- 5.4.1 Direct OEM Sales

- 5.4.2 Industrial Distributors

- 5.4.3 E-commerce/DIY Retail

- 5.5 By End-user Industry

- 5.5.1 Manufacturing & Automotive

- 5.5.2 Oil & Gas

- 5.5.3 Mining & Quarrying

- 5.5.4 Agriculture, Fishing & Forestry

- 5.5.5 Construction

- 5.5.6 Healthcare & Pharmaceutical

- 5.5.7 Energy Generation (Turbines & Nuclear)

- 5.5.8 Other End users (distributive trade, etc.)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 UAE

- 5.6.5.3 Turkey

- 5.6.5.4 South Africa

- 5.6.5.5 Egypt

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Strategic Moves by Key Players in the Industry

- 6.2 Market Share Analysis (Key Players)

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.3.1 Sandvik AB

- 6.3.2 Kennametal Inc.

- 6.3.3 OSG Corporation

- 6.3.4 Sumitomo Electric Industries Ltd.

- 6.3.5 Nachi-Fujikoshi Corp.

- 6.3.6 Walter AG

- 6.3.7 Erasteel SAS

- 6.3.8 YG-1 Co. Ltd.

- 6.3.9 Tiangong International Co. Ltd.

- 6.3.10 Mitsubishi Materials Corp.

- 6.3.11 Guhring KG

- 6.3.12 Dormer Pramet

- 6.3.13 Somta Tools (Pty) Ltd.

- 6.3.14 Niagara Cutter LLC

- 6.3.15 Arch Cutting Tools

- 6.3.16 DeWALT (Stanley Black & Decker)

- 6.3.17 Addison & Co. Ltd.

- 6.3.18 Morse Cutting Tools

- 6.3.19 Union Tool Co.

- 6.3.20 Chongqing Zhengtai Tools