|

시장보고서

상품코드

1842516

vEPC(가상화 Evolved Packet Core) : 시장 점유율 분석, 업계 동향, 통계, 성장 예측(2025-2030년)Virtualized Evolved Packet Core - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

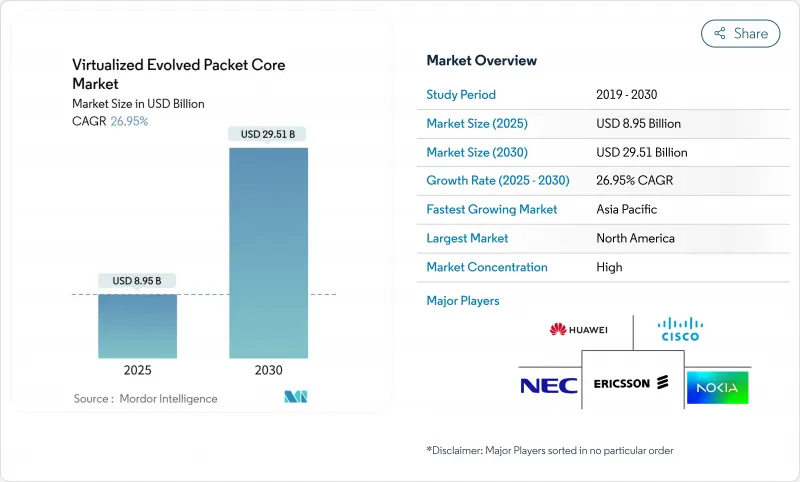

vEPC(가상화 EPC) 시장 규모는 2025년에 89억 5,000만 달러로 평가되었고, 예측 기간(2025-2030년)의 CAGR 26.95%로 성장할 전망되며, 2030년에 295억 1,000만 달러에 달할 것으로 예측됩니다.

성장은 5G 독립형(Standalone) 구축 확대, 기업용 사설 모바일 네트워크 수요 증가, 에너지 효율적인 가상화 코어를 선호하는 통신사의 지속가능성 요구사항에서 비롯됩니다. 통신사들은 자본 및 운영 비용을 절감하기 위해 소프트웨어 정의 네트워크 기능을 가속화하는 한편, 하이퍼스케일 퍼블릭 클라우드 파트너십을 통해 신속한 서비스 출시와 글로벌 커버리지를 실현합니다. 아시아태평양 지역은 정부 지원 디지털 프로그램에 힘입어 도입을 주도하는 반면, 북미는 네트워크 슬라이싱과 엣지-클라우드 시너지를 통한 차별화를 추진하고 있습니다. 한편 유럽은 규정 준수 및 에너지 효율성을 강조하며, 이는 기술 요구사항과 공급업체 선정에 영향을 미칩니다./p>

세계의 vEPC(가상화 EPC) 시장 동향 및 인사이트

가속화된 5G 구축, 클라우드 네이티브 코어 요구 증가

클라우드 네이티브 서비스 기반 아키텍처는 진정한 5G 독립형(SA) 네트워크에 필수적이며, 네트워크 슬라이싱과 프리미엄 서비스를 추구하는 통신사에게 vEPC는 필수 투자 항목입니다. 에릭슨은 2024년 말까지 120건 이상의 상용 5G 코어 계약을 확보했으며, 전 세계 37개 상용 5G SA 네트워크를 지원하며 상용화 준비가 완료되었음을 입증했습니다. T-Mobile과 같은 선행 기업들은 전국적 5G SA를 활용해 네트워크 슬라이스 기반 영상 통화를 도입함으로써 차별화된 가격 모델을 구축했습니다. 경쟁 압박으로 뒤처진 통신사들은 현대화를 가속화하지 않으면 고객 이탈 위험에 직면합니다. 클라우드 네이티브 코어는 소규모 모바일 가상 네트워크 사업자(MVNO)가 기업용 IoT 틈새 시장에 빠르게 진입할 수 있는 길도 열어줍니다. 결과적으로 가상화 진화 패킷 코어(vEPC) 시장은 단기적으로 복합적인 도입 사이클을 경험하고 있습니다.

네트워크 기능 가상화(NFV)를 통한 자본 지출/운영 비용 절감

vEPC 구축으로 워크로드가 일반 하드웨어 및 공유 클라우드 리소스로 전환되면서 사업자들은 상당한 비용 절감을 기록하고 있습니다. 연구에 따르면 단일 하드웨어 코어 대비 자본 지출이 68% 감소하고 운영 비용이 67% 절감되었습니다. 디지털 나시오날 베르하드는 가상화 코어 기반 의도 기반 자동화 운영으로 전환한 후 99.8%의 네트워크 가동률을 달성하고 고객 불만 해결 시간을 90% 단축했습니다. 에너지 절감으로 추가 22% 효율성을 확보해 예산 및 지속가능성 목표를 동시에 달성했습니다. 서비스 출시 가속화로 수익 창출 기간이 1년 이상에서 6개월 미만으로 단축되었습니다. 이러한 경제성으로 vEPC는 선택적 투자에서 이사회 수준의 필수 투자 항목으로 전환되고 있습니다. 벤더들은 이제 AI 기반 오케스트레이션을 내장해 운영 워크로드를 더욱 축소하고 있습니다.

기존 물리적 EPC에 대한 통신사의 관성

투자된 비용과 미션 크리티컬한 위험 회피 성향은 가상화 계획을 지연시킵니다. 쓰리UK는 노키아의 수명 종료된 CloudBand를 현대화가 불가피해졌을 때만 교체했으며, 이는 안정적인 트래픽 흐름을 방해하기를 꺼리는 태도를 보여줍니다. 버라이즌의 장기화된 5G SA 출시 사례는 혁신 선도 기업조차도 마이그레이션 복잡성에 직면함을 보여줍니다. 성숙 시장은 강화된 규제 감독과 엄격한 서비스 수준 기대치로 인해 변화 관리가 더욱 어려워진다. 결과적으로 물리적 코어는 경제적 효용이 정당화되는 기간보다 더 오래 유지되며, 이는 vEPC(가상화 EPC) 시장의 단기적 성장 동력을 약화시킨다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 인더스트리 4.0과 캠퍼스 연결성을 위한 프라이빗 LTE/5G 네트워크

- 에너지 효율적인 코어 네트워크를 위한 통신사 지속 가능성 의무

- 멀티 테넌트 클라우드의 보안 및 규정 준수 문제

부문 분석

2024년 vEPC(가상화 EPC) 시장 점유율의 63%는 클라우드 구현이 차지하며, 이는 통신사들이 탄력적 확장성과 신속한 서비스 반복을 선호함을 반영합니다. 하이퍼스케일러들이 통신 기능 세트를 강화함에 따라 클라우드 부문은 32%의 연평균 복합 성장률(CAGR)로 성장할 것으로 예상되며, 온프레미스 및 하이브리드 대안을 앞지를 전망입니다. 삼성, TELUS, AWS는 북미 최초의 가상 로밍 게이트웨이를 구축했으며, 이는 제어 평면 요소가 퍼블릭 클라우드에서 네이티브로 실행될 때 국경 간 서비스 혁신이 활성화됨을 입증합니다. 이러한 사례들은 인프라 소유권보다 민첩성을 중시하는 광범위한 전환을 뒷받침합니다.

데이터를 현지에 보유하는 사업자들은 클라우드 경제성을 포기하지 않으면서도 주권 규정을 충족하기 위해 과도기적 하이브리드 모델을 채택하고 있습니다. 에릭슨의 컴팩트 패킷 코어(Compact Packet Core)는 전개 복잡성을 80% 줄이고 에너지 사용량을 30% 절감하여 2차 통신사에 클라우드 준비형 번들을 매력적으로 만듭니다. 성과 기반 가격 책정을 규정하는 계약이 증가함에 따라 vEPC(가상화 EPC) 시장은 AI 지원 운영과 같은 관리형 서비스 부가 기능을 내재화하고 있습니다. 소규모 지역 통신사와 MVNO는 SaaS 제공 방식을 활용해 분기 단위가 아닌 몇 주 만에 신규 서비스를 출시하며 고객 기반을 확대하고 있습니다.

vEPC(가상화 EPC) 시장 보고서는 전개 모드(클라우드, 온프레미스, 하이브리드), 애플리케이션(IoT 및 M2M, 모바일 프라이빗 네트워크(MPN) 및 MVNO, 광대역 무선 액세스(BWA), LTE/VoLTE/VoWiFi, 5G 비독립형(NSA) 코어 등), 최종 사용자(통신 사업자, 기업 및 산업 분야, 정부 및 공공 안전, 클라우드 서비스 제공업체, MVNE/MVNO), 지역별로 분류됩니다.

지역 분석

아시아태평양 지역은 2024년 vEPC(가상화 EPC) 시장 규모의 38%를 차지했으며, 이는 20,000개 이상의 산업용 사례를 포함하는 중국의 5,325개 가동 중인 사설 5G 네트워크에 힘입은 결과입니다. 정부의 인센티브와 주파수 정책은 제조업의 도입을 가속화하고 있으며, 중국 정부는 2025년까지 300개 도시에 5G-Advanced 커버리지를 구축하기 위해 30억 달러를 투자할 예정입니다. 인도의 5G SA 커버리지 52%(유럽 2% 대비 압도적 우위)는 클라우드 우선 구축을 통해 신흥 경제권이 기존 아키텍처를 도약하는 방식을 보여줍니다. 이러한 프로그램은 공급업체가 R&D 및 생산을 현지화하도록 강제하는 규모를 제공하여 아시아태평양 지역의 vEPC(가상화 EPC) 시장 리더십을 강화합니다.

북미는 네트워크 슬라이싱과 O-RAN 통합을 통한 프리미엄 서비스 계층을 강조합니다. 버라이즌은 13만 대 이상의 O-RAN 지원 라디오를 배치하고 슬라이스 기반 영상 통화를 출시해 고가치 가입자를 확보했습니다. 기업 동맹은 주목할 만한 사례 연구를 생산합니다 : BMW 스파턴버그 공장은 프라이빗 5G 도입 후 가동 시간 향상을 실현했으며, 삼성, 텔러스, AWS는 완전 가상화 코어를 통한 로밍 혁신을 시연했습니다. 스펙트럼 임대 관련 규제 명확화는 캠퍼스 구축을 추가로 지원하여 가상화 진화 패킷 코어 시장에서의 지역 기여도를 강화합니다.

유럽에서는 다양한 기세를 볼 수 있습니다. 영국 Three는 에릭슨에 9Tbps 클라우드 네이티브 코어 계약을 수주했으며, O2 Telefonica는 AWS 호스팅 코어에서 6개월 만에 100만 사용자 돌파를 달성했습니다. 그러나 영국 통신 보안법과 같은 엄격한 보안 규정 및 공격적인 현대화보다 안정성을 중시하는 위험 회피 문화로 인해 전체 5G SA 가용성은 2%에 그칩니다. 통신사들은 에너지 효율성과 오픈-RAN 실험에 주력하고 있으며, 도이체 텔레콤의 O-RAN 타운 이니셔티브가 이를 입증합니다. 이러한 우선순위는 당장의 지출을 억제하지만, 가상화 진화 패킷 코어 시장 내에서 높은 상호운용성과 저전력 vEPC 솔루션에 대한 장기적 수요를 창출합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- LTE/4G 가입자 기반의 급속한 성장

- 클라우드 네이티브 코어를 요구하는 가속화된 5G 도입

- 네트워크 기능 가상화(NFV)를 통한 자본 지출(CapEx)/운영 지출(OpEx) 절감

- 인더스트리 4.0 및 캠퍼스 연결성을 위한 프라이빗 LTE/5G 네트워크

- 분산된 사용자 평면 오프로드를 가능하게 하는 엣지-클라우드 시너지

- 에너지 효율적인 코어 네트워크를 위한 통신사 지속가능성 의무

- 시장 성장 억제요인

- 기존 물리적 EPC에 대한 통신사의 관성

- 멀티테넌트 클라우드의 보안 및 규정 준수 문제

- 개방형 분산 코어 간 상호운용성 격차

- 5G SA 워크로드에 대한 예측 불가능한 하이퍼스케일 클라우드 총소유비용(TCO)

- 가치 및 공급망 분석

- 규제 상황

- 기술적 전망

- 투자분석(기반라인별)

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모와 성장 예측

- 전개 형태별

- 클라우드 기반

- 온프레미스

- 하이브리드

- 용도별

- IoT 및 M2M

- 모바일 프라이빗 네트워크(MPN) 및 MVNO

- 광대역 무선 액세스(BWA)

- LTE/VoLTE/VoWiFi

- 5G 비독립형(NSA) 코어

- 5G 독립형(SA) 코어

- 최종 사용자별

- 통신 사업자

- 기업 및 업계별

- 정부 및 공공안전

- 클라우드 서비스 제공업체

- MVNE/MVNO

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- GCC 국가

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장의 집중

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- Ericsson

- Huawei Technologies

- Nokia

- Cisco Systems

- ZTE

- Samsung Electronics

- NEC Corporation

- Mavenir

- Microsoft(Affirmed Networks)

- Athonet(HPE)

- Telrad Networks

- Core Network Dynamics

- VMware

- Juniper Networks

- Red Hat(IBM)

- Intel

- Hewlett Packard Enterprise

- Casa Systems

- Parallel Wireless

- Druid Software

제7장 시장 기회와 전망

HBR 25.10.29The Virtualized Evolved Packet Core Market size is estimated at USD 8.95 billion in 2025, and is expected to reach USD 29.51 billion by 2030, at a CAGR of 26.95% during the forecast period (2025-2030).

Growth stems from 5G standalone rollouts, rising enterprise demand for private mobile networks, and operator sustainability mandates that favor energy-efficient virtualized cores. Telcos accelerate software-defined network functions to slash capital and operating outlays, while hyperscale public-cloud partnerships allow rapid service launches and global coverage. Asia Pacific drives adoption on the back of government-backed digital programs, whereas North America pushes differentiation through network slicing and edge-cloud synergies. Meanwhile, Europe emphasizes compliance and energy efficiency, a stance that shapes technical requirements and vendor selection.

Global Virtualized Evolved Packet Core Market Trends and Insights

Accelerated 5G Rollouts Demanding Cloud-Native Cores

Cloud-native service-based architectures are mandatory for true 5G standalone networks, making vEPC a non-negotiable investment for operators pursuing network slicing and premium-tier services. Ericsson secured more than 120 commercial 5G core contracts by late 2024, powering 37 live 5G SA networks worldwide, providing tangible proof of commercial readiness. Early movers such as T-Mobile leveraged nationwide 5G SA to introduce network-slice-enabled video calling, which positions them for differentiated pricing models. Competitive pressure compels lagging carriers to accelerate modernization or risk churn. Cloud-native cores also give smaller mobile virtual network operators fast-track entry into enterprise IoT niches. Consequently, the Virtualized Evolved Packet Core market experiences a compounding adoption cycle in the short term.

CapEx/OpEx Savings from Network-Function Virtualization

Operators record sizeable cost reductions as vEPC setups shift workloads to commodity hardware and shared cloud resources. Studies show 68% lower capital outlays and 67% savings on operating expense versus monolithic hardware cores. Digital Nasional Berhad achieved 99.8% network uptime and cut customer-complaint resolution time by 90% after moving to intent-based automated operations on a virtualized core. Energy savings add a further 22% efficiency, meeting both budget and sustainability goals. Faster service launches shorten time-to-revenue from over a year to less than six months. These economics shift vEPC from optional to essential in board-level investment plans. Vendors now embed AI-powered orchestration to shrink operational workloads even further.

Operator Inertia Toward Legacy Physical EPCs

Sunk investments and mission-critical risk aversion slow virtualization plans. Three UK replaced Nokia's end-of-life CloudBand only when forced to modernize, underscoring reluctance to disrupt stable traffic flows. Verizon's protracted 5G SA launch shows that even innovation leaders grapple with migration complexity. Mature markets face elevated regulatory oversight and stringent service-level expectations, making change management even more difficult. As a result, physical cores persist for longer than their economic utility justifies, dampening short-term momentum in the Virtualized Evolved Packet Core market.

Other drivers and restraints analyzed in the detailed report include:

- Private LTE/5G Networks for Industry 4.0 and Campus Connectivity

- Telco Sustainability Mandates for Energy-Efficient Core Networks

- Security and Compliance Concerns on Multi-Tenant Cloud

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud implementations represented 63% of the Virtualized Evolved Packet Core market share in 2024, reflecting carriers' preference for elastic scaling and rapid service iteration. The cloud cohort is forecast to grow at 32% CAGR, outpacing on-premises and hybrid alternatives as hyperscalers strengthen telecom feature sets. Samsung, TELUS, and AWS created North America's first virtual roaming gateway, which proves that cross-border service innovations flourish when control-plane elements run natively on the public cloud. These examples underpin a broad shift where infrastructure ownership yields to agility.

Operators that retain data on-site embrace transitional hybrid models to satisfy sovereignty rules without forfeiting cloud economics. Ericsson's Compact Packet Core reduces deployment complexity by 80% and cuts energy use by 30%, making cloud-ready bundles attractive to tier-2 carriers. As more contracts stipulate outcome-based pricing, the Virtualized Evolved Packet Core market embeds managed-service add-ons such as AI-assisted operations. Small regional telcos and MVNOs leverage SaaS delivery to launch new offers in weeks rather than quarters, broadening the customer base.

The Virtualized Evolved Packet Core Market Report is Segmented by Deployment Mode (Cloud, On-Premise, and Hybrid), Application (IoT and M2M, Mobile Private Networks (MPN) and MVNO, Broadband Wireless Access (BWA), LTE/VoLTE/VoWiFi, 5G Non-Standalone (NSA) Core, and More), End-User (Telecom Operators, Enterprises and Industrial Verticals, Government and Public Safety, Cloud Service Providers, and MVNE/MVNOs), and Geography.

Geography Analysis

Asia Pacific generated 38% of the 2024 Virtualized Evolved Packet Core market size, supported by China's 5,325 live private 5G networks that include more than 20,000 industrial use cases. Government incentives and spectrum policies accelerate manufacturing adoption, with Beijing investing USD 3 billion in 5G-Advanced coverage across 300 cities in 2025. India's 52% 5G SA coverage, well ahead of Europe's 2%, illustrates how emerging economies leapfrog legacy architectures via cloud-first rollouts. These programs supply scale that compels vendors to localize R&D and production, reinforcing Asia Pacific's leadership in the Virtualized Evolved Packet Core market.

North America emphasizes premium service tiers through network slicing and O-RAN integration. Verizon deployed more than 130,000 O-RAN-capable radios and launched slice-based video calling to capture high-value subscribers. Enterprise alliances produce headline case studies: BMW's Spartanburg plant realized uptime gains after adopting private 5G, and Samsung, TELUS, and AWS demonstrated roaming innovation via fully virtualized cores. Regulatory clarity around spectrum leasing further supports campus deployments, bolstering regional contribution to the Virtualized Evolved Packet Core market.

Europe shows mixed momentum. Three UK awarded Ericsson a 9 Tbps cloud-native core contract, and O2 Telefonica surpassed 1 million users on its AWS-hosted core within six months. Yet overall 5G SA availability stands at 2%, restrained by strict security rules such as the UK Telecoms Security Act and by a risk-averse culture that favors stability over aggressive modernization. Operators focus on energy efficiency and open-RAN experimentation, evidenced by Deutsche Telekom's O-RAN Town initiative. These priorities temper immediate spending but create long-term demand for highly interoperable, low-power vEPC solutions within the Virtualized Evolved Packet Core market.

- Ericsson

- Huawei Technologies

- Nokia

- Cisco Systems

- ZTE

- Samsung Electronics

- NEC Corporation

- Mavenir

- Microsoft (Affirmed Networks)

- Athonet (HPE)

- Telrad Networks

- Core Network Dynamics

- VMware

- Juniper Networks

- Red Hat (IBM)

- Intel

- Hewlett Packard Enterprise

- Casa Systems

- Parallel Wireless

- Druid Software

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid growth in LTE/4G subscriber base

- 4.2.2 Accelerated 5G roll-outs demanding cloud-native cores

- 4.2.3 CapEx / OpEx savings from network-function virtualization

- 4.2.4 Private LTE/5G networks for Industry 4.0 and campus connectivity

- 4.2.5 Edge-cloud synergies enabling distributed user-plane off-load

- 4.2.6 Telco sustainability mandates for energy-efficient core networks

- 4.3 Market Restraints

- 4.3.1 Operator inertia toward legacy physical EPCs

- 4.3.2 Security and compliance concerns on multi-tenant cloud

- 4.3.3 Inter-operability gaps across open, disaggregated cores

- 4.3.4 Unpredictable hyperscale cloud TCO for 5G SA workloads

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Investment Analysis (Baseline-specific)

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-based

- 5.1.2 On-premise

- 5.1.3 Hybrid

- 5.2 By Application

- 5.2.1 IoT and M2M

- 5.2.2 Mobile Private Networks (MPN) and MVNO

- 5.2.3 Broadband Wireless Access (BWA)

- 5.2.4 LTE/VoLTE/VoWiFi

- 5.2.5 5G Non-Standalone (NSA) Core

- 5.2.6 5G Standalone (SA) Core

- 5.3 By End User

- 5.3.1 Telecom Operators

- 5.3.2 Enterprises and Industrial Verticals

- 5.3.3 Government and Public Safety

- 5.3.4 Cloud Service Providers

- 5.3.5 MVNE/MVNOs

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Russia

- 5.4.3.5 Italy

- 5.4.3.6 Spain

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Australia and New Zealand

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 GCC Countries

- 5.4.5.1.2 Turkey

- 5.4.5.1.3 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Egypt

- 5.4.5.2.4 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Ericsson

- 6.4.2 Huawei Technologies

- 6.4.3 Nokia

- 6.4.4 Cisco Systems

- 6.4.5 ZTE

- 6.4.6 Samsung Electronics

- 6.4.7 NEC Corporation

- 6.4.8 Mavenir

- 6.4.9 Microsoft (Affirmed Networks)

- 6.4.10 Athonet (HPE)

- 6.4.11 Telrad Networks

- 6.4.12 Core Network Dynamics

- 6.4.13 VMware

- 6.4.14 Juniper Networks

- 6.4.15 Red Hat (IBM)

- 6.4.16 Intel

- 6.4.17 Hewlett Packard Enterprise

- 6.4.18 Casa Systems

- 6.4.19 Parallel Wireless

- 6.4.20 Druid Software

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment