|

시장보고서

상품코드

1842528

일회용 주사기 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Disposable Syringes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

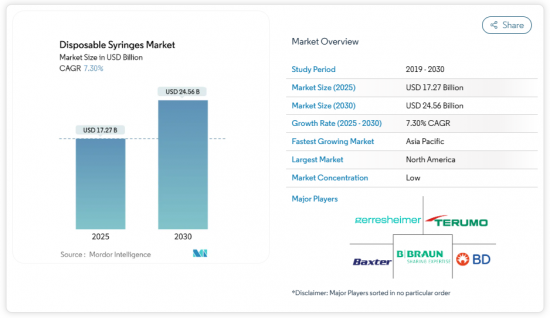

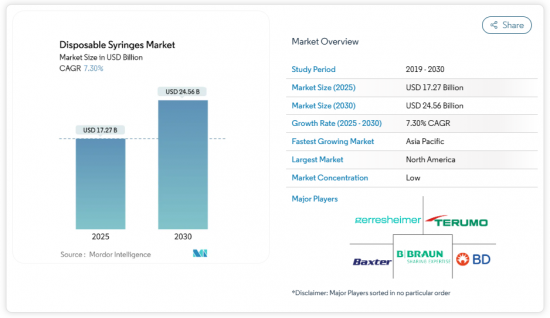

일회용 주사기 시장은 2025년에 172억 7,000만 달러에 달할 것으로 평가되고 있으며, 2030년에는 245억 6,000만 달러에 이를 전망으로, CAGR 7.30%로 성장할 것으로 예측됩니다.

품질 기준의 엄격화, 생물 제제의 판매량 증가, 가정 치료의 보급이 이 시장 확대의 주요 요인입니다. 미국 식품의약국의 품질요건을 충족하지 못한 공급업체와의 계약을 의료기관이 종료하면서 Tier-1 제조업체는 새로운 수주를 획득하고 있습니다. 동시에, 주사 가능한 GLP-1 치료제 및 기타 생물학적 제제는 프리미엄 프리필드 및 안전한 포맷의 급증을 견인하여, 일회용 주사기 시장 내에 폭넓은 가치 풀을 창출하고 있습니다. 만성 치료제의 자체 투여로의 전환은 수지 가격의 변동과 일회용 플라스틱의 모니터링 강화와 관련된 마진 압력을 상쇄하여 수량 증가를 더욱 촉진하고 있습니다.

세계의 일회용 주사기 시장의 동향과 인사이트

NGO 주도의 주사 안전 캠페인이 신흥 시장에서의 채용을 가속

다자간 자금 지원에 지원된 지역의 능력 확대로 기존 접종 프로그램을 위협했던 22억 단위의 자동 주사기 재고 갭이 축소되었습니다. WHO의 인증을 받은 아프리카 최초의 제조업체인 리바이탈 헬스케어는 현재 연간 3억개 이상의 생산을 목표로 하고 있으며 수입품에 비해 납품 비용을 15-20% 줄이고 있습니다. 지역 제조 거점은 공중 보건 응급 상황에서 공급 회복력을 강화하고 물류 비용을 줄임으로써 신흥 시장이 재사용되는 의료기기로부터 전환될 수 있도록 합니다. 이 이니셔티브는 지속 가능한 생산 생태계를 구축함으로써 대응 가능한 일회용 주사기 시장을 확대할 수 있음을 입증합니다.

HIV와 HBV를 억제하기 위해 일회용 주사기로의 전환을 의무화

개발 도상 지역에서는 연간 160억회 이상의 주사가 진행되고 있지만, 그 중 40%는 여전히 재사용되고 있습니다. 규제 당국은 안전하지 않은 주사로 인한 연간 추정 사망자 수 130만 명을 줄이기 위해 재멸균 가능한 장비의 단계적 금지를 도입하고 있습니다. 자동 인입장치와 바늘 캡이 장착된 안전한 주사기는 15-25%의 비싼 가격에도 불구하고 기본 사양으로 자리잡고 있습니다. 세계 의료 시스템은 또한 장치의 형식을 변경할 때 교육 비용을 부담하고 있으며 대규모 안전 포트폴리오를 가진 공급업체에게 유리한 견고한 수요를 창출하고 있습니다. 이러한 의무화로 볼 때 일회용 주사기 시장의 장기 수량 전망이 예상됩니다.

멸균 가능한 유리제 및 철제 대비 높은 비용 증가율

50-100회의 오토클레이브 멸균에 견디는 유리제 주사기는 개당 15-25달러이며, 대량생산 프로그램에서는 1회당 비용은 0.50달러 미만입니다. 일회용 플라스틱 주사기는 0.15-0.35달러로 판매되고 있지만 재사용 가능성이 없기 때문에 예산에 제약이 있는 시설에서는 자본 효율과 당장의 유동성 사이에서 선택하도록 강요됩니다. 멸균 인프라가 존재하는 경우, 관리자는 재사용 가능한 장비를 선호할 수 있으며, 전환 기세가 둔해집니다. 가격에 대한 민감도는 최저 가격으로 입찰을 우선하는 공적 입찰을 통해 자금 조달되는 백신 접종의 추진에서 특히 높게 유지되며, 이러한 시나리오에서는 일회용 주사기 시장의 성장이 억제됩니다.

부문 분석

종래의 의료기기도 여전히 스케일 효율은 높지만, 안전성이 높은 의료기기가 빠르고 성장하고 있으며 조달의 기호도 변화하고 있습니다. 2024년에는 기존 주사기가 일회용 주사기 시장의 62.61%를 차지하였지만, 노동재해 방지 정책의 강화에 따라 안전형은 2030년까지의 CAGR이 7.98%로 예상됩니다. 수축식 시스템은 사용자의 절차를 최소화하고 기존 프로토콜에 원활하게 통합할 수 있으므로 프리미엄 카테고리를 지배합니다. 북미와 유럽의 시설은 현재 가치 기반 구매 대시보드에 주사침 자상 및 손상 지표를 통합하여 승인된 안전 설계로의 계약 전환을 가속화하고 있습니다.

국내 성형능력을 갖춘 제조업체는 운임비용의 차이와 수입규제의 강화로부터 이익을 얻고 있습니다. 기존의 유리 배럴에서 고리형 올레핀 폴리머로의 전환으로 엔지니어는 더 많은 모양을 설계할 수 있어 간호사의 선호도에 영향을 미치는 인체공학적 요인을 개선할 수 있습니다. 안전기구는 평균 판매 가격이 15-25% 높기 때문에 마진을 통해 공구 업그레이드에 충분한 자금을 획득할 수 있습니다. 그 결과, 일회용 주사기 시장은 기존 라인과의 연관성을 완화시키거나 배제하지 않는 눈에 보이는 믹스 시프트를 계속 경험하고 있습니다.

치료용 주사기는 2024년 매출액의 51.21%를 차지하였으며 인슐린, 종양, 백신, GLP-1 등의 수요를 원동력으로 하여 일회용 주사기 시장의 성장을 주도하고 있습니다. 지역사회에서는 자가투여가 매월 안정된 실적을 끌어올리는 반면, 병원의 병동에서는 클로즈드 루프 제형 캐비닛과 통합된 호환 가능한 시스템이 인기를 얻고 있습니다. 비싼 생물학적 제형의 요법은 종종 페이로드의 효능을 보호하기 위해 적은 데드 스페이스 또는 코팅된 플런저를 필요로 하므로 단가가 높아집니다.

한편, 혈액 검체 채취는 CAGR 7.88%라는 빠른 속도로 성장하고 있으며, 얇은 바늘과 진공 대응 배럴 수요를 재구축하고 있습니다. 검사 자동화 플랫폼은 표준화된 치수에 의존하기 때문에 제조업체는 더 엄격한 공차를 보장해야 합니다. 고령화 사회의 만성 질환 모니터링 프로토콜은 샘플 채취를 반복하기 때문에 주사기 소비가 증가합니다. 신흥경제국에서도 진단검사에 대한 보험적용 확대가 더욱 성장을 지원하고 있습니다. 이러한 힘이 결합되어 일회용 주사기 시장 규모에 대한 진단약 기여 증가와 치료제 지상주의가 공존하는 균형잡힌 전망이 탄생하고 있습니다.

지역 분석

북미는 2024년 매출액의 39.91%를 차지했으며, 이는 엄격한 단속을 통해 비적합 수입품은 부적격 판정으로 차단하고 국내 공장은 신속한 검사로 보상되었기 때문입니다. BD의 연간 생산 능력 4억 8,500만 단위를 추가하는 멀티 사이트 프로그램은 지역 공급을 지원하고 팬데믹 대비 비축 사이클 동안 리드 타임을 단축합니다. 높은 수준의 건강 관리 지출은 자동 주사기에 대응하는 안전 주사기의 조기 채용을 지원하고, 지역의 생물 제제 파이프라인은 유리 및 COC 배럴의 지속적인 수요를 보장합니다. 새로운 FDA 품질 관리 시스템 규칙과 ISO 13485의 조화는 중복 감사를 줄이고 제조업체는 품질 엔지니어링 자원을 제품 혁신에 투입할 수 있습니다.

아시아태평양은 인도가 수입 의존도를 70%에서 50%로 줄이는 Production Linked Incentives를 개발하면서 2030년까지 연평균 복합 성장률(CAGR)이 가장 높은 8.12%가 될 것으로 예측됩니다. 국내 기업은 클린룸 업그레이드에 보조금을 받고 해외 파트너는 현지에서 금형을 설치할 때 관세 면제를 받을 수 있으므로 기존 공급업체에 대항하여 토지 구매 비용을 절감할 수 있습니다. 인도네시아, 베트남, 태국에서는 만성 질환의 이환율이 증가하고 있으며, 주사제의 기준선 양이 더욱 증가하고 있습니다. 이 지역은 또한 세계적인 브랜드에 의약품 충전 마감 서비스를 제공하고 있으며 특수 주사기 수출에 연동된 수요 급증을 창출하고 있습니다.

유럽은 성숙하지만 기술 중심 시장이며 의료기기 규정 준수로 포트폴리오의 체계적인 검토를 촉구하고 있습니다. 전용 시판 후 조사 부문을 가진 제조업체는 시장 접근성을 유지하고 있지만 수입 전용 소규모 기업은 임상 평가 요구 사항을 고민합니다. 조달 담당자는 효과적인 재활용 프로젝트와 사용 주기 동안 배출량이 적은 입찰을 선호하기 때문에 지속 가능성 지침이 복잡해지고 있습니다. 조지아에 있는 Jeresheimer의 최신 공장은 유럽 규제의 확실성과 북미 성장을 양립하는 통합 전략을 강조합니다. 독일과 프랑스에서 바이오시밀러 시장으로의 지속적인 진입은 일회용 주사기의 안정적인 프리미엄 부문 소비를 강화할 것으로 보입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 도입

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- NGO 주도의 주사 안전 캠페인이 신흥 시장에서의 채용을 가속

- HIV 및 HBV를 억제하기 위한 일회용 기기로의 이행 의무화

- 생물제제와 GLP-1 주사약의 급증

- 프리필드 자동 주사기 붐에 의한 고급 주사기 수요의 창출

- 중국제 주사기에 대한 미국 FDA의 품질 경고에 의해 Tier-1 제조업체에 공급량이 집중

- 3D 프린터에 의한 마이크로 몰드 금형으로 중규모 제조업체의 설비 투자 감소

- 시장 성장 억제요인

- 멸균 가능한 유리제 및 스틸제 장비 대비 높은 비용 증가율

- 각국 규제 당국이 요구하는 복잡한 신청 절차

- 불안정한 폴리프로필렌 및 시클로올레핀 폴리머 가격

- 의료용 일회용 플라스틱의 절감을 요구하는 ESG 압력 증가

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 기존 주사기

- 안전 주사기

- 수축식

- 비수축식

- 용도별

- 치료용 주사

- 예방접종

- 혈액 검체 채취

- 기타 용도

- 최종 사용자별

- 병원

- 진단 실험실

- 재택 헬스케어

- 기타 최종 사용자

- 소재별

- 플라스틱

- 유리

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Becton, Dickinson and Company

- B. Braun SE

- Terumo Corporation

- Nipro Corporation

- Gerresheimer AG

- Baxter International Inc.

- Cardinal Health

- Schott AG

- Hindustan Syringes & Medical Devices Ltd.

- Retractable Technologies Inc.

- Fresenius Kabi AG

- Sol-Millennium Medical

- APEX MEDICAL DEVICES

- Medtronic(Covidien)

- Stevanato Group

- Embecta Corp.

- Revital Healthcare

- Zhejiang Kindly Medical Devices

- Ypsomed Holding AG

- Jiangsu Delfu medical

- Zhejiang Jianfeng Medical

제7장 시장 기회와 전망

CSM 25.11.03The disposable syringes market is currently valued at USD 17.27 billion in 2025 and is forecast to reach USD 24.56 billion by 2030, advancing at a 7.30% CAGR.

Heightened enforcement of quality standards, rising biologics volumes, and faster adoption of home-based care are the primary forces behind this expansion. Tier-1 manufacturers are capturing new orders as health systems exit contracts with suppliers that failed to meet U.S. Food and Drug Administration quality requirements. At the same time, injectable GLP-1 therapeutics and other biologics are driving a sharp increase in premium pre-filled and safety formats, creating a wider value pool inside the disposable syringes market. A parallel shift toward patient self-administration of chronic therapies further lifts unit volumes, offsetting margin pressure linked to volatile resin prices and growing scrutiny of single-use plastics.

Global Disposable Syringes Market Trends and Insights

NGO-led Injection-Safety Campaigns Accelerate Emerging-Market Adoption

Local capacity expansion supported by multilateral funding has reduced the 2.2 billion unit auto-disable syringe gap that once threatened immunization programs. Revital Healthcare, the first WHO-prequalified African producer, now targets output beyond 300 million units a year, cutting delivered costs 15-20% compared with imports . Regional manufacturing hubs strengthen supply resilience during public-health emergencies and lower logistics expenses, positioning emerging markets to shift away from reused devices. The initiative demonstrates how directed grants can create lasting production ecosystems that widen the addressable disposable syringes market.

Mandated Transition to Single-Use Devices to Curb HIV & HBV

More than 16 billion injections are administered yearly in developing regions, and 40% still involve reused equipment. Regulators are introducing phased bans on re-sterilizable devices to reduce the estimated 1.3 million annual deaths tied to unsafe injections. Safety syringes with automatic retraction or needle shields are becoming the default specification despite a 15-25% price premium, as sterilization overheads often exceed acquisition costs. Global health systems also incur training expenses when switching device formats, creating sticky demand that favors suppliers with large safety portfolios. These mandates underpin long-term volume visibility for the disposable syringes market.

Up-front Cost Premium vs. Sterilizable Glass / Steel Devices

Glass syringes that survive 50-100 autoclave cycles cost USD 15-25 each, placing their per-use expense below USD 0.50 in high-volume programs. Disposable plastic units list at USD 0.15-0.35 but carry no reuse potential, forcing budget-constrained facilities to weigh capital efficiency against immediate liquidity. Where sterilization infrastructure exists, administrators sometimes favor reusable devices, slowing conversion momentum. Price sensitivity remains particularly acute in vaccination drives financed through public tenders that prioritize the lowest upfront bid, compressing growth for the disposable syringes market in those scenarios.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Biologics & GLP-1 Injectable Drugs

- US FDA Quality Alerts on China-Made Syringes Pivot Volume to Tier-1 Producers

- Growing ESG Pressure to Cut Single-Use Medical Plastics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional devices still deliver scale efficiencies, but safety formats are growing faster and reshaping procurement preferences. In 2024 conventional variants held 62.61% of the disposable syringes market, yet safety models are tracking a 7.98% CAGR through 2030 as occupational-hazard prevention policies tighten. Retractable systems dominate the premium category because they minimize user steps and integrate smoothly into existing protocols. Facilities in North America and Europe now embed needle-stick injury metrics in value-based purchasing dashboards, accelerating contract shifts toward approved safety designs.

Manufacturers with domestic molding capacity also benefit from freight-cost differentials and tightened import controls. The transition from legacy glass barrels to cyclic-olefin polymers gives engineers more geometry options, improving ergonomic factors that influence nurse preference. With safety devices carrying 15-25% higher average selling prices, margin capture is sufficient to fund tooling upgrades. As a result, the disposable syringes market continues to experience a visible mix shift that tempers, but does not eliminate, the relevance of conventional lines.

Therapeutic injections accounted for 51.21% of revenue in 2024 and remain the backbone of the disposable syringes market, powered by insulin, oncology, vaccine, and GLP-1 volumes. Self-administration pushes steady monthly throughput in community settings, while hospital wards favor compatible systems that integrate with closed-loop drug-dispensing cabinets. Premium biologic regimens frequently require low-dead-space or coated plungers to protect payload potency, translating into higher unit value.

Blood specimen collection, however, is registering a faster 7.88% CAGR and reshaping demand for thin-wall needles and vacuum-compatible barrels. Laboratory automation platforms rely on standardized dimensions, prompting manufacturers to guarantee tighter tolerances. Chronic disease monitoring protocols in aging populations add repeat sample draws that amplify syringe consumption. Even within emerging economies, expanded insurance coverage for diagnostic testing underpins incremental growth. Together these forces create a balanced outlook in which therapeutic supremacy coexists with a rising diagnostic contribution to disposable syringes market size.

The Disposable Syringes Market is Segmented by Product Type (Conventional Syringes and Safety Syringes [Retractable and Non-Retractable]), Application (Therapeutic Injections, Immunization, and More), End User (Hospitals, Diagnostic Laboratories, and More), Material (Plastic and Glass), and Geography (North America, Europe, Asia-Pacific, and More). The Market and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 39.91% of revenue in 2024 amid stringent enforcement actions that disqualified non-compliant imports and rewarded domestic plants with expedited inspections. BD's multi-site program to add 485 million units of annual capacity anchors regional supply and shortens lead times during pandemic stockpile cycles. High healthcare expenditure levels support early adoption of auto-injector compatible safety syringes, and the local biologics pipeline guarantees sustained demand for glass and COC barrels. Harmonization between the new FDA Quality Management System Regulation and ISO 13485 reduces audit duplication, allowing manufacturers to reallocate quality-engineering resources toward product innovation.

Asia-Pacific is projected to post the fastest 8.12% CAGR through 2030 as India deploys Production Linked Incentives that cut import dependency from 70% to 50%. Domestic firms receive subsidies for clean-room upgrades and international partners gain duty concessions when setting up local molds, shrinking landed costs against entrenched suppliers. Rising chronic-disease incidence across Indonesia, Vietnam, and Thailand further expands baseline injection volumes, while aging demographics amplify requirements for routine diagnostics. The region also supplies pharmaceutical fill-finish services to global brands, creating export-linked demand spikes for specialty syringes.

Europe remains a mature but technology-driven arena where Medical Device Regulation compliance prompts systematic portfolio reviews. Manufacturers with dedicated post-market surveillance units are retaining market access, while smaller import-only firms struggle with clinical evaluation requirements. Sustainability directives add complexity as procurement officers favor bids demonstrating validated recycling pilots or lower life-cycle emissions. Gerresheimer's newest plant in Georgia underscores a dual-continent strategy that balances European regulatory certainty with North American growth. Continued bio-similar market entry in Germany and France will reinforce steady, premium-segment consumption of disposable syringes.

- Beckton Dickinson

- B. Braun

- Terumo

- Nipro

- Gerresheimer

- Baxter

- Cardinal Health

- SCHOTT

- Hindustan Syringes & Medical Devices Ltd.

- Retractable Technologies

- Fresenius

- Sol-Millennium Medical

- APEX MEDICAL DEVICES

- Medtronic

- Stevanato Group

- Embecta Corp.

- Revital Healthcare

- Zhejiang Kindly Medical Devices

- Ypsomed

- Jiangsu Delfu medical

- Zhejiang Jianfeng Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 NGO-led injection-safety campaigns accelerate emerging-market adoption

- 4.2.2 Mandated transition to single-use devices to curb HIV & HBV

- 4.2.3 Surge in biologics & GLP-1 injectable drugs

- 4.2.4 Pre-filled auto-injector boom creates premium syringe demand

- 4.2.5 US FDA quality alerts on China-made syringes pivot volume to Tier-1 producers

- 4.2.6 3-D printed micro-mold tooling slashes cap-ex for mid-scale makers

- 4.3 Market Restraints

- 4.3.1 Up-front cost premium vs. sterilizable glass/steel devices

- 4.3.2 Complex, country-specific regulatory filings

- 4.3.3 Volatile polypropylene & cyclo-olefin polymer prices

- 4.3.4 Growing ESG pressure to cut single-use medical plastics

- 4.4 Regulatory Landscape

- 4.5 Porters Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Conventional Syringes

- 5.1.2 Safety Syringes

- 5.1.2.1 Retractable

- 5.1.2.2 Non-Retractable

- 5.2 By Application

- 5.2.1 Therapeutic Injections

- 5.2.2 Immunization

- 5.2.3 Blood Specimen Collection

- 5.2.4 Other Applications

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Diagnostic Laboratories

- 5.3.3 Home Healthcare Settings

- 5.3.4 Other End Users

- 5.4 By Material

- 5.4.1 Plastic

- 5.4.2 Glass

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Becton, Dickinson and Company

- 6.3.2 B. Braun SE

- 6.3.3 Terumo Corporation

- 6.3.4 Nipro Corporation

- 6.3.5 Gerresheimer AG

- 6.3.6 Baxter International Inc.

- 6.3.7 Cardinal Health

- 6.3.8 Schott AG

- 6.3.9 Hindustan Syringes & Medical Devices Ltd.

- 6.3.10 Retractable Technologies Inc.

- 6.3.11 Fresenius Kabi AG

- 6.3.12 Sol-Millennium Medical

- 6.3.13 APEX MEDICAL DEVICES

- 6.3.14 Medtronic (Covidien)

- 6.3.15 Stevanato Group

- 6.3.16 Embecta Corp.

- 6.3.17 Revital Healthcare

- 6.3.18 Zhejiang Kindly Medical Devices

- 6.3.19 Ypsomed Holding AG

- 6.3.20 Jiangsu Delfu medical

- 6.3.21 Zhejiang Jianfeng Medical

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment