|

시장보고서

상품코드

1842533

내시경 재처리 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Endoscope Reprocessing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

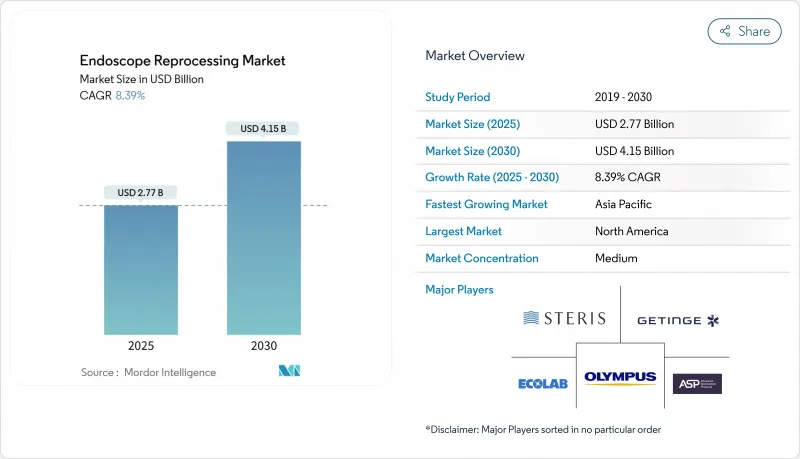

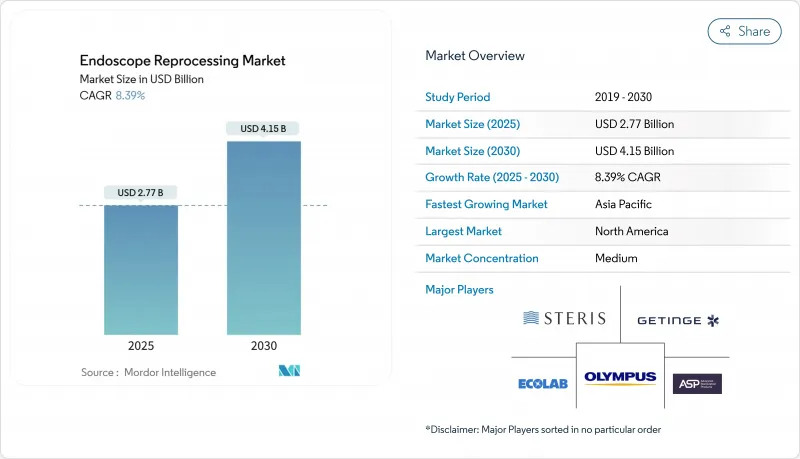

내시경 재처리 시장은 2025년에 27억 7,000만 달러에 이를 전망이며, 2025-2030년의 CAGR을 8.39% 반영하여 2030년에는 41억 5,000만 달러에 이를 것으로 예측되고 있습니다.

이러한 확장은 재사용 가능한 범위 내에서의 엄격한 세척, 소독 및 멸균을 통해 의료 관련 감염을 억제하는 데 내시경 재처리 시장이 중심적인 역할을 하고 있음을 뒷받침하고 있습니다. 특히 소화기(GI) 및 호흡기(Pulmonology) 치료에서 수술이 크게 증가함에 따라 소모품, 자동 재처리기 및 건조 캐비닛에 대한 수요가 증가하고 있습니다. 병원과 외래수술센터(ASC)는 AAMI와 ASGE의 가이던스 갱신에 따라 고수준 소독에서 멸균으로 업그레이드를 진행하고 있습니다. 동시에 단일 사용 부문은 재처리가 복잡한 지역에서 인기를 얻고 있습니다. 공급업체는 사이클 시간을 단축하는 액체 화학 멸균 시스템과 세척 워크플로우의 각 단계를 기록하는 디지털 추적 플랫폼을 제공합니다. 자본 구매는 북미와 서유럽에서 가장 두드러진 반면, 아시아태평양의 신흥 시장은 대량 생산에서 비용효율적인 솔루션에 중점을 두고 있습니다.

세계의 내시경 재처리 시장의 동향과 인사이트

내시경 검사 증가 : 인구 역학의 고령화가 수요를 뒷받침

노인 인구의 확대와 암 검진 가이드라인 강화가 소화기계 및 호흡기 스코프 사용에서 두 자릿수의 증가를 촉진하여 내시경 재처리 시장에 지속적인 성장을 가져오고 있습니다. 2024년 메타분석에 의하면 미국에서만 연간 2,000만건 이상의 소화기 검사가 진행되고 있습니다. 처리량이 증가함에 따라 시설은 재처리 능력 향상, 신속한 턴어라운드가 가능한 세척제, 모든 사이클에서 무균성을 유지하는 누출 검사 도구에 대한 투자에 집중합니다.

저침습 수술 : 스코프 회전율이 재처리 혁신을 촉진

외래수술센터(ASC)는 수익성을 유지하기 위해 타이트한 일정과 빠른 스코프 회전율에 의존합니다. LEAN 워크플로우의 시험적 도입으로 대기실에서의 대기 시간이 48.8% 단축되고, 총 시설 시간이 12% 단축되었습니다. 이러한 이점은 내시경 재처리 시장이 감염 제어 프로토콜을 손상시키지 않고 병목 현상을 줄이는 완전 자동 세척기, 건조 캐비닛, 실시간 추적 소프트웨어를 점점 선호하는 이유를 부각시키고 있습니다.

노동력 과제 : 기술자 부족이 도입을 막는다.

효과적인 세척을 위해서는 스코프 아키텍처와 채널 브러싱 기술에 대한 전문 지식이 필요합니다. 그러나 많은 병원이 자격을 가진 직원을 확보하고 유지하는 데 어려움을 겪고 있으며 실수가 발생하기 쉬운 절차가 심각한 오염 사건으로 이어졌습니다. 자동화에 의해 수작업이 경감되는 부분도 있지만 내시경의 재처리 시장 전체에 있어서 유자격자는 검사, 문제 해결, 품질 보증에 필수적인 존재인 것은 변함은 없습니다.

부문 분석

2024년 내시경 재처리 시장의 점유율은 고수준 소독제와 인디케이터 스트립이 32.26%를 차지했습니다. 헹굼 공정이 필요없는 새로운 효소 세척제는 대략 25L의 물을 절약하고 수작업 세척 시간을 15% 단축합니다. 그러나 바이오필름의 잔존과 관련된 집단감염으로 인해 감염관리위원회는 기화 과산화수소나 과아세트산 등의 멸균제에 주목하고 있습니다. 이 시프트는 인증 감사가 강화됨에 따라 중요한 성능 기준 중 하나인 운영자의 조정 없이 유효한 사이클을 완료하는 통합형 워셔 멸균기에 대한 수요를 높이고 있습니다.

자동 내시경 재처리기는 CAGR 10.82%로 가장 급성장하는 제품 그룹으로 내시경 재처리 시장 전체를 견인하고 있습니다. 공급업체는 모든 범위의 일련 번호, 사이클 파라미터, 누출 테스트 결과를 기록하는 폐쇄 루프 문서화, RFID 태그, 클라우드 기반 분석을 강조합니다. WASSENBURG DRY 320과 같은 시스템은 HEPA 필터에 의한 기류 하에서 30일 동안 미생물학적 품질을 유지합니다. 이러한 제품을 통해 시설은 컴플라이언스를 입증하고 비용이 많이 드는 재처리 실패를 줄일 수 있습니다.

연성 내시경은 2024년 매출의 71.83%를 차지하였며 현재 내시경 재처리 시장 규모를 모달리티 수준에서 지원하고 있습니다. 유연한 내시경은 도달 범위와 연결성으로 인해 소화기, 호흡기, 이비인후과 및 비뇨기과의 실험실에 필수적인 기구입니다. 그러나 그 복잡성 때문에 채널 파편의 영향을 받기 쉽습니다. 따라서 구조화된 보어 스코프 검사 및 형광 마커가 세척 효과를 확인하기 위해 채택되었습니다.

로봇 지원 내시경은 2030년까지 매년 11.65% 증가하고 내시경 재처리 시장에 새로운 기회를 가져올 것으로 예측됩니다. 양팔 로봇 대장 내시경과 다장기 수술 로봇은 인체 공학과 자율성 향상을 보장합니다. 이러한 채용에는 전용 세척기 랙, 프로토콜 변경, 직원 재교육이 필요합니다. 경성 스코프는 관절경 검사와 복강경 검사로 안정적인 틈새를 유지하며 증기 오토클레이브로 확실히 멸균할 수 있는 간단한 루멘의 혜택을 받고 있습니다.

지역 분석

북미는 2024년 매출의 40.85%를 차지하였으며 높은 수술 건수와 FDA, CDC, 인정기관에 의한 엄격한 감시에 의해 뒷받침되고 있습니다. 주요 시설에서의 감염 아웃 브레이크가 주목되어 추적 가능하고 자동화된 워크플로우와 십이지장 내시경을 35분 이내에 멸균할 수 있는 기화식 과산화수소 캐비닛에 대한 수요가 높아지고 있습니다. 2030년까지의 지역별 성장률은 CAGR 8.02%로 예측되고 있으며, 데이터가 풍부한 재처리기, 보어 스코프 검사용 카메라, 리스크가 높은 ERCP 사례용 일회용 십이지장 내시경에 지출이 기울고 있습니다.

아시아태평양은 가장 빠르게 성장하고 있으며 연간 10.76%의 성장이 예상됩니다. 인도의 의료기기 로드맵은 2030년까지 500억 달러의 생산을 목표로 하고 있으며, 내시경 시스템과 보조 재처리 장비는 생산 장려금 대상입니다. 중국, 일본, 한국은 음압 건조 캐비닛과 채널별 누설 테스터에 자본을 배분하는 한편, 자원이 부족한 태평양 제도는 정제수와 인정 기술자의 부족에 직면하고 있습니다.

유럽은 내시경 재처리 시장의 약 30%를 차지하며 2030년까지 연평균 복합 성장률(CAGR) 예측은 8.25%로 예상됩니다. EU 감시에서는 매년 350만 건 이상의 건강관리 관련 감염이 재사용 가능한 장비로 인해 발생합니다. 2024년에 체결된 250,000파운드 이상의 NHS 계약은 오염 제거 장비의 검증과 스코프 추적성 확보를 목표로 하는 병원의 움직임을 반영합니다. 중동 및 아프리카와 남미는 3차 의료시설이 CSSD 유닛을 현대화하고 화학물질 교환을 반복하지 않고 혼합 스코프 재고를 처리할 수 있는 AER를 채택함에 따라 완만한 성장을 이어가고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 도입

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 소화기 질환이나 암에 의한 내시경 수술 증가

- 저침습 수술의 도입과 일일 스코프 회전율 수요 증가

- 유효한 재처리 사이클을 의무화하는 감염 관리 및 인정 기준의 엄격화

- 소요시간과 에러를 줄이는 자동재처리장치의 진보

- 호환 가능한 소독제를 사용한 일회용 내시경 액세서리에 대한 수요 증가

- 외래수술센터(ASC)에서의 내시경 처치의 채용 확대

- 시장 성장 억제요인

- 자격을 가진 내시경 재처리 기술자의 부족과 높은 이직률

- 자동 재처리 시스템과 건조 캐비닛의 높은 초기 비용과 라이프사이클 비용

- 복잡한 십이지장 내시경의 잔류 오염에 의한 안전성에 대한 우려

- 빈번한 감사와 문서화에 의한 소모품 비용 증가와 워크플로우 혼란

- 공급망 분석

- 규제 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 제품별

- 고수준 소독제 & 테스트 스트립

- 세정제 및 효소 와이프

- 자동 내시경 재처리기(AER)

- 싱글 베이신

- 듀얼 베이신

- 수동 세척 스테이션

- 내시경 건조, 보관, 운송 캐비닛

- 기타

- 내시경 모달리티별

- 연성 내시경

- 경성 내시경

- 로봇 지원 내시경

- 용도별

- 소화기 내시경

- 호흡기 및 기관지 내시경

- 비뇨기과&부인과

- 이비인후과 및 복강경

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Advanced Sterilization Products Services Inc

- ARC Group of Companies Inc.

- Belimed AG

- BES Healthcare Ltd

- Creo Medical GmbH

- Ecolab Inc.

- Envista Holdings(Metrex Research)

- Getinge AB

- HOYA Corporation(Pentax Medical)

- Matachana Group

- Olympus Corporation

- Shinva Medical Instrument Co.

- Steelco SpA

- STERIS plc

- UV Smart BV

- Wassenburg Medical BV

제7장 시장 기회와 전망

CSM 25.11.03The endoscope reprocessing market was valued at USD 2.77 billion in 2025 and is forecast to reach USD 4.15 billion by 2030, reflecting an 8.39% CAGR over 2025-2030.

This expansion underscores the central role of the endoscope reprocessing market in curbing healthcare-associated infections through rigorous cleaning, disinfection, and sterilization of reusable scopes. Strong procedure growth, particularly in gastrointestinal (GI) and pulmonology suites, keeps demand elevated for consumables, automated reprocessors, and drying cabinets. Hospitals and ambulatory surgery centers (ASCs) are upgrading from high-level disinfection to sterilization following updated AAMI and ASGE guidance. At the same time, single-use scopes gain traction where reprocessing complexity remains high. Vendors respond with liquid chemical sterilization systems that shorten cycle times and with digitally enabled traceability platforms that log every stage of the cleaning workflow. Capital purchases are most pronounced in North America and Western Europe, whereas emerging Asia Pacific markets focus on high-volume, cost-efficient solutions.

Global Endoscope Reprocessing Market Trends and Insights

Rising Endoscopy Procedures: Aging Demographics Fuel Demand

An expanding elderly population and broader cancer-screening guidelines are driving double-digit increases in GI and respiratory scope use, giving the endoscope reprocessing market sustained tailwinds. More than 20 million GI examinations are performed annually in the United States alone, according to a 2024 meta-analysis. Higher procedural throughput obliges facilities to invest in additional reprocessing capacity, rapid turnaround detergents and leak-testing tools that uphold sterility for every cycle.

Minimally Invasive Surgery: Scope Turnover Drives Reprocessing Innovation

Ambulatory surgery centers rely on tight scheduling and quick scope turnaround to remain profitable. A LEAN workflow pilot cut waiting-room time by 48.8% and reduced total facility time by 12%. These gains highlight why the endoscope reprocessing market increasingly favors fully automated washers, drying cabinets and real-time tracking software that shorten bottlenecks without compromising infection-control protocols.

Workforce Challenges: Technician Shortages Impede Implementation

Effective cleaning demands specialized knowledge of scope architecture and channel brushing techniques. Yet many hospitals struggle to recruit and retain certified staff, with error-prone steps contributing to notable contamination events. Although automation offsets some manual tasks, qualified personnel remain indispensable for inspection, trouble-shooting and quality assurance across the endoscope reprocessing market.

Other drivers and restraints analyzed in the detailed report include:

- Infection-Control Standards: Regulatory Pressure Transforms Practices

- Automated Reprocessing: Technology Reduces Human Error

- Cost Barriers: Financial Constraints Limit Technology Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-level disinfectants and indicator strips hold a 32.26% endoscope reprocessing market share in 2024, reflecting the historical reliance on chemical HLD for flexible scopes. Novel enzymatic detergents that eliminate rinse steps now save nearly 25 L of water and cut manual cleaning time by 15%. Yet outbreaks linked to residual biofilm are steering infection-control committees toward sterilants such as vaporized hydrogen peroxide and peracetic acid. This shift boosts demand for integrated washer-sterilizers that complete validated cycles without operator adjustment, a key performance criterion as accreditation audits intensify.

Automated endoscope reprocessors are the fastest-growing product group at a 10.82% CAGR, propelling the overall endoscope reprocessing market. Vendors emphasize closed-loop documentation, RFID tagging and cloud-based analytics that record every scope serial number, cycle parameters and leak-test result. Drying and storage cabinets also gain prominence; systems such as WASSENBURG DRY 320 preserve microbiological quality for 30 days under HEPA-filtered airflow. Together, these products help facilities demonstrate compliance and reduce costly re-processing failures.

Flexible endoscopes commanded 71.83% of 2024 revenue, underpinning the current endoscope reprocessing market size at the modality level. Owing to their reach and articulation, they remain indispensable across GI, respiratory, ENT, and urology suites. However, their complexity makes them vulnerable to channel debris. Structured borescope inspections and fluorescence markers are thus being adopted to affirm cleaning efficacy.

Robot-assisted endoscopes are projected to rise 11.65% annually through 2030, carving new opportunities in the endoscope reprocessing market. Two-armed robotic colonoscopes and multi-visceral surgical robots promise enhanced ergonomics and autonomy. Their adoption will demand dedicated washer racks, protocol modifications, and staff retraining. Rigid scopes retain a stable niche for arthroscopy and laparoscopy, benefiting from simpler lumens that sterilize reliably in steam autoclaves.

The Endoscope Reprocessing Market Report is Segmented by Product (High-Level Disinfectants and Test Strips, Detergents and Enzymatic Wipes, AER [Single-Basin and Dual-Basin], and More), Endoscope Modality (Flexible Endoscopes and More), Application (Gastrointestinal Endoscopy and More), End-User (Hospitals and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 40.85% of 2024 revenue, supported by high procedural volumes and rigorous oversight from the FDA, CDC and accreditation bodies. A spotlight on infection outbreaks at leading centers has intensified demand for traceable, automated workflows and for vaporized hydrogen peroxide cabinets capable of sterilizing duodenoscopes within 35 minutes. Regional growth is projected at an 8.02% CAGR through 2030, with spending tilted toward data-rich reprocessors, borescope inspection cameras, and disposable duodenoscopes for high-risk ERCP cases.

Asia-Pacific is the fastest-expanding territory, anticipated to advance 10.76% annually. India's medical-device roadmap seeks USD 50 billion in sector output by 2030, with endoscopy systems and ancillary reprocessing devices eligible for production incentives. China, Japan, and South Korea allocate capital to negative-pressure drying cabinets and channel-specific leak testers, while resource-limited Pacific Islands confront shortages of purified water and certified technicians.

Europe commands roughly 30% of the endoscope reprocessing market, posting an 8.25% CAGR projection to 2030. EU surveillance attributes more than 3.5 million healthcare-associated infections to reusable devices each year. NHS contracts exceeding GBP 250,000 awarded in 2024 reflect hospital moves to validate decontamination equipment and ensure scope-level traceability. The Middle East & Africa and South America follow with moderate growth as tertiary centers modernize CSSD units and adopt AERs capable of handling mixed scope inventories without repeated chemical changes.

- Advanced Sterilization Products Services Inc

- ARC Group of Companies Inc.

- Belimed

- BES Healthcare Ltd

- Creo Medical GmbH

- Ecolab

- Envista Holdings (Metrex Research)

- Getinge

- HOYA Corporation (Pentax Medical)

- Matachana Group

- Olympus

- Shinva Medical Instrument Co.

- Steelco

- STERIS

- UV Smart BV

- Wassenburg Medical B.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising endoscopy procedures due to gastrointestinal disorders and cancers

- 4.2.2 Increasing adoption of minimally invasive surgeries and daily scope turnover demands

- 4.2.3 Tightening infection-control and accreditation standards mandating validated reprocessing cycles

- 4.2.4 Advances in automated reprocessors that cut turnaround time and errors

- 4.2.5 Growing demand for single-use endoscopic accessories with compatible disinfectants

- 4.2.6 Expanding outpatient and ambulatory surgery center adoption of endoscopic procedures

- 4.3 Market Restraints

- 4.3.1 Shortage of certified endoscope reprocessing technicians and high turnover rates

- 4.3.2 High upfront and lifecycle costs for automated reprocessing systems and drying cabinets

- 4.3.3 Safety concerns with residual contamination in complex duodenoscopes

- 4.3.4 Frequent audits and documentation cause high consumable costs and workflow disruptions

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 High-Level Disinfectants & Test Strips

- 5.1.2 Detergents & Enzymatic Wipes

- 5.1.3 Automated Endoscope Reprocessors (AER)

- 5.1.3.1 Single-basin

- 5.1.3.2 Dual-basin

- 5.1.4 Manual Cleaning Stations

- 5.1.5 Endoscope Drying, Storage & Transport Cabinets

- 5.1.6 Others

- 5.2 By Endoscope Modality

- 5.2.1 Flexible Endoscopes

- 5.2.2 Rigid Endoscopes

- 5.2.3 Robot-Assisted Endoscopes

- 5.3 By Application

- 5.3.1 Gastro-intestinal Endoscopy

- 5.3.2 Pulmonology & Bronchoscopy

- 5.3.3 Urology & Gynaecology

- 5.3.4 ENT & Laparoscopy

- 5.4 By End-User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgery Centres (ASC)

- 5.4.3 Other End-Users

- 5.5 By Geography (Value)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Product Portfolio Analysis

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Advanced Sterilization Products Services Inc

- 6.4.2 ARC Group of Companies Inc.

- 6.4.3 Belimed AG

- 6.4.4 BES Healthcare Ltd

- 6.4.5 Creo Medical GmbH

- 6.4.6 Ecolab Inc.

- 6.4.7 Envista Holdings (Metrex Research)

- 6.4.8 Getinge AB

- 6.4.9 HOYA Corporation (Pentax Medical)

- 6.4.10 Matachana Group

- 6.4.11 Olympus Corporation

- 6.4.12 Shinva Medical Instrument Co.

- 6.4.13 Steelco S.p.A.

- 6.4.14 STERIS plc

- 6.4.15 UV Smart BV

- 6.4.16 Wassenburg Medical B.V.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment