|

시장보고서

상품코드

1842536

정전기 방지제 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Anti-static Agents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

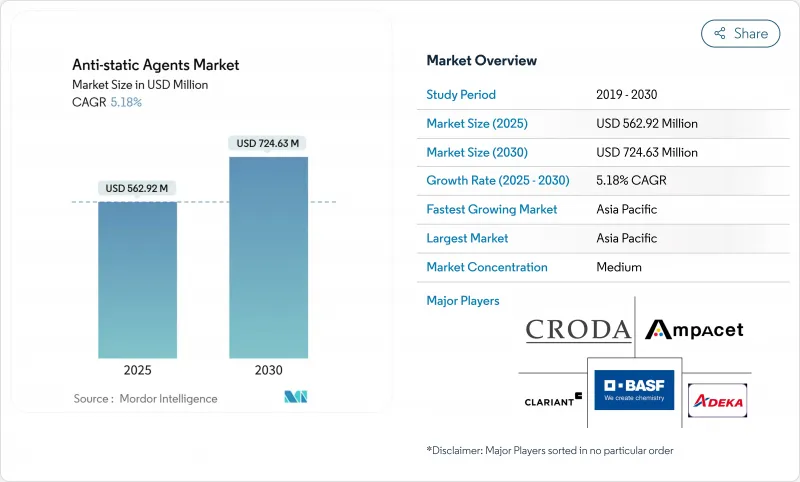

정전기 방지제 시장 규모는 2025년에 5억 6,292만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 5.18%로 성장할 전망이며, 2030년에는 7억 2,463만 달러에 이를 것으로 예측됩니다.

전자기기의 소형화가 급속히 진행되고, 반도체 공장 및 가전제품 라인 전체의 정전기 방전(ESD) 감도가 높아지고 있기 때문에 영구 첨가제와 이행성 첨가제 모두 수요가 높아지고 있습니다. PFAS 및 VOC 규제에 대응하기 위해 브랜드와 가공업자가 솔벤트 시스템에서 전환함에 따라 수성 마스터 배치 플랫폼의 점유율이 확대되고 있습니다. 아시아태평양의 수탁 제조 강도가 세계적인 생산량을 지원하는 반면, 바이오 화학과 실리카 리치 블렌드는 경쟁 포지셔닝을 재구성하고 있습니다. 자동차의 전동화, 전자상거래 패키징, 선진 의료기기 등 정전기 방지제 시장이 고온, 클린룸 대응, PFAS 프리 솔루션으로 향하는 다년의 성장 회랑을 만들어 내고 있습니다.

세계의 정전기 방지제 시장 동향 및 인사이트

전자상거래에 의한 정전기 방지 포장 수요 급증

소비자용 전자기기의 월경 전자상거래 출하는 점포 배송을 능가하고 소포 취급업자는 저밀도 폴리에틸렌(LDPE) 필름이나 기포 백의 엄격한 표면 저항률 제한을 충족해야 합니다. 대규모 물류센터에서는 고속소터가 도입되고 있어 그 마찰은 종종 100m/분을 넘어 마이크로컨트롤러를 마비시키는 정전기의 축적을 악화시킵니다. 따라서 패키징 컨버터는 RoHS 지침 및 식품 접촉 규제를 준수하는 영구 정전기 방지 마스터 배치를 통합하여 첨가제의 첨가량을 3phr 미만으로 억제하여 투명성과 씰 무결성을 유지합니다. 중국의 온라인 소매 점유율은 이미 국내 매출의 50%를 넘고 있으며, 현지 가방 제조업체는 습도에 의존하지 않는 정전기 방지 등급 인증을 추진하고 있습니다. 각 브랜드는 동시에 재활용 가능한 단일 소재 필름을 추구하고 있으며 기계적 재활용의 흐름을 방해하지 않는 아민 기반 화학 물질이 필요합니다.

ESD 감도를 높이는 전자기기의 소형화

3nm 이하의 FinFET 및 게이트 올 어라운드 노드는 14nm 디바이스가 허용하는 피크 전류의 25%만을 견딜 수 있기 때문에 공장에서는 현재 캐리어 트레이와 웨이퍼 박스의 실내 공기 저항률을 10^10Ω 미만으로 지정하고 있습니다. 첨단 시스템 인 패키지 어셈블리는 초박형 인터 포저를 통해 전력을 라우팅하고 방전 중 국부적인 열을 증폭하며 230°C의 리플로우를 견딜 수 있는 영구적인 정전기 방지 코팅이 필요합니다. imec과 같은 조사 컨소시엄은 박형 실리콘에서 고장 전류가 20-40% 저하되는 것을 기록하고 첨가제 공급자를 습도 의존성을 회피하는 실리카 그래프트 폴리에테르아미드로 유도하고 있습니다. 따라서 정전기 방지제 시장은 클린룸용 폴리머의 온도 안정성, 마이그레이션 프리 그레이드에 연구 개발을 집중시키고 있습니다.

타로 유래 원료의 불안정성

바이오디젤 의무화의 급증으로 우지의 경쟁이 격화하고 가격이 상승하여 유지화학 정전기 방지 중간체 공급이 핍박하고 있습니다. EU 정유소에서는 동식물 지방을 가수처리한 식물성 기름 디젤에 돌려보내는 움직임이 강해져 화학물질의 입수가 어려워지기 때문에 배합업자는 팜 지방산 유분을 사용한 헤지를 강요하고 있습니다. 렌더링업체는 생산능력을 뛰어넘어 운영하고 있으며, 콜드체인 로지스틱스는 석유화학 아민에 대한 비용 우위성을 침식하는 운임 프리미엄을 올리고 있습니다. 식품 접촉 정전기 방지제를 사용하는 패키징 기업은 일부 소매업체가 동물 유래 원료를 제한하기 때문에 추가 제약에 직면하고 있습니다. 따라서 생산자는 수지의 성능을 모방한 유채나 사용후 식용유를 베이스로 하는 에스테르의 시험을 강화하고 있습니다.

부문 분석

지방산 아민은 LDPE와 PP 필름에서 입증된 효능을 활용해 2024년 39.04%의 매출을 획득했습니다. 에톡실화 아밍레이드는 계기판에 사용되는 유리 섬유 강화 폴리프로필렌에 적합한 250℃까지의 열안정성으로 CAGR 최고 속도의 7.05%를 기록했습니다. 모노글리세리드는 FDA(미국 식품의약국)의 규제를 받는 식품 포장 용도의 정평이지만, 함유량이 0.5phr까지이기 때문에 성장은 완만합니다. 폴리글리세롤 에스테르는 생체적합성이 가격 프리미엄을 상쇄하는 의료기기용 파우치에 사용됩니다. 새롭게 등장한 4급 폴리에톡실화 구조는 하이드록실 관능기를 부가해, 고유동 PP중에서의 분산성을 향상시켜, 블룸을 감소시킴으로써, 고성능차에 있어서 정전기 방지제 시장의 궤도를 더욱 견고한 것으로 하고 있습니다.

이 하위 부문의 상승은 폴리프로필렌 내장 부품의 정전기 방지제 시장 규모에 영향을 주고 2025-2030년 CAGR 6.8%로 확대될 전망입니다. 폴리에테르 비스페놀 A 공중합체와 같은 영구 첨가제는 단가가 높지만 자동차의 전체 수명에 걸쳐 대시보드를 먼지로부터 보호하기 위해 OEM의 흡수를 촉진하고 에톡실화 시스템의 정전기 방지제 시장 점유율을 끌어올리고 있습니다.

석유화학 원료는 2024년 수요의 79.81%를 공급했으며, 이는 통합 크래커의 경제성을 반영합니다. 그러나 지속가능성 목표는 생산 능력을 유채, 야자 및 사용된 식용유의 경로로 유도하며, CAGR은 현재 7.51%로 성장을 지속하고 있습니다. 유럽에서는 물질 수지 인증 및 탄소 크레딧 거래와 같은 규제의 혜택으로 가격 차이가 12% 이하로 줄어들고 있습니다. 크로다의 생분해성 크로다스탯 400은 CO2 배출량을 60% 줄이면서 바이오 시스템이 전도성과 비교할 수 있음을 입증합니다.

타로의 변동성과 동물성 유도체에 대한 소비자 감정은 2028년까지 식물성 오일에스테르가 일렉트로닉스 출하용 필름의 디폴트가 되도록 축족을 증폭시킵니다. 이러한 변화로 인해 바이오 정전기 방지제 시장 규모는 2030년까지 2억 달러를 초과할 수 있지만 경쟁력은 아시아 바이오 정제 공장의 추가 규모 증가에 달려 있습니다.

지역 분석

아시아태평양은 2024년 세계 매출의 43.08%를 차지했으며, 2030년까지 연평균 복합 성장률(CAGR) 6.98%로 성장할 전망입니다. 중국 본토의 웨이퍼 팹 확대와 인도 Tier-1 자동차 부품의 급성장은 영구 정전기 방지 화학물질에 대한 밀도가 높은 수요 회랑을 형성합니다. 지역 포뮬레이터는 대용량 2축 스크류 라인에 투자합니다. : 산요 가세이의 연산 1,500톤의 태국 공장은 공급 측 스케일 업의 일례입니다. 생분해성 플라스틱에 대한 정부의 우대 조치는 바이오 원료의 채택을 더욱 촉진하고 ASEAN 패키징에서 정전기 방지제 시장 규모를 밀어 올릴 수 있습니다.

북미는 첨단 반도체 패키징과 전동화 자동차 플랫폼을 타고 있습니다. 미국 조인트(US-JOINT)와 같은 컨소시엄 프로그램은 ESD 안전재료의 연구개발에 연방정부의 보조금을 투입하여 이익률이 높은 마스터배치 공급업체를 지원하고 있습니다. 기업의 지속가능성 목표(포춘 500에 랭크되는 대부분의 전자기기 OEM이 2030년까지 탄소 중립을 달성할 것을 공약)는 PFAS 프리화를 가속화하고 수계 제품에 의해 정전기 방지제 시장 전망을 재구축하고 있습니다.

유럽의 엄격한 REACH 업데이트와 대륙 전반에 걸친 PFAS의 단계적 폐지는 실리카 기반 및 바이오 솔루션으로 신속한 전환을 촉진합니다. 클라리언트가 2023년에 PFAS를 완전히 폐지하는 것은 조기 컴플라이언스 준수를 나타냅니다. 주요 자동차 제조업체를 보유한 독일과 프랑스는 VOC 프리 몰딩 컬러 인테리어를 지지하고 내열 영구 정전기 방지제 수요를 끌어올리고 있습니다. 중동, 아프리카, 남미는 전자상거래의 보급과 자동차 조립 증가에 따라 가격에 여전히 민감하지만, 1 자리수의 높은 수량 성장을 기록하고 비용 최적화 이행 등급의 새로운 격전구가 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 전자상거래에 의한 정전기 대책 패키지 수요 급증

- 전자 기기의 소형화에 의한 ESD 감도 증가

- 용제계 마스터 배치로부터 수계 마스터 배치로의 이행

- 자동차 산업에서의 수요 증가

- 헬스케어 및 의료기기 산업의 확대

- 시장 성장 억제요인

- 수지 유래의 원료의 불안정성

- 자본 집약적인 영구 이온 전도성 첨가제

- 고유 소산성 폴리머의 채용 증가

- 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측

- 유형별

- 모노글리세리드

- 폴리글리세린 에스테르

- 디에탄올아미드

- 에톡시화 지방산 아민

- 원료별

- 바이오 베이스(식물 유래, 타로 유래)

- 석유화학 베이스

- 폴리머별

- 폴리프로필렌

- 폴리에틸렌

- 폴리염화비닐

- 기타 폴리머(폴리스티렌 등)

- 최종 사용자 산업별

- 포장

- 일렉트로닉스

- 자동차 및 운송

- 기타(의료 및 헬스케어 등)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율(%) 및 랭킹 분석

- 기업 프로파일

- 3M

- Adeka Corporation

- Ampacet Corporation

- Arkema

- Avient Corporation

- BASF

- Clariant

- Croda International plc

- Emery Oleochemicals

- Evonik Industries AG

- Italmatch Chemicals

- Kao Corporation

- Mitsubishi Chemical Group Corporation

- Palsgaard

- Sanyo Chemical Industries

- Solvay

- Tosaf

제7장 시장 기회 및 전망

AJY 25.10.29The Anti-static Agents Market size is estimated at USD 562.92 million in 2025, and is expected to reach USD 724.63 million by 2030, at a CAGR of 5.18% during the forecast period (2025-2030).

A sharp rise in electronics miniaturization is magnifying electrostatic-discharge (ESD) sensitivity across semiconductor fabs and consumer electronics lines, reinforcing demand for both permanent and migratory additives. Water-borne masterbatch platforms are gaining share as brands and processors pivot away from solvent systems in response to PFAS and VOC regulations. Asia-Pacific's contract manufacturing strength anchors global volume, while bio-based chemistry and silica-rich blends reshape competitive positioning. Automotive electrification, e-commerce packaging, and advanced health-care devices together create multi-year growth corridors that the antistatic agent market is gearing toward with higher-temperature, clean-room-ready, PFAS-free solutions.

Global Anti-static Agents Market Trends and Insights

Surge In E-Commerce-Led Demand For Antistatic Packaging

Cross-border e-commerce shipments of consumer electronics outpace store deliveries, obliging parcel handlers to meet tighter surface-resistivity limits in low-density polyethylene (LDPE) films and bubble bags. Large logistics centers deploy high-speed sorters whose friction often exceeds 100 m/min, exacerbating static buildup that can cripple micro-controllers. Packaging converters therefore integrate permanent antistatic masterbatches that comply with RoHS and food-contact codes, keeping additive loading below 3 phr to preserve clarity and seal integrity. China's online retail share, already above 50% of national sales, pushes local bag makers to qualify humidity-independent antistatic grades. Brands simultaneously pursue recyclable mono-material films, requiring amine-based chemistries that do not hinder mechanical-recycling streams.

Miniaturization Of Electronics Heightening ESD Sensitivity

FinFET and gate-all-around nodes below 3 nm withstand only 25% of the peak current tolerated by 14 nm devices, so fabs now specify room-air resistivity under 10^10 Ω for carrier trays and wafer boxes. Advanced system-in-package assemblies route power through ultrathin interposers, amplifying local heat during a discharge and demanding permanent antistatic coatings rated for 230 °C reflow. Research consortia such as imec document failure-current declines of 20-40% on thinned silicon, guiding additive suppliers toward silica-grafted polyether amides that avoid humidity dependence. The antistatic agent market, therefore, concentrates R&D on temperature-stable, migration-free grades for clean-room polymers.

Volatility In Tallow-Derived Feedstocks

Surging biodiesel mandates elevate competition for beef-tallow, inflating prices and tightening supply for oleochemical antistatic intermediates. EU refineries channel more animal fat toward hydro-treated vegetable-oil diesel, hindering chemical availability and forcing formulators to hedge with palm-fatty-acid distillate routes. Renderers operate near capacity, and cold-chain logistics add freight premiums that erode cost advantages over petrochemical amines. Packaging firms using food-contact antistatic agents face further constraints as certain retailers restrict animal-derived ingredients. Producers consequently intensify trials of rapeseed- and used-cooking-oil-based esters that mimic tallow performance.

Other drivers and restraints analyzed in the detailed report include:

- Transition From Solvent-Borne To Water-Borne Masterbatches

- Growing Demand From The Automotive Industry

- Capital-Intensive Permanent Ionic-Conductive Additives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fatty-acid amines captured 39.04% revenue in 2024, leveraging proven efficacy in LDPE and PP films. Ethoxylated amine grades now post the fastest 7.05% CAGR, propelled by thermal stability up to 250 °C that suits glass-fiber-reinforced polypropylene used in instrument panels. Monoglycerides remain staples in FDA-regulated food-packaging applications, though growth is muted because inclusion levels cap at 0.5 phr. Polyglycerol esters serve medical-device pouches where biocompatibility offsets price premiums. Emerging quaternary polyethoxylated structures add hydroxyl functionality, improving dispersion in high-flow PP and reducing bloom, further cementing the antistatic agent market trajectory in performance vehicles.

The sub-segment's ascent influences the antistatic agent market size for polypropylene interior parts, which is slated to expand at 6.8% CAGR between 2025-2030. Permanent additives such as polyether-bisphenol A copolymers command higher unit pricing but shield dashboards from dust for the full vehicle life, encouraging OEM uptake and lifting the antistatic agent market share for ethoxylated systems.

Petrochemical feedstocks supplied 79.81% of 2024 demand, a reflection of integrated cracker economics. Yet sustainability goals are steering capacity toward rapeseed-, palm-, and used-cooking-oil pathways that now clock a 7.51% CAGR. Regulatory carrots such as mass-balance certification and carbon-credit trading in Europe reduce the price delta to below 12%. Croda's biodegradable Crodastat 400 demonstrates that bio-based systems can match conductivity while cutting CO2 footprint by 60%.

Tallow volatility and consumer sentiment against animal derivatives amplify the pivot, making vegetable-oil esters the default for electronics shipping films by 2028. This shift could push the bio-based antistatic agent market size past USD 200 million by 2030, though competitive parity hinges on further scale-up in Asian bio-refineries.

The Antistatic Agent Market Report Segments the Industry by Type (Monoglycerides, Diethanolamides, and More), Source (Bio-Based and Petrochemical-Based), Polymer (Polypropylene, Polyethylene, and More), End-User Industry (Packaging, Electronics, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific controlled 43.08% of global revenue in 2024 and advances at a 6.98% CAGR through 2030. Mainland China's wafer-fab expansion and India's tier-1 auto-components surge build dense demand corridors for permanent antistatic chemistries. Regional formulators invest in high-capacity twin-screw lines: Sanyo Chemical's 1,500 t/y Thai plant exemplifies supply-side scaling. Government incentives for biodegradable plastics further encourage bio-feedstock adoption, potentially bolstering the antistatic agent market size in ASEAN packaging.

North America rides advanced semiconductor packaging and electrified-vehicle platforms. Consortium programs such as US-JOINT funnel federal grants into ESD-safe materials R&D, which supports high-margin masterbatch suppliers. Corporate sustainability goals-most Fortune 500 electronics OEMs pledge carbon neutrality by 2030-accelerate PFAS-free conversions, reshaping the antistatic agent market landscape with water-borne offerings.

Europe's stringent REACH updates and the continent-wide PFAS phase-out catalyze rapid pivots to silica-based and bio-based solutions. Clariant's complete PFAS exit in 2023 exemplifies early compliance. Germany and France, housing leading auto makers, champion VOC-free molded-in-color interiors, lifting demand for heat-resistant, permanent antistatic agents. The Middle East, Africa, and South America remain price-sensitive but post high single-digit volume growth as e-commerce penetration and automotive assembly rise, making them emergent battlegrounds for cost-optimized migratory grades.

- 3M

- Adeka Corporation

- Ampacet Corporation

- Arkema

- Avient Corporation

- BASF

- Clariant

- Croda International plc

- Emery Oleochemicals

- Evonik Industries AG

- Italmatch Chemicals

- Kao Corporation

- Mitsubishi Chemical Group Corporation

- Palsgaard

- Sanyo Chemical Industries

- Solvay

- Tosaf

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in E-commerce-led demand for anti-static packaging

- 4.2.2 Miniaturisation of electronics heightening ESD sensitivity

- 4.2.3 Transition from solvent-borne to water-borne masterbatches

- 4.2.4 Growing demand from the automotive industry

- 4.2.5 Expansion in the healthcare and medical devices industry

- 4.3 Market Restraints

- 4.3.1 Volatility in tallow-derived feedstocks

- 4.3.2 Capital-intensive permanent ionic-conductive additives

- 4.3.3 Rising adoption of inherently dissipative polymers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Monoglycerides

- 5.1.2 Polyglygerol Esters

- 5.1.3 Diethanolamides

- 5.1.4 Ethoxylated Fatty Acid Amines

- 5.2 By Source

- 5.2.1 Bio-based (Vegetable-, Tallow-derived)

- 5.2.2 Petrochemical-based

- 5.3 By Polymer

- 5.3.1 Polypropylene

- 5.3.2 Polyethylene

- 5.3.3 Polyvinyl Chloride

- 5.3.4 Other Polymers(Polystyrene, etc.)

- 5.4 By End-User Industry

- 5.4.1 Packaging

- 5.4.2 Electronics

- 5.4.3 Automotive and Transportation

- 5.4.4 Other End-User Industries (Medical and Healthcare, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Adeka Corporation

- 6.4.3 Ampacet Corporation

- 6.4.4 Arkema

- 6.4.5 Avient Corporation

- 6.4.6 BASF

- 6.4.7 Clariant

- 6.4.8 Croda International plc

- 6.4.9 Emery Oleochemicals

- 6.4.10 Evonik Industries AG

- 6.4.11 Italmatch Chemicals

- 6.4.12 Kao Corporation

- 6.4.13 Mitsubishi Chemical Group Corporation

- 6.4.14 Palsgaard

- 6.4.15 Sanyo Chemical Industries

- 6.4.16 Solvay

- 6.4.17 Tosaf

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment