|

시장보고서

상품코드

1842549

탄저균 치료 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Anthrax Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

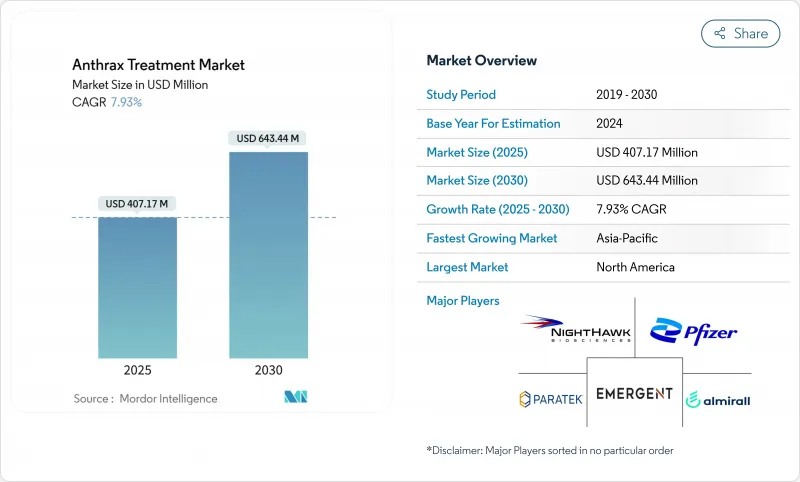

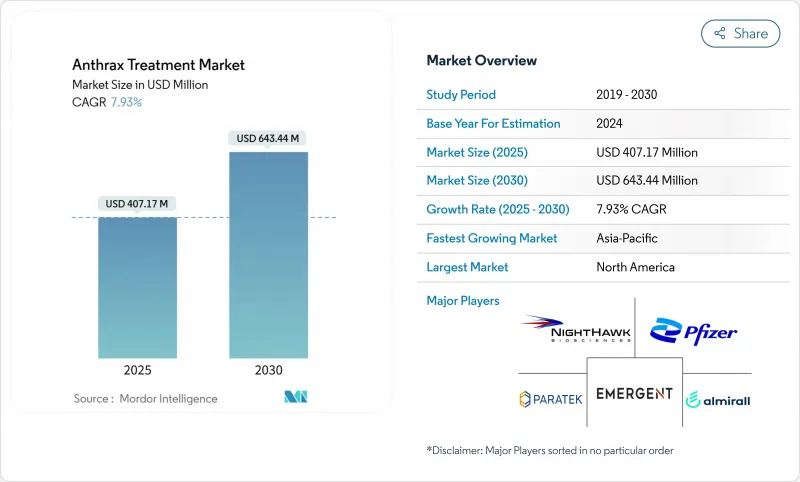

탄저균 치료 시장은 2025년에는 4억 717만 달러로 추정되고, 2030년에는 6억 4,344만 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR 7.93%로 성장이 전망됩니다.

이 기세는 정부의 생물 방위 예산 지속, 규제 당국의 규제 경로 가속화, 기존의 의약품이 아닌 의료 대책을 국가 자산으로 자리매김하는 안보 의식의 고조에 기인하고 있습니다. 2023-2027년 795억 달러의 자금 수요에 대한 언급과 유럽 및 아시아태평양의 유사한 이니셔티브가 장기적인 수요를 뒷받침하고 있습니다. 탄저균 치료 시장은 차세대 백신 승인, 성숙하고 있는 단일클론항체 플랫폼, AI를 활용한 약물 재이용 파이프라인을 통해 치료법을 다양화시키면서 탐색 기간을 단축할 수 있습니다. 상업적 수익성은 여전히 완만하지만, 예측 가능한 소블린 조달과 보충 사이클은 광범위한 민간 판매 채널의 부재를 상쇄하는 수익의 가시성을 계약자에게 제공합니다.

세계의 탄저균 치료 시장 동향 및 인사이트

정부의 생물 방위 자금 및 비축 프로그램

안정적이고 다년간의 공적 자금으로 인해 탄저균 치료 시장은 준정부 조달장으로 변하고 있습니다. BARDA에 의한 NUDYRA의 보충 계약과 67억 달러의 전략적 국가 비축 확대는 급격한 구매에서 라이프사이클 관리로의 전환을 보여주고 서지 능력을 유지할 수 있는 제조업체에게 보상하고 있습니다. NIH가 자금을 제공하는 에페트라보롤과 같은 신규 약물의 개발은 공적 자본이 초기 단계의 연구 개발을 맡아 회사를 상업적 수요 위험으로부터 격리하고 있음을 보여줍니다. 유럽연합(EU)과 호주에서 유사한 틀은 이 모델을 반영한 것으로, 제조업의 경제성을 안정시키는 세계적인 수요의 동기화를 창출하고 있습니다. 그 결과 예측 가능한 생산 파이프라인이 전문 시설과 강인한 공급망을 지원하고 탄저균 치료 시장의 장기 성장을 뒷받침하고 있습니다.

바이오테러의 위협 및 국가 안보에 대한 관심 증가

지정학적 긴장 증가는 생물 무기를 틈새 관심사에서 국방 우선 순위의 주류로 밀어 올리고 있습니다. 국방위협 감소국의 1,220만 달러의 위험 예측 프로그램과 NATO 통합 CBRN 준비 연습은 정부가 인텔리전스 평가를 실제 조달에 어떻게 연결시키는지를 보여줍니다. 안보 기구는 가혹한 환경에서도 안정적이고 전개 가능하며 효과적인 치료법을 요구하고 있으며 기존 병원의 틀을 넘어서는 제제 연구를 장려하고 있습니다. 이러한 전략적 요구는 군사 교리에 통합되어 있기 때문에 자금 조달은 불경기와 선거주기와는 무관합니다. 그 결과, 탄저균 치료 시장은 헬스케어의 재량 지출이 아니라 국가 안보에 연결되는 지속적인 수익 기반을 얻고 있습니다.

제한된 상업적 수익성이 민간 연구 개발을 방해

탄저균 치료의 수익은 지속적인 시장 진입보다 비축 보충 캘린더에 따른 대량 구매에 달려 있습니다. 2023년 4분기부터 2024년 4분기에 이르는 에머전트 바이오솔루션의 매출액 71% 변동은 계약의 타이밍이 순수한 생명공학 투자자들이 피할 수 있는 재무 변동을 어떻게 창출하는지를 명확하게 보여줍니다. 저분자 항생제의 경우 개발 비용은 1억 달러를 초과할 수 있지만, 접근 가능한 탄저균 치료 시장 규모는 정부 배분에 의해 제약을 받고 상승 리턴에 상한이 설정되어 있습니다. 이러한 구조적 역학은 적극적인 개발자의 밑단을 좁히고 파이프라인의 다양화를 늦추고 예측 기간 동안 공급망 집중 위험을 높입니다.

부문 분석

탄저균 치료 시장 규모는 노출 후 예방 및 치료 요법에서 항생제의 오랜 역할로 인해 2024년에 가장 커집니다. 비축 관리자는 비용 효율성으로 시프로플록사신 및 독시사이클린을 선호하지만, 효능 논쟁과 내성 동향이 포트폴리오의 다양화를 촉진하고 있습니다. 항독소 제형은 수익 기반이 작고 내성균에 의존하지 않는 독소 중화 능력으로 인해 가장 강력한 성장을 보여줍니다. Raxibacumab 및 Obiltoxaximab은 미국의 전략적 국가 비축 계획에 표준적으로 포함되어 있으며 Anthrasil은 단일 소스의 취약성을 완화시키는 혈장 유래의 다양성에 기여합니다. UPMC의 2025년 돌파구는 역사적인 'point of no return'을 넘어 치료 기간을 연장함으로써 임상 용도의 가능성을 넓히는 것을 약속하고 있습니다. 컴퓨터에 의한 리퍼포징은 부종 인자와 치사 인자의 저분자 억제제를 발견하고 탄저균 치료 시장을 추가로 재구성할 수 있는 미래의 보조 요법을 제시했습니다.

정부와의 계약에서는 항생제와 항독소를 함께 포장하는 것이 증가하고 있으며, 다단계 대응 프로토콜에서 각 클래스가 보완적인 역할을 하는 것이 인정되고 있습니다. 따라서 탄저균 치료 시장에서 항독소의 점유율은 순수한 임상 수요보다는 정책 전환의 혜택을 받고 있습니다. 백신은 군사 전개와 같은 노출 전 예방이 중심인 것으로 변함이 없지만, 한국에서 재조합 백신이 승인됨으로써 민간인 예방에도 적응이 퍼질 가능성이 있습니다. 응고 이상증과 전신성 염증을 다루는 보조 요법은 여전히 겸손한 매출이지만 중증 사례에서는 중요한 가치를 제공하고 탄저균 치료 시장을 정의하는 전반적인 치료 패러다임을 강화하고 있습니다.

특히, 치료까지의 시간이 결정적이 되는 중증의 흡입성 탄저에서는 전신 투여가 신속하게 가능한 주사제가 재고의 대부분을 차지하고 있습니다. 락시바쿠맙과 오비르톡사시맙은 여전히 정맥내 투여만으로, 이 기호를 지원합니다. 그럼에도 불구하고, 경구 항생제는 좁은 범위에서 대량 투여가 요구되는 노출 후 예방 캠페인에서 지지되고 있습니다. 전임상시험에서는 노출 후 24시간 이내에 투여를 개시했을 경우의 치료 효과가 확인되어 현장에서 정제의 물류면에서의 매력이 검증되고 있습니다. 업데이트된 CDC 가이드라인은 60일간의 예방 과정에 독시사이클린 또는 레보플록사신의 경구 투여를 권장하며, 진화하는 증거와 정책이 일치합니다.

캡슐 제형의 온도 안정성 시험은 백신의 내열성 조사와 마찬가지로 열대에서의 전개를 제한하는 콜드체인 의존성을 제거하는 것을 목표로 합니다. 낙하산과 무인 항공기에 의한 운송에 적합한 스트립 포장 항생제의 채택은 의약품 설계 및 방위 물류를 융합시키는 미래의 기술 혁신을 시사합니다. 현재 연구중인 흡입용 분말 제제를 포함한 다른 경로도 궁극적으로 현재의 선택을 보완할 수 있지만, 규제 당국이 경구제와 주사제의 경로에 익숙해지기 때문에 예측 기간 중에는 이 두 경로가 탄저균 치료 시장을 계속 형성하게 됩니다.

지역 분석

2024년 탄저균 치료 시장은 세계 최대의 바이오디펜스 지출과 FDA 승인 프로세스의 합리화를 배경으로 북미가 52.23%의 매출을 차지해 지배적이었습니다. BARDA의 다년간 계약은 현지 제조 능력을 지원하고 Project BioShield의 예측 가능한 보충 주기는 공급자의 현금 흐름을 안정시킵니다. 캐나다와 멕시코는 삼국 간의 방위 협력과 공급망 물류 공유를 통해 수요 증가에 기여하고 공급 중단에 대한 지역 회복력을 확보하고 있습니다.

유럽은 매출에서 2위를 차지하고 있지만, 각국 조달 전략의 단편화에 의해 미국에 비해 구매력은 약해지고 있습니다. 의료 안보위원회가 주도하는 EU 수준의 대처에서는 비축의 사양을 서서히 조화시켜, 팬데믹 백신의 모델과 같은 공동 구입을 모색하고 있습니다. NATO 연습은 국경을 넘어서는 상호 운용성을 강화하고, 회원국에 조달 로드맵의 갱신을 촉구하고 있습니다. EMA와의 규제 연계에 의해 이중 신청 전략이 가속화되어 미국이 승인한 탄저균 대책약의 보완 시장으로서 유럽이 매력적이 됩니다.

아시아태평양은 CAGR 9.49%로 가장 급성장하고 있으며, 한국의 2025년 재조합 백신 승인, 일본의 QUAD와 연계한 생물방위 투자, 호주의 의료 대책 이니셔티브의 확대가 그 원동력이 되고 있습니다. 국방동맹은 협조적인 조달로 이어져 보다 광범위한 균주를 커버하고 내열성 향상을 약속하는 차세대 플랫폼을 대량으로 구입하게 됩니다. 중국과 인도는 불투명한 규제 제도가 단기적인 수익 전망을 약화시키고 있는 것, 국산 백신 개발의 파일럿 프로젝트나 BSL-4 연구센터의 확대가 보여주듯 관심이 높아지고 있습니다. 이러한 추세를 종합하면 아시아태평양의 탄저균 치료 시장 점유율은 2030년까지 유럽과 비교할 때까지 상승할 수 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 정부의 생물 방위 자금 조달 및 비축 프로그램

- 바이오 테러의 위협 및 국가 안보에 대한 관심 증가

- CBRN 대책에 관한 규제의 신속화

- 단일클론항체 플랫폼의 스케일 효율화

- 탄저균에 대한 AI 주도의 약제 재이용 파이프라인

- 공동 조달을 뒷받침하는 APAC 방위 얼라이언스

- 시장 성장 억제요인

- 한정된 상업적 수익성이 민간 연구개발의 저해요인

- 항균제 내성균 증가에 의한 항생제 유용성의 저하

- 열대지역에서의 항독소 및 백신 전개에서 콜드체인의 갭

- 긴급 사용 허가에 대한 국민의 회의적인 견해

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 항생제

- 항독소

- 백신

- 보조요법 및 지지요법

- 투여 경로별

- 경구

- 주사제

- 기타

- 최종 사용자별

- 군 및 방위 관계자

- 민간 긴급 비축품

- 병원 및 전문 클리닉

- 유통 채널별

- 정부 조달 기관

- 병원 약국

- 소매 및 온라인 약국

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Emergent BioSolutions

- GlaxoSmithKline(GSK)

- Elusys Therapeutics

- Altimmune

- Soligenix

- Bavarian Nordic

- Pfizer

- Roche

- DynPort Vaccine Company

- SIGA Technologies

- Tonix Pharmaceuticals

- AN2 Therapeutics

- GC Biopharma

- Emergent Product Development(Raxibacumab)

제7장 시장 기회 및 전망

AJY 25.10.29The anthrax therapeutics market was valued at USD 407.17 million in 2025 and is forecast to reach USD 643.44 million by 2030, reflecting a 7.93% CAGR during the period.

Momentum stems from sustained government biodefense budgets, accelerated regulatory pathways, and heightened security awareness that positions medical countermeasures as national assets rather than conventional pharmaceutical products. Project BioShield's multi-year contracts, the Public Health Emergency Medical Countermeasures Enterprise's mention need of USD 79.5 billion funding for 2023-2027, and similar European and Asia-Pacific initiatives collectively anchor long-term demand. The anthrax therapeutics market benefits from next-generation vaccine approvals, maturing monoclonal-antibody platforms, and AI-enabled drug-repurposing pipelines that shorten discovery timelines while diversifying treatment modalities. Commercial profitability remains modest, yet predictable sovereign procurement and replenishment cycles provide contractors with revenue visibility that offsets the absence of broad civilian sales channels.

Global Anthrax Treatment Market Trends and Insights

Government Biodefense Funding & Stockpiling Programs

Steady, multi-year public funding converts the anthrax therapeutics market into a quasi-sovereign procurement arena. BARDA's replenishment contracts for NUZYRA and its USD 6.7 billion Strategic National Stockpile expansion demonstrate a move from episodic purchasing to life-cycle management that rewards manufacturers able to sustain surge capacity. NIH-funded development of novel agents such as epetraborole illustrates how public capital underwrites early-stage R&D, insulating companies from commercial demand risk. Similar frameworks in the European Union and Australia mirror this model, creating synchronized global demand that stabilizes manufacturing economics. The result is a predictable production pipeline that supports specialized facilities and a resilient supply chain, reinforcing long-run growth for the anthrax therapeutics market.

Rising Bioterrorism Threat & National Security Focus

Escalating geopolitical tensions elevate biological weapons from niche concerns to mainstream defense priorities. The Defense Threat Reduction Agency's USD 12.2 million hazard-prediction program and NATO's integrated CBRN preparedness exercises show how governments couple intelligence assessments with real procurement commitments. Security agencies demand therapies that remain stable, deployable, and effective in austere environments, encouraging formulation research that stretches beyond traditional hospital settings. These operational requirements, framed within military doctrine, ensure that funding remains insulated from economic downturns and electoral cycles. Consequently, the anthrax therapeutics market gains a durable revenue base tied to national security rather than discretionary healthcare spending.

Limited Commercial Profitability Discouraging Private R&D

Revenue for anthrax therapeutics hinges on batch purchases that follow stockpile replenishment calendars rather than continuous market pull. Emergent BioSolutions' 71% revenue swing between Q4 2023 and Q4 2024 underscores how contract timing creates financial volatility that pure-play biotech investors often avoid. For small-molecule antibiotics, development costs can exceed USD 100 million, yet the total accessible anthrax therapeutics market size is constrained by government allocations, capping upside returns. This structural dynamic narrows the field of active developers, slows pipeline diversification, and elevates supply-chain concentration risk over the forecast horizon.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Fast-Track Incentives for CBRN Countermeasures

- Monoclonal-Antibody Platform Scale Efficiencies

- Escalating Antimicrobial Resistance Reducing Antibiotic Utility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The anthrax therapeutics market size for antibiotics stood highest in 2024 thanks to their long-established role in post-exposure prophylaxis and treatment regimens. Stockpile managers favor ciprofloxacin and doxycycline for cost-efficiency, but efficacy debates and resistance trends stimulate portfolio diversification. Antitoxins, while holding a smaller revenue base, exhibit the strongest growth owing to their toxin-neutralizing capacity independent of bacterial resistance. Raxibacumab and Obiltoxaximab are standard inclusions in U.S. Strategic National Stockpile planning, while Anthrasil contributes plasma-derived diversity that mitigates single-source vulnerability. UPMC's 2025 breakthrough extending therapeutic windows beyond the historical "point of no return" promises to widen clinical applicability. Computational repurposing has flagged several small-molecule inhibitors of edema and lethal factors, suggesting future adjunct therapies that may further reshape the anthrax therapeutics market.

Government contracts increasingly package antibiotics and antitoxins together, acknowledging the complementary roles each class plays in multi-phase response protocols. The anthrax therapeutics market share for antitoxins thus benefits from policy shifts rather than pure clinical demand. Vaccines remain primarily preventive for pre-exposure settings such as military deployments, yet South Korea's recombinant platform approval could broaden indications toward civilian prophylaxis. Adjunctive therapies addressing coagulopathies and systemic inflammation still command modest revenue but provide critical value in severe cases, reinforcing the holistic treatment paradigm that now defines the anthrax therapeutics market.

Injectable formats dominate stockpiles due to rapid systemic availability, especially for severe inhalational anthrax where time-to-treatment is decisive. Raxibacumab and Obiltoxaximab remain intravenous only, anchoring this preference. Nonetheless, oral antibiotics are gaining favor for post-exposure prophylaxis campaigns where mass distribution is required within narrow windows. Preclinical studies confirm therapeutic efficacy when dosing commences within 24 hours of exposure, validating the logistical appeal of tablets in field conditions. Updated CDC guidelines recommend oral doxycycline or levofloxacin for 60-day prophylaxis courses, aligning policy with evolving evidence.

Temperature stability trials for capsule formulations mirror vaccine thermostability research, seeking to eliminate cold-chain dependence that constrains tropical deployments. Adoption of strip-packaged antibiotics suitable for parachute or drone delivery hints at future innovations that meld pharmaceutical design with defense logistics. Other routes, including inhalational powder formulations under investigation, could eventually complement current options, yet regulatory familiarity with oral and injectable pathways means these two will continue shaping the anthrax therapeutics market over the forecast horizon.

The Anthrax Treatment Market Report Segments the Industry Into by Product Type (Antibiotics, Antitoxinx and More), Rouet of Administration (Oral, Injectabales and More), by End User (Military & Defense Personnel, Civilian Emergency Stockpiles and More), by Distribution Channel (Government Procurement Agencies, Hospitals and More) and Geography (North America, Europe, Asia Pacific and More).

Geography Analysis

North America dominated the anthrax therapeutics market in 2024, accounting for 52.23% revenue on the back of the world's largest biodefense outlays and streamlined FDA approval processes. BARDA's multi-year contracts underpin local manufacturing capacity, while Project BioShield's predictable replenishment cycles stabilize supplier cash flows. Canada and Mexico contribute incremental demand through trilateral defense cooperation and shared supply-chain logistics, ensuring regional resilience against supply disruptions.

Europe ranks second in revenue, though fragmentation among national procurement strategies dilutes buying power relative to the United States. EU-level initiatives led by the Health Security Committee are gradually harmonizing stockpile specifications and exploring joint purchasing akin to pandemic vaccine models. NATO exercises reinforce cross-border interoperability, prompting member states to update procurement roadmaps that could lift regional demand during 2026-2030. Regulatory alignment with EMA accelerates dual filing strategies, making Europe an attractive supplementary market for U.S.-approved anthrax countermeasures.

Asia-Pacific is the fastest growing geography, set for a 9.49% CAGR driven by South Korea's 2025 recombinant vaccine approval, Japan's QUAD-aligned biodefense investments, and Australia's expanding Medical Countermeasures Initiative. Defense alliances translate into coordinated procurement, with bulk buys favoring next-generation platforms that promise broader strain coverage and improved thermostability. China and India signal rising interest, evidenced by pilot projects in indigenous vaccine development and BSL-4 research center expansion, although opaque regulatory systems temper near-term revenue prospects. Collectively, these trends propel regional momentum that could raise Asia-Pacific's anthrax therapeutics market share to rival Europe by 2030.

- Emergent Bio Solutions

- GlaxoSmithKline (GSK)

- Elusys Therapeutics

- Altimmune

- Soligenix

- Bavarian Nordic

- Pfizer

- Roche

- DynPort Vaccine Company

- SIGA Technologies

- Tonix Pharmaceuticals

- AN2 Therapeutics

- GC Biopharma

- Emergent Product Development (Raxibacumab)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government biodefense funding & stockpiling programs

- 4.2.2 Rising bioterrorism threat & national security focus

- 4.2.3 Regulatory fast-track incentives for CBRN counter-measures

- 4.2.4 Monoclonal-antibody platform scale efficiencies

- 4.2.5 AI-driven drug-repurposing pipelines for B. anthracis

- 4.2.6 APAC defence alliances boosting joint procurement

- 4.3 Market Restraints

- 4.3.1 Limited commercial profitability discouraging private R&D

- 4.3.2 Escalating antimicrobial resistance reducing antibiotic utility

- 4.3.3 Cold-chain gaps for antitoxin/vaccine deployment in tropics

- 4.3.4 Public skepticism over emergency-use authorizations

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Antibiotics

- 5.1.2 Antitoxins

- 5.1.3 Vaccines

- 5.1.4 Adjunctive & Supportive Therapies

- 5.2 By Route of Administration

- 5.2.1 Oral

- 5.2.2 Injectable

- 5.2.3 Others

- 5.3 By End User

- 5.3.1 Military & Defense Personnel

- 5.3.2 Civilian Emergency Stockpiles

- 5.3.3 Hospitals & Specialty Clinics

- 5.4 By Distribution Channel

- 5.4.1 Government Procurement Agencies

- 5.4.2 Hospital Pharmacies

- 5.4.3 Retail & Online Pharmacies

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Emergent BioSolutions

- 6.3.2 GlaxoSmithKline (GSK)

- 6.3.3 Elusys Therapeutics

- 6.3.4 Altimmune

- 6.3.5 Soligenix

- 6.3.6 Bavarian Nordic

- 6.3.7 Pfizer

- 6.3.8 Roche

- 6.3.9 DynPort Vaccine Company

- 6.3.10 SIGA Technologies

- 6.3.11 Tonix Pharmaceuticals

- 6.3.12 AN2 Therapeutics

- 6.3.13 GC Biopharma

- 6.3.14 Emergent Product Development (Raxibacumab)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment