|

시장보고서

상품코드

1842550

비강 약물 전달 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Nasal Drug Delivery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

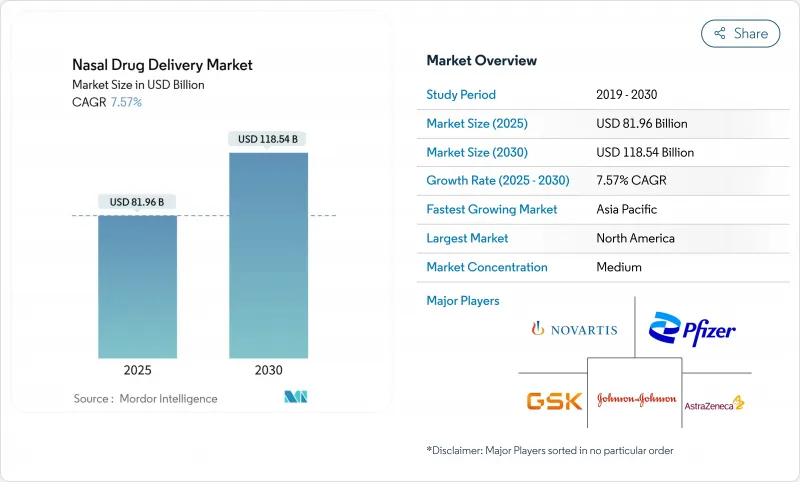

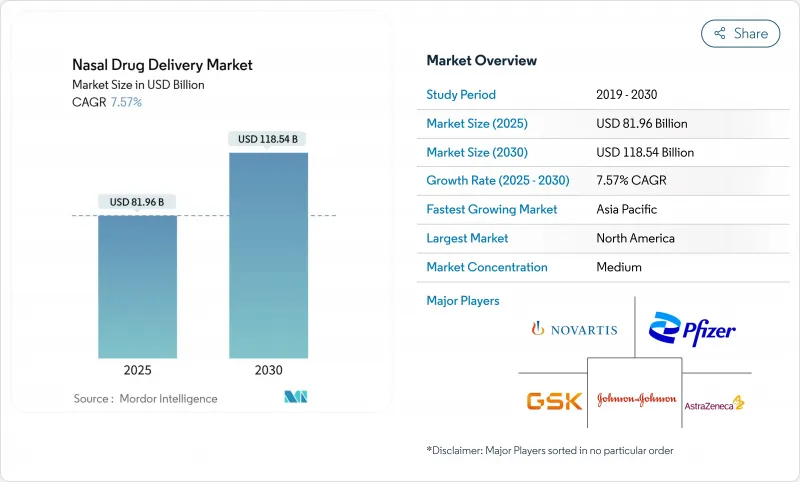

비강 약물 전달 시장은 2025년에 819억 6,000만 달러로 추정되고, 2030년에는 1,180억 4,000만 달러에 도달할 것으로 예측되며, CAGR 7.57%로 성장할 전망입니다.

이러한 견조한 성장은 저분자 치료제 및 고분자 치료제 모두에서 비강 투여가 틈새 분야에서 주류 선택으로 바뀌는 규제 당국의 승인을 반영합니다. 바늘이 없는 에피네프린, 집에서 인플루엔자 예방접종, 중국 최초의 비강 항우울제 등은 환자 중심의 혁신의 강력한 추진력을 보여줍니다. 특히 자가투여가 과밀한 의료 현장의 부담을 경감하는 경우, 기업은 새로운 디바이스와 약제의 조합으로 규제의 기세에 대항하고 있습니다. 건식 분말 기술, 가압 전달 시스템 및 스마트 장치의 통합은 제제 과학과 엔지니어링의 엄격함을 균형 잡을 수 있는 기업에게 경쟁 우위를 더욱 높일 수 있습니다. 모든 지역에서 비강 약물 전달 시장은 더 빠른 투여 시작, 저침습 경로, 콜드체인 제약으로부터의 해방을 요구하는 환자로부터 이익을 얻고 있습니다.

세계의 비강 약물 전달 시장 동향 및 인사이트

알레르기성 비염 및 만성 부비동염의 유병률 증가

알레르기성 비염 및 만성 부비동염의 부담이 증가하고 있기 때문에 비강 치료에 대한 수요가 견조해지고 있습니다. FDA는 2024년 3월 비용종이 없는 만성 부비동염에 대한 플루티카손 프로피온산 에스테르(XHANCE)를 승인하고 염증을 일으킨 코 조직을 대상으로 하는 호기 전달 기술을 검증했습니다. 3단계 데이터에서는 현저한 증상 완화 및 악화 감소가 확인되었으며, 호흡기 시장의 대응 가능성이 확대되고 있습니다. 파이프라인 프로그램은 늦은 임상시험에서 코와 눈 점수를 향상시킨 IL-4 수용체 단일클론항체인 스타포키바트와 같은 생물학적 제형에도 확장되어 새로운 부류의 표적 비강 면역요법을 시사합니다.

자가투여의 보급

규제 당국은 현재 환자의 손에 의한 투여를 지지하고 있습니다. 2024년 9월, FDA는 자체 투여가 승인된 최초의 백신인 FluMist의 자택 사용을 승인했습니다. 유용성 연구는 연령대에 관계없이 안전하게 투여할 수 있음을 확인하였고, 주사 바늘에 대한 불안과 진료 일정의 병목 현상을 모두 제거하였습니다. 유사한 설계 원칙은 의사의 모니터링 없이 긴급 에피네프린을 허용하는 neffy에도 적용되었습니다. 병원 약사의 교육 프로그램은 올바른 절차를 강화하고 장비 혁신과 실제 어드히어런스 사이의 피드백 루프를 강화했습니다.

약성 비염을 일으키는 과도한 사용으로 인한 합병증

장기간 혈관 수축제의 사용은 코 막힘의 재발을 유발할 수 있습니다. 설문 조사에 따르면 캐나다 이비인후과 의사의 75%가 현재 경고 표시가 불충분하다고 생각하고 있으며, 30% 가까이 있는 환자가 상담을 받더라도 시판 스프레이를 멈출 수 없다고 합니다. 심한 경우에는 수술로 인한 비갑 개축 소술이 필요하며 복잡성과 비용이 많이 듭니다.

부문 분석

2024년의 비강 약물 전달 시장의 43.23%는 스프레이가 차지했으며, 이는 수십년에 걸친 임상에서의 친숙함을 반영하고 있습니다. 그러나 항체나 펩티드를 안정화시키기 위해 동결 건조 및 분무 건조법을 이용하는 기업이 늘어나 건조 분말은 매년 10.56% 성장할 것으로 예측되고 있습니다. 박막 동결건조된 단일클론항체는 냉장 없이 효과적인 에어로졸 성능을 달성합니다. 호흡식 기복기는 점착성 부형제와 결합되어 체류 시간을 더욱 연장시킵니다. 적하제는 소아과에서 그 역할을 유지하며 겔제는 지속적인 점막 접촉이 필요한 만성 사례에 해당합니다. 각 투약 형태는 각각 다른 임상 요구에 대응하고 있지만, 안정성 및 환자의 편리성을 양립시킨 분제가 가장 기세가 있습니다.

비강 약물 전달 시장 규모는 건조 분말이 가장 빠르게 확장되는 반면, 스프레이는 계속 기준선 수익의 중심이 되고 있습니다. 현재 제품 설계의 핵심은 입자 형태를 일관된 투여에 연결하는 퀄리티 바이 디자인의 틀입니다. 나노 캐리어를 탑재한 분말은 백신, 유전자 치료, 뇌를 표적으로 한 종양학으로 치료의 프론티어를 밀어 펼치고 있습니다. 이 균형 잡힌 포트폴리오를 통해 제조업체는 성숙한 수량과 고성장 혁신의 흐름을 헤지할 수 있습니다.

비가압식은 저비용으로 심플한 설계로 인해 2024년 매출의 62.12%를 차지했습니다. 생물학적 제형은 종종 정확하고 반복 가능한 용량을 필요로 하기 때문에 가압식은 CAGR 9.66%의 궤도에 있습니다. Aptar의 SipNose 기술 인수는 깨지기 쉬운 단백질을 보호하는 부드러운 미스트 플랫폼에 대한 자신감의 표현입니다. Bespak의 주문을 받아서 만들어진 벨브는 정확도를 더 강화합니다. 동시에 NasaDose와 같은 단위 용량 장치는 무균성을 향상시키고 긴급 신경학적 분무에 매력적입니다.

비강 약물 전달 시장이 발전함에 따라 용기 선택은 분자의 복잡성을 따릅니다. 큰 항체는 분출 형태가 보장되고 전단 응력이 최소화되는 가압 장치를 선호합니다. 저분자와 충혈제거제는 가격에 민감한 펌프식 스프레이에 머물러 있습니다. 푸시 풀 다이내믹은 공급업체가 이중 제조 라인을 유지하면서 제형 규제를 충족시키기 위해 품질 관리를 향상시켜야 함을 의미합니다.

지역 분석

북미는 성숙한 규제 체제, 조기 도입 기업, 높은 알레르기성 비염 유병률을 배경으로 2024년 38.47% 시장 점유율을 유지했습니다. 이 지역은 또한 FDA의 강력한 참여를 반영하고 고분자 비강 생물 제형의 첫 번째 출시 지역 역할을 합니다. 유럽은 견고한 상환 구조로 이어지지만, 제네릭 의약품의 가격대가 완만해지기 때문에 성장은 보다 완만해지고 있습니다. 그러나 엄격한 의료기기 가이드 라인은 유전자 재조합 제제의 프리미엄 영역을 유지합니다.

아시아태평양은 CAGR 10.16%로 돌출한 성장 엔진입니다. 중국에서는 2024년 6월 우울증 치료제로 에스케타민의 점비약이 승인되었으며 중추신경계의 생물 제형이 승인되었습니다. 일본은 급추하고 있습니다. 아큐리스 파마가 2024년에 신청한 디아제팜은 미래의 비강 발작 치료제의 발매를 시사하고 있습니다. 호주는 바늘을 사용하지 않는 에피네프린의 개발을 급피치로 진행하고 있으며, 이러한 동향을 반영하고 있습니다.

중동 및 아프리카는 현재 진행중인 콜드체인 개선으로 고감도 생물 제형이 주요 도시의 중심부에 도달했습니다. 남미에서는 호흡기 질환의 이환율이 높고 외래 진료소가 혼잡하여 자기 투여 스프레이의 매력이 높아지고 있습니다. 공급망이 성숙함에 따라, 비강 약물 전달 시장은 제조 지역화와 규제 조화를 통해 지역 실적을 계속 확대할 것으로 보입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 알레르기성 비염 및 만성 부비동염의 유병률 증가

- 자가투여의 보급 확대

- 바늘을 사용하지 않는 투여 방법에 대한 환자 기호의 고조

- 비강 투여에 의한 고분자 생물 제제의 승인(2025년 이후)

- 팬데믹에 의한 콜드체인에 의한 비용 절감 추진

- 어드히어런스 추적을 위한 센서가 있는 스마트 비강 장치

- 시장 성장 억제요인

- 비염을 일으키는 과도한 사용으로 인한 합병증

- 주요 알레르기성 비염 브랜드 특허의 절벽(2025-2027년)

- 온도에 민감한 생물 제형의 콜드체인 무결성 위험

- 엄격한 규제

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 제형별

- 스프레이

- 액제

- 젤

- 건조 분말

- 기타

- 용기 유형별

- 비가압 용기

- 가압 용기

- 치료 용도별

- 비염

- 코 막힘

- 천식

- 통증 관리

- 백신 접종

- 기타

- 최종 사용자별

- 병원

- 재택치료

- 외래수술센터(ASC)

- 전문 클리닉

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Solventum

- Neurelis Inc.

- AptarGroup Inc.

- AstraZeneca PLC

- BD(Becton, Dickinson & Co.)

- GlaxoSmithKline PLC

- Johnson & Johnson Services Inc.

- Merck & Co., Inc.

- Novartis AG

- Pfizer Inc.

- Teva Pharmaceutical Industries Ltd.

- Cipla Ltd.

- Bausch Health Companies Inc.

- OptiNose Inc.

- Impel NeuroPharma Inc.

- Kurve Technology Inc.

- Recipharm AB

- Sun Pharma Industries Ltd.

- Hikma Pharmaceuticals PLC

- Dr. Reddy's Laboratories Ltd.

- Sandoz International GmbH

제7장 시장 기회 및 전망

AJY 25.10.29The nasal drug delivery market is valued at USD 81.96 billion in 2025 and is forecast to reach USD 118.04 billion in 2030, advancing at a 7.57% CAGR.

This solid growth reflects regulatory approvals that have shifted intranasal administration from niche use to a mainstream option for both small- and large-molecule therapeutics. Needle-free epinephrine, at-home influenza vaccination, and the first intranasal antidepressant in China illustrate the powerful pull of patient-centric innovation. Companies are matching the regulatory momentum with new device-drug combinations, especially where self-administration reduces the burden on overcrowded care settings. Dry-powder technologies, pressurized delivery systems, and smart-device integration together deepen the competitive moat for firms that can balance formulation science with engineering rigor. Across every region, the nasal drug delivery market benefits from patients seeking faster onset, less invasive routes, and freedom from cold-chain constraints.

Global Nasal Drug Delivery Market Trends and Insights

Increasing Prevalence of Allergic Rhinitis & Chronic Sinusitis

The rising burden of allergic rhinitis and chronic sinusitis sustains steady demand for intranasal therapies. The FDA cleared fluticasone propionate (XHANCE) for chronic rhinosinusitis without nasal polyps in March 2024, validating exhalation-delivery technology that targets inflamed nasal tissue. Phase 3 data show marked symptom relief and fewer exacerbations, broadening the addressable respiratory market. Pipeline programs extend to biologics such as stapokibart, an IL-4 receptor monoclonal antibody that improved nasal and ocular scores in late-stage trials, pointing to a new class of targeted intranasal immunotherapies.

Growing Adoption of Self-Administration Practices

Regulators now back patient-handled delivery. In September 2024 the FDA authorized FluMist for at-home use, the first vaccine approved for self-administration. Usability studies confirmed safe delivery across age brackets, removing both needle anxiety and clinic scheduling bottlenecks. Similar design principles guided neffy, which enables emergency epinephrine without medical supervision, a meaningful advance for people who avoid injectors. Education programs from hospital pharmacists reinforce correct technique, tightening the feedback loop between device innovation and real-world adherence.

Overuse Complications Causing Rhinitis Medicamentosa

Prolonged vasoconstrictor use can trigger rebound congestion. Surveys show 75% of Canadian otolaryngologists think current warning labels are insufficient, and nearly 30% of patients cannot stop over-the-counter sprays despite counseling. Severe cases call for surgical turbinate reduction, adding complexity and cost.

Other drivers and restraints analyzed in the detailed report include:

- Rising Patient Preference for Needle-Free Routes

- Regulatory Approvals of Large-Molecule Biologics Via Intranasal Route (2025+)

- Patent Cliff For Leading Allergic-Rhinitis Brands (2025-27)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sprays owned 43.23% of the nasal drug delivery market in 2024, reflecting decades of clinical familiarity. Dry powders, however, are projected to grow 10.56% annually as firms harness freeze-drying and spray-drying methods to stabilize antibodies and peptides. Thin-film freeze-dried monoclonal antibodies achieve effective aerosol performance without refrigeration. Breath-actuated insufflators, combined with mucoadhesive excipients, further lift residence time. Drops retain a role in pediatrics, while gels cater to chronic cases needing sustained mucosal contact. Each modality meets distinct clinical needs, yet powders capture the highest forward momentum by marrying stability with patient convenience.

The nasal drug delivery market size for dry powders is set to expand at the fastest clip, whereas sprays continue to anchor baseline revenue. Product design now centers on Quality by Design frameworks that link particle morphology to consistent dosing. Nanocarrier-loaded powders push the therapeutic frontier into vaccines, gene therapy, and brain-targeted oncology. This balanced portfolio lets manufacturers hedge mature volume against high-growth innovation streams.

Non-pressurized formats delivered 62.12% of 2024 sales due to low cost and simple design. Pressurized systems are on a 9.66% CAGR trajectory because biologics often need exact, repeatable doses. Aptar's acquisition of SipNose technology signals confidence in soft-mist platforms that protect fragile proteins. Bespak's customizable valves add another layer of precision. At the same time, unit-dose devices such as NasaDose improve sterility, making them attractive for emergency neurologic sprays.

As the nasal drug delivery market evolves, container choice increasingly follows molecule complexity. Large antibodies favor pressurized devices that guarantee plume geometry and minimal shear stress. Small molecules and decongestants stay in pump sprays for price sensitivity. The push-pull dynamic means suppliers must maintain dual manufacturing lines while upgrading quality control to meet combination-product regulations.

Nasal Drug Delivery Market Report is Segmented by Dosage Form (Sprays, Drops & Liquids, Gels, Dry Powders and Others), Container Type (Non-Pressurized Containers and Pressurized Containers), Therapeutic Application (Rhinitis, Nasal Congestion, Asthma, Pain Management and More), End User (Hospitals, Home Health Care and More) and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 38.47% market share in 2024 on the back of a mature regulatory framework, early adopter payers, and high allergic-rhinitis prevalence. The region also acts as the first launch pad for large-molecule nasal biologics, reflecting strong FDA engagement. Europe follows with robust reimbursement structures, yet growth is more measured as generics temper price points. Stringent device guidelines, though, preserve premium space for engineered combination products.

Asia Pacific is the standout growth engine at a 10.16% CAGR. China's June 2024 approval of esketamine nasal spray for depression validated the route for central-nervous-system biologics and unlocked a sizeable untreated segment. Japan positions itself as a fast follower: Aculys Pharma's diazepam filing in 2024 signals future intranasal seizure-rescue launches. Australia mirrors these trends by fast-tracking needle-free epinephrine.

Middle East and Africa benefit from ongoing cold-chain upgrades that allow sensitive biologics to reach major urban centers. In South America, high respiratory-disease incidence and crowded outpatient clinics strengthen the appeal of self-administered sprays. As supply chains mature, the nasal drug delivery market will continue to widen its geographic footprint through localized manufacturing and regulatory harmonization.

- Solventum

- Neurelis Inc.

- AptarGroup Inc.

- AstraZeneca

- BD (Becton, Dickinson & Co.)

- GlaxoSmithKline

- Johnson & Johnson

- Merck

- Novartis

- Pfizer

- Teva Pharmaceutical Industries

- Cipla

- Bausch Health

- OptiNose Inc.

- Impel NeuroPharma Inc.

- Kurve Technology Inc.

- Recipharm

- Sun Pharma Industries Ltd.

- Hikma Pharmaceuticals

- Dr. Reddy's Laboratories Ltd.

- Sandoz Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence Of Allergic Rhinitis & Chronic Sinusitis

- 4.2.2 Growing Adoption Of Self-Administration Practices

- 4.2.3 Rising Patient Preference For Needle-Free Routes

- 4.2.4 Regulatory Approvals Of Large-Molecule Biologics Via Intranasal Route (2025+)

- 4.2.5 Pandemic-Driven Cold-Chain Cost-Saving Push

- 4.2.6 Sensor-Enabled Smart Nasal Devices For Adherence Tracking

- 4.3 Market Restraints

- 4.3.1 Overuse Complications Causing Rhinitis Medicamentosa

- 4.3.2 Patent Cliff For Leading Allergic-Rhinitis Brands (2025-27)

- 4.3.3 Cold-Chain Integrity Risk For Temperature-Sensitive Biologics

- 4.3.4 Stringent Regulations

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Dosage Form

- 5.1.1 Sprays

- 5.1.2 Drops & Liquids

- 5.1.3 Gels

- 5.1.4 Dry Powders

- 5.1.5 Others

- 5.2 By Container Type

- 5.2.1 Non-Pressurized Containers

- 5.2.2 Pressurized Containers

- 5.3 By Therapeutic Application

- 5.3.1 Rhinitis

- 5.3.2 Nasal Congestion

- 5.3.3 Asthma

- 5.3.4 Pain Management

- 5.3.5 Vaccination

- 5.3.6 Others

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Home Health Care

- 5.4.3 Ambulatory Surgery Centers

- 5.4.4 Specialty Clinics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Solventum

- 6.3.2 Neurelis Inc.

- 6.3.3 AptarGroup Inc.

- 6.3.4 AstraZeneca PLC

- 6.3.5 BD (Becton, Dickinson & Co.)

- 6.3.6 GlaxoSmithKline PLC

- 6.3.7 Johnson & Johnson Services Inc.

- 6.3.8 Merck & Co., Inc.

- 6.3.9 Novartis AG

- 6.3.10 Pfizer Inc.

- 6.3.11 Teva Pharmaceutical Industries Ltd.

- 6.3.12 Cipla Ltd.

- 6.3.13 Bausch Health Companies Inc.

- 6.3.14 OptiNose Inc.

- 6.3.15 Impel NeuroPharma Inc.

- 6.3.16 Kurve Technology Inc.

- 6.3.17 Recipharm AB

- 6.3.18 Sun Pharma Industries Ltd.

- 6.3.19 Hikma Pharmaceuticals PLC

- 6.3.20 Dr. Reddy's Laboratories Ltd.

- 6.3.21 Sandoz International GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment