|

시장보고서

상품코드

1842553

외과용 드레싱 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Surgical Dressing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

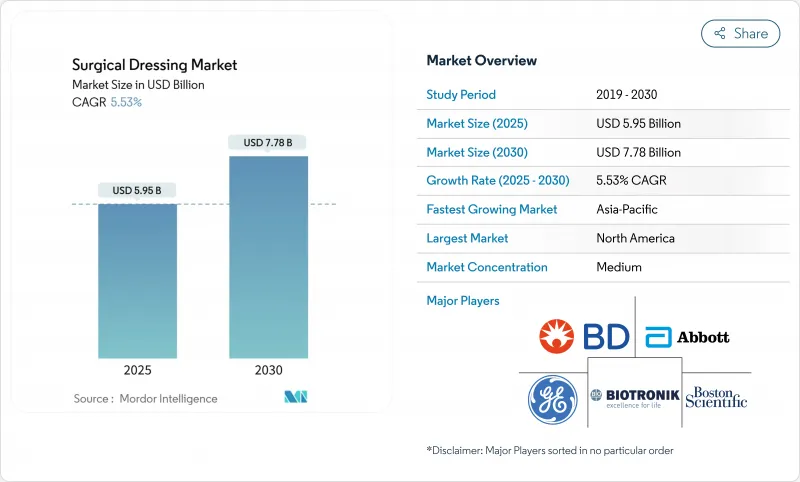

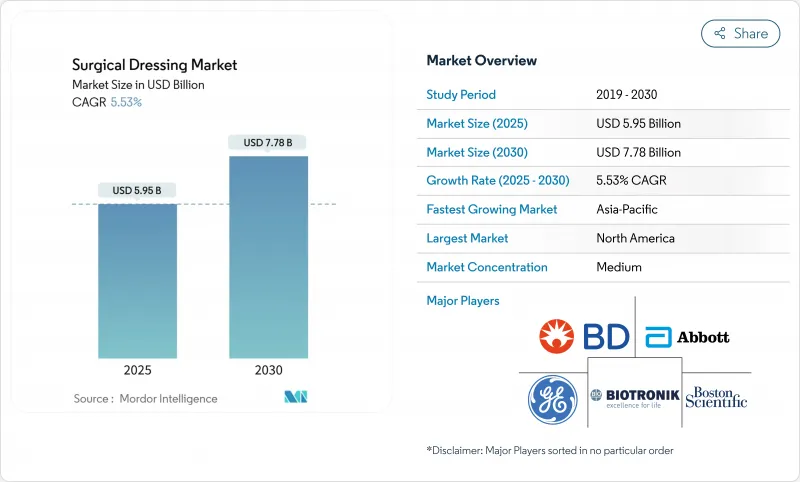

외과용 드레싱 시장은 2025년에 59억 5,000만 달러로 추정되고, CAGR 5.53%로 성장할 전망이며, 2030년에는 73억 8,000만 달러에 이를 것으로 예측됩니다.

고령자에 있어서 만성 상처의 발생률 가속화, 처치에 대한 외래로의 이행, 스마트 항균 생물 활성 드레싱의 꾸준한 기술 혁신입니다. 삼출물에서 바이오마커를 측정하는 캘리포니아 엔지니어링 대학의 iCares 붕대와 같은 실시간 센서 통합은 수동 코팅에서 능동 치료로의 전환을 시사합니다. 중국, 인도, 미국의 규제 개혁은 프리미엄 제품의 채용 장벽을 낮추는 반면, 피부 대체 드레싱에 보험이 적용되어 시장 접근이 확대됩니다. 특수 고분자 공급망 위험과 FDA에 의한 항균성 드레싱의 재분류는 낙관적인 관점을 약화시키지만, 근본적인 인구 역학과 임상 요구는 외과용 드레싱 시장을 계속 지원하고 있습니다.

세계의 외과용 드레싱 시장 동향 및 인사이트

고령화 및 만성 상처 증가

만성 상처는 이미 세계 4,000만 명 이상에 영향을 미치고 있으며, 미국 의료 시스템은 매년 280억 달러 이상의 비용이 듭니다. 당뇨병과 말초 동맥 질환은 궤양 위험을 증가시키기 때문에 당뇨병 발에 관한 국제 작업부는 치유되지 않는 궤양에 수크로오스 옥타 황산염 드레싱을 권장합니다. 메디케어에 따르면 수혜자의 10.5%가 만성 상처를 앓고 있지만 자원 사용량은 매우 많다고 합니다. 메타 분석에 따르면, 고급 드레싱은 전통적인 거즈에 비해 평균 1.09일 치유를 빠르게 하며, 통증 점수도 낮습니다. 이러한 인구 역학 요인은 외과용 드레싱 시장에서 첨단 제품과 표준 제품의 안정적인 불황에 강한 수요를 지원합니다.

외래 및 재택 케어로의 이행

외래에 대한 수술의 이행에 따라 드레싱에 대한 요구가 커지고 있습니다. WoundConnect와 같은 원격 모니터링 플랫폼은 임상의가 매일 방문하지 않고 치유의 진행 상황을 감독하는 데 도움이 되어 병원 이용을 최대 15%까지 줄입니다. 새로운 CMS 코드(G0541, G0542)는 원격 의료를 통해 제공되는 간병인 상처 케어 트레이닝에 적용되어 재택 관리를 촉진합니다. 솔벤텀의 VAC Peel &Place 드레싱은 7일간의 장착과 2분간의 장착이 가능하며, 외래 환자 시프트에 맞춘 제품의 대표격입니다. 이러한 요인들이 결합되어 외과용 드레싱 시장 전체에서 장시간 착용 및 저숙련 솔루션에 대한 수요가 높아지고 있습니다.

엄격한 다중 관할 지역의 규제 경로

EU의 의료기기 규제에서는 종합적인 임상 평가와 시판 후 감시가 요구되고, 승인까지의 스케줄에 12-18개월로 상당한 비용이 들게 되었습니다. FDA는 항균성 드레싱을 클래스 I에서 클래스 II 또는 III로 재분류하기 위한 협의를 하고 있으며, 이로 인해 많은 레거시 제품이 보다 엄격한 시판 전 심사로 이행할 수 있습니다. 독립행정법인 의약품 의료기기 종합 기구에 따르면 일본은 G7 국가 중에서 의료기술 승인의 타임 러그가 가장 길고 평균 24-36개월입니다. 소프트웨어를 통합한 스마트 드레싱은 사이버 보안에 대한 감시의 눈이 엄격해 중소기업에게는 어려움입니다. 이러한 장애물은 외과용 드레싱 시장에서 신기술의 전개를 늦추고 있습니다.

부문 분석

1차 드레싱은 상처지면에서의 중심적인 역할 때문에 2024년 외과용 드레싱 시장 매출의 66.54%를 차지했습니다. 하이드로겔과 알긴산 드레싱은 이상적인 수분 밸런스를 유지하고 최근의 시험에서는 거즈에 비해 1.09일 빨리 치료되는 것으로 나타났습니다. 필름 드레싱은 현재 눈에 보이는 증상보다 빨리 감염을 인식하는 인쇄 pH 센서를 갖추고 있으며 임상 의사에게 조기 발견의 이점을 제공합니다. 고흡수성 폴리머를 사용한 폼 드레싱은 폴 하트만이 실리콘 폼의 호조를 끌어들여 상처 매출액 6억 890만 유로를 기록해 점유율을 확대했습니다. 2차 드레싱은 CAGR 6.12%로 가장 급속하게 성장하고 있는데, 이는 층상 프로토콜로 흡수성과 고정성이 요구되기 때문입니다. 각 회사는 접착제의 경계를 개선하고 허약한 환자의 피부 외상을 줄이는 동시에 7일간 장착해도 씰의 무결성을 유지할 수 있도록 하고 있습니다.

블루투스 연결이 가능한 스마트 프라이머리 드레싱은 배터리 수명과 비용으로 제한되는 틈새 존재이지만, 퇴역군인 병원에서의 파일럿 연구는 환자 만족도가 높은 것으로 나타났습니다. 합성 폴리머 필름은 여전히 판매량의 대부분을 차지하고 있지만, 항균제를 온디맨드로 방출하는 생물공학적으로 설계된 셀룰로오스 복합체는 임상의의 관심을 모으고 있습니다. 가치 기반 계약은 재입원 감소를 평가하므로 구매자는 액티브 드레싱의 단가 높이를 총 의료비 절감 효과와 비교 검토합니다. 지속적인 기술 혁신으로 프라이머리 드레싱은 외과용 드레싱 시장의 최전선에 계속 군림하고 있습니다.

2024년 외과용 드레싱 시장 규모에서 차지하는 궤양 케어의 비율은 31.25%였으며, 고령화 사회에서의 욕창과 정맥성 궤양의 지속적인 부담을 반영하고 있습니다. 그러나 당뇨병 관련 수술은 CAGR 5.93%로 가장 급성장이 전망되는 이용 사례입니다. 당뇨병 발에 관한 국제 워킹 그룹은 현재 신경 허혈성 궤양이 표준 치료에서 4주 이상 경과한 경우 수크로오스 옥타 설페이트 드레싱을 권장합니다. 심혈관계 치료 후 음압 요법은 추가 적용 범위를 확장합니다.

화상의 치료는 여전히 은을 함침시킨 옵션에 의존하지만, 최적의 이온 방출에 대한 논의가 계속되고 있습니다. 장기 이식을 받은 환자는 육아 형성을 촉진하면서 기회 감염을 예방하는 고성능 드레싱을 요구하고 있습니다. 지급자는 점점 더 많은 드레싱을 사용할 수 있도록 사진 증명과 디지털 평면 측정을 요구하고 있으며, 공급업체는 스마트 제품에 이미지 캡처 도구를 통합해야 합니다. 이러한 요구 증가는 외과용 드레싱 시장 전반에 걸친 전문 분야의 성장 전망을 강화하고 있습니다.

지역 분석

북미가 리더십을 유지해 2024년 외과용 드레싱 시장의 42.15%를 차지했습니다. 메디케어나 민간지급 기관에서의 활발한 상환은 치유기간을 단축하거나 통원 횟수를 줄이는 기술에 보답하는 것입니다. 국방부는 2025년 스미스 플러스 네퓨에 7,500만 달러의 음압 시스템을 주문했으며, 이는 선진 의료에 대한 정부의 신뢰를 보여줍니다. 특정 피부 대체물을 상처 관리 제품으로 분류하는 최근 CMS의 정책 전환은 청구를 단순화하고 프리미엄 제품의 신속한 도입을 촉진했습니다. 오라세 상처 젤과 같은 세포 치료제에 대한 FDA의 고속 트랙 지정은 생물학적 혁신에 대한 규제 당국의 지원을 보여줍니다.

아시아태평양은 가장 급성장하는 지역으로, 2030년까지 CAGR 7.15%로 성장할 전망입니다. 중국의 2024년 의료기기법은 품질 관리를 강화하는 한편 국가의료제품관리국을 통해 긴급히 필요한 제품의 심사레인을 앞당깁니다. 인도의 의료기기 프로모션에 관한 자율규범은 윤리적인 마케팅과 명확한 라벨링을 장려하고 임상의의 신뢰를 향상시킵니다. 일본의 400억 달러 의료기기 시장은 고령화와 국민 모두 보험제도가 수요를 유지하고 성장하고 있습니다. 호주는 일부 해외 승인을 승인함으로써 이미 FDA 승인을 받은 드레싱 등록을 가속화하고 수출업체에게 이익을 얻고 있습니다.

유럽에서는 컴플라이언스 비용 상승에도 불구하고 의료기기 규정 하에서 꾸준한 성장을 기록하고 있습니다. 임상 데이터와 시장 조사에 조기 투자를 한 기업이 경쟁력을 획득하고 있습니다. 하트먼은 2024년 상처 케어의 기존 사업 성장률이 4.4%라고 보고했습니다. 북유럽 국가에서는 지속가능성을 목표로 순환형 경제 정책에 따른 생분해성 드레싱 시도가 진행되고 있습니다. 브렉시트 이후 영국 제조업체는 CE와 UKCA를 별도로 신청해야 했고 복잡성이 증가했지만 국내 혁신 보조금도 자극되었습니다. 모든 하위 지역에서 다양한 상환 계획이 지역별 경제적 증거를 요구하고 있으며 공급업체는 각 지불 시스템에 맞는 가치 서류를 작성해야 합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 도입

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 고령화 및 만성 상처 증가

- 외래 및 재택 케어로의 시프트

- 항균 및 생리 활성 드레싱의 제품 혁신

- 고급 드레싱에 대한 상환제도 확대(미국, EU)

- 신흥 아시아에서 수술 건수 증가

- 드레싱에 스마트 및 IoT 센서 통합

- 시장 성장 억제요인

- 여러 법역에 걸친 엄격한 규제 경로

- 입찰 주도의 병원 조달에 의한 가격 저하

- 특수 폴리머 및 특수 섬유 공급망의 불안정성

- 스마트 드레싱의 채용을 제한하는 임상 데이터의 갭

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 제품별

- 프라이머리드레싱

- 필름 드레싱

- 하이드로겔 드레싱

- 하이드로콜로이드 드레싱

- 폼 드레싱

- 알지네이트 드레싱

- 기타 1차 드레싱

- 2차 드레싱

- 흡수제

- 붕대

- 접착 테이프

- 보호제

- 기타 2차 드레싱

- 프라이머리드레싱

- 용도별

- 궤양

- 열상

- 장기 이식

- 심장혈관 수술

- 당뇨병 관련 수술

- 기타 용도

- 최종 사용자별

- 병원 및 클리닉

- 외래수술센터(ASC)

- 재택치료 및 기타 최종 사용자

- 상처 유형별

- 급성 상처

- 만성 상처

- 재료별

- 천연 섬유

- 합성 폴리머

- 생체공학 및 복합재료

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- 3M Company

- Smith & Nephew Plc

- Molnlycke Health Care AB

- ConvaTec Group Plc

- Coloplast A/S

- Cardinal Health Inc.

- Medtronic Plc

- Medline Industries LP

- Johnson & Johnson(Ethicon)

- B. Braun SE

- Hollister Inc.

- Paul Hartmann AG

- Lohmann & Rauscher GmbH

- Urgo Medical

- BSN medical(Essity)

- Acelity(KCI)-3M Advanced Wound Care

- Derma Sciences(Integra LifeSciences)

- Winner Medical Co.

- Advancis Medical

- Medipur

제7장 시장 기회 및 전망

AJY 25.10.29The surgical dressings market is valued at USD 5.95 billion in 2025 and is forecast to reach USD 7.38 billion by 2030, advancing at a 5.53% CAGR.

Demand growth rests on three pillars: the accelerating incidence of chronic wounds among older adults, the migration of procedures to outpatient settings, and steady innovation in smart, antimicrobial, and bio-active dressings. Real-time sensor integration, such as Caltech's iCares bandage that measures biomarkers in exudate, signals a shift from passive coverage to active therapy. Regulatory reforms in China, India, and the United States lower adoption barriers for premium products, while payer policies that now reimburse skin-substitute dressings broaden market access. Supply chain risks in specialty polymers and possible FDA reclassification of antimicrobial dressings temper optimism, yet the underlying demographic and clinical need continues to anchor the surgical dressings market trajectory.

Global Surgical Dressing Market Trends and Insights

Aging Population & Rise in Chronic Wounds

Chronic wounds already affect more than 40 million people worldwide and cost the United States healthcare system over USD 28 billion each year . Diabetes and peripheral arterial disease elevate ulcer risk, prompting the International Working Group on the Diabetic Foot to recommend sucrose octasulfate dressings for non-healing ulcers . Medicare reports that 10.5% of beneficiaries present with chronic wounds but generate outsized resource use, so payers welcome therapies that shorten healing time. Meta-analyses show advanced dressings can accelerate closure by an average of 1.09 days and lower pain scores versus traditional gauze. This demographic driver supports steady, recession-resistant demand across advanced and standard products in the surgical dressings market.

Shift Toward Outpatient & Home-Based Care

Procedure migration to ambulatory sites raises need for dressings that stay in place longer and simplify self-care. Remote monitoring platforms such as WoundConnect help clinicians oversee healing progress without daily visits, reducing hospital utilization by up to 15%. New CMS codes (G0541, G0542) pay for caregiver wound-care training delivered via telehealth, incentivizing home-based management. Solventum's V.A.C. Peel & Place dressing, designed for seven-day wear and two-minute application, typifies products tailored to the outpatient shift. These factors collectively lift demand across the surgical dressings market for extended-wear, low-skill solutions.

Stringent Multi-Jurisdiction Regulatory Pathways

The EU Medical Device Regulation now demands comprehensive clinical evaluation and post-market surveillance, adding 12-18 months and significant expense to approval timelines. The FDA is consulting on reclassifying antimicrobial dressings from Class I to Class II or III, which could shift many legacy products into a stricter pre-market review. Japan continues to post the longest med-tech approval lag among G7 countries, averaging 24-36 months according to its Pharmaceuticals and Medical Devices Agency. Smart dressings that incorporate software draw additional cybersecurity scrutiny, challenging smaller firms. These hurdles slow roll-out of novel technologies within the surgical dressings market.

Other drivers and restraints analyzed in the detailed report include:

- Product Innovations in Antimicrobial & Bio-Active Dressings

- Reimbursement Expansion for Advanced Dressings (US, EU)

- Price Erosion from Tender-Driven Hospital Procurement

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Primary dressings generated 66.54% of surgical dressings market revenue in 2024 due to their central role at the wound bed. Hydrogel and alginate variants maintain an ideal moisture balance, and recent trials show a 1.09-day faster closure versus gauze. Film dressings now house printed pH sensors that flag infection ahead of visible symptoms, giving clinicians an early-warning advantage. Foam dressings with super-absorbent polymers gained share after Paul Hartmann reported EUR 608.9 million in wound revenue on strong silicone-foam uptake. Secondary dressings grow fastest at 6.12% CAGR because layered protocols call for added absorption and securement. Companies refine adhesive borders to reduce skin trauma in frail patients while retaining seal integrity for seven-day wear.

Smart primary dressings capable of Bluetooth connectivity remain a niche, limited by battery life and cost, yet pilot studies in veteran hospitals show high patient satisfaction. Synthetic polymer films still dominate volume but bio-engineered cellulose composites that release antimicrobials on demand capture clinician interest. As value-based contracts reward lower readmissions, purchasers weigh the higher unit price of active dressings against demonstrated reductions in total care costs. Continuous innovation keeps primary dressings at the forefront of the surgical dressings market.

Ulcer care contributed 31.25% to the surgical dressings market size in 2024, reflecting the ongoing burden of pressure and venous ulcers among aging populations. Yet diabetes-related surgery represents the fastest-growing use case at 5.93% CAGR. The International Working Group on the Diabetic Foot now endorses sucrose octasulfate dressings when neuro-ischemic ulcers stall after four weeks of standard care. Negative-pressure therapy after cardiovascular procedures further broadens application scope.

Burn treatment remains dependent on silver-impregnated options, but debate over optimal ion release persists. Organ-transplant recipients demand high-performance dressings that guard against opportunistic infections while promoting granulation. Payers increasingly require photographic proof and digital planimetry to authorize multiple high-cost dressing applications, pushing suppliers to embed image-capture tools within smart products. These evolving needs reinforce growth prospects for specialty segments within the wider surgical dressings market.

The Surgical Dressing Market Report Segments the Industry Into by Product (Primary Dressing, Secondary Dressing), by Application (Ulcers, Burns, Organ Transplants, and More), by End-User (Hospitals/Clinics, Ambulatory Surgical Centers, and More), Wound Type (Acute Wounds and Chronic Wounds), Material (Natural Fibers, and More), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America maintains leadership, holding 42.15% of the surgical dressings market in 2024. Robust reimbursement under Medicare and private payers rewards technologies that shorten healing or reduce clinic visits. The Department of Defense in 2025 awarded Smith+Nephew a USD 75 million contract for negative-pressure systems, signaling government confidence in advanced modalities. Recent CMS policy shifts that classify certain skin substitutes as wound management products simplify billing, fostering faster uptake of premium offerings. FDA fast-track designations for cellular therapies such as Aurase Wound Gel indicate regulatory support for biologic innovation.

Asia-Pacific is the fastest-growing region, expanding at a 7.15% CAGR through 2030. China's 2024 medical device law tightens quality management while setting accelerated review lanes for urgently needed products via its National Medical Products Administration. India's voluntary code on medical device promotion encourages ethical marketing and clearer labeling, improving clinician trust. Japan's USD 40 billion device market grows as its aging population and universal coverage sustain demand, although lengthy approval timelines constrain rapid launches. Australia's recognition of select overseas approvals speeds registration for dressings that already hold FDA clearance, benefiting exporters.

Europe records steady growth under the Medical Device Regulation despite higher compliance costs. Companies that invested early in clinical data and post-market surveillance now gain a competitive edge. Hartmann reported 4.4% organic wound-care growth in 2024, aided by silicone foam uptake, even as hospital tenders drove pricing pressure. Sustainability goals in Nordic countries have prompted pilots of biodegradable dressings, aligning with circular-economy policies. Post-Brexit, UK manufacturers must file separate CE and UKCA submissions, adding complexity but also stimulating domestic innovation grants. Across all sub-regions, diverse reimbursement schemes require localized economic evidence, compelling suppliers to tailor value dossiers to each payer system.

- 3M

- Smiths Group

- Molnlycke Health Care

- Convatec

- Coloplast

- Cardinal Health

- Medtronic

- Medline Industries

- Johnson & Johnson

- B. Braun

- Hollister

- Hartmann Group

- Lohmann & Rauscher GmbH

- Urgo Medical

- BSN medical (Essity)

- Acelity (KCI) - 3M Advanced Wound Care

- Derma Sciences (Integra LifeSciences)

- Winner Medical Co.

- Advancis Medical

- Medipur

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ageing population & rise in chronic wounds

- 4.2.2 Shift toward outpatient & home-based care

- 4.2.3 Product innovations in antimicrobial & bio-active dressings

- 4.2.4 Reimbursement expansion for advanced dressings (US, EU)

- 4.2.5 Growth of surgical volumes in emerging Asia

- 4.2.6 Integration of smart/IoT sensors in dressings

- 4.3 Market Restraints

- 4.3.1 Stringent multi-jurisdiction regulatory pathways

- 4.3.2 Price erosion from tender-driven hospital procurement

- 4.3.3 Supply-chain volatility in specialty polymers & fibers

- 4.3.4 Clinical data gaps limiting adoption of "smart" dressings

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Primary Dressing

- 5.1.1.1 Film Dressing

- 5.1.1.2 Hydrogel Dressing

- 5.1.1.3 Hydrocolloid Dressing

- 5.1.1.4 Foam Dressing

- 5.1.1.5 Alginate Dressing

- 5.1.1.6 Other Primary Dressings

- 5.1.2 Secondary Dressing

- 5.1.2.1 Absorbents

- 5.1.2.2 Bandages

- 5.1.2.3 Adhesive Tapes

- 5.1.2.4 Protectives

- 5.1.2.5 Other Secondary Dressings

- 5.1.1 Primary Dressing

- 5.2 By Application

- 5.2.1 Ulcers

- 5.2.2 Burns

- 5.2.3 Organ Transplants

- 5.2.4 Cardiovascular Surgery

- 5.2.5 Diabetes-Related Surgery

- 5.2.6 Other Applications

- 5.3 By End-User

- 5.3.1 Hospitals & Clinics

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Home-Care & Other End-Users

- 5.4 By Wound Type

- 5.4.1 Acute Wounds

- 5.4.2 Chronic Wounds

- 5.5 By Material

- 5.5.1 Natural Fibers

- 5.5.2 Synthetic Polymers

- 5.5.3 Bio-engineered / Composite

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 3M Company

- 6.3.2 Smith & Nephew Plc

- 6.3.3 Molnlycke Health Care AB

- 6.3.4 ConvaTec Group Plc

- 6.3.5 Coloplast A/S

- 6.3.6 Cardinal Health Inc.

- 6.3.7 Medtronic Plc

- 6.3.8 Medline Industries LP

- 6.3.9 Johnson & Johnson (Ethicon)

- 6.3.10 B. Braun SE

- 6.3.11 Hollister Inc.

- 6.3.12 Paul Hartmann AG

- 6.3.13 Lohmann & Rauscher GmbH

- 6.3.14 Urgo Medical

- 6.3.15 BSN medical (Essity)

- 6.3.16 Acelity (KCI) - 3M Advanced Wound Care

- 6.3.17 Derma Sciences (Integra LifeSciences)

- 6.3.18 Winner Medical Co.

- 6.3.19 Advancis Medical

- 6.3.20 Medipur

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment