|

시장보고서

상품코드

1842556

웨스턴 블롯팅 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global Western Blotting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

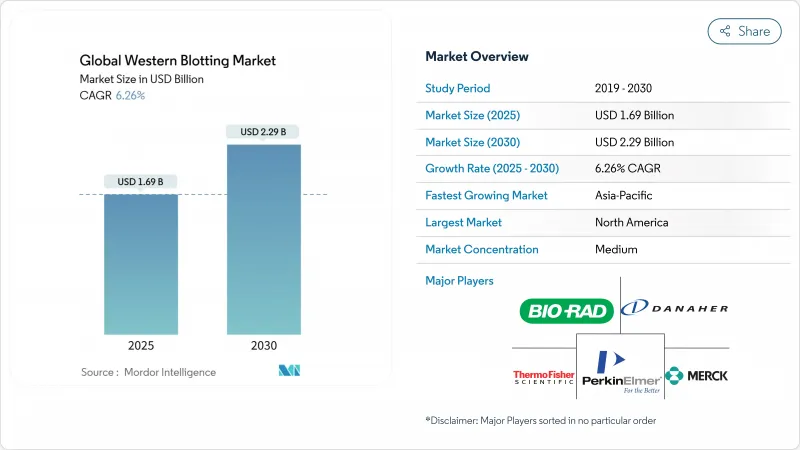

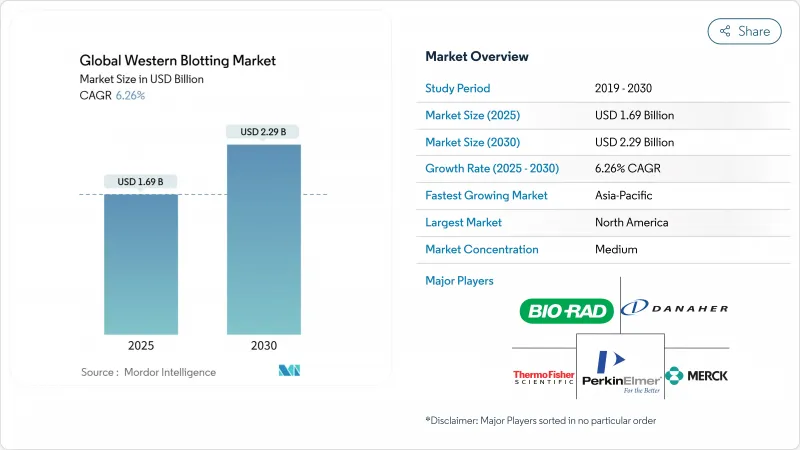

웨스턴 블롯팅 시장은 2025년에 16억 9,000만 달러로 추정되고, 2030년에는 22억 9,000만 달러에 이를 것으로 예측되며, CAGR 6.26%로 성장할 전망입니다.

만성 질환 이환율 증가, 단백질체학 파이프라인 확대, 자동화 투자 파동은 연구 및 진단 워크플로우에서 단백질 확인 분석에 대한 수요를 강화하고 있습니다. 자동화 및 마이크로플루이딕스 플랫폼은 더 높은 처리량, 더 적은 시약 소비, 더 나은 재현성을 필요로 하는 실험실을 끌어들입니다. 항체 검증에서 인공지능(AI)의 통합, 분석 견뢰성에 대한 규제 지침의 강화, 생명과학 분야의 지속적인 자금 조달은 웨스턴 블롯팅 시장의 향후 성장을 지원하고 있습니다. 멀티플렉스 면역분석 및 질량분석 기반 접근법으로부터의 경쟁 압력은 강해지고 있지만, 웨스턴 블롯팅은 여전히 단백질의 발현, 번역후 변형, 치료 제품의 품질을 확인하기 위한 벤치마킹 기법입니다.

세계의 웨스턴 블롯팅 시장 동향 및 인사이트

만성 질환의 유병률 상승

암 발생률은 1995-2022년 유럽에서 58% 상승하여 종양 생물학이나 대사 이상 연구에 있어서 단백질 바이오마커 확인의 지속적인 수요를 만들어내고 있습니다. 종양학 연구는 현재 존재하지 않는 단백질과 번역후 수식의 미묘한 변화를 검출해야 하며, 웨스턴 블롯팅은 그 기능을 확실히 지원합니다. 노인 인구 증가는 만성 질환의 사례 수를 더욱 늘리고 블롯 소모품과 이미지 시약의 일상적인 사용을 강화하고 있습니다. 정밀의료 프로그램이 증가함에 따라, 실험실은 더 높은 처리량을 최소한의 수작업으로 처리하는 자동화된 블롯 플랫폼을 통합합니다. 이러한 패턴은 웨스턴 블롯팅 시장의 수익 길을 길게하고 있습니다.

단백질체학 및 바이오마커 탐색 파이프라인 확대

대규모 단백질체학에 대한 노력이 의약품 탐색의 형태를 바꾸고 있습니다. Thermofisher Scientific에 의한 Olink의 인수(31억 달러)를 통해 회사의 포트폴리오에 5,300개 이상의 유효한 바이오마커 타겟이 추가되었습니다. 마이크로플루이딕스 웨스턴 블롯팅을 이용한 싱글셀 단백질 분석은 벌크 분석에서 놓친 이질성을 드러냅니다. AI를 활용한 항체 스크리닝이 후보의 선택을 가속하고, 밸리데이션에 걸리는 시간을 단축해, 이용 사례를 확대하고 있습니다. 2024년에 18% 증가한 401만 달러로 평가되는 탠덤 질량 태그 시약의 매출 증가는 단백질체학 보완 도구에 대한 적극적인 지출을 보여줍니다. 이러한 추세는 웨스턴 블롯팅 시장에서 지속적인 플랫폼 업그레이드를 지원합니다.

대체 면역 분석 및 알파 기술의 급속한 보급

병렬 반응 모니터링 질량 분광법은 현재 민감도를 향상시킨 항체 없는 검출을 제공하며 기존의 면역 블롯팅에 직접 과제하고 있습니다. MSD, Luminex, AlphaLISA와 같은 멀티플렉스 플랫폼은 펨토그램 레벨 감지로 사이토카인의 동시 측정을 가능하게 합니다. 이 시스템은 분석 시간을 단축하고, 양을 단순화하며, 높은 처리량 스크리닝의 요구에 부합합니다. 속도와 다중화에 중점을 둔 연구실은 특정 워크플로우를 웨스턴 블롯팅 방법에서 전환시켜 제조업체에게 마이크로유체 칩과 통합 이미징을 통한 기술 혁신을 강요하고 있습니다. 웨스턴 블롯팅이 검증의 역할을 유지하는 반면, 대안 기술은 웨스턴 블롯팅 시장의 일상 정량 분야의 확장을 제한합니다.

부문 분석

소모품은 멤브레인, 항체, 완충액, 화학발광 기질의 정기적인 매출을 반영하며 2024년 매출의 65.2%를 차지했습니다. 이러한 광범위한 설치 기반은 웨스턴 블롯팅 시장 공급업체에게 안정적인 현금 흐름을 보장합니다. 자동화 장비 및 마이크로플루이딕스 장비는 절대 판매 규모가 작으며 사용자가 속도와 시약이 적은 실적를 선호하기 때문에 2030년까지 연평균 복합 성장률(CAGR) 8.12%로 확대될 전망입니다. 키트 기반 솔루션은 워크플로우를 더욱 간소화하고, 사용자 편차를 줄이며, 규제 문서화를 용이하게 합니다. 이 부문의 탄력성은 플랫폼의 세련도에 관계없이 불가피한 소모품 교체 사이클에 있습니다.

마이크로플루이딕스 장치는 항체 사용량을 전통적인 1%로 줄이고 분석당 비용을 줄이며 공급 제약을 완화합니다. 이미징 시스템에는 밴드 강도를 평가하는 AI 알고리즘이 내장되어 해석의 주관성이 줄어듭니다. 전통적인 습식 전송 장비는 자본 예산이 하이 엔드 자동화를 채택하는 것을 제한하는 학술 실험실에서 여전히 유용합니다. 겔과 모세관 전기영동 모듈은 시료 준비와 다운스트림 블롯팅의 브리징을 계속하여 웨스턴 블롯팅 시장 전체의 연속성을 지원합니다.

지역 분석

북미는 성숙한 연구 인프라, 엄청난 바이오 의약품 연구개발비, 검증된 단백질 방법을 평가하는 엄격한 규제 감독에 의해 지원되어 2024년 세계 매출의 42.0%를 창출했습니다. 미국이 판매의 대부분을 차지하였고, 캐나다와 멕시코는 바이오 클러스터와 임상시험 활동의 성장을 통해 증수에 기여하고 있습니다. 정부 보조금, 벤처 캐피탈 흐름, 첨단 공급업체 생태계는 자동화 블롯 플랫폼의 조기 채용을 촉진하고 지역 리더십을 유지하고 있습니다.

유럽은 독일, 영국, 프랑스, 스위스에 확립된 생명공학 거점이 있으며 이에 이어집니다. 유럽의 규제 당국은 현재 재현성 있는 분석을 요구하고 있으며, 검증된 항체 소스와 표준 조작 절차에 대한 선호도를 강화하고 있습니다. 스위스의 1,500개 이상의 기업과 60,000명 이상의 고용으로 구성된 생명공학 네트워크는 집중적인 혁신이 어떻게 장비 수요를 키우는지를 보여줍니다. 이탈리아와 스페인과 같은 시장은 제약 제조 및 대학 연구를 통해 시장 규모를 확대하고 있지만, 예산 제약이 장비의 보급률에 영향을 미치고 있습니다.

아시아태평양은 가장 급성장하고 있는 지역으로 2030년까지 CAGR 8.80%로 성장이 예측되고 있습니다. 중국의 대규모 벤처 투자와 국영 생명 과학 공원은 블롯팅 소모품과 자동 이미징 시스템의 대량 조달을 촉진하고 있습니다. 인도에서는 트랜스레이셔널 리서치와 생물 제제의 국내 생산을 지원하는 정부의 이니셔티브로 도입이 가속화되고 있습니다. 일본과 한국은 강력한 의약품 기반과 세계 표준 간의 규제 무결성을 활용하여 대체 사이클을 유지하고 있습니다. 호주와 동남아시아 국가들은 규모가 작은 반면, 보조금을 단백질체학 시설로 향하게 하여 웨스턴 블롯팅 시장에 대한 지역 진입을 강화하고 있습니다. 학계, 정부, 산업계를 연결하는 협력 모델이 인프라를 강화하고 장기적인 성장세를 확실히 하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 만성 질환 증가

- 단백질체학 및 바이오마커 탐색 파이프라인 확대

- 제약 및 바이오테크놀러지 연구개발 예산 증가

- 자동화 및 마이크로유체 Wb 플랫폼의 채용

- 웨스턴 블롯팅 수요를 높이는 AI 주도의 항체 밸리데이션 워크플로우

- 재현 가능한 단백질 데이터에 대한 규제의 초점

- 시장 성장 억제요인

- 대체 면역 분석 및 알파 기술의 급속한 보급

- 웨스턴 블롯팅 장치와 항체의 높은 자본 비용 및 운영 비용

- 재현성을 손상시키는 항체의 배치 간 변동

- 저시약 검정을 지지하는 실험실의 탈탄소화 목표

- 밸류체인 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품별

- 장치

- 겔 및 모세관 전기영동 시스템

- 기존의 습식, 세미드라이 및 드라이 블롯팅 시스템

- 자동화 및 마이크로플루이딕스 플랫폼

- 이미저

- 소모품

- 시약 및 버퍼

- 키트

- 장치

- 용도별

- 생물의학 및 생화학 조사

- 질병 진단

- 농업 및 식품 안전 검사

- 최종 사용자별

- 학술기관 및 연구기관

- 바이오의약품 및 바이오테크놀러지 기업

- 병원 및 진단실험실

- CRO 및 시험 수탁 기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Thermo Fisher Scientific

- Bio-Rad Laboratories

- Danaher(Cytiva & ProteinSimple)

- Merck KGaA(Millipore Sigma)

- PerkinElmer

- LI-COR Biosciences

- Bio-Techne Corporation

- GE Healthcare

- Abcam plc

- Agilent Technologies

- Roche Diagnostics

- Azure Biosystems

- Rockland Immunochemicals

- Advansta Inc.

- GenScript Biotech

- RayBiotech Life

- ProteinSimple(Sartorius)

- BioVision Inc.

- Promega Corporation

- SignalChem Biotech

제7장 시장 기회 및 전망

AJY 25.10.29The western blot market is valued at USD 1.69 billion in 2025 and is forecast to reach USD 2.29 billion by 2030, advancing at a 6.26% CAGR.

Increased chronic-disease incidence, the expansion of proteomics pipelines, and a wave of automation investments reinforce demand for protein confirmation assays in research and diagnostic workflows. Automated and microfluidic platforms are attracting laboratories that need higher throughput, less reagent consumption, and better reproducibility, while the ongoing preference for validated antibody-based techniques protects the core consumables business. Integration of artificial intelligence (AI) in antibody validation, tighter regulatory guidance on analytical robustness, and sustained life-sciences funding collectively anchor future growth for the Western blot market. Competitive pressure from multiplex immunoassays and mass-spectrometry-based approaches is intensifying, yet western blotting remains a benchmark method for confirming protein expression, post-translational modifications, and therapeutic product quality.

Global Western Blotting Market Trends and Insights

Rising Prevalence of Chronic Diseases

Cancer incidence climbed 58% in Europe between 1995 and 2022, creating sustained demand for protein biomarker confirmation in tumor biology and metabolic-disorder studies.Oncology research now requires the detection of low-abundance proteins and subtle post-translational changes, functions that western blotting supports reliably. The growing elderly population further enlarges case volumes for chronic conditions, reinforcing routine use of blot consumables and imaging reagents. As precision-medicine programs multiply, laboratories integrate automated blot platforms that handle higher throughput with minimal manual error. These patterns together lengthen the revenue runway for the Western blot market.

Expansion of Proteomics & Biomarker Discovery Pipelines

Large-scale proteomics initiatives are reshaping pharmaceutical discovery. Thermo Fisher Scientific's USD 3.1 billion purchase of Olink added more than 5,300 validated biomarker targets to its portfolio. Single-cell protein assays enabled by microfluidic western blotting now reveal heterogeneity that bulk analyses miss. AI-driven antibody screening accelerates candidate selection, cutting validation time and widening use cases. Rising sales of tandem-mass-tag reagents, up 18% to USD 4.01 million in 2024, indicate vigorous spending on complementary proteomics tools. These trends underpin continuous platform upgrades within the Western blot market.

Rapid Uptake of Alternative Immunoassay & Alpha Technologies

Parallel-reaction-monitoring mass spectrometry now offers antibody-free detection with enhanced sensitivity, directly challenging conventional immunoblotting. Multiplex platforms such as MSD, Luminex, and AlphaLISA permit simultaneous cytokine measurements with femtogram-level detection. These systems shorten assay time, simplify quantity, and align with high-throughput screening needs. Laboratories focused on speed and multiplexing migrate certain workflows away from western blotting, pressuring manufacturers to innovate with microfluidic chips and integrated imaging. While western blotting retains validation roles, the alternative technologies limit expansion in routine quantitation segments of the western blot market.

Other drivers and restraints analyzed in the detailed report include:

- Escalating Pharma / Biotech R&D Budgets

- Adoption of Automated & Microfluidic WB Platforms

- High Capital & Operating Cost of Western Blot Instruments & Antibodies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Consumables generated 65.2% of revenue in 2024, reflecting recurring sales of membranes, antibodies, buffers, and chemiluminescent substrates. This broad installed base secures stable cash flow for suppliers in the Western blot market. Automated and microfluidic instruments, while representing a smaller absolute revenue pool, are expanding at 8.12% CAGR to 2030 as users prioritize speed and low reagent footprints. Kit-based solutions further streamline workflows, lowering user variability and facilitating regulatory documentation. The segment's resilience resides in unavoidable consumable replacement cycles, regardless of platform sophistication.

Microfluidic devices reduce antibody usage to 1% of conventional volumes, trimming per-assay costs and easing supply constraints. Imaging systems now include embedded AI algorithms that assess band intensity, reducing interpretation subjectivity. Traditional wet-transfer equipment still serves academic labs where capital budgets limit the adoption of high-end automation. Gel and capillary electrophoresis modules continue to bridge sample preparation with downstream blotting, supporting overall western blot market continuity.

The Western Blotting Market is Segmented by Product (Instruments {Gel & Capillary Electrophoresis Systems and More} and Consumables), Application (Biomedical & Biochemical Research, Disease Diagnostics, and More), by End-User (Academia and Research Institutes, Biopharma Companies, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 42.0% of worldwide revenue in 2024, underpinned by mature research infrastructure, substantial biopharmaceutical R&D outlays, and rigorous regulatory oversight that values validated protein methods. The United States accounts for most sales, while Canada and Mexico contribute incremental gains through growing biotech clusters and clinical-trial activity. Government grants, venture capital flow, and an advanced supplier ecosystem foster early adoption of automated blot platforms, sustaining regional leadership.

Europe follows with well-established biotechnology hubs in Germany, the United Kingdom, France, and Switzerland. European regulators now demand reproducible analytics, reinforcing preferences for validated antibody sources and standard operating procedures. Switzerland's biotech network of more than 1,500 companies and 60,000 jobs illustrates how concentrated innovation feeds equipment demand. Markets such as Italy and Spain add volume via pharmaceutical manufacturing and university research, though budget constraints influence instrument penetration rates.

Asia Pacific is the fastest-growing territory, projected at an 8.80% CAGR through 2030. China's significant venture investments and state-sponsored life-sciences parks drive substantial procurement of blotting consumables and automated imaging systems. India accelerates adoption through government initiatives supporting translational research and domestic biologics production. Japan and South Korea leverage strong pharmaceutical bases and regulatory alignment with global standards to sustain replacement cycles. Australia and Southeast Asian countries, while smaller, are channeling grant funding toward proteomics facilities, strengthening regional participation in the western blot market. Collaborative models linking academia, government, and industry bolster infrastructure, ensuring long-term growth momentum.

List of Companies Covered in this Report:

- Thermo Fisher Scientific

- Bio-Rad Laboratories

- Danaher (Cytiva & ProteinSimple)

- Merck

- PerkinElmer

- LI-COR Biosciences

- Bio-Techne

- GE Healthcare

- Abcam

- Agilent Technologies

- Roche

- Azure Biosystems

- Rockland Immunochemicals

- Advansta Inc.

- GenScript Biotech

- RayBiotech Life

- ProteinSimple (Sartorius)

- Biovision

- Promega

- SignalChem Biotech

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Chronic Diseases

- 4.2.2 Expansion of Proteomics & Biomarker Discovery Pipelines

- 4.2.3 Escalating Pharma / Biotech R&D Budgets

- 4.2.4 Adoption of Automated & Microfluidic Wb Platforms

- 4.2.5 Ai-Driven Antibody Validation Workflows Boosting Western Blot Demand

- 4.2.6 Regulatory Focus on Reproducible Protein Data

- 4.3 Market Restraints

- 4.3.1 Rapid Uptake of Alternative Immunoassay & Alpha Technologies

- 4.3.2 High Capital & Operating Cost of Western Blot Instruments & Antibodies

- 4.3.3 Antibody Batch-To-Batch Variability Undermining Reproducibility

- 4.3.4 Laboratory Decarbonization Targets Favoring Low-Reagent Assays

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Instruments

- 5.1.1.1 Gel & Capillary Electrophoresis Systems

- 5.1.1.2 Traditional Wet / Semi-dry / Dry Blotting Systems

- 5.1.1.3 Automated & Microfluidic Platforms

- 5.1.1.4 Imagers

- 5.1.2 Consumables

- 5.1.2.1 Reagent and Buffers

- 5.1.2.2 Kits

- 5.1.1 Instruments

- 5.2 By Application

- 5.2.1 Biomedical & Biochemical Research

- 5.2.2 Disease Diagnostics

- 5.2.3 Agricultural & Food Safety Testing

- 5.3 By End-User

- 5.3.1 Academic & Research Institutes

- 5.3.2 Biopharma & Biotechnology Companies

- 5.3.3 Hospitals & Diagnostic Laboratories

- 5.3.4 CROs & Contract Testing Labs

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Thermo Fisher Scientific

- 6.3.2 Bio-Rad Laboratories

- 6.3.3 Danaher (Cytiva & ProteinSimple)

- 6.3.4 Merck KGaA (Millipore Sigma)

- 6.3.5 PerkinElmer

- 6.3.6 LI-COR Biosciences

- 6.3.7 Bio-Techne Corporation

- 6.3.8 GE Healthcare

- 6.3.9 Abcam plc

- 6.3.10 Agilent Technologies

- 6.3.11 Roche Diagnostics

- 6.3.12 Azure Biosystems

- 6.3.13 Rockland Immunochemicals

- 6.3.14 Advansta Inc.

- 6.3.15 GenScript Biotech

- 6.3.16 RayBiotech Life

- 6.3.17 ProteinSimple (Sartorius)

- 6.3.18 BioVision Inc.

- 6.3.19 Promega Corporation

- 6.3.20 SignalChem Biotech

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment