|

시장보고서

상품코드

1842560

전사체학 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global Transcriptomics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

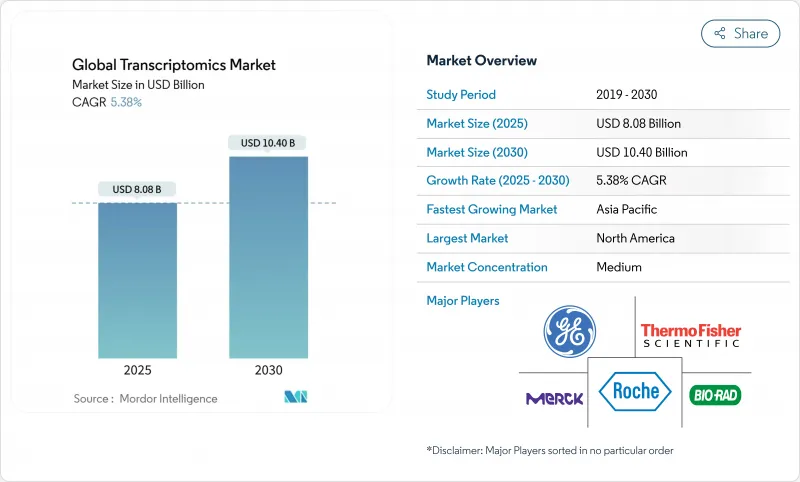

전사체학 시장 규모는 2025년에 80억 8,000만 달러로 추정되고, 2030년에는 104억 달러로 확대될 것으로 예상되며, 이는 안정적인 CAGR 5.38%로 성장할 전망입니다.

단기 성장은 종양학, 면역학 및 희귀질환 용도 분야에서 유전자 발현 프로파일링에 대한 임상 수요 증가로 인한 것이며, 장기적인 확장은 인공지능(AI)의 통합, 공간 시퀀싱의 진보, 광범위한 보험 상환의 채택으로 이어집니다. 단일 셀 RNA 시퀀싱(scRNA-seq)는 현재 수익의 거의 절반을 지원하지만, 실험실이 조직 구조의 컨텍스트를 추구함에 따라 공간 전사체학은 다른 모든 기술을 능가합니다. 북미에서는 성숙한 상환 경로가 리더십을 유지하는 한편, 아시아태평양에서는 국가가 지원하는 유전체학 이니셔티브와 임상시험 비용의 저하로부터 이익을 얻고 있습니다. 전사체학을 단백질체학 및 대사체학과 번들링하는 전략적 인수는 시장 개발이 단독 발현 플랫폼이 아니라 엔드 투 엔드 정밀의료 솔루션으로 축발을 옮긴다는 것을 시사합니다.

세계의 전사체학 시장 동향 및 인사이트

RNA-Seq 플랫폼의 급속한 보급

임상 실험실에서는 TruSight Oncology Comprehensive와 같은 분석이 2024년 FDA에서 승인됨에 따라 RNA 시퀀싱 워크플로우의 통합이 점점 더 진행되고, 상환의 확실성이 높아지며, 플랫폼의 보급이 가속화되고 있습니다. Oxford Nanopore과 Pacific Biosciences의 긴 리드 기술은 스플라이스 변형 검출을 해결하고 직접 RNA 시퀀싱의 판독 정확도 중앙값 98.8%를 보고했습니다. 2023년에 처음으로 임상 시퀀서의 수익이 연구 용도를 뛰어넘어 제조업체는 처리량보다 자동화 및 해석 소프트웨어를 중시하게 됩니다.

전사체학에 기초한 창약의 개척

제약회사는 scRNA-seq 데이터로부터 창약 타겟을 탐색하는 멀티오믹스 AI를 도입하여 개발 기간을 단축하고 있습니다. 공간 전사체학은 암 연구에 중요한 미세 환경 컨텍스트를 추가했고 FDA는 2024년 Omics Days 회의에서 바이오마커 검증 경로를 명확히 하고 투자에 박차를 가했습니다.

높은 플랫폼 및 소모품 비용

scRNA-seq의 실시에는 3,170달러에서 2만 5,540달러가 필요해, 연구조성금을 압박하고, 소규모 임상실험실의 의욕을 깎고 있습니다. 소모품은 플랫폼의 서비스 수명에 걸쳐 장비 비용을 초과하지만 공급업체 간의 경쟁이 제한되어 가격 하락은 완만합니다. 신규 진입의 엘리먼트 바이오사이언시스와 울티마 제노믹스는 보다 저비용의 케미스트리를 약속하고 있지만, 보급에는 아직 2년이 걸립니다. 임대와 서비스 모델은 자본 지출을 상쇄하는 데 도움이 되지만 수명주기 비용을 증가시키고 워크플로우의 유연성을 떨어 뜨립니다.

부문 분석

2024년의 전사체학 시장 점유율은 싱글셀 RNA 시퀀싱이 47.25%를 차지하였고, 벌크법에서는 간과되는 세포의 불균일성을 해결하는 역할이 강조되었습니다. 이 분야의 성숙을 통해 기술 혁신은 워크플로우의 처리량과 비용 절감을 향한 반면, 공간 플랫폼은 실험실이 조직 구조의 컨텍스트를 요구함에 따라 CAGR 6.45%로 성장할 전망입니다.

전사체학 시장은 scRNA-seq와 공간 바코딩을 융합시키고 분해능을 희생하지 않고 인사이트를 높이는 멀티모달 솔루션에 계속 기울고 있습니다. Long Lead Chemistry는 복잡한 이소형을 포착하여 종양학 및 신경학 조사 범위를 확장합니다. 마이크로어레이는 쇠퇴하고 있지만, 정량 PCR은 빠르고 낮은 플렉스 분석의 비계를 유지합니다. 따라서 공급업체는 다양한 수익원을 확보하기 위해 고 컨텐츠 검색 도구와 목표 임상 패널 간의 포트폴리오 균형을 유지합니다.

2024년에는 전사체학 시장 규모의 54.28%를 소모품이 차지하였고, 경상적인 현금 흐름을 보장하는 면도 모델의 위력이 강조되고 있습니다. 장비 매출은 핵심 기능이 공급업체간에 수렴함에 따라 감속하여 6.71%의 성장에 그쳤습니다.

소프트웨어 및 분석 서비스의 판매는 데이터가 복잡해짐에 따라 가속화되며, 전문 공급업체는 습식 실험실 시약을 초과하는 가치를 얻을 수 있습니다. 클라우드 네이티브 파이프라인은 고급 바이오인포매틱스를 민주화하지만 임상 등급 키트의 프리미엄 가격은 높은 마진을 유지합니다. 장비 설치 대수가 최상위 연구센터에서 포화 상태가 됨에 따라 소모품 공급업체는 신흥 시장과 중견 병원으로 축발을 옮겨 지역 예산에 맞게 키트의 크기와 가격대를 조정합니다.

지역 분석

2024년 전사체학 시장 점유율은 북미가 45.28%를 차지하였고, 풍부한 벤처 캐피탈, 밀집한 바이오파마 클러스터, 임상 검증을 촉진하는 FDA 동반진단 패스웨이 등이 그 요인이 되고 있습니다. Cancer Moonshot과 같은 민간 파트너십은 대규모 표현 아틀라스 프로젝트를 유지하며 국내 소모품 수요를 높게 유지하고 있습니다. 캐나다는 단일 지불 제도를 활용하여 집단 수준의 유전자 발현 연구를 실시하고, 멕시코는 비용의 저하와 임상시험의 활성화를 통해 제조 수탁 투자를 유치하고 있습니다.

아시아태평양의 CAGR은 7.29%로 중국의 수십억 달러 규모의 정밀의료 보조금과 일본의 공간 유전체 진단의 조기 도입이 뒷받침되고 있습니다. 인도의 위탁 조사 생태계는 방대한 환자 풀과 전사체학 엔드포인트를 점점 더 포함하는 비용 효율적인 시험을 결합합니다. 호주 정부가 자금을 제공하는 제노믹스 호주 프로그램은 트랜스레이셔널 오믹스 공동 연구를 장려하고 학술적 돌파구를 상업적 분석으로 이끌고 있습니다. 다양한 규제 체제는 기회인 동시에 장애이기도 하며 조기 승인을 제공하는 시장도 있고 현지에서 장기간의 검증을 요구하는 시장도 있습니다.

유럽에서는 Genome of Europe와 같은 프로젝트를 통해 기초 연구의 성과가 높게 유지되고 있지만, 일반 데이터 보호 규칙(GDPR(EU 개인정보보호규정))의 엄격한 규칙에 의해 신규 진단약의 임상 사용까지의 시간이 길어지고 있습니다. 독일, 영국, 프랑스는 확립된 상환 코드에 의해 지원되며 검사 건수를 독점하고 있습니다. 스위스와 네덜란드와 같은 소국은 높은 컨텐츠의 단일세포 분석과 플랫폼 통합 컨설팅을 전문으로 합니다. 브렉시트 후의 협력 체제는 데이터 교환의 계속을 보증해, 이 지역의 일관된 연구 개발 상황을 유지합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- RNA-Seq 플랫폼의 급속한 보급

- 전사체학에 기초한 창약의 확대

- 클라우드 네이티브 Ai 파이프라인에 의한 대규모 트랜스크립트 데이터 분석의 민주화

- 만성 질환의 부담 증가 및 정밀 진단 수요 증가

- 공간 및 단일 세포 전사체학의 출현

- 식량난 지역에서 아그리유전체학 프로그램

- 시장 성장 억제요인

- 높은 플랫폼 및 소모품 비용

- 바이오인포매틱스의 스킬 갭 및 데이터 처리의 복잡성

- 엄격한 데이터 프라이버시 및 임상 검증 규제

- 단일 세포 시약 공급 병목

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 기술별

- 마이크로어레이

- 실시간 정량 PCR(qPCR)

- 차세대 시퀀서(RNA-Seq)

- 단일 셀 RNA-Seq

- 공간 전사체학

- 인시츄 하이브리드화 및 기타 방법

- 제품별

- 소모품 및 시약

- 장치

- 소프트웨어 및 서비스

- 용도별

- 창약 및 의약품 개발

- 진단 및 질환 프로파일링

- 바이오마커 및 타겟 식별

- 농업 및 식물과학

- 기타

- 최종 사용자별

- 학술기관 및 연구기관

- 제약 및 바이오테크놀러지 기업

- 임상 및 진단 실험실

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Illumina Inc.

- Thermo Fisher Scientific

- 10x Genomics

- Agilent Technologies Inc.

- BGI Genomics

- Bio-Rad Laboratories Inc.

- NanoString Technologies

- Pacific Biosciences of California

- Qiagen NV

- F. Hoffmann-La Roche AG

- Merck KGaA(MilliporeSigma)

- PerkinElmer Inc.

- Standard BioTools(Fluidigm)

- Oxford Nanopore Technologies

- Dovetail Genomics

- Promega Corporation

- Guardant Health

- Takara Bio Inc.

- Danaher(Cytiva)

- Becton, Dickinson & Co.

제7장 시장 기회 및 전망

AJY 25.10.29The transcriptomics market size reached USD 8.08 billion in 2025 and is projected to expand to USD 10.40 billion by 2030, reflecting a steady 5.38% compound annual growth rate (CAGR).

Near-term growth stems from rising clinical demand for gene-expression profiling across oncology, immunology, and rare-disease applications, while longer-term expansion will be driven by artificial-intelligence (AI) integration, spatial sequencing advances, and broad reimbursement adoption. Single-cell RNA sequencing (scRNA-seq) underpins almost half of current revenues, yet spatial transcriptomics is outpacing all other technologies as laboratories seek tissue-architecture context. North America's mature reimbursement pathways sustain its leadership, whereas Asia-Pacific benefits from state-backed genomics initiatives and lower clinical-trial costs. Strategic acquisitions that bundle transcriptomics with proteomics and metabolomics signal a market pivot toward end-to-end precision-medicine solutions rather than stand-alone expression platforms.

Global Transcriptomics Market Trends and Insights

Rapid Adoption Of RNA-Seq Platforms

Clinical laboratories increasingly integrate RNA-sequencing workflows following 2024 FDA approvals of assays such as TruSight Oncology Comprehensive, creating reimbursement certainty and accelerating platform uptake . Long-read technologies from Oxford Nanopore and Pacific Biosciences have solved splice-variant detection, reporting median 98.8% read accuracy for direct RNA sequencing. Clinical sequencing revenues exceeded research use for the first time in 2023, pushing manufacturers to emphasize automation and interpretation software rather than throughput. The shift raises quality-control expectations but simultaneously unlocks premium pricing, reinforcing a recurring consumables model that underpins sustained transcriptomics market growth.

Expansion Of Transcriptomics-Based Drug Discovery

Pharmaceutical companies deploy multi-omics AI to mine scRNA-seq data for drug targets, cutting development timelines; Recursion Pharmaceuticals' approach exemplifies this trend. Spatial transcriptomics adds micro-environment context critical for oncology research, and FDA guidance from its 2024 Omics Days conference clarified biomarker-validation pathways, spurring investment. Resulting translational studies move expression biomarkers from discovery to pivotal trials faster, lifting demand for high-throughput sequencing reagents.

High Platform & Consumable Costs

A scRNA-seq run ranges from USD 3,170 to USD 25,540, straining research grants and discouraging small clinical labs. Consumables outpace instrument costs over a platform's life, yet limited supplier competition slows price declines. Emerging entrants Element Biosciences and Ultima Genomics promise lower-cost chemistries, but widespread adoption remains two years away. Leasing and service models help offset capital expenditure, though they raise lifecycle costs and reduce workflow flexibility.

Other drivers and restraints analyzed in the detailed report include:

- Rising Chronic Disease Burden & Precision Diagnostics Demand

- Emergence Of Spatial & Single-Cell Transcriptomics

- Bioinformatics Skill Gap & Data-Handling Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-cell RNA sequencing held 47.25% transcriptomics market share in 2024, underscoring its role in resolving cellular heterogeneity that bulk methods overlook . The segment's maturity redirects innovation toward workflow throughput and cost reduction, while spatial platforms record a 6.45% CAGR as laboratories seek tissue-structure context.

The transcriptomics market continues to tilt toward multimodal solutions that merge scRNA-seq with spatial barcoding, enhancing insight without sacrificing resolution. Long-read chemistries capture complex isoforms, broadening oncologic and neurologic study scope. Although microarrays fade, quantitative PCR maintains a foothold for rapid, low-plex assays. Vendors therefore balance portfolios between high-content discovery tools and targeted clinical panels to secure diverse revenue streams.

Consumables generated 54.28% of the transcriptomics market size in 2024, emphasizing the power of a razor-razorblade model that assures recurrent cash flow. Instrument sales slowed as core features converged across vendors, yielding only 6.71% growth.

Software and analytical-service revenues accelerate as data complexity grows, allowing specialized providers to capture value beyond wet-lab reagents. Cloud-native pipelines democratize advanced bioinformatics, yet premium prices for clinical-grade kits keep margins high. As the installed instrument base saturates top research centers, consumable vendors pivot to emerging markets and mid-tier hospitals, tailoring kit sizes and price points to local budgets.

The Transcriptomics Market Report Segments the Industry Into by Technology (Microarray, Real-Time Quantitative Polymerase Chain Reaction (Q-PCR), and More), by Product (Consumables, Instruments, and More), by Application (Diagnostics and Disease Profiling, Drug Discovery, and More), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 45.28% transcriptomics market share in 2024, anchored by abundant venture capital, dense biopharma clusters, and FDA companion-diagnostic pathways that encourage clinical validation. Public-private partnerships such as the Cancer Moonshot sustain large-scale expression-atlas projects, keeping domestic consumables demand high. Canada leverages a single-payer system to run population-level gene-expression studies, while Mexico lures contract-manufacturing investment through lower costs and rising clinical-trial activity.

Asia-Pacific posts a 7.29% CAGR, propelled by China's multi-billion-dollar precision-medicine grants and Japan's early adoption of spatial-omic diagnostics. India's contract-research ecosystem couples vast patient pools with cost-efficient trials that increasingly include transcriptomic endpoints. Australia's government-funded Genomics Australia program encourages translational-omics collaborations, funneling academic breakthroughs into commercial assays. Diverse regulatory regimes remain both opportunity and obstacle, with some markets offering accelerated approvals and others demanding prolonged local validation.

Europe maintains strong basic-research output through projects like Genome of Europe, yet stringent General Data Protection Regulation (GDPR) rules lengthen time-to-clinic for novel diagnostics. Germany, the United Kingdom, and France dominate test volumes, supported by established reimbursement codes. Smaller nations such as Switzerland and the Netherlands specialize in high-content single-cell analytics and platform integration consulting. Post-Brexit collaboration frameworks ensure continued data exchange, preserving the region's cohesive R&D landscape.

- Illumina

- Thermo Fisher Scientific

- 10x Genomics

- Agilent Technologies

- BGI

- Bio-Rad Laboratories

- NanoString Technologies

- Pacific Biosciences of California

- QIAGEN

- Roche

- Merck KGaA (MilliporeSigma)

- PerkinElmer

- Standard BioTools (Fluidigm)

- Oxford Nanopore Technologies

- Dovetail Genomics

- Promega

- Guardant Health

- Takara Bio

- Danaher

- Beckton Dickinson

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption Of RNA-Seq Platforms

- 4.2.2 Expansion Of Transcriptomics-Based Drug Discovery

- 4.2.3 Cloud-Native Ai Pipelines Are Democratizing Large-Scale Transcriptomic Data Analysis,

- 4.2.4 Rising Chronic Disease Burden & Precision Diagnostics Demand

- 4.2.5 Emergence Of Spatial & Single-Cell Transcriptomics

- 4.2.6 Agri-Genomics Programs In Food-Insecure Regions

- 4.3 Market Restraints

- 4.3.1 High Platform & Consumable Costs

- 4.3.2 Bioinformatics Skill Gap & Data-Handling Complexity

- 4.3.3 Stringent Data-Privacy / Clinical-Validation Regulations

- 4.3.4 Supply Bottlenecks For Single-Cell Reagents

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD Million)

- 5.1 By Technology

- 5.1.1 Microarray

- 5.1.2 Real-time Quantitative PCR (qPCR)

- 5.1.3 Next-Generation Sequencing (RNA-Seq)

- 5.1.4 Single-cell RNA-Seq

- 5.1.5 Spatial Transcriptomics

- 5.1.6 In-situ Hybridization & Other Methods

- 5.2 By Product

- 5.2.1 Consumables & Reagents

- 5.2.2 Instruments

- 5.2.3 Software & Services

- 5.3 By Application

- 5.3.1 Drug Discovery & Development

- 5.3.2 Diagnostics & Disease Profiling

- 5.3.3 Biomarker & Target Identification

- 5.3.4 Agriculture & Plant Science

- 5.3.5 Others

- 5.4 By End User

- 5.4.1 Academic & Research Institutes

- 5.4.2 Pharmaceutical & Biotechnology Companies

- 5.4.3 Clinical & Diagnostic Laboratories

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 Illumina Inc.

- 6.3.2 Thermo Fisher Scientific

- 6.3.3 10x Genomics

- 6.3.4 Agilent Technologies Inc.

- 6.3.5 BGI Genomics

- 6.3.6 Bio-Rad Laboratories Inc.

- 6.3.7 NanoString Technologies

- 6.3.8 Pacific Biosciences of California

- 6.3.9 Qiagen NV

- 6.3.10 F. Hoffmann-La Roche AG

- 6.3.11 Merck KGaA (MilliporeSigma)

- 6.3.12 PerkinElmer Inc.

- 6.3.13 Standard BioTools (Fluidigm)

- 6.3.14 Oxford Nanopore Technologies

- 6.3.15 Dovetail Genomics

- 6.3.16 Promega Corporation

- 6.3.17 Guardant Health

- 6.3.18 Takara Bio Inc.

- 6.3.19 Danaher (Cytiva)

- 6.3.20 Becton, Dickinson & Co.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment