|

시장보고서

상품코드

1842561

스텐트 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Stents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

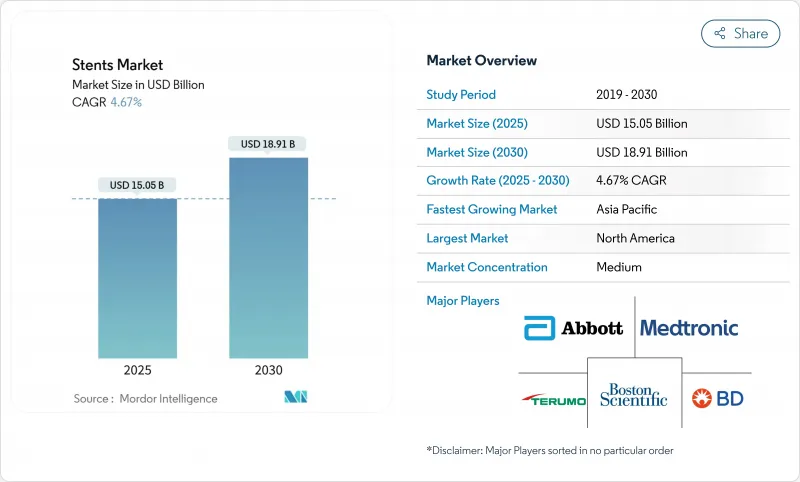

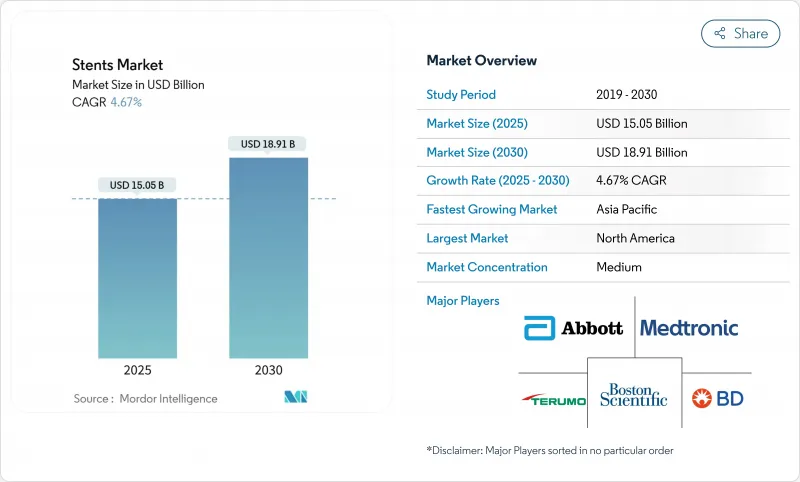

스텐트 시장의 2025년 시장 규모는 150억 5,000만 달러로 추정되고, 2030년에는 189억 1,000만 달러에 이를 전망이며, CAGR 4.67%로 확대될 것으로 예측됩니다.

관상 동맥 질환의 지속적인 기술, 저침습성 말초 인터벤션의 광범위한 채택, 꾸준한 제품 투입으로 매출은 증가 기조를 유지하고 있습니다. 주요 제조업체 간의 통합은 세계 전개 및 유통 효율을 향상시키고 의료 시스템의 외래 환경으로의 전환은 조달 역학을 재구성합니다. 조기 퇴원 및 일괄 지불에 대한 정책 당국의 지원은 재원 일수를 단축하는 장비의 구매를 가속화하고 병원 및 외래수술센터(ASC)의 스텐트 재고 업그레이드를 촉구합니다. 이와 병행하여 혈관의 크기 결정과 실시간 의사결정 지원을 위한 인공지능 도구는 이식의 정확성을 높이고, 비용이 많이 드는 합병증을 줄이며, 스텐트 시장의 장기 수요를 강화하고 있습니다.

세계의 스텐트 시장 동향 및 인사이트

관상 동맥 질환 및 말초 동맥 질환의 유병률 증가

말초 동맥 질환은 전 세계적으로 추정 2억-2억 5,000만 명이 앓고 있으며, 유병률은 지역차가 현저해, 북미의 5.6%에서 중남미의 14.5%까지 폭이 있습니다. 인구통계학적 고령화, 흡연율 및 고혈압률의 지속(각각 말초질환 위험의 45.6%와 35.1%를 차지함)에 의해 혈관 인터벤션의 후보자가 많이 존재합니다. 신흥국 진단 기술의 향상 및 의식의 고조에 따라 관상동맥과 말초 양쪽 스텐트에 대한 수요가 강화되어 스텐트 시장의 장기적인 성장 촉진요인으로 질병 만연이 자리잡고 있습니다.

경요골 PCI 및 데이 케이스 절차의 급속한 보급

경요골 동맥 접근의 채용률은 최근 조사 기간 동안 15.9%에서 69.1%로 상승하여 출혈 사건을 줄이고 당일 퇴원 프로토콜을 가능하게 했습니다. 미국 심장협회는 2025년 말초 인터벤션에 대한 경골 동맥 접근법을 승인하고 임상 용도의 폭을 넓혔습니다. 외래수술센터가 PCI에 과금하는 시설수는 2019년 30시설에서 2023년 65시설로 증가하여 입원 환자 설정에서의 이행을 실증하고 있습니다. 이러한 패턴은 외래 의료 제공업체들 사이에서 디바이스 수요를 가속화하고 스텐트 시장에서 가치 기반 케어의 이니셔티브를 강화하고 있습니다.

까다로운 다중 지역 승인 일정

FDA는 품질 시스템 규제 개정을 ISO 13485와 정합시키는 반면, 유럽에서는 의료기기 규제가 시행되고 시장 투입까지의 시간이 연장되기 때문에 제조업체는 다양한 규제 경로를 조정해야 합니다. 신흥국은 추가적인 임상 증거 요건을 도입하기 때문에 기업은 시가 시기를 어긋나게 하여 규정 준수 비용을 증가시킵니다. 강력한 규제 팀을 보유한 선도적인 기존 기업은 지연을 흡수할 수 있지만, 중소 혁신 기업은 스텐트 시장에 대한 새로운 진입을 지연시키는 장벽에 직면합니다.

부문 분석

관상동맥 스텐트는 다지 병변에서 수술 건수의 정착이 배경에 있으며, 2024년 스텐트 시장 점유율의 55.12%를 차지했습니다. 초박형 스트럿과 생분해성 폴리머를 특징으로 하는 약물 용출 모델은 여전히 기본 옵션이며, 베어 메탈 디자인은 더 짧은 기간의 이중 항혈소판 요법을 필요로 하는 틈새 요구를 충족합니다. 한편, 말초 스텐트는 장골 병변과 대퇴 무와 동맥 병변에 대한 치료 적응의 확대와 구부러진 해부학적 구조에서 장치의 추종성 향상으로 CAGR 7.34%의 성장이 예측됩니다. Abbott의 무릎 아래의 생체 흡수성 스캐 폴드의 FDA 승인은 말초 질환에서 '아무것도 남기지 않는' 선택에 대한 행운을 보여줍니다.

말초 인터벤션을 위한 스텐트 시장 규모는 신흥국에서의 검진 프로그램과 듀플렉스 초음파 검사의 가용성이 향상됨에 따라 꾸준히 확대될 것으로 예측됩니다. 복잡한 대동맥류용 스텐트 그래프트는 엔드리크의 위험을 줄이는 분기형이나 울타리 모양의 디자인으로 진화를 계속하고 있는 한편, 신경혈관의 흐름을 바꾸는 것은 경부의 넓은 동맥류용으로서 주목을 끌고 있습니다. 제조업체 각사는 친수성 코팅과 AI를 활용한 전개 피드백을 통합하여 어려운 혈관 영역에서의 치료 성적을 향상시키고 있습니다.

코발트 크롬 합금은 높은 반경방향 강도와 내식성을 제공하기 때문에 금속 생체재료가 스텐트 시장의 길거리골인 것을 계속해 2024년 매출의 63.24%를 차지했습니다. 가격에 민감한 분야에서는 스테인레스 스틸이 비용면에서 우위를 유지하고 있습니다. 그럼에도 불구하고 폴리머 스캐폴드는 CAGR 8.68%에서 가장 진보가 빠른 카테고리입니다. 이것은 만성 염증을 최소화하는 생분해성 솔루션에 대한 임상 열의를 반영합니다. 마그네슘 기반 구조물은 전임상 모델에서 스테인레스 스틸의 5.8%에 비해 2.8%의 혈소판 부착률을 나타내며, 보다 낮은 혈전 형성성을 보였습니다.

재조합 인간화 콜라겐과 같은 천연 생체 재료 코팅은 신속한 내피화를 촉진하고 약물을 사용하지 않는 장치에 대한 특수 틈새를 열 수 있습니다. 현재, 방출 제어 폴리머 매트릭스는 비계 흡수 및 약물 용출을 동기화할 수 있게 하고, 기계적 무결성에 대한 이전의 우려를 다루고 있습니다. 규모의 경제와 제조의 발전으로 인해 제조 비용이 계속 떨어지고 고급 폴리머 기구가 스텐트 시장의 주류 분야에 침투하는 데 도움이 될 것입니다.

지역 분석

북미의 스텐트 시장 규모는 2025년에 51억 9,000만 달러로 추정되며, 연간 50만 건의 PCI 수술, 세련된 카테터 실험실, AI 가이드 부착 사이징 툴의 조기 도입이 그 원동력이 되었습니다. 당일치기 PCI를 권장하는 호의적인 상환과 임상 지침 업데이트는 지속적인 장치 업데이트 사이클을 지원합니다. 캐나다의 국민 모두보험제도와 병원의 자본예산은 보다 신중하지만, 인구동태의 고령화 및 당뇨병 유병률의 상승으로 시술 건수는 증가하고 있습니다.

유럽에서는 MDR 준수를 통해 높은 제품 품질을 보장하고 각국의 의료 제도가 비용 효과적인 지표를 중시하기 때문에 매출은 한 자리수의 안정적인 성장을 보여줍니다. 독일, 프랑스, 영국은 여전히 가장 큰 지출국이며 남유럽과 동유럽 국가들은 EU 인프라 자금을 통해 카테라보 시설 업그레이드를 추진하고 있습니다. 서유럽 전체의 스텐트 시장 점유율은 가격 통제에 의해 억제되고 있지만, 가치 기반 조달은 이중 항혈소판 요법을 단축하고 재입원을 줄이는 기술에 보답하기 시작하고 있습니다.

아시아태평양은 향후 스텐트 수요에 가장 큰 기여를 하는 지역으로, 2024년에는 중국에서만 100만 건이 넘는 관동맥 인터벤션이 실시되었습니다. 혁신적인 의료기기의 현지 승인을 합리화하는 개혁에 의해 출시까지의 기간이 단축되고 있지만, 주마다의 카탈로그 가격 설정에 의해 마진의 압박 요인이 되고 있습니다. 인도의 국민보험제도는 PCI에 대한 접근을 확대하고 있으며, 일본은 급속한 고령화에 의해 폴리머를 포함하지 않는 초박형 스텐트의 프리미엄 가격을 유지하고 있습니다. 동남아시아 국가들은 심장센터의 규모를 확대하고 있으며 인도네시아와 베트남에서는 관민 파트너십이 인프라의 전개를 가속화하고 있습니다. 이러한 동향을 종합하면 아시아태평양은 스텐트 시장에서 가장 급성장하고 있는 지역이라고 할 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 관상동맥 질환 및 말초동맥 질환의 유병률 증가

- 경요골 PCI 및 당일치기의 급속한 보급

- 폴리머 프리데스 및 바이오솔버블로의 기술 변화

- AI 주도의 고정밀 사이징 및 전개 플랫폼

- 저침습 치료 및 혈관내 절차의 성장

- 고령화에 따른 생활 습관병 증가

- 시장 성장 억제요인

- 여러 지역에서의 엄격한 승인 스케줄

- 리콜 비용의 상승

- 약제 코팅 풍선에 대한 상환 갭의 축소

- 니켈 과민증의 소송 위험

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 제품별

- 관상동맥 스텐트

- 약제 용출 스텐트

- 베어 메탈 스텐트

- 생체 흡수성 스텐트

- 말초 스텐트

- 장골 스텐트

- 대퇴-무릎와 스텐트

- 신장 관련 스텐트

- 경동맥 스텐트

- 스텐트 이식편 및 임플란트

- 관상동맥 스텐트

- 재료별

- 금속계 생체 재료

- 고분자 생체 재료

- 천연 생체 재료

- 용도별

- 관상동맥 질환

- 말초동맥 질환

- 대동맥류

- 신경혈관 질환

- 소화관 폐색

- 비뇨기 폐색

- 호흡기기도 폐색

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 심장 카테터 검사실

- 전문 클리닉

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Abbott

- Boston Scientific

- Medtronic

- Becton, Dickinson & Co.

- B. Braun

- Terumo

- Biotronik

- MicroPort Scientific

- Cook Medical

- Elixir Medical

- Allium Medical

- Cordis

- Lepu Medical Technology

- Meril Life Sciences

- JenaValve Technology

- SMT

- SINOMED

- Alvimedica

- Endologix

제7장 시장 기회 및 전망

AJY 25.10.29The stents market is valued at USD 15.05 billion in 2025 and is forecast to reach USD 18.91 billion by 2030, expanding at a 4.67% CAGR.

Sustained procedure volumes in coronary artery disease, wider adoption of minimally invasive peripheral interventions and steady product launches are keeping revenue on an upward trajectory. Consolidation among leading manufacturers is improving global reach and distribution efficiency, while health-system migration toward outpatient settings is reshaping procurement dynamics. Policymaker support for early discharge and bundled payments is accelerating purchases of devices that shorten hospital stays, driving hospitals and ambulatory surgical centers to upgrade stent inventories. In parallel, artificial-intelligence tools for vessel sizing and real-time decision support are enhancing implantation accuracy and reducing costly complications, reinforcing long-term demand in the stents market.

Global Stents Market Trends and Insights

Increasing Prevalence of Coronary & Peripheral Arterial Disease

Peripheral arterial disease affects an estimated 200-250 million people worldwide and shows marked variation in regional prevalence, ranging from 5.6% in North America to 14.5% in South-Central Asia. Demographic aging and persistent smoking and hypertension rates-contributing 45.6% and 35.1% of peripheral disease risk respectively-are sustaining a large pool of candidates for vascular interventions. As diagnostics improve and awareness rises in emerging economies, demand for both coronary and peripheral stents strengthens, positioning disease prevalence as the prime long-term growth catalyst for the stents market.

Rapid Uptake of Transradial PCI & Day-Case Procedures

Transradial access adoption climbed from 15.9% to 69.1% across recent study periods, reducing bleeding events and enabling same-day discharge protocols. The American Heart Association endorsed transradial approaches for peripheral interventions in 2025, broadening clinical applications. Ambulatory surgical centers billing for PCI increased from 30 sites in 2019 to 65 in 2023, illustrating procedure migration away from inpatient settings.These patterns are accelerating device demand among outpatient providers and reinforcing value-based care initiatives in the stents market.

Stringent Multi-Region Approval Timelines

Manufacturers must reconcile divergent regulatory pathways as the FDA aligns Quality System Regulation amendments with ISO 13485 while Europe enforces Medical Device Regulation, extending time-to-market. Emerging countries introduce additional clinical evidence requirements, forcing companies to stagger launches and increasing compliance costs. Large incumbents with robust regulatory teams can absorb delays, but smaller innovators face barriers that may slow new entrants into the stents market.

Other drivers and restraints analyzed in the detailed report include:

- Technological Shift to Polymer-Free DES & Bioresorbables

- AI-Driven Precision Sizing & Deployment Platforms

- High and Rising Product Recall Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Coronary stents accounted for 55.12% of stents market share in 2024 on the back of entrenched procedure volumes in multivessel disease. Drug-eluting models featuring ultrathin struts and biodegradable polymers remain the default choice, while bare-metal designs fulfill niche needs that require shorter dual antiplatelet therapy. Peripheral stents, however, are forecast to grow at a 7.34% CAGR, driven by expanding treatment indications for iliac and femoropopliteal lesions and better device trackability in tortuous anatomy. Abbott's FDA nod for a bioresorbable scaffold below the knee illustrates momentum toward "leave nothing behind" options in peripheral disease.

The stents market size for peripheral interventions is projected to expand steadily as screening programs and duplex ultrasound accessibility improve in emerging economies. Stent grafts for complex aortic aneurysms continue to evolve with branched and fenestrated designs that reduce endoleak risk, while neurovascular flow-diverters capture attention for wide-necked aneurysms. Manufacturers are integrating hydrophilic coatings and AI-enabled deployment feedback to improve outcomes in difficult vascular territories.

Metallic biomaterials remained the backbone of the stents market, claiming 63.24% revenue in 2024 because cobalt-chromium alloys offer high radial strength and corrosion resistance. Stainless steel retains a cost advantage in price-sensitive segments. Nonetheless, polymeric scaffolds are the fastest-advancing category at an 8.68% CAGR, reflecting clinical enthusiasm for biodegradable solutions that minimize chronic inflammation. Magnesium-based constructs exhibit 2.8% platelet adherence versus 5.8% for stainless steel in preclinical models, indicating lower thrombogenicity.

Natural biomaterial coatings such as recombinant humanized collagen foster rapid endothelialization and are likely to carve out specialized niches for drug-free devices. Controlled-release polymer matrices now enable synchronized drug elution with scaffold resorption, addressing previous concerns over mechanical integrity. Economies of scale and manufacturing advances will continue to lower production costs, helping premium polymeric devices penetrate mainstream segments of the stents market.

The Stents Market Report is Segmented by Product (Coronary Stents [Drug-Eluting Stents and More], Peripheral Stents, and Stent Grafts & Implants), Material (Metallic Biomaterials, Polymeric Biomaterials, and More), Application (Coronary Artery Disease, Peripheral Artery Disease and More), End User (Hospitals, Ambulatory Surgical Centers and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's stents market size stood at USD 5.19 billion in 2025, driven by 500,000 annual PCI procedures, sophisticated catheter laboratories and early adoption of AI-guided sizing tools. Favorable reimbursement and clinical guideline updates that endorse day-case PCI support continuous device refresh cycles. Canada's universal coverage and hospital capital budgets are more measured, yet procedure volumes benefit from aging demographics and rising diabetes prevalence.

Europe displays steady single-digit revenue growth as MDR compliance ensures high product quality and as national health systems favour cost-effectiveness metrics. Germany, France and the United Kingdom remain top spenders, while Southern and Eastern European countries are upgrading cath-lab fleets through EU infrastructure funds. The stents market share across Western Europe is tempered by price controls, but value-based procurement is beginning to reward technologies that shorten dual antiplatelet therapy and reduce rehospitalization.

Asia-Pacific is the largest incremental contributor to future unit demand, with China alone performing over 1 million coronary interventions in 2024. Reforms streamlining local approval for innovative devices are shortening launch timelines, although province-specific catalog pricing creates margin pressures. India's national insurance scheme broadens access to PCI, while Japan maintains premium pricing for polymer-free and ultra-thin stents due to rapid ageing. Southeast Asian nations are scaling cardiac centers, and public-private partnerships in Indonesia and Vietnam are accelerating infrastructure deployment. Collectively, these trends anchor Asia-Pacific as the fastest-growing region within the stents market.

- Abbott Laboratories

- Boston Scientific

- Medtronic

- Beckton Dickinson

- B. Braun

- Terumo

- BIOTRONIK

- MicroPort

- Cook Group

- Elixir Medical

- Allium Medical

- Cordis

- Lepu Medical

- Meril Life Sciences

- JenaValve Technology

- SMT

- SINOMED

- Alvimedica

- Endologix

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence Of Coronary & Peripheral Arterial Disease

- 4.2.2 Rapid Uptake Of Transradial PCI & Day-Case Procedures

- 4.2.3 Technological Shift To Polymer-Free Des & Bioresorbables

- 4.2.4 AI-Driven Precision Sizing & Deployment Platforms

- 4.2.5 Growth in Minimally-Invasive Therapies and Endovascular Procedures

- 4.2.6 Rising Burden of Lifestyle-Related Disorders Coupled with Aging Population

- 4.3 Market Restraints

- 4.3.1 Stringent Multi-Region Approval Timelines

- 4.3.2 High And Rising Product Recall Costs

- 4.3.3 Shrinking Reimbursement Gap Vs. Drug-Coated Balloons

- 4.3.4 Nickel-Hypersensitivity Litigation Risk

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Product

- 5.1.1 Coronary Stents

- 5.1.1.1 Drug-eluting Stents

- 5.1.1.2 Bare-metal Stents

- 5.1.1.3 Bioabsorbable Stents

- 5.1.2 Peripheral Stents

- 5.1.2.1 Iliac Stents

- 5.1.2.2 Femoral-Popliteal Stents

- 5.1.2.3 Renal & Related Stents

- 5.1.2.4 Carotid Stents

- 5.1.3 Stent Grafts & Implants

- 5.1.1 Coronary Stents

- 5.2 By Material

- 5.2.1 Metallic Biomaterials

- 5.2.2 Polymeric Biomaterials

- 5.2.3 Natural Biomaterials

- 5.3 By Application

- 5.3.1 Coronary Artery Disease

- 5.3.2 Peripheral Artery Disease

- 5.3.3 Aortic Aneurysm

- 5.3.4 Neurovascular Disease

- 5.3.5 Gastrointestinal Obstruction

- 5.3.6 Urological Obstruction

- 5.3.7 Respiratory Airway Obstruction

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Cardiac Catheterization Labs

- 5.4.4 Specialty Clinics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Abbott

- 6.3.2 Boston Scientific

- 6.3.3 Medtronic

- 6.3.4 Becton, Dickinson & Co.

- 6.3.5 B. Braun

- 6.3.6 Terumo

- 6.3.7 Biotronik

- 6.3.8 MicroPort Scientific

- 6.3.9 Cook Medical

- 6.3.10 Elixir Medical

- 6.3.11 Allium Medical

- 6.3.12 Cordis

- 6.3.13 Lepu Medical Technology

- 6.3.14 Meril Life Sciences

- 6.3.15 JenaValve Technology

- 6.3.16 SMT

- 6.3.17 SINOMED

- 6.3.18 Alvimedica

- 6.3.19 Endologix

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment