|

시장보고서

상품코드

1842567

의료용 임플란트 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Medical Implants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

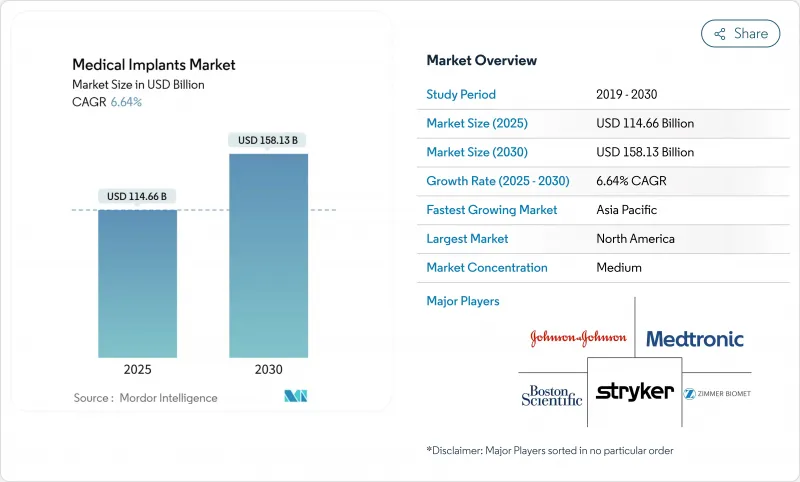

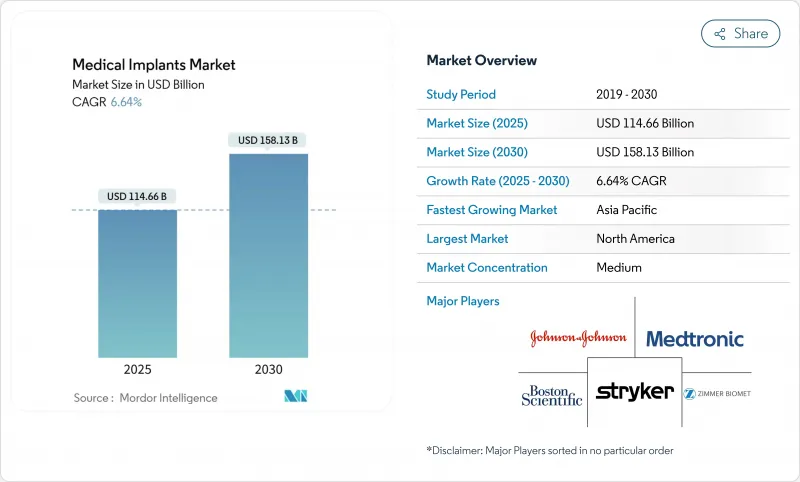

의료용 임플란트 시장의 규모는 2025년에 1,146억 6,000만 달러로 추정되고, 2030년에는 1,581억 3,000만 달러에 이를 것으로 예측되며, 예측 기간(2025-2030년)의 CAGR은 6.64%로 예상됩니다.

고령화, 만성질환 부담 확대, 꾸준한 기술 도입으로 인한 지속적인 수요는 비용과 규제의 압력이 계속되고 있음에도 불구하고 성장세로 이어지고 있습니다. 스마트 센서 대응 기기, 3D 프린팅 부품, 신흥국에서의 액세스 확대가 경쟁 역학을 재구성하고 있는 한편, 엄격한 승인 프로세스를 극복하고 비용 대비 효과를 증명할 수 있는 제조업체는 의료용 임플란트 시장에서 큰 이익을 획득하는 입장에 있습니다.

세계의 의료용 임플란트 시장의 동향과 인사이트

고령화와 만성질환 부담 증가

2030년까지 5명 중 1명이 60세 이상이 되기 때문에 정형외과용 관절, 심장혈관용기구, 치과용 보철물에 대한 수요가 가속화되고 있습니다. 골관절염과 심장병의 유병률 증가가 수술 건수를 밀어 올리고 있으며, 지불자는 보다 많은 사례 수에 대응하기 위해 환급 정책을 갱신하도록 촉구하고 있습니다. 100일간의 가정 요양이 필요한 티타늄 인공 심장과 같은 기술 혁신은 차세대 임플란트가 어떻게 복잡한 노인들의 요구에 부응하는지를 보여줍니다. 따라서 의료 시스템의 입안자는 인구 역학의 기세가 의료용 임플란트 시장의 장기적인 기폭제가 될 것으로 보고 있습니다.

기술 진보 : 생체 흡수성 재료 및 스마트 임플란트

치유가 완료되면 용해되는 생체 흡수성 스캐폴드는 연률 7.63%로 성장하여 재수술을 줄이고 있습니다. 또한 무선 원격 측정의 병렬 발전으로 관절의 각도와 하중을 실시간으로 보고하는 Wi-Fi 지원 무릎 관절 시스템이 개발되었습니다. 폐쇄 루프 신경 자극기 및 형상 기억 3D 인쇄 구조물은 재료 과학과 디지털 통합이 결과를 향상시키는 방법을 더욱 입증합니다. 이러한 솔루션이 승인됨에 따라 의료용 임플란트 시장의 지원 가능한 기반이 확대되고 있습니다.

규제 당국의 심사 강화 및 승인 시기의 장기화

FDA의 2026년 품질시스템 대개혁과 영국의 브렉시트 후의 서베일런스 규칙에 의해 문서화의 레이어가 늘어나고 출시가 지연됩니다. 소규모 개발 기업은 파이프라인의 진행을 방해할 수 있는 규모 중심의 컴플라이언스 비용에 직면하고 승인이 대기업에 집중되면서 의료용 임플란트 시장의 단기적인 확대가 다소 억제될 수 있습니다.

부문 분석

2024년 의료용 임플란트 시장의 36.22%를 정형외과용 기기가 차지하였으며, 이는 고관절과 무릎 관절의 대체 수요에 의해 뒷받침되고 있습니다. 치과용 시스템은 규모가 작고, 아시아태평양에서의 심미 의식의 고조와 중산층의 지출 확대에 의해 CAGR 8.65%를 상회할 것으로 예측됩니다. 고강도 지르코니아제 어버트먼트나 배치 유도 기술 등의 기술 혁신은 성공률을 높여 진료 시간을 단축합니다. 의료용 임플란트 시장에서 치과 솔루션의 규모는 빠르게 확대될 것으로 예측되며, 전문 클리닉은 97.29%의 성공률을 활용하여 선택적 흡수를 촉진하고 있습니다. 제조업체 각사는 이 기세를 받아들이기 위해, 치아에 매립하는 솔루션에의 포트폴리오 투자를 실시했습니다.

정형외과 분야에서는 입증된 티타늄과 코발트 크롬 플랫폼이 계속 주도권을 잡고 있지만, 2024년에 인가된 ROSA 숄더 시스템으로 대표되는 로봇 지원 수술은 정밀도 향상과 절개 창의 축소를 실현하고 있습니다. 근골격계 질환의 지속적인 유행은 기술의 업데이트 사이클과 함께 정형외과의 수익원을 확보하고 있습니다. 심장혈관, 안과 및 유방의 각 범주는 보다 광범위한 의료용 임플란트 시장에서 순환적인 노출을 완화하고 추가적인 다양화를 가져옵니다.

금속 생체재료는 비교할 수 없는 내하중 강도로 2024년 의료용 임플란트 시장에서 45.13%의 점유율을 유지했습니다. 티타늄과 코발트 크롬 합금은 수십 년에 걸친 임상 증거에 힘입어 고관절, 무릎 관절 및 스텐트에서 여전히 주요 소재입니다. 그러나, 생체흡수성 폴리머는 CAGR 7.63%로 확대되어, 장기간의 이물 혼입이 바람직하지 않은 수요를 메우고 있습니다. 생체 흡수성 의료용 임플란트 시장 규모는 불규칙한 골 결손에 적합하고 면역 반응을 조절하는 NIR 프로그래밍 형상 기억 PLA/PCL 스캐폴드 등의 획기적인 기술로 인해 혜택을 받고 있습니다.

폴리머와 세라믹 분야는 중간 영역의 중요한 틈새를 차지합니다. 약물 용출성 폴리머 매트릭스와 내마모성 알루미나 치관은 독특한 성능 상 이점을 제공합니다. 한편 특수 신흥기업은 흡수성과 구조적 무결성을 융합시킨 하이브리드 복합재를 개발하여 파괴적인 참가자로 자리매김하고 있습니다. 규제 당국의 관행이 개선됨에 따라 천연 소재의 채용이 가속화되고 의료용 임플란트 시장에서의 설계 가능성이 확산됨과 동시에 금속의 점유율이 점차 낮아질 전망입니다.

지역 분석

북미는 2024년 세계 매출의 41.41%를 차지하였으며 견조한 보험 적용, 기술 혁신 자금, 2023년 3,326건의 FDA 510(k) 인가에 의해 뒷받침되고 있습니다. 치과용 및 골판용 장치에 대한 최근 지침 초안은 파이프라인의 보충을 촉진하고 그 경로를 더욱 명확하게 하고 있습니다. 고령화된 집단의 지속적인 대체 수요로 인해 수술 건수가 계속 증가하고 이 지역의 의료용 임플란트 시장에서의 핵심 역할이 강화됩니다.

아시아태평양의 CAGR은 2025년부터 2030년까지 7.84%에 이를 것으로 예측됩니다. 인도에서는 새롭게 5개의 AIIMS가 개설되는 등 다층적인 병원 건설이 진행되고 있으며, 고급 수술 능력이 강화되고 있습니다. 중국의 '건강 2030' 개혁은 장비 심사의 합리화와 시판 후 모니터링을 우선시하고 관료적인 시간 지연을 줄이는 한편 품질을 강화하고 있습니다. 규제의 유연성은 가격 경쟁력있는 임상 서비스와 함께 이 지역을 의료용 임플란트 시장 수요 및 제조 허브로 자리 잡고 있습니다.

유럽은 국민 모두를 위한 보험 제도와 높은 만성 질환 이환율에 의해 여전히 중요한 공헌을 하고 있습니다. 인구의 21.3%가 65세 이상의 노인이기 때문에 정형외과 및 심장 판막에 대한 수요가 지속되고 있습니다. 폴리머 밸브 플랫폼에 대한 연구로 장기적인 내구성 전망이 높아지고 있습니다. 동시에 EU 의료기기 규제의 시행에 의해 컴플라이언스 기준치가 인상되어 일시적인 매출 하락에도 불구하고 결국에는 제품의 안전성이 확보되게 됩니다. 이러한 요소는 의료용 임플란트 시장에서 유럽의 전략적 관련성을 유지합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 도입

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 고령화와 만성질환 부담 증가

- 선택적 미용 치과 처치의 급증

- 의료용 임플란트의 기술 진보

- 저침습 외래 임플란트 치료로의 시프트에 의한 입원 기간의 단축

- 건강 관리 인프라 개발 및 의료 관광

- 3D 프린팅의 보급

- 시장 성장 억제요인

- 주요 시장의 규제 강화와 승인 기간의 장기화

- 높은 비용과 한정된 환급

- 환자나 외과의를 주저하게 만드는 과거의 제품 리콜

- 고급 임플란트에 대한 제한된 환급 정책

- 규제 전망

- 기술적 전망

- Porter's Five Forces 분석

- 구매자의 협상력

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측(금액, 수량)

- 제품별

- 정형외과 임플란트

- 고관절 정형외과용 기기

- 무릎 정형외과용 기기

- 척추정형외과용 기기

- 관절 재건

- 기타 정형외과 제품

- 심장혈관 임플란트

- 페이싱 디바이스

- 스텐트

- 심장 구조 임플란트

- 안과 임플란트

- 안내 렌즈

- 녹내장 임플란트

- 치과 임플란트

- 안면 임플란트

- 유방 임플란트

- 기타 임플란트

- 정형외과 임플란트

- 재료유형별

- 금속 생체 재료

- 폴리머 생체 재료

- 세라믹 생체 재료

- 천연/생체 흡수성 생체 재료

- 기술별

- 기존 임플란트

- 3D 프린팅/적층 조형 임플란트

- 스마트 센서 탑재 임플란트

- 최종 사용자별

- 병원

- 전문 클리닉

- 외래수술센터(ASC)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Johnson & Johnson(DePuy Synthes, Ethicon, Mentor)

- Medtronic plc

- Stryker Corporation

- Zimmer Biomet Holdings

- Abbott Laboratories

- Boston Scientific Corporation

- BIOTRONIK SE & Co. KG

- CONMED Corporation

- Globus Medical, Inc.

- Integra LifeSciences Holdings

- Smith Nephew plc

- Institut Straumann AG

- Dentsply Sirona

- Osstem Implant Co., Ltd.

- GC Aesthetics

- Arthrex, Inc.

- Cook Medical

- B. Braun SE

- uteshiyamedicare

- gpcmedical.com

제7장 시장 기회와 전망

CSM 25.11.03The medical implants market size is estimated at USD 114.66 billion in 2025, and is expected to reach USD 158.13 billion by 2030, at a CAGR of 6.64% during the forecast period (2025-2030).

Persistent demand from an aging population, expanding chronic disease burden, and steady technology adoption underpin this growth path despite ongoing cost and regulatory pressures. Smart-sensor-enabled devices, 3-D printed components, and widening access in emerging economies are reshaping competitive dynamics, while manufacturers capable of navigating stringent approval processes and proving cost-effectiveness are positioned to capture outsized gains in the medical implants market.

Global Medical Implants Market Trends and Insights

Aging Population & Higher Chronic Disease Burden

Demand for orthopedic joints, cardiovascular devices, and dental prosthetics is accelerating as 1 in 5 people will be over 60 by 2030. Higher prevalence of osteoarthritis and heart disease is pushing procedure volumes upward, prompting payers to update reimbursement policies to accommodate larger case loads. Innovations such as the titanium artificial heart that kept a patient home for 100 days illustrate how next-generation implants meet complex geriatric needs. Health-system planners therefore view demographic momentum as a long-run catalyst for the medical implants market.

Technological Advancements: Bioresorbable Materials and Smart Implants

Bioresorbable scaffolds that dissolve when healing is complete are growing at 7.63% annually and reducing revision surgeries. Parallel advances in wireless telemetry have produced Wi-Fi-enabled knee systems that report joint angles and load in real time. Closed-loop neurostimulators and shape-memory 3-D printed constructs further demonstrate how materials science and digital integration enhance outcomes. As these solutions gain approval, they are enlarging the addressable base for the medical implants market.

Intensifying Regulatory Scrutiny & Prolonged Approval Timelines

The FDA's 2026 quality-system overhaul and post-Brexit surveillance rules in the United Kingdom add documentation layers and delay launches. Smaller developers face scale-driven compliance costs that may impede pipeline progress, concentrating approvals among larger firms and slightly tempering short-term expansion of the medical implants market.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Minimally Invasive & Outpatient Implant Procedures

- Healthcare Infrastructure Development & Medical Tourism

- High Cost & Limited Reimbursement

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Orthopedic devices generated 36.22% of the medical implants market in 2024, supported by hip and knee replacement demand. Dental systems, though smaller, are forecast to outpace with an 8.65% CAGR, lifted by higher esthetic awareness and expanding middle-class spending in Asia Pacific. Innovations such as high-strength zirconia abutments and navigated placement techniques raise success rates and shorten chair time. The medical implants market size for dental solutions is projected to widen rapidly, with specialty clinics leveraging 97.29% success statistics to promote elective uptake. Manufacturers are tailoring portfolio investments toward tooth-borne solutions to capture this momentum.

Continued orthopedic leadership stems from proven titanium and cobalt-chromium platforms, but robotic-assisted procedures, exemplified by the ROSA Shoulder System cleared in 2024, are delivering precision gains and smaller incisions. Sustained musculoskeletal disease prevalence, combined with technology refresh cycles, secures orthopedic revenue streams even as dental outgrows. Cardiovascular, ophthalmic, and breast categories provide incremental diversification, buffering cyclical exposure within the broader medical implants market.

Metallic biomaterials retained 45.13% share of the medical implants market in 2024 due to unmatched load-bearing strength. Titanium and cobalt-chromium alloys remain primary in hips, knees, and stents, supported by decades of clinical evidence. However, bioresorbable polymers are expanding at 7.63% CAGR, closing gaps where long-term foreign bodies are undesirable. The medical implants market size for bioresorbables is benefiting from breakthroughs such as NIR-programmable shape-memory PLA/PCL scaffolds that conform to irregular bone defects and modulate immune response.

Polymer and ceramic segments occupy vital mid-spectrum niches. Drug-eluting polymer matrices and wear-resistant alumina dental crowns afford unique performance advantages. Meanwhile, specialty start-ups are engineering hybrid composites that blend resorption with structural integrity, positioning themselves as disruptive entrants. As regulatory familiarity improves, natural material adoption should accelerate, gradually eroding metallic share while broadening design possibilities within the medical implants market.

The Medical Implants Market Report is Segmented by Product (Orthopedic Implants, Cardiovascular Implants, Ophthalmic Implants, Dental Implants, and More), Type of Material (Metallic Biomaterial, Polymers Biomaterial, and More), Technology (Conventional Implants and More), End User (Hospitals, and More) and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

North America contributed 41.41% of global revenue in 2024, underpinned by robust insurance coverage, innovation funding, and 3,326 FDA 510(k) clearances in 2023. Recent draft guidance on dental and bone-plate devices further clarifies pathways, encouraging pipeline replenishment. Continued replacement demand among aging cohorts keeps procedure volumes elevated, reinforcing the region's anchor role in the medical implants market.

Asia Pacific is projected to deliver a 7.84% CAGR between 2025-2030. India's multilayer hospital build-out, including five new AIIMS sites, is boosting advanced surgery capacity. China's Healthy China 2030 reforms prioritize streamlined device reviews and post-market vigilance, trimming bureaucratic lag while tightening quality. Regulatory flexibility, combined with price-competitive clinical services, positions the region as both demand and manufacturing hub for the medical implants market.

Europe remains a vital contributor owing to universal coverage structures and high chronic disease prevalence. With 21.3% of the population aged 65 or older, demand for orthopedic and heart valves persists. Research into polymeric valve platforms is elevating long-term durability prospects. Concurrently, implementation of the EU Medical Device Regulation raises compliance thresholds, modestly tempering near-term launches but ultimately ensuring product safety. These elements sustain Europe's strategic relevance in the medical implants market.

- Johnson & Johnson (DePuy Synthes, Ethicon, Mentor)

- Medtronic

- Stryker

- Zimmer Biomet

- Abbott Laboratories

- Boston Scientific

- BIOTRONIK

- Conmed

- Globus Medical

- Integra LifeSciences Holdings

- Smith+Nephew plc

- Straumann Group

- Dentsply Sirona

- Osstem Implant Co., Ltd.

- GC Aesthetics

- Arthrex

- Cook Group

- B. Braun

- uteshiyamedicare

- gpcmedical.com

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ageing Population & Higher Chronic Disease Burden

- 4.2.2 Surge in Elective Cosmetic & Dental Procedures

- 4.2.3 Technological Advancements in the Medical Implants

- 4.2.4 Shift Toward Minimally Invasive & Outpatient Implant Procedures Reducing Hospital Stay

- 4.2.5 Healthcare Infrastructure Development & Medical Tourism

- 4.2.6 Growing Popularity of 3D Printing

- 4.3 Market Restraints

- 4.3.1 Intensifying Regulatory Scrutiny & Prolonged Approval Timelines Across Major Markets

- 4.3.2 High Cost & Limited Reimbursement

- 4.3.3 Historical Product Recalls Fueling Patient & Surgeon Hesitancy

- 4.3.4 Limited Reimbursement Policies for Advanced Implants

- 4.4 Regulatory Outlook

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value & Volume)

- 5.1 By Product

- 5.1.1 Orthopedic Implants

- 5.1.1.1 Hip Orthopedic Devices

- 5.1.1.2 Knee Orthopedic Devices

- 5.1.1.3 Spine Orthopedic Devices

- 5.1.1.4 Joint Reconstruction

- 5.1.1.5 Other Orthopedic Products

- 5.1.2 Cardiovascular Implants

- 5.1.2.1 Pacing Devices

- 5.1.2.2 Stents

- 5.1.2.3 Structural Cardiac Implants

- 5.1.3 Ophthalmic Implants

- 5.1.3.1 Intraocular Lens

- 5.1.3.2 Glaucoma Implants

- 5.1.4 Dental Implants

- 5.1.5 Facial Implants

- 5.1.6 Breast Implants

- 5.1.7 Other Implants

- 5.1.1 Orthopedic Implants

- 5.2 By Type of Material

- 5.2.1 Metallic Biomaterials

- 5.2.2 Polymer Biomaterials

- 5.2.3 Ceramic Biomaterials

- 5.2.4 Natural / Bioresorbable Biomaterials

- 5.3 By Technology

- 5.3.1 Conventional Implants

- 5.3.2 3-D Printed / Additive Manufactured Implants

- 5.3.3 Smart Sensor-Enabled Implants

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Specialty Clinics

- 5.4.3 Ambulatory Surgical Centers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Johnson & Johnson (DePuy Synthes, Ethicon, Mentor)

- 6.3.2 Medtronic plc

- 6.3.3 Stryker Corporation

- 6.3.4 Zimmer Biomet Holdings

- 6.3.5 Abbott Laboratories

- 6.3.6 Boston Scientific Corporation

- 6.3.7 BIOTRONIK SE & Co. KG

- 6.3.8 CONMED Corporation

- 6.3.9 Globus Medical, Inc.

- 6.3.10 Integra LifeSciences Holdings

- 6.3.11 Smith+Nephew plc

- 6.3.12 Institut Straumann AG

- 6.3.13 Dentsply Sirona

- 6.3.14 Osstem Implant Co., Ltd.

- 6.3.15 GC Aesthetics

- 6.3.16 Arthrex, Inc.

- 6.3.17 Cook Medical

- 6.3.18 B. Braun SE

- 6.3.19 uteshiyamedicare

- 6.3.20 gpcmedical.com

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment