|

시장보고서

상품코드

1842572

리드 센서 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Reed Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

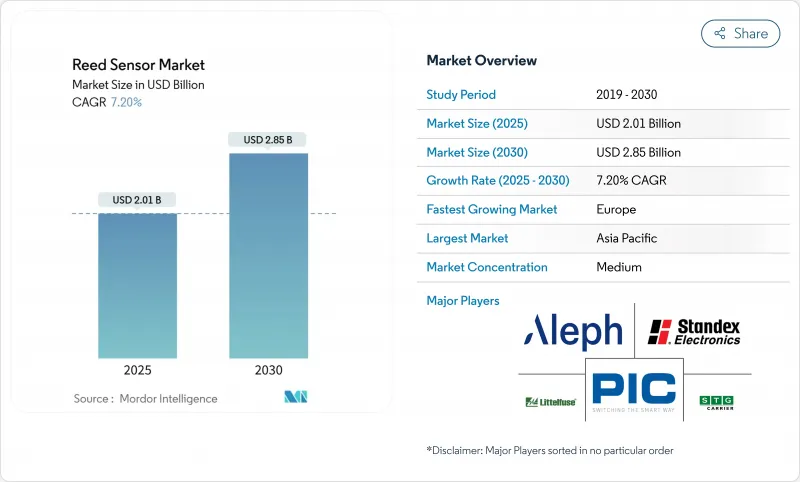

리드 센서 시장의 규모는 2025년에 20억 1,000만 달러로 추정되고, 2030년에는 28억 5,000만 달러에 이를 것으로 예측되며, 예측 기간(2025-2030년)의 CAGR은 7.20%로 예상됩니다.

전기자동차 배터리 팩, 수소 연료전지 스택 및 실외 스마트 미터 인클로저의 본질 안전 방폭형 스위칭에 대한 수요가 증가함에 따라 이러한 확대가 지원됩니다. 리드 센서 시장은 스파크 프리 동작, 대기 시간 소비 전력 제로, 가혹한 조건 하에서 20년에 걸쳐 입증된 현장 신뢰성을 제공함으로써 솔리드 스테이트 홀이나 TMR의 대체품에 대항하여 틈새를 지키고 있습니다. 아시아태평양은 여전히 생산의 견인 역할을 하지만, 재생에너지 및 기능 안전에 대한 유럽 규제의 뒷받침이 이 지역의 급성장을 견인하고 있습니다. 경쟁의 심각성은 중간 정도이며 세계 리더는 규모, 수직 통합 유리 가공, 나노구조 접점 등의 재료 혁신을 활용하여 제품 수명 연장과 비용 절감을 도모하고 있습니다.

세계의 리드 센서 시장의 동향과 인사이트

저전력 스마트 그리드 미터 급증

레거시 미터를 20년간 유지보수가 필요 없는 스마트 장치로 대체하는 유틸리티 기업은 자기 작동으로 인한 대기 전력이 0인 펄스 카운트용 리드 스위치를 점점 도입하고 있습니다. 밀폐형 실링은 실외 케이스의 응축을 방지하고 -40°C - 85°C 범위에서 수명을 연장합니다. Gridpertise와 같은 기업의 대규모 배포는 현재 1억 800만 유닛을 넘어서고 있으며 리드 기반 설계의 확장성을 뒷받침하고 있습니다. 폴란드의 Tauron Dystrybucja는 자기 펄스의 무결성에 의존하는 자동 판독을 통해 이미 560만 건의 고객을 관리하고 있습니다. 2030년까지 계속되는 송전망의 디지털화는 배터리 독립적인 견고한 스위칭에 대한 수요를 유지합니다.

EV 배터리 관리 채택

전기자동차 및 수소 자동차에 장착된 배터리 팩에는 스파크 프리 신뢰성 위치 감지 및 누출 감지가 필요합니다. 콘티넨탈의 e-Motor 로터 온도 센서는 온도 오차를 3°C로 억제하여 자석 최적화로 인한 효율을 향상시킵니다. Honeywell의 전해액 누설 센서는 발화원을 피하기 위해 밀폐 접점을 사용하여 열 폭주 이벤트에 대해 20분간 경고 창을 제공합니다. Marquardt는 수소 전지의 전압 모니터에 리드 소자를 적용하여 치명적인 고장 전에 H2 누설을 제어합니다. EV의 보급이 가속되면 리드 센서 시장의 CAGR은 2.1포인트 상승할 전망입니다.

솔리드 스테이트 센서 대체

홀 IC와 TMR IC는 현재 패키지 내 진단 및 ASIL-D 준수로 출하되어 자동차 스티어링과 페달 모듈의 경쟁 압력을 높이고 있습니다. 유도형 리니어 센서는 12mm 이상으로 -0.85%의 정확도를 달성하여 일반적인 리드의 공차를 능가하고 있습니다. 이러한 솔리드 스테이트의 진보로 리드 센서 시장의 CAGR은 1.4포인트 떨어지지만 가격에 민감한 알람과 액면계는 여전히 리드 부품을 선택하고 있습니다.

부문 분석

표면 실장형 디바이스는 2024년 리드 센서 시장 점유율의 38.7%를 차지하였습니다. 공기압 실린더용 나사식 배럴 센서는 리드 센서 시장 전체의 성장을 밀어 올리는 산업 자동화의 파도에 따라 8.3%의 연평균 복합 성장률(CAGR)을 형성하고 있습니다. 리드 센서 산업은 또한 레거시 어플라이언스를 위한 관통 구멍 모델을 유지하고 플랜지 패키지는 밀폐성을 요구하는 항공우주 수요를 확보하고 있습니다. 파이어 크래커 형식은 프로파일 높이가 가장 중요한 노트북 덮개 감지에 적합합니다. 예측 기간 동안 SMD를 채택하면 조립 인력이 줄어들고 웨어러블 기기에서 설계의 자유도가 높아지며 주요 공급업체에게 규모를 바탕으로 한 가격 우위가 유지됩니다.

나사형 배럴 제품에 대한 수요는 브라운필드 공장에서 실린더 수의 피드백 포인트가 급증함에 따라 지속적인 견인력을 낳고 있습니다. 원통형 하우징은 접점을 오일이나 금속 파편으로부터 보호하여 보증 클레임을 줄입니다. 이러한 견고한 유닛의 리드 센서 시장의 규모는 2030년까지 연평균 복합 성장률(CAGR) 8.3%로 확대되어 6억 3,000만 달러의 수익 증가가 예상됩니다. 라인 제조업체는 브래킷을 변경하지 않고 장착이 가능한 나사식 인서트를 선호하며 이는 기계적 호환성이 리드 센서 시장을 신속한 대체 가능성으로부터 보호하고 있음을 보여줍니다.

폼 A 스위치는 2024년 리드 센서 시장의 41.3%를 차지했으며, 개방 회로가 보안 및 액면 경보에 페일 세이프 로직을 제공했습니다. 그러나 배터리 구동 IoT 태그는 거의 0의 정지 전류를 요구하기 때문에 래칭 폼 E 설계가 CAGR 8.6%로 가장 높은 성장을 기록합니다. 나노구조 접점의 진보에 의해 라이프 사이클이 4배로 증가하여 스마트 미터나 자산 추적 장치에서의 채용이 가속화하고 있습니다.

폼 B의 노멀 클로즈 유형은 HVAC 팬 가드에 대응하고, 폼 C의 체인지 오버 접점은 PLC 제어 공정 밸브에 사용됩니다. 쌍안정 폼 E 모델의 리드 센서 시장의 규모는 2030년까지 4억 2,000만 달러에 달할 전망으로, 레거시 리드 릴레이에서 듀티 사이클 무선 노드로의 전환을 촉진합니다. 이러한 장치는 전력 없이 상태를 기억하므로 유지보수 팀은 서비스 빈도를 줄이고 리드 센서 업계 전체의 채용 곡선을 강화하는 정량화 가능한 OPEX 절약을 추가합니다.

리드 센서 시장은 실장 유형(표면 실장, PCB 스루홀, 기타), 접점 위치(폼 A(SPST-NO), 폼 B(SPST-NC), 기타), 스위칭 능력(저전압/신호(30V 미만), 중전압(30-200V), 기타), 용도(자동차, 가전, 기타), 지역에 따라 구분됩니다. 시장 예측은 금액(USD)으로 제공됩니다.

지역 분석

아시아태평양은 2024년 리드 센서 시장의 40.4%를 차지하였고 중국의 2,850억 위안에 상당하는 센서 경제와 고밀도 유리관 제조거점이 그 원동력이 되었습니다. 전기자동차와 스마트 공장의 현지 조달에 대한 국가 우대 조치로 OEM은 국내 리드 공급업체로 향하고 있지만 수입 특수 유리는 여전히 고전압 등급을 지원합니다. 일본의 정밀 공정 관리와 한국의 스마트폰 조립은 안정적인 대량 소비를 보장하고 인도의 승용차 제조는 전반적인 수요를 높이는 새로운 도어 닫힘 감지 수요를 창출합니다.

유럽은 Euro 7 규정에 따라 기능 안전이 강화되고 해상 풍력 발전소에서는 밀폐형 리미트 스위치가 필요하기 때문에 2030년까지 연평균 복합 성장률(CAGR)이 8.6%로 가장 급성장하는 지역입니다. SICK와 Endress Hauser의 730명 규모의 합작회사는 신뢰성 있는 유량 측정을 위한 리드 접점을 통합한 공정 분석에서의 지역 통합의 예입니다. 북유럽 전력 회사에서는 전기 기계식 미터의 100%를 스마트 엔드포인트로 교체하여 수량도 증가하고 있습니다. 독일의 기계 제조업체는 공기압 슬라이드에 나사식 배럴 센서를 통합하여 이 지역의 산업 리드 판매량을 강화하고 있습니다.

북미는 한 자릿수 중반의 건전한 페이스로 전진하고 있습니다. 유틸리티에서는 리드 펄스 접점에 의존하는 경우가 많은 20년간 사용 가능한 옥외 스마트 미터를 사용하고 있습니다. Littelfuse의 2025년 1분기 매출은 5억 5,400만 달러로 데이터센터의 배전과 EV 서비스 기기가 센서의 흡수를 촉진하는 가운데 수요의 회복력을 뒷받침하고 있습니다. 군용 스펙 유리와 접점에 대한 항공우주 산업의 요구에 따라 미국의 틈새 공급업체는 이익을 확보하고 있습니다. 멕시코의 소형 트럭 공장은 도어 스위치와 안전 벨트 스위치를 추가하고 캐나다의 재생에너지 프로젝트는 고전압 용도의 기회를 확대합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 저전력 스마트 그리드 미터의 급증

- EV 배터리 관리의 채용

- 인더스트리얼 4.0 리노베이션 및 자동화

- 스마트 홈과 IoT 디바이스의 보급

- 수소 연료전지 안전 시스템

- 일회용 의료기기용 소형 센서

- 시장 성장 억제요인

- 솔리드 스테이트(홀/TMR) 센서의 대체

- 고진동 존에서의 신뢰성 문제

- 유리관 공급 체인의 제약

- 고밀도 EV 파워트레인의 EMI 문제

- 업계 밸류체인 분석

- 규제 상황

- 기술적 전망

- 업계의 매력 - Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 거시경제 요인이 시장에 미치는 영향

제5장 시장 규모 및 성장 예측(금액)

- 실장 유형별

- 표면 실장(SMD)

- PCB 스루홀

- 나사 부착 배럴

- 플랜지/플랫팩

- 원통형/파이어 크래커

- 레버 암

- 플로트/레벨

- 기타

- 접점 위치별

- A형(SPST-NO)

- B형(SPST-NC)

- C형(SPDT)

- E형(래칭)

- 기타

- 스위칭 능력별

- 저전압/신호(<30V)

- 중전압(30-200 V)

- 고전압(>200V)

- 고전류(>1A)

- 고내열성

- 기타

- 용도별

- 자동차

- 가전제품

- 산업 자동화 및 로봇

- 안전 및 보안 시스템

- 헬스케어 및 의료기기

- IT 및 통신

- 기타 용도

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 대만

- 말레이시아

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장의 집중

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- Littelfuse Inc.

- Standex Electronics Inc.

- PIC GmbH

- Aleph Holdings Co. Ltd.

- STG Germany GmbH

- Coto Technology Inc.

- Reed Switch Developments Corp.

- ZF Friedrichshafen AG

- Reed Relays & Electronics India Ltd.

- WIKA Instruments India Pvt Ltd.

- HSI Sensing

- Magnasphere Corp.

- Hamlin Electronics(Littelfuse)

- Sensata Technologies

- Comus International

- MEDER electronic

- Schneider Electric(SE)

- SMC Corporation

- NTE Electronics Inc.

- TE Connectivity

- OKI Sensor Device Corp.

- Changjiang Electronics Tech

- Zhejiang Xurui Electronic Co.

- Shanghai Kaiyuan Microelectronics

- HOKUYO Automatic Co. Ltd.

제7장 시장 기회와 앞으로의 동향

- 시장 기회와 수요 가능성 평가

The Reed Sensor Market size is estimated at USD 2.01 billion in 2025, and is expected to reach USD 2.85 billion by 2030, at a CAGR of 7.20% during the forecast period (2025-2030).

Rising demand for intrinsically safe, hermetically sealed switching in electric-vehicle battery packs, hydrogen fuel-cell stacks, and outdoor smart-meter enclosures underpins this expansion. The reed sensor market continues to defend its niche against solid-state Hall and TMR alternatives by offering spark-free operation, zero-standby-power consumption, and proven 20-year field reliability in harsh conditions. Asia-Pacific remains the production engine, but Europe's regulatory push for renewable energy and functional safety drives the fastest regional growth. Competitive intensity is moderate: global leaders leverage scale, vertically integrated glass processing, and material innovations such as nanostructured contacts to stretch product life and lower cost.

Global Reed Sensor Market Trends and Insights

Surge in Low-Power Smart-Grid Metering

Utilities replacing legacy meters with 20-year maintenance-free smart devices increasingly specify reed switches for pulse counting because magnetic actuation draws zero standby power. Hermetic sealing prevents condensation in outdoor enclosures, extending service life across -40 °C to +85 °C. Large-scale rollouts by firms such as Gridspertise-now surpassing 108 million units-confirm the scalability of reed-based designs. Poland's Tauron Dystrybucja already manages 5.6 million customers via automated reading that depends on magnetic pulse integrity. Continued grid digitalization until 2030 sustains demand for robust, battery-independent switching.

EV Battery-Management Adoption

Battery packs in electric and hydrogen vehicles require spark-free, reliable position and leakage sensing. Continental's e-Motor Rotor Temperature Sensor trims temperature error to 3 °C, improving magnet optimization for efficiency. Honeywell's electrolyte-leak sensor offers a 20-minute warning window for thermal-runaway events, using hermetically sealed contacts to avoid ignition sources. Marquardt applies reed elements in hydrogen cell voltage monitors to catch H2 leaks before catastrophic failure. Accelerating EV adoption, therefore, adds a 2.1 percentage-point lift to the reed sensor market CAGR.

Solid-State Sensor Substitution

Hall and TMR ICs now ship with in-package diagnostics and ASIL-D compliance, raising competitive pressure in automotive steering and pedal modules. Inductive linear sensors achieve +-0.85% accuracy over 12 mm, eclipsing typical reed tolerances. These solid-state gains shave 1.4 percentage points from the reed sensor market CAGR, though price-sensitive alarms and liquid-level gauges still choose reed parts.

Other drivers and restraints analyzed in the detailed report include:

- Industrial-4.0 Retrofits and Automation

- Smart-Home and IoT Device Proliferation

- Reliability Issues in High-Vibration Zones

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surface-mount devices delivered 38.7% of the reed sensor market share in 2024, reflecting automated pick-and-place economics on high-volume consumer boards. Threaded-barrel sensors for pneumatic cylinders shape the strongest 8.3% CAGR, aligned with the industrial automation wave that lifts overall reed sensor market growth. The reed sensor industry also retains through-hole models for legacy appliances, while flange packages secure aerospace demand for hermeticity. Firecracker formats suit laptop lid detection, where profile height is paramount. Over the forecast period, SMD adoption lowers assembly labor, widens design wins in wearables, and sustains at-scale pricing advantages for leading suppliers.

Demand for threaded-barrel products pairs with a proliferation of cylinder-count feedback points in brownfield factories, creating sustained pull. Cylindrical housings safeguard contacts from oil and metal shavings, keeping warranty claims low. The reed sensor market size for these rugged units is forecast to expand at an 8.3 % CAGR to 2030, translating into USD 0.63 billion of incremental revenue. Line builders prefer threaded inserts because they retrofit without bracket changes, illustrating how mechanical compatibility protects the reed sensor market from quick substitutability.

Form A switches commanded 41.3% of the reed sensor market in 2024 because normally-open circuits provide fail-safe logic in security and liquid-level alarms. Latching Form E designs, however, log the highest 8.6% CAGR as battery-run IoT tags seek near-zero quiescent current. Advancements in nanostructured contacts quadruple life cycles, bolstering uptake in smart meters and asset trackers.

Form B normally-closed types cater to HVAC fan guards, while Form C changeover contacts find traction in PLC-controlled process valves. The reed sensor market size for bistable Form E models is set to reach USD 0.42 billion by 2030, capitalizing on the migration of legacy reed relays to duty-cycled wireless nodes. As these devices remember state without power, maintenance teams cut service frequency, adding quantifiable OPEX savings that reinforce the adoption curve across the reed sensor industry.

Reed Sensor Market is Segmented by Mounting Type (Surface Mount, PCB Through-Hole, and More), Contact Position (Form A (SPST-NO), Form B (SPST-NC), and More), Switching Capability (Low-Voltage/Signal (<30 V), Medium-Voltage (30-200 V), and More), Application (Automotive, Consumer Electronics and Home Appliances, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 40.4% of the reed sensor market revenue in 2024, powered by China's CNY 285 billion sensor economy and its dense glass-tube manufacturing base. National incentives for local content in electric vehicles and smart factories steer OEMs toward domestic reed suppliers, yet imported specialty glass still underpins high-voltage grades. Japan's precision process control and South Korea's smartphone assembly ensure steady high-volume consumption, while India's passenger-car build-out triggers new door-ajar fitments that raise overall demand.

Europe is the fastest-growing region at an 8.6% CAGR through 2030 as Euro 7 rules tighten functional safety and as offshore wind farms require hermetically sealed limit switches. SICK and Endress+Hauser's 730-staff joint venture exemplifies regional consolidation in process analytics that integrates reed contacts for reliable flow measurement. Nordic utilities swapping 100% of electromechanical meters for smart endpoints also lift volumes. German machine builders embed threaded-barrel sensors into pneumatic slides, reinforcing the region's pull on industrial-grade reed volume.

North America advances at a healthy mid-single-digit pace. Utilities specify 20-year outdoor smart meters that often rely on reed pulse contacts; state decarbonization mandates accelerate rollouts. Littelfuse's USD 554 million Q1 2025 revenue underscores demand resilience, with data-center power distribution and EV service equipment fueling sensor uptake. Aerospace requirements for Mil-Spec glass and contacts keep US niche suppliers profitable. Mexico's light-truck plants add door and seat-belt switches, while Canadian renewables projects expand high-voltage application opportunities.

- Littelfuse Inc.

- Standex Electronics Inc.

- PIC GmbH

- Aleph Holdings Co. Ltd.

- STG Germany GmbH

- Coto Technology Inc.

- Reed Switch Developments Corp.

- ZF Friedrichshafen AG

- Reed Relays & Electronics India Ltd.

- WIKA Instruments India Pvt Ltd.

- HSI Sensing

- Magnasphere Corp.

- Hamlin Electronics (Littelfuse)

- Sensata Technologies

- Comus International

- MEDER electronic

- Schneider Electric (SE)

- SMC Corporation

- NTE Electronics Inc.

- TE Connectivity

- OKI Sensor Device Corp.

- Changjiang Electronics Tech

- Zhejiang Xurui Electronic Co.

- Shanghai Kaiyuan Microelectronics

- HOKUYO Automatic Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in low-power smart-grid metering

- 4.2.2 EV battery-management adoption

- 4.2.3 Industrial-4.0 retrofits and automation

- 4.2.4 Smart-home and IoT device proliferation

- 4.2.5 Hydrogen fuel-cell safety systems

- 4.2.6 Disposable medical-device mini-sensors

- 4.3 Market Restraints

- 4.3.1 Solid-state (Hall/TMR) sensor substitution

- 4.3.2 Reliability issues in high-vibration zones

- 4.3.3 Glass-tube supply-chain constraints

- 4.3.4 EMI issues in dense EV powertrains

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Mounting Type

- 5.1.1 Surface Mount (SMD)

- 5.1.2 PCB Through-Hole

- 5.1.3 Threaded Barrel

- 5.1.4 Flange/Flat Pack

- 5.1.5 Cylindrical/Firecracker

- 5.1.6 Lever Arm

- 5.1.7 Float/Level

- 5.1.8 Others

- 5.2 By Contact Position

- 5.2.1 Form A (SPST-NO)

- 5.2.2 Form B (SPST-NC)

- 5.2.3 Form C (SPDT)

- 5.2.4 Form E (Latching)

- 5.2.5 Others

- 5.3 By Switching Capability

- 5.3.1 Low-Voltage/Signal (<30 V)

- 5.3.2 Medium-Voltage (30-200 V)

- 5.3.3 High-Voltage (>200 V)

- 5.3.4 High-Current (>1 A)

- 5.3.5 High-Temp-Resistant

- 5.3.6 Others

- 5.4 By Application

- 5.4.1 Automotive

- 5.4.2 Consumer Electronics and Home Appliances

- 5.4.3 Industrial Automation and Robotics

- 5.4.4 Safety and Security Systems

- 5.4.5 Healthcare and Medical Devices

- 5.4.6 Telecommunications and IT

- 5.4.7 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Taiwan

- 5.5.4.6 Malaysia

- 5.5.4.7 Australia

- 5.5.4.8 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Littelfuse Inc.

- 6.4.2 Standex Electronics Inc.

- 6.4.3 PIC GmbH

- 6.4.4 Aleph Holdings Co. Ltd.

- 6.4.5 STG Germany GmbH

- 6.4.6 Coto Technology Inc.

- 6.4.7 Reed Switch Developments Corp.

- 6.4.8 ZF Friedrichshafen AG

- 6.4.9 Reed Relays & Electronics India Ltd.

- 6.4.10 WIKA Instruments India Pvt Ltd.

- 6.4.11 HSI Sensing

- 6.4.12 Magnasphere Corp.

- 6.4.13 Hamlin Electronics (Littelfuse)

- 6.4.14 Sensata Technologies

- 6.4.15 Comus International

- 6.4.16 MEDER electronic

- 6.4.17 Schneider Electric (SE)

- 6.4.18 SMC Corporation

- 6.4.19 NTE Electronics Inc.

- 6.4.20 TE Connectivity

- 6.4.21 OKI Sensor Device Corp.

- 6.4.22 Changjiang Electronics Tech

- 6.4.23 Zhejiang Xurui Electronic Co.

- 6.4.24 Shanghai Kaiyuan Microelectronics

- 6.4.25 HOKUYO Automatic Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-Space and Unmet-Need Assessment