|

시장보고서

상품코드

1842593

세포 건강 스크리닝 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Cellular Health Screening - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

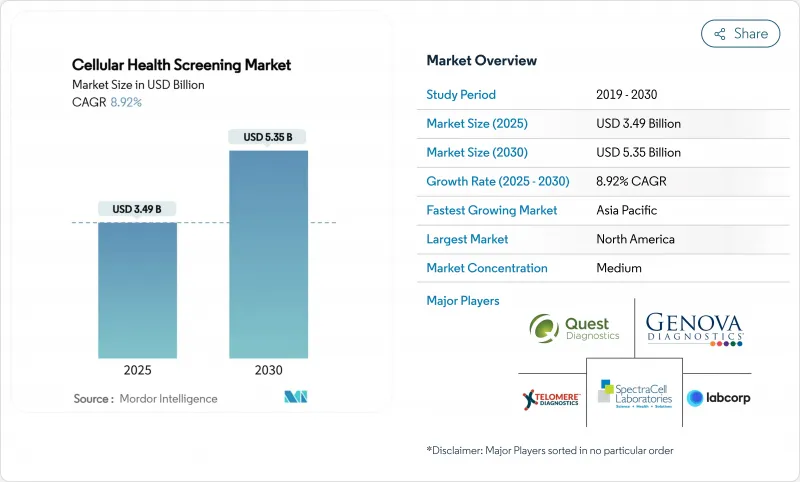

세포 건강 스크리닝 시장은 2025년에 34억 9,000만 달러를 창출하고 CAGR 8.92%를 나타내 2030년까지 53억 5,000만 달러로 증가할 것으로 예측됩니다.

개별화의료에 대한 국민의 강한 관심, 검사실이 개발한 검사에 대한 규제의 명확화, 예방의료의 우선도의 높아짐이 이 확대를 지지하고 있습니다. 북미는 광범위한 실험실 네트워크와 조기 소비자 직접 판매(DTC) 도입을 지원하며 여전히 지역 최대 구매자입니다. 아시아태평양은 고령화 연구 프로그램에 대한 국가의 자금 지원 및 중간층 수요 증가에 힘입어 지역별로 가장 빠른 성장을 보이고 있습니다. 단일 검사 패널이 여전히 수익의 대부분을 차지하고 있지만, 원시 바이오마커 데이터를 실용적인 권장 정보로 변환하는 머신러닝 분석에 도움이 되며, 다중 검사 패널과 타액 기반 채취 키트가 빠르게 확대되고 있습니다. 미토콘드리아 기능 장애를 만성 질환과 연관시키는 임상 증거가 증가함에 따라 신제품 출시와 첨단 세포 진단 투자에 계속 박차를 가하고 있습니다.

세계의 세포 건강 스크리닝 시장 동향과 인사이트

맞춤형 의료 프로그램

병원에서는 텔로미어 길이와 산화 스트레스 점수를 사용하여 복용량을 좁히면 동반진단과 약물 요법을 결합하는 경우가 늘고 있습니다. 2024년 FDA가 일루미나의 TruSight Oncology Comprehensive 분석을 허가함에 따라 멀티플렉스 바이오마커 패널이 주류 의료에 효과적임이 입증되었습니다. 종양 내과 및 순환기 내과에서는 세포 마커를 전자 의료 기록 워크플로우에 통합하여 위험에 따라 치료 선택이 가능해졌습니다. 기업의 웰니스 계약은 더욱 기세를 늘리고, 고용주는 직원의 스크리닝 프로그램을 통해 수집된 생물학적 연령 측정 기준에 보험료를 연결하고 있습니다. 머신 러닝 엔진은 이러한 데이터 세트를 향상시키고 예측 정확도를 향상시키고 새로운 결과의 출현에 따라 지속적인 모델을 개선할 수 있습니다.

예방 건강 관리에 대한 정부 자금 지원

일본의 후생성은 전국적인 대사성 질환 리스크 검사에 심자도 검사를 채용하여 조기 발견 툴에 대한 정책적 헌신을 표명하고 있습니다. 호라이즌 유럽의 보조금과 NIH의 제로 사이언스 예산은 바이오마커 검증 연구에 새로운 자금을 투입하여 실험실에서 임상으로 파이프라인의 진전을 가속화하고 있습니다. 국가 지급자는 가역적인 단계에서 질병을 발견하는 데 비용 회피의 가치가 있다고 생각하고, 보조금 모집은 멀티오믹스 데이터 세트를 마이닝하는 AI 알고리즘의 통합을 명시하게 되었습니다. 이러한 인센티브는 신흥기업이 조기에 프로토콜을 표준화하도록 촉구하고, 하류 규제 당국과의 마찰을 줄이고, 상업화 일정을 단축시킵니다.

샘플 운송 안정성과 콜드체인 위험

산화 스트레스 분석과 사이토 카인 분석은 운송 중에 온도 상승에 부딪히면 열화되어 결과의 정확성이 저하됩니다. 모델 연구는 단지 2-8°C를 단시간 초과한 경우에도 바이오마커의 무결성이 감소한다는 것을 보여줍니다. 첨단 온도 패키징 및 온박스 데이터 로거를 사용하는 것이 효과적이지만 비용과 무게를 증가시킵니다. 기업은 채취 거점 근처에 위성 실험실을 설치하고 냉장 없이 안전하게 이동할 수 있는 건조 혈액 스폿 형식을 실험함으로써 대응하고 있습니다. 저소득 지역에서는 불충분 한 콜드체인 네트워크가 세포 건강 스크리닝 시장을 널리 보급하는 장벽이되었습니다.

부문 분석

단일 검사 형식은 명확한 임상 적응증과 저렴한 비용으로 지원되었으며 2024년 세포 건강 스크리닝 시장의 63.35%를 차지했습니다. 멀티 검사 번들은 매출이 작지만 2030년까지 연평균 복합 성장률(CAGR)은 13.25%를 나타내 전체적 건강 스냅샷에 대한 소비자의 의지로 인해 2030년까지 기록될 것으로 예상됩니다. 알고리즘 플랫폼이 몇 분 이내에 수십 개의 마커를 해석하고 복잡한 데이터를 간결한 행동 계획으로 변환할 수 있게 되었기 때문에 복수 검사에 의한 세포 건강 스크리닝 시장 규모는 급속히 확대될 것으로 예측됩니다. 의사는 연간 1회의 건강 진단으로 텔로미어, 염증, 미토콘드리아 마커를 한 번에 파악하기 위해 멀티플렉스 패널을 주문하는 것이 늘고 있습니다. DTC 브랜드는 멀티 검사의 편의성을 활용하여 정기 구매 코칭을 업셀하고 참여도를 강화하고 있습니다.

벤더는 패널을 계층화하고 사용자에게 엔트리 번들로 시작하고 시간이 지남에 따라 바이오 마커를 추가하여 가격 민감도에 대응합니다. 또한 직원의 건강 증진에 다중 검사 키트를 도입하여 고용주도 결근을 줄이기 위해 성장하고 있습니다. 실험실은 높은 처리량 시퀀싱과 질량 분석 워크플로우를 통합하여 턴어라운드를 지연시키지 않고 증가하는 샘플 양을 관리합니다. 하드웨어 자동화는 샘플당 비용을 더욱 줄이고, 세포 건강 스크리닝 시장에서 경쟁력 있는 가격 설정을 지원합니다.

텔로미어 분석은 2024년에 40.53%의 점유율을 유지했지만, 미토콘드리아 기능 검사는 미토콘드리아의 건강, 심혈관 위험, 대사성 질환과의 관련이 조사에서 확인되었기 때문에 CAGR은 15.85%를 나타낼 전망입니다. 따라서 미토콘드리아 분석과 관련된 세포 건강 스크리닝 시장 규모는 빠르게 확대될 것으로 보입니다.

새로운 형광 기반 판독 및 호흡 측정 플랫폼은 처리량과 감도를 향상시키고 이러한 평가를 일상 스크리닝에 실용화합니다. 공급자에 따라 미토콘드리아 점수와 NAD 경로를 대상으로 한 식사 권장 사항을 패키징하고 사용자에게 명확한 개입 로드맵을 제공합니다. 산화 스트레스와 염증성 사이토카인 패널은 임상의가 만성 질환의 진행을 모니터링하는 역할을 강조하기 때문에 수요가 유지되고 있습니다. 중금속 부하 분석은 분석 시간을 단축하는 미세 유체 센서의 기술 혁신에 힘입어 산업 오염 지역에서 틈새 시장을 열어줍니다. 인공지능 오버레이는 조기 병태를 예측하는 바이오마커 클러스터를 확인하고 세포 건강 스크리닝 시장에서 종합적인 미토콘드리아 검사의 임상적 매력을 더욱 높여줍니다.

지역 분석

북미는 2024년 매출의 37.82%를 차지하며, 고밀도 검사 시설 네트워크, 지원적인 상환 조종사, 적극적인 케어에 돈을 지불하는 것을 괴롭히지 않는 기술에 정통한 인구에 의해 지원되었습니다. 미국은 LDT 모니터링에 대한 FDA의 명확한 지침의 혜택을 누리고 있으며, 검사 시설은 검사 품질을 보호하면서 시장에 예측 가능한 경로를 얻을 수 있습니다. 캐나다 시장 전망은 퀘스트 다이아그노스틱스가 9억 8,500만 달러를 투자하여 라이플라보 인수를 완료하고 통합 스크리닝 서비스를 제공하는 전국적인 용량을 증강함으로써 강화되었습니다. 멕시코에서는 중산계급이 대두해, 저렴한 DTC 킷 수요가 높아지고 있어, 현지의 벤더는 미국 벤더와 제휴해, 물류의 현지화를 진행하고 있습니다.

유럽에서는 IVDR에 의한 기술 기준의 통일이 진행되고, 컴플라이언스 비용은 상승하는 것, 검사법의 타당성에 대한 사회적 신뢰는 향상하고, 견조한 기세를 유지하고 있습니다. 독일과 영국은 강력한 임상 연구 생태계에 힘입어 채택을 이끌고 있으며, 프랑스는 웰니스 패키지에서 셀룰러 패널을 상환하는 민간 보험 회사의 참여가 증가하고 있습니다. 남유럽 국가들은 EU의 부흥 기금을 활용하여 검사 시설의 인프라를 현대화하고 역사적인 능력 격차를 축소하고 있습니다. 엄격한 데이터 프라이버시 규범은 유전체의 악용을 경계하는 소비자의 공감을 불러 프라이버시 바이 디자인을 도입하는 유럽의 프로바이더가 바람직한 선택지로 자리잡고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 13.31%를 나타낼 전망입니다. 중국은 병원 수준의 검사 시설 클러스터를 확대하고 혁신 보조금을 통해 국내 검사 개발자를 지원합니다. 일본은 전국적인 심자도 검진을 통해 예방의료를 제도화하고 바이오마커의 조기 발견에 대한 정부의 신념을 강조합니다. 인도의 디지털 헬스 구상은 모바일 사혈 서비스에 의한 1채 1채에의 검체 채취로, 농촌의 채널을 엽니다. 한국과 호주는 AI와 바이오마커 탐색을 융합시킨 산학 컨소시엄을 장려하고 제품 파이프라인을 가속화하고 있습니다. 진전은 하고 있는 것, 규제 프레임워크이 좌절하고, 콜드체인의 인프라도 불균등하기 때문에 벤더는 나라마다 시장 진출 전략을 조정해, 현지의 유통업체와 제휴해 물류나 문화적인 뉘앙스에 대응해야 합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 맞춤형 의료 프로그램의 채용

- 예방 건강 관리에 대한 정부의 자금 지원

- 고령화와 만성질환 부담

- 직접 소비자용 검사 플랫폼의 확대

- AI에 의한 생물학적 연령 스코어링의 통합

- 보험료와 텔로미어 지표를 연동시키는 고용주의 복리 후생 제도

- 시장 성장 억제요인

- 샘플 수송의 안정성과 콜드체인 위험

- 진화하는 규제와 상환의 불확실성

- 재택 유전체 텔로미어 데이터에 대한 데이터 프라이버시 우려

- 산화 스트레스 분석 결과의 실험실 간 편차

- Five Forces 분석

- 신규 진입자의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측

- 패널 유형별

- 단일 검사 패널

- 텔로미어 검사

- 산화 스트레스 검사

- 염증 검사

- 중금속 검사

- 다중 검사 패널

- 단일 검사 패널

- 검사 유형별

- 텔로미어 길이

- 산화 스트레스 마커

- 염증성 사이토카인

- 중금속 부하

- 미토콘드리아 기능

- 샘플 유형별

- 혈액

- 소변

- 타액

- 구강 내막 면봉

- 모발/기타 조직

- 최종 사용자별

- 임상 진단 실험실

- 병원 연구소

- 연구 및 학술기관

- 웰니스 및 항노화 클리닉

- 홈 헬스케어/개인 소비자

- 기업 웰니스 제공업체

- 유통 채널별

- 소비자 직접 판매(온라인)

- 의사 처방/클리닉 베이스

- 고용주 후원 프로그램

- 소매 약국

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Quest Diagnostics Inc.

- Laboratory Corporation of America Holdings(Labcorp)

- SpectraCell Laboratories Inc.

- Genova Diagnostics

- Bio-Reference Laboratories Inc.(OPKO Health)

- Telomere Diagnostics Inc.

- Segterra Inc.

- Grail LLC

- RepeatDx

- Agilent Technologies Inc.

- Bloom Diagnostics GmbH

- Cell Science Systems Corp.

- Fagron Genomics

- Life Length SL

- Chronomics Ltd.

- Zymo Research Corp.

- TruDiagnostic LLC

- 23andMe Inc.

- MyDNAge(Epiq MD)

- Becton, Dickinson and Company

제7장 시장 기회와 전망

KTH 25.10.29The cellular health screening market generated USD 3.49 billion in 2025 and is forecast to rise to USD 5.35 billion by 2030, reflecting an 8.92% CAGR.

Strong public interest in personalized medicine, regulatory clarity for laboratory-developed tests, and the growing priority of preventive care underpin this expansion. North America remains the largest regional buyer, supported by extensive laboratory networks and early direct-to-consumer (DTC) adoption. Asia-Pacific posts the fastest regional advance, propelled by state funding for aging-research programs and expanding middle-class demand. Single-test panels still dominate revenues, yet multi-test panels and saliva-based collection kits are scaling rapidly, aided by machine-learning analytics that transform raw biomarker data into actionable recommendations. Mounting clinical evidence linking mitochondrial dysfunction to chronic disease continues to spur new product launches and investment in advanced cellular diagnostics.

Global Cellular Health Screening Market Trends and Insights

Personalized-medicine programs

Hospitals increasingly couple companion diagnostics with drug regimens, using telomere length and oxidative-stress scores to refine dosing. The FDA authorization of Illumina's TruSight Oncology Comprehensive assay in 2024 validated multiplex biomarker panels for mainstream care. Oncology and cardiology units now embed cellular markers inside electronic health-record workflows, enabling risk-stratified treatment selection. Corporate wellness contracts add momentum, with employers tying premiums to biological-age metrics gathered via employee screening programs. Machine-learning engines enrich these datasets, improving prediction accuracy and allowing continuous model refinement as new outcomes emerge.

Government funding for preventive healthcare

Japan's Ministry of Health has adopted magnetocardiography for nationwide metabolic disease risk checks, signaling policy commitment to early detection tools. Horizon Europe grants and NIH geroscience budgets channel fresh capital toward biomarker validation studies, accelerating pipeline progress from lab bench to clinic. National payers see cost-avoidance value in finding disease at a reversible stage, and grant calls now specify integration of AI algorithms that mine multi-omics datasets. These incentives encourage start-ups to standardize protocols early, reducing downstream regulatory friction and shortening commercialization timelines.

Sample-transport stability and cold-chain risk

Oxidative-stress and cytokine assays degrade when shipments encounter temperature spikes, compromising result accuracy. Modeling studies show even brief excursions outside 2-8 °C diminish biomarker integrity. Advanced thermal packaging and on-box dataloggers help, yet add cost and weight. Companies respond by locating satellite labs nearer collection hubs and experimenting with dried-blood-spot formats that travel safely without refrigeration. In low-income regions, insufficient cold-chain networks remain a barrier to broad uptake of the cellular health screening market.

Other drivers and restraints analyzed in the detailed report include:

- Aging population and chronic-disease burden

- Expansion of DTC test platforms

- Evolving regulatory and reimbursement uncertainty

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-test formats held 63.35% of the cellular health screening market in 2024, supported by clear clinical indications and lower cost. Multi-test bundles, though smaller in revenue, record a 13.25% CAGR to 2030 thanks to consumer appetite for holistic health snapshots. The cellular health screening market size for multi-test offerings is projected to expand rapidly as algorithmic platforms can interpret dozens of markers within minutes, converting complex data into concise action plans. Physicians increasingly order multiplex panels during annual physicals to capture telomere, inflammation, and mitochondrial markers in one visit. DTC brands leverage multi-test convenience to upsell subscription coaching, reinforcing engagement.

Vendors address price sensitivity by tiering panels, letting users start with an entry bundle then add biomarkers over time. Growth also stems from employers that deploy multi-test kits in workforce wellness drives to reduce absenteeism. Laboratories integrate high-throughput sequencing and mass-spectrometry workflows to manage the rising sample volume without delaying turnaround. Hardware automation further trims per-sample cost, supporting competitive pricing in the cellular health screening market.

Telomere assays retained 40.53% share in 2024, yet mitochondrial function testing will post the highest 15.85% CAGR as research confirms links between mitochondrial health, cardiovascular risk, and metabolic disease. The cellular health screening market size tied to mitochondrial assays will therefore widen swiftly.

Novel fluorescence-based readouts and respirometry platforms increase throughput and sensitivity, making these evaluations practical for routine screening. Some providers package mitochondrial scores with dietary recommendations that target NAD+ pathways, giving users a clear intervention roadmap. Oxidative-stress and inflammatory-cytokine panels maintain demand because clinicians value their role in monitoring chronic-disease progression. Heavy-metal burden assays carve a niche in regions with industrial pollution, supported by microfluidic sensor innovations that cut analysis time. AI overlays identify biomarker clusters predictive of early pathology, further raising the clinical appeal of comprehensive mitochondrial testing in the cellular health screening market.

The Cellular Health Screening Market Report is Segmented by Panel Type (Single-Test Panels [Telomere Tests, Oxidative Stress Tests, and More], and Multi-Test Panels), Test Type (Telomere Length, Oxidative Stress Markers, and More), Sample Type (Blood, Urine, and More), End User (Hospital Laboratories, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 37.82% of 2024 revenue, anchored by dense laboratory networks, supportive reimbursement pilots, and a tech-savvy population willing to pay for proactive care. The United States benefits from clear FDA guidance on LDT oversight, giving laboratories predictable pathways to market while safeguarding test quality. Canada's market outlook strengthened when Quest Diagnostics closed its USD 985 million LifeLabs purchase, boosting nationwide capacity to deliver integrated screening services. Mexico's emerging middle class drives demand for affordable DTC kits, and local distributors partner with U.S. vendors to localize logistics.

Europe maintains solid momentum as the IVDR harmonizes technical standards, improving public trust in assay validity though raising compliance costs. Germany and the United Kingdom lead adoption, backed by strong clinical-research ecosystems, while France sees rising participation from private insurers that reimburse cellular panels within wellness packages. Southern European countries tap EU recovery funds to modernize laboratory infrastructure, narrowing historical capacity gaps. Strict data-privacy norms resonate with consumers wary of genomic misuse, positioning European providers that embed privacy-by-design as preferred options.

Asia-Pacific records the fastest regional CAGR at 13.31% through 2030. China expands hospital-grade laboratory clusters and supports domestic test developers through innovation grants. Japan institutionalizes preventive medicine through nationwide magnetocardiography screening, underscoring government belief in early biomarker detection. India's digital-health initiatives open rural channels, with mobile phlebotomy services collecting samples door-to-door. South Korea and Australia encourage university-industry consortia that fuse AI with biomarker discovery, accelerating product pipelines. Despite progress, disparate regulatory frameworks and uneven cold-chain infrastructure mean vendors must tailor go-to-market strategies by country, partnering with local distributors to address logistical and cultural nuances.

- Quest Diagnostics

- LabCorp

- SpectraCell Laboratories

- Genova Diagnostics

- Bio-Reference Laboratories Inc. (OPKO Health)

- Telomere Diagnostics

- Segterra

- Grail LLC

- RepeatDx

- Agilent Technologies

- Bloom Diagnostics

- Cell Science Systems Corp.

- Fagron Genomics

- Life Length S.L.

- Chronomics Ltd.

- Zymo Research Corp.

- TruDiagnostic LLC

- 23andMe

- MyDNAge (Epiq MD)

- Beckton Dickinson

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Adoption Of Personalized-Medicine Programs

- 4.2.2 Government Funding For Preventive Healthcare

- 4.2.3 Ageing Population & Chronic-Disease Burden

- 4.2.4 Expansion Of Direct-To-Consumer Test Platforms

- 4.2.5 AI-Driven Biological-Age Scoring Integrations

- 4.2.6 Employer Wellness Schemes Tying Premiums To Telomere Metrics

- 4.3 Market Restraints

- 4.3.1 Sample-Transport Stability & Cold-Chain Risk

- 4.3.2 Evolving Regulatory & Reimbursement Uncertainty

- 4.3.3 Data-Privacy Concerns For At-Home Genomic Telomere Data

- 4.3.4 Inter-Lab Variability Of Oxidative-Stress Assay Results

- 4.4 Porter's Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Panel Type

- 5.1.1 Single-test Panels

- 5.1.1.1 Telomere Tests

- 5.1.1.2 Oxidative Stress Tests

- 5.1.1.3 Inflammation Tests

- 5.1.1.4 Heavy-Metals Tests

- 5.1.2 Multi-test Panels

- 5.1.1 Single-test Panels

- 5.2 By Test Type

- 5.2.1 Telomere Length

- 5.2.2 Oxidative Stress Markers

- 5.2.3 Inflammatory Cytokines

- 5.2.4 Heavy-Metal Burden

- 5.2.5 Mitochondrial Function

- 5.3 By Sample Type

- 5.3.1 Blood

- 5.3.2 Urine

- 5.3.3 Saliva

- 5.3.4 Buccal Swab

- 5.3.5 Hair / Other Tissues

- 5.4 By End User

- 5.4.1 Clinical Diagnostic Laboratories

- 5.4.2 Hospital Laboratories

- 5.4.3 Research & Academic Institutes

- 5.4.4 Wellness & Anti-aging Clinics

- 5.4.5 Home Healthcare / Individual Consumers

- 5.4.6 Corporate Wellness Providers

- 5.5 By Distribution Channel

- 5.5.1 Direct-to-Consumer (Online)

- 5.5.2 Physician-Ordered / Clinic-Based

- 5.5.3 Employer-Sponsored Programs

- 5.5.4 Retail Pharmacies

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Quest Diagnostics Inc.

- 6.3.2 Laboratory Corporation of America Holdings (Labcorp)

- 6.3.3 SpectraCell Laboratories Inc.

- 6.3.4 Genova Diagnostics

- 6.3.5 Bio-Reference Laboratories Inc. (OPKO Health)

- 6.3.6 Telomere Diagnostics Inc.

- 6.3.7 Segterra Inc.

- 6.3.8 Grail LLC

- 6.3.9 RepeatDx

- 6.3.10 Agilent Technologies Inc.

- 6.3.11 Bloom Diagnostics GmbH

- 6.3.12 Cell Science Systems Corp.

- 6.3.13 Fagron Genomics

- 6.3.14 Life Length S.L.

- 6.3.15 Chronomics Ltd.

- 6.3.16 Zymo Research Corp.

- 6.3.17 TruDiagnostic LLC

- 6.3.18 23andMe Inc.

- 6.3.19 MyDNAge (Epiq MD)

- 6.3.20 Becton, Dickinson and Company

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment