|

시장보고서

상품코드

1842594

기저세포암 치료 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Basal Cell Carcinoma Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

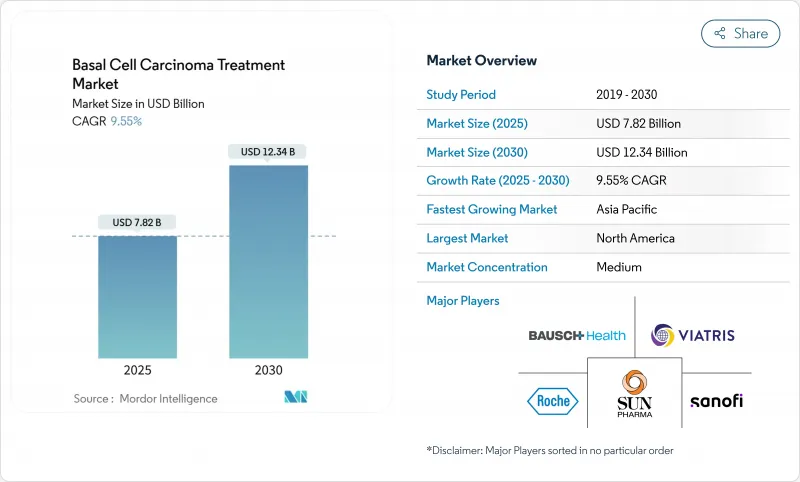

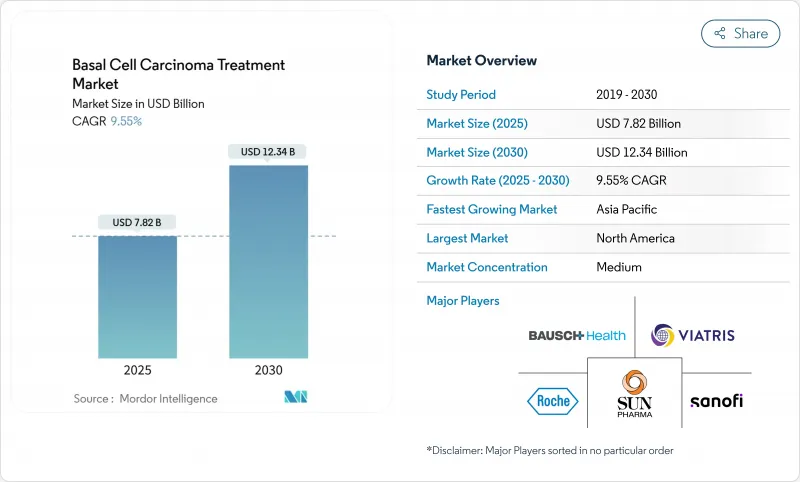

기저세포암 치료 시장은 2025년에 78억 2,000만 달러에 이를 전망이며, 2030년에는 123억 4,000만 달러에 이를 전망으로, CAGR 9.55%로 성장할 것으로 예측됩니다.

강력한 성장은 세계적인 피부암 이환율 증가, 저침습 치료로의 전환, 신흥 경제권의 전문 피부과 서비스에 대한 광범위한 접근의 수렴을 반영합니다. 이 기세는 수십년 동안 자외선에 노출된 고령화 사회와 평균 자외선량을 증가시킨 환경 변화에 의해 증폭되고 있습니다. 외과적 절제는 여전히 표준 치료이지만, 비침습적 장비와 국소 감광제가 상업적 지원을 받으면서 광역학적 요법이 급속히 확대되고 있습니다. AI를 활용한 더모스코피나 FDA가 승인한 진단 기기에 의해 발견부터 치료까지의 간격이 단축되어 보다 빠른 개입이 가능해지고 있습니다. 북미는 성숙한 환급제도에 의해 주도권을 유지하고 아시아태평양은 한국과 일본에서의 이환율 급증을 배경으로 급성장하고 있습니다.

세계의 기저세포암 치료 시장의 동향과 인사이트

피부암 유병률 상승

세계의 기저세포암 이환율은 2021년에 440만명에 이르렀고, 연령표준화율은 10만명 당 51.71명에 상당합니다. 1차 케어에서 피부과의 커버율 향상과 이미지 기반 트리아지에 의해 충분한 의료를 받을 수 없는 지역에서 지금까지 드러나지 않았던 사례 수가 밝혀지고 있습니다. 기후모델 예측에 따르면 오존이 1% 감소할 때마다 기저세포암 발생률은 2.7% 상승하고, 기온이 2°C 상승하면 2050년까지 11% 증가할 수 있습니다. 일본에서는 인구동태가 급속히 변하고 있으며, 90세 이상의 노인이 진단의 17%를 차지하고 있습니다. 실외 노동자의 직업적 노출은 여전히 높으며, 고용주는 자외선 보호 장비에 대한 투자와 정기적인 검진을 촉구하고 있습니다.

누적 자외선 노출량이 많은 고령화 사회

일본의 암 등록에서는 1989년에서 2021년 사이에 70세 이상의 환자 비율이 44%에서 74%로 증가했습니다. 티민 다이머 형성으로 인한 DNA 손상은 수십년 동안 축적되기 때문에 노인 집단은 특히 영향을 받기 쉽습니다. 헬스케어 시스템은 노인 피부과 부문을 증설해, 노인 스크리닝의 역치를 낮추는 것으로 대응해, 조기 발견을 촉진하고 비용 대비 효과를 향상시키고 있습니다.

고급 약물 요법 및 수술의 높은 비용

비스모데깁과 세미플리맙의 약가는 각각 월 13,000달러와 10,000달러이며, 많은 자비 부담 환자는 구입하기 어렵습니다. 모스 현미경 수술은 5년간의 치유율이 98%를 넘었음에도 불구하고 표준 절제술보다 120-370% 많은 비용이 듭니다. 환자 1인당 평균 의료비는 2006년 1,000달러에서 2011년 1,600달러로 상승했으며 현재도 계속 상승하고 있습니다. 저소득 국가에서는 시장 진입이 7년 정도 늦어지는 경우가 있어 가격이나 규제의 과제가 부각되고 있습니다. 스킨젝트와 같은 패치 기반 접근법은 미화 1,000달러의 가격대를 목표로 하고 있으며, 가용성 격차를 없애기 위해 노력하고 있습니다.

부문 분석

2024년 기저세포암 치료 시장 규모의 36.14%를 외과적 수법이 차지하였고 광범위 절제와 모스 현미경 프로토콜에 대한 임상의의 신뢰를 뒷받침하고 있습니다. Mohs의 이용률은 1992년부터 2009년에 걸쳐 700% 확대되었지만, 보험료가 높아 지불자의 감시의 대상이 되고 있습니다. 방사선 요법은 수술에 적합하지 않은 환자에 대해 80-92%의 국소 제어율을 기록합니다. 광역학적 요법은 CAGR 11.13%에서 가장 급성장하는 치료법으로, 치유 기간의 단축과 미용 상의 이점이 뒷받침됩니다. 5-플루오로우라실과 칼시포트리엔의 병용 외용 요법은 4주간의 단일 요법에 비해 7-14일에 클리어런스를 달성합니다. 헤지호그 경로 억제제 및 체크포인트 항체는 진행 사례에서 생존을 연장합니다. 세미플리맙은 국소 진행 사례에서 29%, 전이 사례에서 21%의 객관적 효과를 보였습니다. VP-315와 같은 신규 종양 용해 펩티드는 2상 시험에서 97%의 전주효과와 51%의 조직학적 완전한 완화를 나타내며, 외과적 치료를 필요로 하지 않는 혁신적인 미래를 보여줍니다.

2세대 딜리버리 플랫폼과 AI를 통한 병변 매핑은 이러한 치료 변화를 보완합니다. 광 간섭 단층계는 병변 중심에서 95.5%의 정확도를 달성하고, 외과의사는 절제 마진을 제한하고 건강한 조직을 온존할 수 있습니다. 이러한 정확도는 수술 단계를 줄이고 환자 처리량을 가속화하고 시설 비용을 줄입니다. 기술이 외래환자에 침투함에 따라 광선역학적 치료제 및 국소치료제의 기저세포암 치료 시장 규모는 비례하여 확대될 것으로 예측됩니다.

지역 분석

북미는 2024년 기저세포암 치료 시장 수익의 43.58%를 차지하였고, 2030년까지의 CAGR은 8.89%를 달성할 전망입니다. FDA가 승인한 DermaSensor와 같은 최첨단 진단법은 1차 케어의 가능성을 넓히지만, 모스 경막 절제술의 비용이 표준 절제술의 120-370%에 머물기 때문에 공제액이 큰 의료 보험 제도가 치료의 흡수를 억제하고 있습니다. 세미플리맙과 코시벨리맙의 획기적인 신약 지정이 입증한 바와 같이, 규제 당국의 민첩성은 혁신자에게 혜택을 줄 수 있지만, 2024년 12월부터 2025년 7월까지 에퓨덱스의 결함으로 인해 공급망의 취약성이 표면화되었습니다.

아시아태평양은 CAGR 10.36%로 기저세포암 치료 시장이 가장 급성장하고 있는 지역입니다. 한국에서는 1999년부터 2019년에 걸쳐 증례 수가 7배로 증가하였고, 기저세포암의 진단 건수는 488건에서 3,908건으로 급증했습니다. 규제기관은 80.9%의 정확도를 가진 canofyMD SCAI AI 소프트웨어를 승인하고 기술 선진국으로서의 채용을 강조했습니다. 일본 등록에 따르면 90세 이상의 환자가 17%를 차지하게 되면서 인구통계학적 압력이 밝혀졌습니다. 조직학적 하위유형의 차이로 인해 서양 집단보다 표재성 병변의 빈도가 낮기 때문에 지역별 지침이 필요합니다.

유럽에서는 국민 모두를 위한 보험 제도와 엄격한 자외선 조사 정책에 의해 CAGR 9.12%로 진전하고 있습니다. 유럽위원회는 진행성 기저세포암에 대한 최초의 면역요법으로서 세미플리맙을 승인하여 규제상황이 호의적임을 보여주었습니다. BF-200 ALA를 이용한 광선역학적 요법의 임상시험으로 90.9%의 클리어런스를 기록하여 미용에 민감한 치료에 있어서 유럽의 리드를 강화합니다. 중동 및 아프리카는 CAGR 9.94%로 성장해 민간건강과 정부의 임상시험 승인이 확대됐습니다. 아랍에미리트(UAE)는 2025년 5월 Medicus Pharma의 마이크로니들 패치 SkinJect의 임상시험을 승인하고 현지에서 임상 연구 능력으로의 전환을 보여주었습니다. 그러나 지방의 피부과에 대한 접근은 여전히 드물며 원격 피부과 플랫폼의 이용이 시급합니다. 남미는 9.67%의 성장률을 보이지만 신형 생물제제의 환급 장애물에 직면하여 비용 효율적인 제네릭 의약품과 원격 스크리닝 시험에 대한 가능성이 존재합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 도입

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 피부암 증가

- 누적 자외선 노출량이 많은 고령화 사회

- AI를 활용한 더모스코피에 의한 조기 발견 및 조기 치료

- 평균 자외선량이 증가하는 환경 변화

- 헤지호그 경로 억제제의 적응 확대

- 직장의 자외선 안전에 관한 법률이 검진 수요를 뒷받침

- 시장 성장 억제요인

- 고급 약물 요법과 수술의 높은 비용

- 1차 케어 환경에서의 과소진단

- 체크포인트 억제제의 병용에 대한 환급의 장애물

- 헤지호그 억제제의 장기 독성에 관한 안전성에 대한 우려

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 역학 동향

제5장 시장 규모 및 성장 예측

- 치료 유형별

- 수술

- 외과적 절제술

- 모스 현미경 수술

- 전기 천공 소파술(ED&C)

- 방사선요법

- 광선역학적 요법

- 동결요법

- 국소화학요법

- 5-플루오로우라실(5-FU)

- 티르바니불린

- 이미퀴모드

- 경구약

- 점적요법

- 수술

- 병기별

- 표재성

- 결절성

- 침윤성

- 전이성

- 최종 사용자별

- 병원

- 전문 클리닉

- 외래수술센터(ASC)

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 경쟁 벤치마킹

- 시장 점유율 분석

- 기업 프로파일

- AbbVie(Allergan)

- Bausch Health Companies Inc.

- BridgeBio Pharma Inc

- Bristol Myers Squibb Co.

- Castle Biosciences Inc.

- Eisai Co., Ltd.

- F. Hoffmann-La Roche AG

- Galderma SA

- LEO Pharma A/S

- Medicus Pharma Ltd

- Medivir AB

- Merck & Co., Inc.

- Novartis AG

- Perrigo Company plc

- Pfizer Inc.

- Regeneron Pharmaceuticals Inc.

- Regeneron Pharmaceuticals Inc.

- Sanofi SA

- Sun Pharmaceutical Industries Ltd

- Taro Pharmaceutical Industries Ltd

- Verrica Pharmaceuticals Inc.

- Viatris Inc.

제7장 시장 기회와 전망

CSM 25.11.03The basal cell carcinoma treatment market is valued at USD 7.82 billion in 2025 and is forecast to reach USD 12.34 billion by 2030, advancing at a 9.55% CAGR.

Strong growth reflects the convergence of rising global skin-cancer incidence, the shift toward minimally invasive therapies, and broader access to specialty dermatology services across emerging economies. Momentum is amplified by an aging population that has accumulated decades of ultraviolet exposure and by environmental changes that have intensified average UV radiation. Surgical excision remains the standard of care, yet photodynamic therapy is scaling rapidly as non-invasive devices and topical photosensitizers gain commercial traction. AI-driven dermoscopy and FDA-cleared diagnostic devices are shortening detection-to-treatment intervals, which in turn supports earlier-stage interventions. North America sustains leadership through mature reimbursement systems, while Asia-Pacific posts the fastest growth on the back of surging incidence in Korea and Japan.

Global Basal Cell Carcinoma Treatment Market Trends and Insights

Rising prevalence of skin cancers

Global basal cell carcinoma incidence reached 4.4 million new cases in 2021, equal to an age-standardized rate of 51.71 per 100,000. Enhanced dermatology coverage and image-based triage in primary care expose historically hidden caseloads in underserved regions. Climate-model forecasts show that every 1% depletion of ozone could elevate basal cell carcinoma incidence by 2.7%, while a 2 °C temperature rise could add 11% more cases by 2050. Japan illustrates demographic acceleration, with individuals aged >= 90 now comprising 17% of diagnoses. Occupational exposure remains high among outdoor workers, prompting employers to invest in UV-protective gear and routine screenings.

Aging population with higher cumulative UV exposure

The share of patients older than 70 increased from 44% to 74% in Japanese cancer registries between 1989 and 2021. DNA damage due to thymine-dimer formation accumulates across decades, making geriatric cohorts especially susceptible. Healthcare systems have responded by adding geriatric dermatology divisions and lowering screening thresholds for senior citizens, which fosters earlier-stage identification and improves cost-effectiveness.

High cost of advanced drug therapies & surgeries

Vismodegib and cemiplimab list at USD 13,000 and USD 10,000 per month, respectively, placing them out of reach for many self-pay patients. Mohs micrographic surgery costs 120-370% more than standard excision, even though five-year cure rates exceed 98%. Average per-patient spending rose from USD 1,000 in 2006 to USD 1,600 in 2011 and continues to climb. Market entry lags can span up to seven years in lower-income economies, evidencing affordability and regulatory challenges. Patch-based approaches such as SkinJect target a USD 1,000 price point, aiming to close the affordability gap.

Other drivers and restraints analyzed in the detailed report include:

- AI-driven dermoscopy enabling earlier detection & treatment

- Environmental changes increasing average UV radiation

- Under-diagnosis in primary-care settings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surgical techniques accounted for 36.14% of the basal cell carcinoma treatment market size in 2024, underscoring clinician confidence in wide excision and Mohs micrographic protocols. Mohs utilization expanded 700% from 1992 to 2009, yet premium costs have triggered payer scrutiny. Radiation therapy records 80-92% local-control rates for patients unsuitable for surgery. Photodynamic therapy is the fastest-growing modality at an 11.13% CAGR, buoyed by short healing times and cosmetic advantages. Combination topical regimens-5-fluorouracil plus calcipotriene-now achieve clearance within seven-to-14 days compared with four-week monotherapy. Hedgehog-pathway inhibitors and checkpoint antibodies extend life in advanced cases: cemiplimab delivers 29% objective responses in locally advanced and 21% in metastatic cohorts. Novel oncolytic peptides such as VP-315 yielded 97% overall response and 51% complete histologic clearance in Phase 2, indicating a disruptive non-surgical future.

Second-generation delivery platforms and AI-guided lesion mapping complement these therapeutic shifts. Optical coherence tomography reaches 95.5% accuracy at lesion centers, allowing surgeons to limit excision margins and preserve healthy tissue. Such precision reduces operative stages, accelerating patient throughput and lessening facility costs. As technology penetrates outpatient centers, the basal cell carcinoma treatment market size for photodynamic and topical agents is projected to expand proportionally.

The Basal Cell Carcinoma Treatment Market Report is Segmented by Treatment Type (Surgery [Surgical Excision and More], Radiation Therapy, and More), Disease Stage (Superficial, Nosular, and More), End-User (Hospitals, Specialty Clinics, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America controls 43.58% of the basal cell carcinoma treatment market revenue in 2024 and is positioned for an 8.89% CAGR to 2030. Cutting-edge diagnostics such as FDA-approved DermaSensor widen primary-care capabilities, but high-deductible health plans temper therapy uptake as Mohs costs remain 120-370% above standard excision. Regulatory agility benefits innovators, evidenced by breakthrough designations for cemiplimab and cosibelimab, yet supply-chain fragilities surfaced via EFUDEX shortages from December 2024 to July 2025.

Asia-Pacific is the basal cell carcinoma treatment market's fastest-growing region at 10.36% CAGR. Korea saw cases climb seven-fold from 1999 to 2019, with basal cell carcinoma soaring from 488 to 3,908 diagnoses. Regulatory bodies green-lit canofyMD SCAI AI software at 80.9% accuracy, underscoring tech-forward adoption. Japan's registries show patients aged >= 90 now represent 17% of cases, spotlighting demographic pressure. Differences in histological subtypes mandate region-specific guidelines, as superficial lesions are less frequent than in Western cohorts.

Europe advances at 9.12% CAGR fueled by universal coverage and strict UV-exposure policies. The European Commission approved cemiplimab as the first immunotherapy for advanced basal cell carcinoma, showcasing a receptive regulatory landscape. Photodynamic therapy trials with BF-200 ALA register 90.9% clearance, reinforcing Europe's lead in cosmetically sensitive treatments. Middle East and Africa progress at 9.94% CAGR, catalyzed by expanding private healthcare and governmental trial approvals. The UAE authorized Medicus Pharma's SkinJect microneedle patch trials in May 2025, marking a shift toward local clinical research capacity. Yet rural dermatology access remains sparse, pressing teledermatology platforms into service. South America grows at 9.67% but faces reimbursement hurdles for newer biologics, paving the way for cost-effective generics and remote screening pilots.

- Abbvie

- Bausch Health

- BridgeBio Pharma Inc

- Bristol-Myers Squibb

- Castle Biosciences Inc.

- Eisai

- Roche

- Galderma

- Leo Pharma

- Medicus Pharma Ltd

- Medivir

- Merck

- Novartis

- Perrigo Company

- Pfizer

- Regeneron Pharmaceuticals

- Regeneron Pharmaceuticals

- Sanofi

- Sun Pharmaceuticals Industries

- Taro Pharmaceutical Industries

- Verrica Pharmaceuticals Inc.

- Viatris

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising prevalence of skin cancers

- 4.2.2 Aging population with higher cumulative UV exposure

- 4.2.3 AI-driven dermoscopy enabling earlier detection & treatment

- 4.2.4 Environmental changes increasing average UV radiation

- 4.2.5 Label expansions of Hedgehog-pathway inhibitors

- 4.2.6 Workplace sun-safety legislation boosting screening demand

- 4.3 Market Restraints

- 4.3.1 High cost of advanced drug therapies & surgeries

- 4.3.2 Under-diagnosis in primary-care settings

- 4.3.3 Reimbursement hurdles for checkpoint-inhibitor combinations

- 4.3.4 Safety concerns over long-term Hedgehog-inhibitor toxicity

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Epidemiology Trends

5 Market Size & Growth Forecasts (Value)

- 5.1 By Treatment Type

- 5.1.1 Surgery

- 5.1.1.1 Surgical Excision

- 5.1.1.2 Mohs Micrographic Surgery

- 5.1.1.3 Electrodesiccation and Curettage (ED&C)

- 5.1.2 Radiation Therapy

- 5.1.3 Photodynamic Therapy

- 5.1.4 Cryotherapy

- 5.1.5 Topical Chemotherapy

- 5.1.5.1 5-fluorouracil (5-FU)

- 5.1.5.2 Tirbanibulin

- 5.1.5.3 Imiquimod

- 5.1.6 Oral Medications

- 5.1.7 Intravenous Medications

- 5.1.1 Surgery

- 5.2 By Disease Stage

- 5.2.1 Superficial

- 5.2.2 Nodular

- 5.2.3 Infiltrative

- 5.2.4 Metastatic

- 5.3 By End-User

- 5.3.1 Hospitals

- 5.3.2 Specialty Clinics

- 5.3.3 Ambulatory Surgical Centers

- 5.3.4 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Competitive Benchmarking

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 AbbVie (Allergan)

- 6.4.2 Bausch Health Companies Inc.

- 6.4.3 BridgeBio Pharma Inc

- 6.4.4 Bristol Myers Squibb Co.

- 6.4.5 Castle Biosciences Inc.

- 6.4.6 Eisai Co., Ltd.

- 6.4.7 F. Hoffmann-La Roche AG

- 6.4.8 Galderma S.A.

- 6.4.9 LEO Pharma A/S

- 6.4.10 Medicus Pharma Ltd

- 6.4.11 Medivir AB

- 6.4.12 Merck & Co., Inc.

- 6.4.13 Novartis AG

- 6.4.14 Perrigo Company plc

- 6.4.15 Pfizer Inc.

- 6.4.16 Regeneron Pharmaceuticals Inc.

- 6.4.17 Regeneron Pharmaceuticals Inc.

- 6.4.18 Sanofi S.A.

- 6.4.19 Sun Pharmaceutical Industries Ltd

- 6.4.20 Taro Pharmaceutical Industries Ltd

- 6.4.21 Verrica Pharmaceuticals Inc.

- 6.4.22 Viatris Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment