|

시장보고서

상품코드

1842598

소비자 유전체학 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Consumer Genomics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

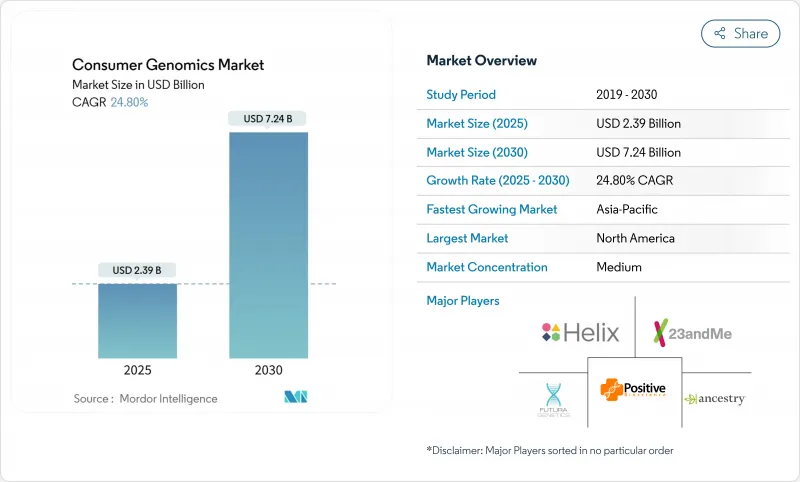

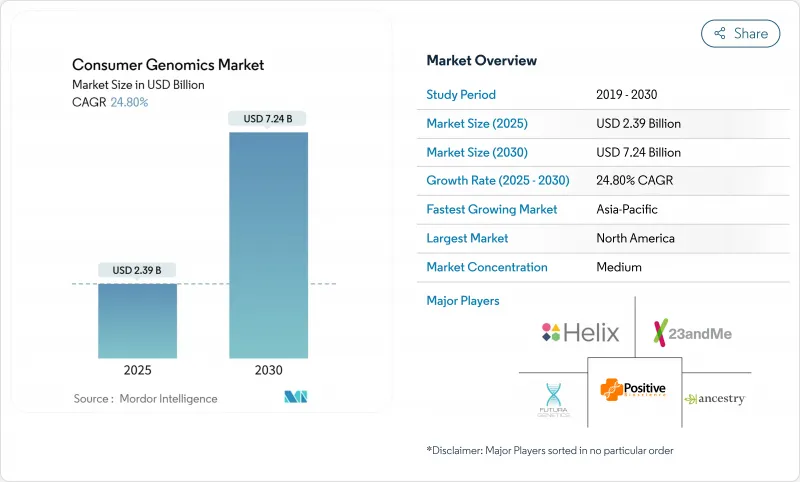

소비자 유전체학 시장은 2025년 23억 9,000만 달러에 이르고, 2030년에는 72억 4,000만 달러에 달할 것으로 예상되며, CAGR은 24.8%를 나타낼 전망입니다.

건강 관리의 디지털화 동향을 반영하여 기존의 의료 경로를 피하고 유전체 정보를 얻는 디지털 소비자의 비율이 증가하고 있습니다. 2021년까지 약 3,500만 명의 미국인이 이미 가정용 키트를 구입했으며 적극적인 건강 관리로의 주류 전환이 강조되었습니다. 현재 가계 검사 서비스는 매출의 38.4%를 차지하고 있지만, 급성장하고 있는 건강, 웰니스, 스포츠 영양 검사는 개별화된 질병 예방의 새로운 길을 열고 있습니다. 일염기 다형(SNP) 제노타이핑은 44.6%의 점유율을 차지하고 지배적인 기술임에 변함이 없지만, 다유전자 리스크 스코어링 분석은 유전체 리스크를 예방 프로그램에 연결하는 보험사와의 제휴를 통해 급속히 확대하고 있습니다. 온라인 채널은 키트 출하의 82.1%를 차지하고 있지만, 건강 데이터의 소비자 소유권을 인정하는 규제 당국의 뒷받침도 있어, 새롭게 형성된 보험 제휴가 가장 급속하게 확대하고 있습니다.

세계의 소비자 유전체학 시장 동향과 인사이트

DTC 키트에 대한 소비자와 의사의 관심 증가

2023년에는 3,300만 건 이상의 검사가 실시되어 유전체 리터러시가 어떻게 일상적인 건강 판단에 영향을 미치는지 보여주었습니다. 의사는 특히 유전 상담이 해석을 지원하는 경우 홈 기반 결과를 예방 의료를위한 대화의 계기로 간주합니다. 소비자의 강화는 데이터를 정확한 다이어트, 운동, 투약 선택으로 변환하는 가계, 약리 유전학 및 질병 소인을 결합한 서비스에 대한 수요에 나타납니다. 클리닉은 DTC 파일을 전자 의료 기록으로 가져와 종단 모니터링을 수행하는 안전한 포털을 통합하여 이러한 추세를 보완합니다. 이 변화는 지속적인 유전체의 참여를 향한 단발 검사에서 행동의 움직임을 뒷받침합니다.

시퀀싱 비용의 지속적인 감소와 기술 진보

최초의 인간 유전체 비용은 30억 달러였습니다. 현재 전체 유전체 시퀀싱 서비스의 가격은 정기적으로 1,000달러 미만이었고, 한때 주류로의 도입을 제한했던 경제적 장벽이 축소되고 있습니다. 차세대 시퀀서는 보다 높은 정밀도와 짧은 실행 시간을 실현하여 신속한 인사이트를 요구하는 소비자의 기대에 따라 1주일 이내의 턴어라운드를 가능하게 합니다. GeneDx는 최근 Fabric Genomics에 5,100만 달러를 지불하고 AI 기반 변형 해석을 통합했습니다. 이러한 진보는 심혈관, 신진 대사 및 종양 질환을 다루는 풍부한 다유전자 점수에 직접 반영됩니다.

데이터 프라이버시 및 사이버 보안 침해

23andMe의 700만 프로파일이 유출된 2023년의 정보 유출 사건은 유전체 보관소가 위험에 처할 때 신뢰가 얼마나 빨리 손상되는지를 입증했습니다. 그 이후 미국 연방 거래위원회는 감시를 강화하고 보안 관행을 거짓으로 설명하거나 고객이 동의를 철회 할 때 원시 DNA 파일을 지우지 않은 기업에 벌금을 부과하고 있습니다. 유전자정보무차별법(Genetic Information Nondiscrimination Act)과 같은 보호법이 있음에도 불구하고 보험에서 유전자차별에 대한 사회적 불안은 여전히 큽니다. 업계 리더들은 현재 회의적인 구매자를 안심시키기 위해 은행 수준의 암호화, 제로 지식 증명 아키텍처, 정기적인 제3자 감사를 중심으로 마케팅을 하고 있습니다.

부문 분석

가계조사 서비스는 2024년 매출의 38.4%를 차지하고 처음으로 키트를 구입하는 사람들에게 조기 진입이 매력적임을 보여주었습니다. 건강, 영양, 스포츠 퍼포먼스 측정법의 보급이 진행되고, 영양 지도, 수면 지도, 개별화 보조 식품을 통합한 프리미엄 제품의 소비자 유전체학 시장 규모가 재형성되고 있습니다. 엘리트와 아마추어 선수들이 유전자형에 적합한 대영양소 비율을 요구하고 있기 때문에 스포츠 영양 검사만으로도 2030년까지의 CAGR은 29.5%를 나타낼 전망입니다. 단발성 질환의 진단 패널도 보인자 스크리닝과 실용적인 생식 상담을 결합하여 지보를 굳히고 있습니다. 소비자는 가계, 형질, 웰니스를 하나의 구독으로 정리한 번들 제품을 점점 선호하게 되어, 단일 목적의 가계도 키트가 서서히 쇠퇴해 나가는 것을 시사하고 있습니다. 모바일 코칭 앱을 포함한 보다 광범위한 디지털 건강 생태계 내에 검사를 배치하는 이해관계자는 단일 판매에서 정기 인사이트로 진화함에 따라 고객의 평생 가치를 강화합니다.

2세대 플랫폼에는 항응고제, 항우울제, 스타틴 등의 대사산물의 상태를 실용적인 투약 조정으로 변환하는 파마코유전체학 모듈이 내장되어 있습니다. 이러한 데이터는 전자 의료 기록에 기재되어 처방이 결정됨으로써 약물 유해 사건이 감소했다고 클리닉으로부터 보고되었습니다. 웰빙 및 진단 클레임에 대한 규제의 명확성은 기능 설계에 계속 영향을 미치고 있지만 초기 증거에 따르면 멀티 카테고리 키트는 납기를 연장하지 않고 더 높은 평균 판매 가격을 보장합니다.

SNP 제노타이핑은 2024년의 키트 판매량의 44.6%를 차지했는데, 비용 효율과 10년에 걸친 정밀도의 실적이 지지되고 있습니다. 그럼에도 불구하고 보험이 지원하는 프로그램은 수십만 개의 변형을 통합하여 복잡한 질병의 지속적인 위험 곡선을 제공하는 다 유전자 위험 점수 엔진으로의 전환을 가속화하고 있습니다. 이 하위 부문은 CAGR 32.4%를 나타내 소비자 유전체학 시장의 다른 어떤 기술 스택을 상회할 것으로 예측됩니다. 전체 유전체 시퀀싱는 1,000달러 미만의 가격 변곡점을 누리고 있으며, Bupa는 300유전자에 걸친 종합적인 보장을 요구하는 일부 가입자를 위한 유전체 웰니스 패키지를 시험적으로 도입하고 있습니다. 마이크로어레이는 과거 참조 라이브러리가 변형 선택에 원활하게 매핑되기 때문에 조상 조사에 계속 적합합니다. 한편, 타겟 시퀀싱 패널은 커버리지의 깊이가 중요한 심혈관과 종양에 특화된 키트로 틈새를 열어줍니다.

클라우드 파이프라인은 원시 리드 정렬, 변형 통화 및 주석이 며칠이 아닌 몇 시간 만에 완료될 때까지 성숙했으며 공급업체는 1자리 수의 납기를 약속할 수 있는 민첩성을 얻었습니다. 컨테이너화된 바이오인포매틱스의 성숙을 통해 소규모 신흥기업은 고가의 On-Premise 인프라를 구축하지 않고 하이퍼스케일러 마켓플레이스에서 용량을 빌릴 수 있게 되어 데이터가 풍부한 분야로의 진입이 민주화되었습니다.

지역 분석

북미는 소비자의 높은 인지도, 성숙한 디지털 결제 인프라, 임상의가 유전체의 의사결정 지원 툴에 익숙해지기 때문에 2024년에 41.7%의 매출을 유지했습니다. 이 지역의 소비자 유전체학 시장 규모는 프라이버시와 데이터 소유권을 둘러싼 소송 위험이 국가별 입법에 의해 완화됨에 따라 계속 확대될 것으로 보입니다. 주요 대학은 킷 벤더와 제휴하여 연구 코호트를 크라우드 소싱하고 무료 또는 할인 가격으로 검사를 제공함으로써 레퍼런스 데이터베이스에 추가 등록 수를 늘리고 있습니다.

CAGR 27.4%를 나타내는 아시아태평양은 주요 확장 프론티어로 눈에 띕니다. 중국, 인도, 동남아시아의 가처분 소득 증가는 생활 습관병 증가와 교차하여 예방적 유전체 위험 평가를 매력적인 가계 지출로 삼고 있습니다. 지방 정부는 소비자의 호기심을 자극하는 국가 유전체 프로젝트에 투자하고 있지만 공급업체는 언어 장애물을 극복하기 위해 컨텐츠를 베이징어, 힌디어 및 바하사어로 현지화합니다. 집에서의 타액 채취는 대도시의 병원의 행렬을 회피할 수 있어, 바쁜 스케줄을 해내는 중류 가정이 편리하고 있습니다.

유럽에서는 진보적인 데이터 권리와 이질적인 시험 규칙이 이율 배반하고 있습니다. 일반 데이터 보호 규칙(General Data Protection Regulation)은 명시적 동의 실천, 다중 요소 인증, 암호화된 전송을 강제하고 컴플라이언스 비용을 증가시키지만 소비자의 신뢰를 높이고 있습니다. 네덜란드와 영국과 같은 국가는 직접 주문을 허용하지만 프랑스는 의료 기관의 모니터링을 의무화하고 있습니다. 공급업체는 현지 법률에 맞게 기능을 활성화하거나 비활성화하는 모듈형 플랫폼을 배포하여 종합적인 확장 전략이 아닌 개별 대응 전략을 보여줍니다. 소비자는 건강 지향 패키지, 특히 지역의 공중 보건 우선순위를 따르는 심혈관계와 대사계의 특징을 통합하는 패키지에 대한 의욕을 높입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 도입

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- DTC 키트에 대한 소비자와 의사의 관심 증가

- 시퀀싱 비용의 지속적인 저하와 기술 진보

- DTC를 지원하는 규제 회랑 확대

- 보험 계획에 있어서의 다유전자 리스크 스코어의 통합

- 소매 약국의 유전체 키오스크와 파트너십

- 블록체인을 활용한 유전체 데이터 수익화 에코시스템

- 시장 성장 억제요인

- 데이터 프라이버시 및 사이버 보안 침해

- 각국 규제의 모호함과 진화

- 채무 초과에 의한 유전자 데이터베이스의 청산

- 과도하게 집중된 인종 데이터셋으로 인한 AI 편향성

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 진입자의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모·성장 예측

- 용도별

- 유전적 관련성

- 진단

- 라이프 스타일, 웰니스 및 영양

- 조상

- 맞춤형 의학 및 약리유전학

- 스포츠 영양 및 건강

- 레크리에이션 특성

- 기타 용도 유형

- 기술별

- 마이크로어레이 유전자형 분석

- 단일염기다형성 유전자형 분석

- 표적 시퀀싱 패널

- 전체 엑솜 시퀀싱(WES)

- 전체 게놈 시퀀싱(WGS)

- 다유전자 위험 점수 분석

- 기타 기술

- 샘플 유형별

- 타액

- 구강 내막 면봉

- 혈액 스팟

- 기타 샘플

- 유통 채널별

- 소비자 직접 판매

- 의사 중개 및 클리닉

- 약국 및 소매

- 건강 및 웰빙 파트너십

- 보험사 파트너십

- 기업 웰니스 프로그램

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- 23andMe

- AncestryDNA

- MyHeritage

- Helix

- Illumina

- Color Genomics

- Veritas Genetics

- Nebula Genomics

- Futura Genetics

- Gene by Gene

- Pathway Genomics

- Xcode Life

- Toolbox Genomics

- CircleDNA

- Dante Labs

- LifeDNA

- Living DNA

- Invitae

제7장 시장 기회와 전망

KTH 25.10.29The consumer genomics market reached USD 2.39 billion in 2025 and is forecast to reach USD 7.24 billion by 2030, advancing to a 24.8% CAGR.

A rising share of digitally engaged consumers now bypasses traditional medical routes to secure genomic insights, reflecting broader healthcare digitization trends. Roughly 35 million Americans had already purchased at-home kits by 2021, underscoring a mainstream shift toward proactive health management. Ancestry services currently account for 38.4% of revenues, yet fast-growing health, wellness, and sports nutrition tests are unlocking new avenues for personalized disease prevention. Single-nucleotide polymorphism (SNP) genotyping remains the dominant technology with a 44.6% share, while polygenic risk-scoring analytics is scaling quickly through insurer alliances that link genomic risk to preventive programs. Online channels capture 82.1% of kit shipments, but newly formed insurance partnerships are expanding fastest, aided by regulatory corridors that recognize consumer ownership of health data.

Global Consumer Genomics Market Trends and Insights

Rising Consumer & Physician Interest in DTC Kits

More than 33 million tests were performed in 2023, illustrating how genomic literacy now influences everyday health decisions. Physicians increasingly view home-based results as a conversation starter for preventive care, especially when genetic counseling supports interpretation. Consumer empowerment is evident in demand for combined ancestry, pharmacogenetic, and disease-predisposition offerings that translate data into precise diet, exercise, and medication choices. Clinics complement this trend by integrating secure portals that import DTC files into electronic health records for longitudinal monitoring. The shift confirms a behavioral move from episodic testing toward continuous genomic engagement.

Continuous Fall in Sequencing Costs & Tech Advances

The first human genome cost USD 3 billion. Today, whole genome sequencing services are regularly priced below USD 1,000, shrinking the economic barrier that once limited mainstream adoption. Next-generation sequencers deliver higher accuracy and shorter run times, enabling week-long turnarounds that align with consumer expectations for rapid insights. GeneDx recently paid USD 51 million for Fabric Genomics to integrate AI-based variant interpretation, a deal that highlights market demand for automated analytics at scale. These advances feed directly into richer polygenic scores covering cardiovascular, metabolic, and oncologic conditions.

Data-Privacy & Cybersecurity Breaches

The 2023 breach that exposed 7 million 23andMe profiles demonstrated how quickly trust can erode when genomic vaults are compromised. The U.S. Federal Trade Commission has since tightened oversight, fining firms that misrepresent security practices or fail to purge raw DNA files when customers withdraw consent. Public anxiety remains acute around genetic discrimination in insurance, despite protections such as the Genetic Information Nondiscrimination Act. Industry leaders now anchor marketing around bank-grade encryption, zero-knowledge proof architectures, and regular third-party audits to reassure skeptical buyers.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Supportive DTC Regulatory Corridors

- Integration Of Polygenic Risk Scores Within Insurance Plans

- Patchy, Evolving Multi-Country Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ancestry services commanded 38.4% of 2024 revenue, illustrating their early mover appeal among first-time kit buyers. Growing penetration of health, nutrition, and sports performance assays is reshaping the consumer genomics market size for premium products that integrate dietary guidance, sleep coaching, and personalized supplements. Sports nutrition tests alone are charting a 29.5% CAGR through 2030 as elite and amateur athletes seek genotype-matched macronutrient ratios. Diagnostic panels for monogenic disorders also gain ground by pairing carrier screening with actionable reproductive counseling. Consumers increasingly prefer bundled offerings that fold ancestry, traits, and wellness into one subscription, suggesting a gradual fade of single-purpose genealogy kits. Stakeholders that position tests within broader digital health ecosystems, including mobile coaching apps, strengthen customer lifetime value as they evolve from one-off sales to recurring insights.

Second-generation platforms now embed pharmacogenomic modules that translate metabolizer status into practical medication adjustments covering anticoagulants, antidepressants, and statins. Clinics report reduced adverse drug events when such data appears in electronic health records ahead of prescribing decisions. Regulatory clarity around wellness versus diagnostic claims continues to influence feature design, yet early evidence indicates multi-category kits secure higher average selling prices without prolonging turnaround times.

SNP genotyping underpins 44.6% of 2024 kit volumes, favored for cost efficiency and a decade-long legacy of accuracy. Even so, insurance-backed programs are accelerating the shift toward polygenic risk-scoring engines that integrate hundreds of thousands of variants to deliver continuous risk curves for complex diseases. This subsegment is expected to expand at a 32.4% CAGR, outpacing any other technology stack inside the consumer genomics market. Whole-genome sequencing enjoys a price inflection point below USD 1,000, prompting Bupa to pilot genomic wellness packages for select enrollees seeking comprehensive coverage across 300 genes. Microarrays remain relevant for ancestry work because historical reference libraries map seamlessly to their variant selection, whereas targeted sequencing panels carve niches in cardiovascular or oncology-focused kits where depth of coverage matters.

Cloud pipelines have matured to the point where raw read alignment, variant calling, and annotation complete in hours rather than days, giving vendors the agility to promise single-digit-day delivery windows. The maturation of containerized bioinformatics also enables smaller upstarts to rent capacity from hyperscaler marketplaces without building expensive on-premise infrastructure, democratizing entrance into data-rich segments.

The Consumer Genomics Market is Segmented by Application (Genetic Relatedness, Diagnostics, and More), Technology (Microarray Genotyping, SNP Genotyping, and More), Sample Type (Saliva, Buccal Swab, and More), Distribution Channel (Direct-To-Consumer, Physician-Mediated & Clinics, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 41.7% revenue in 2024 due to high consumer awareness, mature digital payment infrastructure, and clinician familiarity with genomic decision-support tools. The consumer genomics market size in the region will keep expanding as state-by-state legislative clarity tempers earlier litigation risks surrounding privacy and data ownership. Leading universities frequently partner with kit vendors to crowd-source research cohorts, offering free or discounted tests that funnel additional volume into reference databases.

Asia-Pacific, advancing at a 27.4% CAGR, stands out as the prime expansion frontier. Rising disposable incomes in China, India, and Southeast Asia intersect with escalating lifestyle diseases, making preventive genomic risk assessment an attractive household expenditure. Local governments are investing in national genome projects that stimulate consumer curiosity while suppliers localize content in Mandarin, Hindi, and Bahasa to overcome linguistic hurdles. At-home saliva collection bypasses hospital queues in megacities, a convenience valued by middle-class families balancing busy schedules.

Europe presents a dichotomy of progressive data rights and heterogeneous testing rules. The General Data Protection Regulation forces explicit consent practices, multi-factor authentication, and encrypted transfer, elevating compliance costs but building consumer confidence. Countries like the Netherlands and the UK permit direct ordering, yet France insists on medical oversight. Vendors deploy modular platforms that activate or deactivate features to fit local laws, indicating a tailored rather than blanket expansion strategy. Consumers show a growing appetite for health-oriented packages, especially those integrating cardiovascular and metabolic traits that align with regional public-health priorities.

- 23andMe

- AncestryDNA

- MyHeritage

- Helix

- Illumina

- Color Genomics

- Veritas Genetics

- Nebula Genomics

- Futura Genetics

- Gene by Gene

- Pathway genomics

- Xcode Life

- Toolbox Genomics

- CircleDNA

- Dante Labs

- LifeDNA

- Living DNA

- Invitae

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Consumer & Physician Interest In DTC Kits

- 4.2.2 Continuous Fall In Sequencing Costs & Tech Advances

- 4.2.3 Expansion Of Supportive DTC Regulatory Corridors

- 4.2.4 Integration Of Polygenic Risk Scores Within Insurance Plans

- 4.2.5 Retail-Pharmacy Genomic Kiosks & Partnerships

- 4.2.6 Blockchain-Enabled Genomic Data Monetization Ecosystems

- 4.3 Market Restraints

- 4.3.1 Data-Privacy & Cybersecurity Breaches

- 4.3.2 Patchy, Evolving Multi-Country Regulations

- 4.3.3 Insolvency-Driven Liquidation Of Genetic Databases

- 4.3.4 AI-Driven Bias From Over-Indexed Ethnicity Datasets

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Application

- 5.1.1 Genetic Relatedness

- 5.1.2 Diagnostics

- 5.1.3 Lifestyle, Wellness & Nutrition

- 5.1.4 Ancestry

- 5.1.5 Personalized Medicine & Pharmacogenetics

- 5.1.6 Sports Nutrition & Health

- 5.1.7 Recreational Traits

- 5.1.8 Other Application Types

- 5.2 By Technology

- 5.2.1 Microarray Genotyping

- 5.2.2 SNP Genotyping

- 5.2.3 Targeted Sequencing Panels

- 5.2.4 Whole Exome Sequencing (WES)

- 5.2.5 Whole Genome Sequencing (WGS)

- 5.2.6 Polygenic Risk Scoring Analytics

- 5.2.7 Other Technologies

- 5.3 By Sample Type

- 5.3.1 Saliva

- 5.3.2 Buccal Swab

- 5.3.3 Blood Spot

- 5.3.4 Other Samples

- 5.4 By Distribution Channel

- 5.4.1 Direct-to-Consumer

- 5.4.2 Physician-mediated & Clinics

- 5.4.3 Pharmacies & Retail

- 5.4.4 Health & Wellness Partnerships

- 5.4.5 Insurance Partnerships

- 5.4.6 Corporate Wellness Programs

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 23andMe

- 6.3.2 AncestryDNA

- 6.3.3 MyHeritage

- 6.3.4 Helix

- 6.3.5 Illumina

- 6.3.6 Color Genomics

- 6.3.7 Veritas Genetics

- 6.3.8 Nebula Genomics

- 6.3.9 Futura Genetics

- 6.3.10 Gene by Gene

- 6.3.11 Pathway Genomics

- 6.3.12 Xcode Life

- 6.3.13 Toolbox Genomics

- 6.3.14 CircleDNA

- 6.3.15 Dante Labs

- 6.3.16 LifeDNA

- 6.3.17 Living DNA

- 6.3.18 Invitae

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment