|

시장보고서

상품코드

1842613

나노테크놀러지 약물전달 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Nanotechnology Drug Delivery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

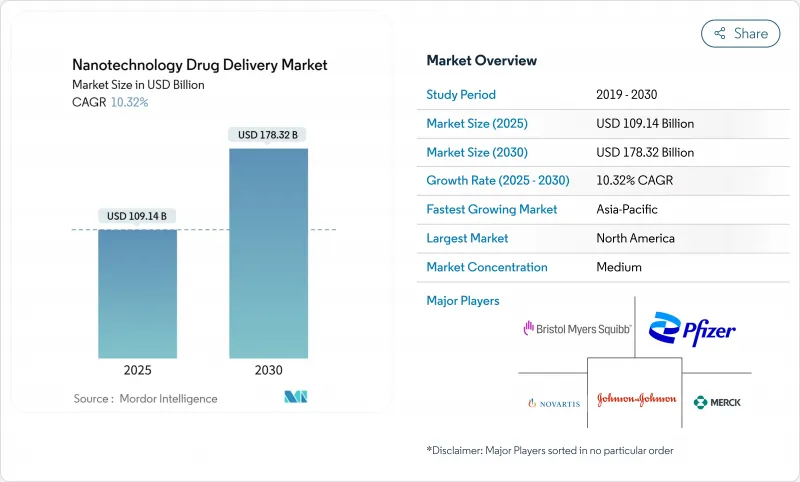

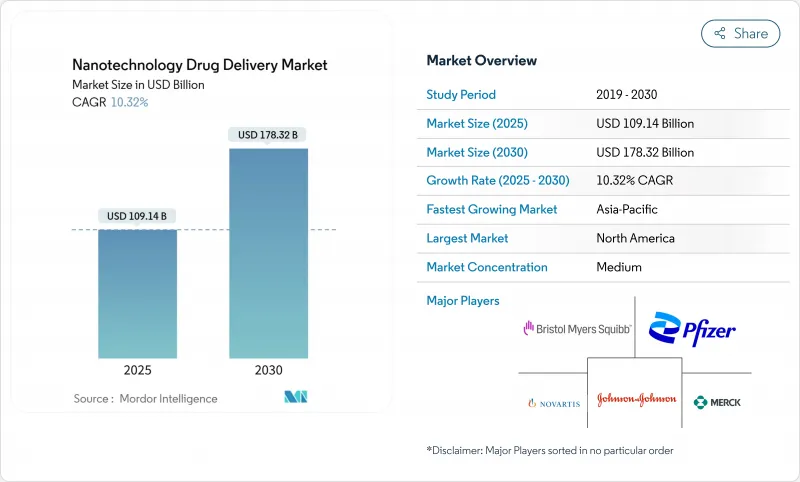

나노테크놀러지 약물전달 시장은 2025년에 1,091억 4,000만 달러가 되고, 2030년에는 1,783억 2,000만 달러에 달하며, CAGR 10.32%를 나타낼 전망입니다.

이 기세는 첨단 제조, 명확한 규제 경로, 나노화된 캐리어가 약물의 표적성 및 안전성 프로파일을 향상시키는 임상적 증명의 축적 사이의 긴밀한 협력을 반영합니다. 이미 수익의 3분의 1을 차지하고 있는 지질 나노입자에 대한 수요가 급증하고, 유전자 의료 및 기타 복잡한 생물학적 제제에 대한 제약 부문의 축족은 성장을 더욱 추진하고 있습니다. 암 영역은 종양의 불균일성에 대처하는 프리미엄으로 정밀 베이스의 제제를 제공업체가 요구하고 있기 때문에 계속 수익의 기둥이 되고 있어, 유전자 치료와 mRNA 프로그램이 확대 페이스를 리드하고 있습니다. 지역별로는 연구개발비 정착과 규제 당국의 움직임 속도에 따라 북미가 리드를 유지하고 있지만, 두꺼운 공적 자금과 급속한 생산 능력 증강을 배경으로 아시아태평양이 급증하고 있습니다. 투여 경로도 다양화되고 있으며, 흡입 디바이스의 개량과 제제 과학이 성막 효율의 향상을 추진하는 가운데, 폐 투여가 정맥 투여의 우위성에 도전하기 시작하고 있습니다. 장기적으로는 제조 노하우가 나노테크놀러지 약물전달 시장에서 중요한 차별화 요인이 되기 때문에 확장 가능한 지질 및 폴리머 시스템을 중심으로 한 플랫폼의 통합이 경쟁력학의 전환을 약속합니다.

세계의 나노테크놀러지 약물전달 시장 동향과 인사이트

암, 유전성 질환, 심혈관 질환의 유병률 상승

암, 희귀 유전성 질환, 만성 심장 질환의 이환율이 가속화되고 있으며, 보다 정확한 투여와 조직 타겟팅을 필요로 하는 환자의 대처 가능한 풀이 확대되고 있습니다. 평균 수명 증가와 진단의 향상이 증례 수를 늘리고, 독물의 유출을 억제하면서 생물학적 장벽을 통과할 수 있는 나노 대응 제제에의 요구를 강화하고 있습니다. 심혈관 치료에서 나노입자는 동맥 경화 플라크를 겨냥하도록 설계되었습니다. 오레곤 주립 대학의 연구자들은 전임상 모델에서 염증 캐스케이드를 진진시키기 위해 나노입자를 사용했는데, 표적화 정밀도가 94% 향상되었음을 보고하고 질병 부담이 구체적인 상업 수요로 바뀌고 있음을 강조하고 있습니다. 한 치료 분야에서의 성공은 인접한 분야에 대한 관심을 불러일으키고, 건강 관리 시스템 전체에 대한 채용 곡선을 가속화하는 경우가 많습니다. 병원 처방전에서 뛰어난 효능과 안전성 기록이 확인됨에 따라 나노제제에 대한 수요가 높아지고, 나노테크놀러지 약물전달 시장의 수익 기반이 강화됩니다.

나노화 생물 제제 및 유전자 치료 파이프라인 성장

메신저 RNA 백신은 지질 나노입자 전달의 상업적 및 규제적 실현 가능성을 검증하고 차세대 유전자 치료를 목적으로 하는 벤처 자금 조달과 전략적 거래 파동을 일으켰습니다. 주요 의약품 제조업체는 학술 연구소와 제휴하여 깨지기 쉬운 분자를 보호하고 엔도솜으로부터의 탈출을 촉진하는 캡슐화 화학물질을 개선하고 있습니다. 화이자와 UT 사우스 웨스턴과의 RNA 페이로드 기술에 대한 공동 연구는 벤치에서 침대 측으로의 전환 시간을 단축하는 것을 목표로 한 공동 연구 모델의 전형적입니다. 보다 많은 후보들이 중간 단계의 임상시험을 클리어함에 따라 규제 당국의 안심감도 높아지고, 승인 리스크가 경감되고, 종양학, 희소질환, 대사성 질환에 걸친 나노기반의 치료제에의 길이 퍼지고 있습니다. 이와 같이 파이프라인의 성장은 전문적인 제조 능력에 대한 수요를 강화하고 나노테크놀러지 약물전달 시장에서 사업을 전개하는 공급업체에게 장기적인 수익 전망을 지원하게 됩니다.

나노 제형의 높은 CMC & GMP 컴플라이언스 비용

나노 약물은 종종 맞춤형 제조 설비, 미립자 모니터링 및 고급 분석이 필요하기 때문에 고정 비용은 기존 주사제를 크게 초과합니다. 입자 크기, 제타 전위 및 표면 화학의 상세한 특성화는 보존 기간 동안 유지되어야 하며 복잡성이 증가하고 있습니다. 나노재료 의약품에 대한 FDA의 2024년 지침은 엄격한 공정 내 시험을 강조하고 있지만, 많은 중소기업들은 그 비용을 비축하기 위해 어려움을 겪고 있습니다. 높은 컴플라이언스 비용은 상시 일정을 늦추고 후속 제제의 개발을 억제하고 나노테크놀러지 약물전달 시장의 확대를 억제할 수 있습니다.

부문 분석

지질 나노입자는 2024년 매출의 32.33%를 차지하며 나노테크놀러지 약물전달 시장의 핵심이 되었습니다. 임상 검증과 호환되는 부형제 공급망이 결합되어 2030년까지 연평균 복합 성장률(CAGR) 예측은 13.23%로 높은 보급률을 유지할 전망입니다. mRNA 백신의 성공 소식은 전체 치료 카테고리의 지질 기반 설계를 정상화하고 CDMO에 전용 라인을 확장하고 장기 계약을 확보하도록 촉구했습니다. 폴리머 시스템은 점유율 2위이지만 만성 요법에서 방출 프로파일의 조절이 뛰어나 멀티페이로드 구조에서 유망시되고 있습니다. 나노크리스탈은 난용성 약물을 위한 공간을 확보하고 있으며, 덴드리머는 합성 부하가 큰데도 다가 리간드 디스플레이에 중점을 둔 연구자들에게 어필하고 있습니다. 양자점은 이미징이라는 틈새 분야를 유지하고 있지만, 중금속 코어에 의한 규제상의 역풍에 직면하고 있습니다. 프로세스의 확장성과 규제 전례는 프론트 러너 플랫폼을 실험적 틈새에서 계속 벗어나 보다 광범위한 나노테크놀러지 약물전달 시장 내 자본 배분에 대한 지침이 될 것으로 보입니다.

2024년 매출의 43.54%는 암 영역이었습니다. 암 치료에서는 보다 높은 투여 강도나 국소적인 방출을 가능하게 하는 혁신이 보상되는 경우가 많기 때문입니다. 화학 치료제의 리포솜 제형은 여전히 영구 수익의 기둥입니다. 유전자 치료와 mRNA의 적응증은 CAGR 13.63%에서 진행되고 있으며, 분자 수준의 개입으로 업계의 이동을 상징하고 있습니다. 신경 영역에서는 혈액 뇌 장벽을 통과하는 나노 캐리어를 이용한 프로그램이 기세를 늘리고 있으며, 류마티스 영역에서는 항염증제의 후보가 서서히 스테로이드의 전신 투여를 대체하고 있습니다. 심혈관계의 임상시험은 여전히 소규모이지만, 플라크를 표적으로 하는 나노입자가 단계 III에서 효과적이면 더욱 확대될 수 있습니다. 이들을 종합하면 나노테크놀러지 약물전달 시장 전체의 현금흐름을 안정시키는 다양한 비즈니스 기회가 탄생하게 됩니다.

지역 분석

북미는 2024년 세계 매출의 39.67%를 차지하며 FDA의 명확한 지침과 벤처 자금조달망의 밀접한 덕분에 인간 최초 임상시험의 자석으로 계속되었습니다. 캐나다는 관대한 R&D 공제와 미국과 자주 협력하는 현실적인 규제 당국을 통해 이 지역의 상황을 강화하고 있습니다. 나노테크놀러지 약물전달 시장은 약물감시를 확보하면서 기술 혁신에 보상하는 예측 가능한 상환제도로부터 이익을 얻고 있습니다.

유럽은 Horizon Europe의 조성금과 학술계와 산업계를 트랜스레이셔널 파이프라인에 연결하는 각국 공동출자에 의해 견인력을 유지하고 있습니다. 독일의 화학 클러스터는 부형제와 계면활성제를 공급하고 베네룩스 지역은 임상시험 인프라를 제공합니다. 중앙 집권적인 조달로 인한 가격 압력에도 불구하고 이러한 특성은 통합되어 견고한 나노테크놀러지 약물전달 시장을 지원합니다.

아시아태평양은 가장 빠르게 성장하는 지역으로 13.03%의 연평균 복합 성장률(CAGR)을 기록하고 공급망을 재구성하고 있습니다. 중국은 cGMP 나노파크에 자금을 공급하고 지원적인 지적재산 개혁을 전개함으로써 비용 효율적인 제조 허브로서의 지위를 확립하고 지역 확대를 지원하고 있습니다. 재료 과학에 뛰어난 일본은 지질과 폴리머 라이브러리를 발전시키고, 한국의 콩그로말리트는 디바이스와 의약품 개발을 통합하여 타임라인을 단축합니다. 인도는 제네릭 나노주사제로 세계 수출 시장을 노리고 있습니다. 이러한 개발은 생산 속도를 향상시키고 나노테크놀러지 약물전달 시장 전체를 활성화시킵니다.

라틴아메리카와 중동은 현재 수익은 소폭이지만 지역 질병 부담에 적합한 고급 제제에 대한 수요가 높아지고 있습니다. 예를 들어, 브라질과 사우디아라비아는 백신과 나노 치료제의 생산을 현지화하려는 의향을 보여주며 미래 시장 성장의 기초를 만들고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 암, 유전성 질환, 심혈관 질환의 유병률의 상승

- 나노화 생물 제제와 유전자 치료의 파이프라인의 성장

- 확장 가능한 지질 나노입자(LNP) 제조의 급속한 진보

- 개별화/정밀투여 플랫폼에 대한 병원 수요

- 프로그램 가능한 나노 캐리어와 자극 응답성 DDS에 대한 벤처 투자

- 정부의 나노 의료 메가 그랜트

- 시장 성장 억제요인

- 나노 제제의 높은 CMC 및 GMP 컴플라이언스 비용

- 불확실한 장기 나노 독성 데이터

- 미세 유체 기반 생산에서 스케일 업의 병목

- 나노제제화된 제네릭 의약품의 한정된 상환 경로

- 가치/공급망 분석

- 규제 상황

- 기술 전망

- Porter's Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모와 성장 예측

- 기술별

- 나노크리스탈

- 고분자 나노입자

- 지질 나노입자/리포솜

- 고분자 미셀

- 덴드리머

- 양자점

- 기타

- 용도별

- 종양학

- 신경학

- 심혈관

- 항염증/면역학

- 항감염

- 안과학

- 기타

- 투여 경로별

- 정맥 주사

- 경구

- 폐

- 경피 및 국소

- 기타

- 최종 사용자별

- 제약 및 바이오테크놀러지 기업

- 계약 연구 및 제조 기관

- 병원 및 클리닉

- 학술 및 연구 기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Pfizer(Wyeth/Liposome Co heritage)

- Bristol Myers Squibb

- Merck Co& Inc

- Novartis

- Johnson & Johnson

- AstraZeneca

- Gilead Sciences

- Nanobiotix

- NanoCarrier

- Taiwan Liposome Co

- BlueWillow Biologics

- NanOlogy

- CytImmune Sciences

- Aquanova AG

- Aphios Corp

- Concept Medical

- Evonik Health Care

- Precision NanoSystems

- CordenPharma

- 20/20 GeneSystems

제7장 시장 기회와 전망

KTH 25.11.05The nanotechnology drug delivery market stood at USD 109.14 billion in 2025 and is on track to reach USD 178.32 billion by 2030, expanding at a 10.32% CAGR.

This momentum reflects tighter alignment between advanced manufacturing, clearer regulatory pathways, and accumulating clinical proof that nano-enabled carriers improve drug targeting and safety profiles. Growth is further propelled by surging demand for lipid nanoparticles, which already account for one-third of revenue, as well as by the pharmaceutical sector's pivot toward genetic medicine and other complex biologics. Oncology continues to anchor revenues as providers seek premium, precision-based formulations that address tumor heterogeneity, while gene therapy and mRNA programs lead the pace of expansion. Regionally, North America keeps its lead thanks to entrenched R&D spending and fast-moving regulators, yet Asia Pacific is rising fastest on the back of generous public funding and rapid capacity build-outs. Routes of administration are also diversifying as pulmonary delivery begins to challenge intravenous dominance amid improved inhalation devices and formulation science driving higher deposition efficiency. Longer term, platform consolidation around scalable lipid and polymer systems promises to shift competitive dynamics as manufacturing know-how becomes a critical differentiator within the nanotechnology drug delivery market.

Global Nanotechnology Drug Delivery Market Trends and Insights

Rising Prevalence of Cancer, Genetic & Cardiovascular Diseases

Accelerating incidence of cancer, rare genetic disorders, and chronic heart conditions is enlarging the addressable pool of patients who need more precise dosing and tissue targeting. Growing life expectancy and better diagnostics add to case volumes, reinforcing the call for nano-enabled formulations that can navigate biological barriers while reducing toxic spillover. In cardiovascular care, nanoparticles are being designed to hone in on atherosclerotic plaques, a capability that broadens therapeutic windows for potent agents. Researchers at Oregon State University reported a 94% jump in targeting accuracy when nanoparticles were used to quell inflammatory cascades in preclinical models, underscoring how disease burden is turning into concrete commercial demand. Successful outcomes in one therapeutic area often spark spill-over interest in adjacent fields, speeding adoption curves across the healthcare system. As hospital formularies observe superior efficacy and safety records, demand for nano-formulations grows, strengthening the revenue base for the nanotechnology drug delivery market.

Growing Pipeline of Nano-Enabled Biologics & Gene Therapies

Messenger RNA vaccines validated the commercial and regulatory feasibility of lipid nanoparticle delivery, triggering a wave of venture funding and strategic deals aimed at next-generation gene therapies. Large drug makers are partnering with academic labs to refine encapsulation chemistries that protect fragile molecules and promote endosomal escape. Pfizer's collaboration with UT Southwestern on RNA payload technologies typifies the collaboration model intended to cut translation times from bench to bedside. As more candidates clear mid-stage trials, comfort within regulatory agencies rises, diminishing approval risk and widening the funnel for nano-based therapeutics across oncology, rare diseases, and metabolic disorders. Pipeline growth thus reinforces demand for specialized manufacturing capacity, supporting longer-term revenue visibility for suppliers operating in the nanotechnology drug delivery market.

High CMC & GMP Compliance Cost for Nano-Formulations

Nano drugs often require bespoke production suites, particulate monitoring, and advanced analytics that push fixed costs well above those of conventional injectables. Detailed characterization of particle size, zeta potential, and surface chemistry must be maintained across shelf life, adding complexity. The FDA's 2024 guidance on nanomaterial drug products emphasizes rigorous in-process testing, which many smaller firms struggle to afford. High compliance costs can delay launch timelines and discourage follow-on formulations, moderating expansion in the nanotechnology drug delivery market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Advances in Scalable Lipid-Nanoparticle Manufacturing

- Hospital Demand for Personalized/Precision Dosing Platforms

- Uncertain Long-Term Nano-Toxicology Data

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lipid nanoparticles generated 32.33% of 2024 revenue and remain the anchor of the nanotechnology drug delivery market. A blend of clinical validation and compatible excipient supply chains keeps adoption high, with a forecast 13.23% CAGR to 2030. News of successful mRNA vaccines normalized lipid-based design across therapeutic categories, prompting CDMOs to expand dedicated lines and secure long-term contracts. Polymeric systems, while second in share, excel at modulating release profiles in chronic therapies and show promise in multi-payload constructs. Nanocrystals are carving a space for poorly soluble drugs, whereas dendrimers appeal to researchers focused on multivalent ligand display despite heavier synthetic workloads. Quantum dots retain an imaging niche but face regulatory headwinds due to heavy-metal cores. Process scalability and regulatory precedent will continue to separate front-runner platforms from experimental niches, guiding capital allocation inside the broader nanotechnology drug delivery market.

Oncology accounted for 43.54% revenue in 2024 because cancer care often rewards innovations that enable higher dose intensities or localized release. Liposomal reformulations of chemotherapeutics remain an enduring revenue stream. Gene therapy and mRNA indications are advancing at 13.63% CAGR, emblematic of the industry's shift toward molecular-level interventions. Neurology programs are gathering momentum by harnessing nano carriers to cross the blood-brain barrier, while anti-inflammatory candidates gradually displace systemic steroids in rheumatoid settings. Cardiovascular trials remain smaller but stand to broaden if plaque-targeting nanoparticles validate in Phase III. Collectively, these tracks create a diversified opportunity set that stabilizes cash flow across the nanotechnology drug delivery market.

The Nanotechnology Drug Delivery Market Report is Segmented by Technology (Nanocrystals, Polymeric Nanoparticles, and More), Application (Oncology, Neurology, Cardiovascular, and More), Route of Administration (Intravenous, Oral, and More), End User (Pharmaceutical and Biotechnology Companies, Contract Research and Manufacturing Organizations, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 39.67% of global revenue in 2024 and remains a magnet for first-in-human studies thanks to clear FDA guidance and dense venture funding networks. Canada bolsters the regional picture with generous R&D credits and pragmatic regulators who often coordinate with their US counterparts. The nanotechnology drug delivery market benefits here from predictable reimbursement systems that reward innovation while ensuring pharmacovigilance.

Europe maintains traction through Horizon Europe grants and national co-funding that knits academia and industry into translational pipelines. Germany's chemical clusters supply excipients and surfactants, while the Benelux region offers clinical trial infrastructure. Together these attributes support a robust nanotechnology drug delivery market despite pricing pressure from centralized procurement.

Asia Pacific is the fastest-growing territory, posting a 13.03% CAGR that is reshaping supply chains. China anchors regional expansion by financing cGMP nano parks and rolling out supportive IP reforms, positioning itself as a cost-effective manufacturing hub. Japan's materials science prowess advances lipid and polymer libraries, whereas South Korea's conglomerates integrate device and drug development to shorten timelines. India targets global export markets with generic nano injectables. These developments collectively increase manufacturing velocity, lifting the overall nanotechnology drug delivery market.

Latin America and the Middle East currently post modest revenue but exhibit growing demand for advanced formulations that fit local disease burdens. Brazil and Saudi Arabia, for example, have signaled intent to localize vaccine and nano-therapeutic production, laying groundwork for future market growth.

- Pfizer (Wyeth/Liposome Co heritage)

- Bristol-Myers Squibb

- Merck Co& Inc

- Novartis

- Johnson & Johnson

- AstraZeneca

- Gilead Sciences

- Nanobiotix

- NanoCarrier

- Taiwan Liposome

- BlueWillow Biologics

- NanOlogy

- CytImmune Sciences

- Aquanova

- Aphios Corp

- Concept Medical

- Evonik Health Care

- Precision NanoSystems

- CordenPharma

- 20/20 GeneSystems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence Of Cancer, Genetic & Cardiovascular Diseases

- 4.2.2 Growing Pipeline Of Nano-Enabled Biologics & Gene Therapies

- 4.2.3 Rapid Advances In Scalable Lipid-Nanoparticle (LNP) Manufacturing

- 4.2.4 Hospital Demand For Personalized/Precision Dosing Platforms

- 4.2.5 Venture Investment In Programmable Nanocarriers & Stimuli-Responsive DDS

- 4.2.6 Government Nanomedicine Mega-Grants

- 4.3 Market Restraints

- 4.3.1 High CMC & GMP Compliance Cost For Nano-Formulations

- 4.3.2 Uncertain Long-Term Nano-Toxicology Data

- 4.3.3 Scale-Up Bottlenecks For Microfluidic-Based Production

- 4.3.4 Limited Reimbursement Pathways For Nano-Formulated Generics

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Technology

- 5.1.1 Nanocrystals

- 5.1.2 Polymeric Nanoparticles

- 5.1.3 Lipid Nanoparticles / Liposomes

- 5.1.4 Polymeric Micelles

- 5.1.5 Dendrimers

- 5.1.6 Quantum Dots

- 5.1.7 Others

- 5.2 By Application

- 5.2.1 Oncology

- 5.2.2 Neurology

- 5.2.3 Cardiovascular

- 5.2.4 Anti-inflammatory / Immunology

- 5.2.5 Anti-infective

- 5.2.6 Ophthalmology

- 5.2.7 Others

- 5.3 By Route of Administration

- 5.3.1 Intravenous

- 5.3.2 Oral

- 5.3.3 Pulmonary

- 5.3.4 Transdermal & Topical

- 5.3.5 Others

- 5.4 By End-user

- 5.4.1 Pharmaceutical & Biotechnology Companies

- 5.4.2 Contract Research & Manufacturing Organizations

- 5.4.3 Hospitals & Clinics

- 5.4.4 Academic & Research Institutes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Pfizer (Wyeth/Liposome Co heritage)

- 6.3.2 Bristol Myers Squibb

- 6.3.3 Merck Co& Inc

- 6.3.4 Novartis

- 6.3.5 Johnson & Johnson

- 6.3.6 AstraZeneca

- 6.3.7 Gilead Sciences

- 6.3.8 Nanobiotix

- 6.3.9 NanoCarrier

- 6.3.10 Taiwan Liposome Co

- 6.3.11 BlueWillow Biologics

- 6.3.12 NanOlogy

- 6.3.13 CytImmune Sciences

- 6.3.14 Aquanova AG

- 6.3.15 Aphios Corp

- 6.3.16 Concept Medical

- 6.3.17 Evonik Health Care

- 6.3.18 Precision NanoSystems

- 6.3.19 CordenPharma

- 6.3.20 20/20 GeneSystems

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment