|

시장보고서

상품코드

1842615

지혈 밸브 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Hemostasis Valve - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

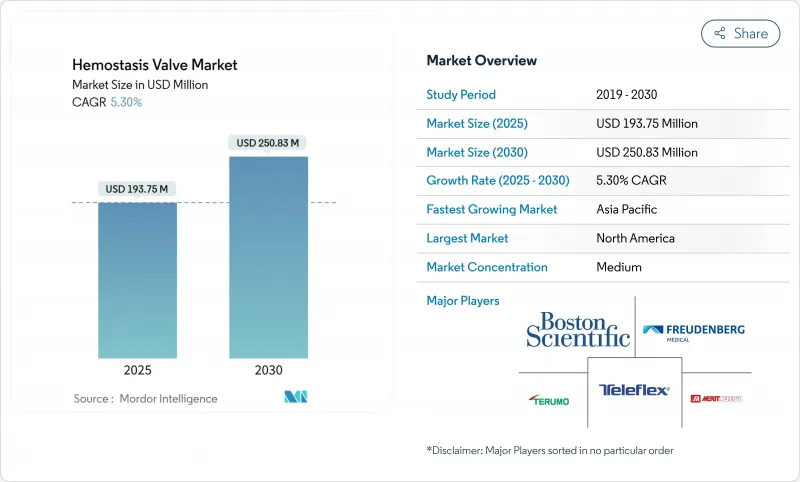

지혈 밸브 시장은 2025년에 1억 9,375만 달러를 창출하고, 2030년에는 CAGR 5.30%를 나타내 2억 5,083만 달러에 이를 것으로 예측되고 있습니다.

보스턴 사이언티픽사가 2025년 1분기에 보고한 인터벤셔널 카디올로지 수술 건수의 20.9% 증가에 따른 성장으로 장비의 견조한 이용을 뒷받침하고 있습니다. 대퇴골 접근에서 요골 접근으로의 지속적인 전환은 더 작은 프렌치 크기로 밀봉의 무결성을 유지하는 얇은 밸브 수요를 촉진합니다. 제품 혁신의 중심은 한 손 조작과 내강 압력을 실시간으로 전달하는 압력 반응형 "스마트"밸브입니다. EU-MDR 재인증과 관련된 규제 비용과 의료용 실리콘의 원재료 부족이 비용 압박 요인이 되고 있지만, 외래에서의 당일 퇴원 프로토콜의 채용이 증가하고 있기 때문에 처리 처리량의 향상을 통해 이러한 장애물을 상쇄할 수 있습니다.

세계의 지혈 밸브 동향과 인사이트

인터벤셔널 심장병학·방사선학 수술의 급증

2025년 1분기 결산에서는 보스턴 사이언티픽의 매출이 전년 동기 대비 20.9% 증가했지만, 이는 카테터 치료 증가에 기인합니다. 복잡한 절차는 여러 번 기구 교체가 필요하기 때문에 출혈을 최소화하는 신뢰성 있는 지혈 밸브의 필요성이 증가하고 있습니다. 오퍼레이터는 현재 고위험 신경 인터벤션에 프리미엄 씰을 선호하고 있으며, 중수막 동맥 색전술의 수는 2029년까지 7만 9,483건에 달할 가능성이 있습니다. 수기 건수 증가는 일회용 밸브의 지속적인 수요에 직결됩니다. 게다가 미국에서는 계속해서 레이디얼 액세스에 대한 상환 제도가 충실하고 있어 밸브의 이용이 유지되고 있습니다. 이러한 요인을 종합하면 예상 CAGR은 1.8포인트 상승합니다.

심혈관 질환과 만성 대사성 질환의 전반적인 부담 증가

연령 표준화된 허혈성 심장병 유병률은 사망률이 감소했음에도 불구하고 여전히 높으며, 환자의 평생 동안 더 많은 인터벤션을 반복하게 됩니다. 아시아에서는 이미 인구 10만명당 722.45례의 심부전이 기록되어 있어 카테터를 이용한 치료의 필요성이 높아지고 있습니다. 고혈압 인구 증가는 전기 생리학적 치료 건수를 더욱 증가시켜 특수 지혈 솔루션의 채용을 뒷받침합니다. 만성 질환 모니터링을위한 반복 절차는 지속적인 성장 궤도를 보장합니다. 신흥 시장을 위한 저가형 디스포저블 키트가 액세스를 확대합니다. 이 복합 효과로 성장 궤도는 1.2포인트 상승합니다.

높은 처리량 검사실에서의 업무 복잡성과 감독의 과제

현재 의사들은 매년 100개가 넘는 절차를 수행하고 있지만, 사례의 복잡성은 증가하고 있으며, 직원의 피로와 방사선 노출의 우려가 높아지고 있습니다. 노동력 부족으로 역량을 유지하기 위한 교육 프로그램이 필요합니다. 실시간 인식 시스템은 자동화를 약속하지만 아직 실험적입니다. 다양한 외장 크기에 대응하는 다양한 밸브의 재고를 유지하는 것은 물류를 복잡하게 만들고 절차를 지연시킬 수 있습니다. 이러한 비즈니스 장애물을 합산하면 예상 CAGR 성장률을 0.7% 낮출 수 있습니다.

부문 분석

지혈 밸브 Y 커넥터는 2024년에 43.35%의 지혈 밸브 시장 점유율을 유지했으며, 진단용 혈관 조영술의 듀얼 포트 액세스에서 역할이 정착되어 있음이 확인되었습니다. 이 분야의 안정성은 반복 구매를 보장하는 방대한 설치 기반의 지원이되었습니다. 그러나 운전자의 피드백은 교환 시간을 단축하기 위해 한 손으로 조작하는 것이 점점 선호되고 있으며, 한 손 지혈 밸브의 급속한 보급 방아쇠가되고 있습니다. 이 변화는 효율 지표를 엄격하게 추적하는 교육 병원 조달 정책에도 영향을 미칩니다.

한 손 밸브는 WATCHDOG 시스템으로 대표되는 고압 하에서도 무결성을 유지하는 크로스 슬릿 씰을 통합합니다. 이중 Y 커넥터는 가이드와이어와 마이크로카테터의 동시 액세스를 필요로 하는 틈새 기술을 대상으로 하며, 통합 연장 라인 밸브는 만성 완전 폐색 절차에 기세를 늘리고 있습니다. 푸시 풀 디자인은 레거시 설정에서 살아남지만 카니버리화에 직면합니다. 높은 듀로미터 실리콘을 포함한 소재의 진보는 장시간의 회전 아테렉토미에 있어서의 밸브의 피로를 경감해, 워크 플로우의 합리화에 열심인 대량 생산 센터에서의 채용을 더욱 뒷받침하고 있습니다.

지역 분석

북미는 2024년 지혈 밸브 시장의 37.82%를 차지했으며, 높은 시술 건수와 선진적인 상환제도에 지지를 받았습니다. 레이디얼 밸브가 널리 채용되어 고령화 사회와 함께 안정된 수요가 유지되고 있습니다. 유럽은 EU-MDR에 대한 대응이 비용면에서의 역풍이 되어, 당면의 성장을 억제할 가능성은 있는 것, 안정된 지출로 이에 계속됩니다.

아시아태평양은 뛰어난 지역이며 국내 제조업체가 지역의 가격 감응도에 맞추어 비용 효율적인 밸브의 생산 규모를 확대하고 있기 때문에 CAGR은 8.31%를 나타낼 전망입니다. 인도네시아와 필리핀에서는 정부 기금을 통한 카테터 실험실의 전개로 데이케이스의 용량이 중요해지고 멸균 사이클을 견딜 수 있는 내구성 있는 밸브에 대한 수요가 생겨나고 있습니다. 일본과 한국은 품질 기준을 계속 설정하고 있으며, 현지 공급업체에게 고정밀 성형 기술의 채용을 촉구하고 있습니다. 이에 따라 아시아태평양의 지혈 밸브 시장 규모는 10년간 약 8,100만 달러로 예측되어 유의미한 점유율 확대가 예상됩니다.

중동 및 아프리카는 사우디아라비아와 아랍에미리트(UAE)에서 시작된 국립 심장병 센터 프로그램을 배경으로 잠재적 가능성을 보여줍니다. 남미는 브라질이 자본 설비의 수입 장벽을 철폐함으로써 점차 전진하고 있지만, 환율 변동이 기세를 약화시키고 있습니다. 이러한 지역을 총칭하면 포화 상태에 있는 신흥국 시장을 헤지하는 다국적 기업에 다양화의 기회를 제공하게 됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 인터벤셔널 심장병학 및 방사선학적 수술의 급증

- 심혈관 질환 및 만성 대사성 질환의 세계 부담 증가

- 저침습 혈관내 수술의 채용 확대

- 레이디얼 액세스와 저프렌치 디바이스로의 급속한 변화가 얇은 밸브 수요 촉진

- 재사용 가능한 키트를 필요로 하는 신흥 경제국에서의 당일치기 카테터 실험실의 급증

- 실시간 모니터링을 가능하게 하는 압력 응답형 스마트 지혈 밸브의 상품화

- 시장 성장 억제요인

- 높은 처리량 카테터 실험실의 운영 복잡성과 감독상의 과제

- 대체 혈관 폐쇄 기술의 이용 가능성

- 의료 등급의 실리콘 및 폴리카보네이트 수지의 불안정한 공급

- EU-MDR Class-Iib/III의 재인증에 따른 비용 상승

- Porter's Five Forces 분석

- 신규 진입자의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모·성장 예측

- 제품 유형별

- 지혈 밸브 Y 커넥터

- 이중 Y 커넥터 밸브

- 한손용 지혈 밸브

- 통합 연장 라인 밸브

- 푸시풀 지혈 밸브

- 기타

- 용도별

- 혈관조영술

- 혈관성형술

- 전기생리학 시술

- 신경중재 시술

- 말초혈관 중재술

- 기타 용도

- 최종 사용자별

- 병원

- 외래 수술 센터(ASC)

- 카테터실

- 전문 클리닉

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Boston Scientific Corporation

- Merit Medical Systems

- Teleflex Incorporated

- Terumo Corporation

- Freudenberg Medical

- Argon Medical Devices

- B. Braun Melsungen AG

- Antmed Corporation

- Abbott Laboratories

- DeRoyal Industries Inc.

- Minivalve International

- Asahi Intecc Co. Ltd.

- Cook Medical

- Medtronic plc

- Nipro Corporation

- Qosina Corp.

- Galt Medical Corp.

- Becton Dickinson & Co.

- Cardionovum GmbH

- Nordson Medical

- Smiths Medical (ICU Medical)

제7장 시장 기회와 전망

KTH 25.10.29The hemostasis valve market generated USD 193.75 million in 2025 and is projected to reach USD 250.83 million by 2030, reflecting a 5.30% CAGR.

Growth accompanies a 20.9% jump in interventional cardiology procedure volumes reported by Boston Scientific in Q1 2025, underscoring robust device utilization. The continuing transition from femoral to radial access drives demand for low-profile valves that maintain seal integrity with smaller French sizes. Product innovation now centers on single-handed operation and pressure-responsive "smart" valves able to relay real-time intraluminal pressure. Regulatory costs tied to EU-MDR re-certification and raw-material shortages of medical-grade silicone pose cost pressures, yet rising adoption of same-day discharge protocols in ambulatory settings offsets these hurdles through higher procedural throughput.

Global Hemostasis Valve Market Trends and Insights

Surging Volume of Interventional Cardiology & Radiology Procedures

Q1 2025 results showed a 20.9% year-over-year sales rise for Boston Scientific attributable to higher catheterization activity. Complex procedures require multiple device exchanges, elevating the need for reliable hemostasis valves that minimize blood loss. Operators now favor premium seals for high-risk neuro-interventions, where middle meningeal artery embolization volumes could hit 79,483 cases by 2029. Increased procedure counts translate directly into recurring demand for disposable valves. In addition, supportive reimbursement schemes in the United States continue to reward radial access, sustaining device utilization. These factors collectively add 1.8 percentage points to the anticipated CAGR.

Rising Global Burden of Cardiovascular & Chronic Metabolic Diseases

Age-standardized ischemic heart disease prevalence remains high even as mortality declines, leading to more repeat interventions over a patient's lifetime. Asia already records 722.45 heart-failure cases per 100,000 population, intensifying catheter-based therapy needs. A growing hypertensive population further drives electrophysiology volumes, pushing adoption of specialized hemostasis solutions. Procedure repetitions for chronic disease monitoring secure a durable growth runway. Lower-cost disposable kits aimed at emerging markets broaden access. The combined effect raises the growth trajectory by 1.2 percentage points.

Operational Complexity & Supervision Challenges in High-Throughput Cath-Labs

Physicians now execute more than 100 procedures each year, but case complexity climbs, raising staff fatigue and radiation exposure concerns. Workforce shortages oblige tailored education programs to sustain competencies. Real-time perception systems promise automation yet remain experimental. Maintaining diverse valve inventories for varied sheath sizes complicates logistics and can delay procedures. Collectively, these operational hurdles shave 0.7 percentage points off expected CAGR growth.

Other drivers and restraints analyzed in the detailed report include:

- Growing Adoption of Minimally-Invasive Endovascular Surgeries

- Rapid Shift to Radial Access & Lower-French Devices

- Availability of Alternative Vascular Closure Technologies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hemostasis Valve Y-Connectors retained a 43.35% hemostasis valve market share in 2024, confirming their entrenched role in dual-port access for diagnostic angiography. The segment's stability underpins a sizable installed base that ensures repeat purchases. Operator feedback, however, increasingly favors single-handed manipulation to cut exchange times, triggering rapid adoption of One-Handed Hemostasis Valves that post a 9.25% CAGR through 2030. The shift influences procurement policies at teaching hospitals where efficiency metrics are closely tracked.

One-Handed valves incorporate cross-slit seals that maintain integrity at elevated pressures, exemplified by the WATCHDOG system. Double Y-Connectors target niche procedures needing simultaneous guidewire and microcatheter access, whereas Integrated Extension-Line valves gain momentum for chronic total occlusion work. Push-Pull designs survive in legacy setups but face cannibalization. Material advances, including high-durometer silicone, reduce valve fatigue during lengthy rotational atherectomy, further boosting adoption among high-volume centers keen on workflow streamlining.

The Hemostasis Valve Market Report is Segmented by Product Type (Hemostasis Valve Y-Connectors, Double Y-Connector Valves, One-Handed Hemostasis Valves, and More), Application (Angiography, Angioplasty, and More), End-User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 37.82% of the hemostasis valve market in 2024, bolstered by high procedural volumes and advanced reimbursement structures. Extensive radial adoption combined with an aging population maintains steady unit demand. Europe follows with consistent spending, although EU-MDR compliance introduces cost headwinds that may temper near-term growth.

Asia-Pacific is the standout, poised for an 8.31% CAGR as domestic manufacturers scale production of cost-effective valves aligned with regional price sensitivities. Government-funded cath-lab rollouts in Indonesia and the Philippines emphasize day-case capacity, creating demand for durable valves that tolerate sterilization cycles. Japan and South Korea continue to set quality benchmarks, spurring local suppliers to adopt high-precision molding technologies. The hemostasis valve market size for Asia-Pacific is therefore projected to close the decade at roughly USD 81 million, representing meaningful share gains.

The Middle East and Africa show latent potential, hinged on national cardiac-center programs emerging in Saudi Arabia and the United Arab Emirates. South America gradually advances as Brazil lifts capital-equipment import barriers, yet currency volatility moderates momentum. Collectively, these regions provide diversification opportunities for multinationals hedging against saturated developed markets.

- Boston Scientific

- Merit Medical Systems

- Teleflex

- Terumo

- Freudenberg

- Argon Medical Devices

- B. Braun

- Antmed

- Abbott Laboratories

- DeRoyal Industries

- Minivalve International

- Asahi Intecc Co. Ltd.

- Cook Group

- Medtronic

- Nipro

- Qosina Corp.

- Galt Medical Corp.

- Becton Dickinson & Co.

- Cardionovum

- Nordson Medical

- Smiths Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Volume of Interventional Cardiology & Radiology Procedures

- 4.2.2 Rising Global Burden of Cardiovascular & Chronic Metabolic Diseases

- 4.2.3 Growing Adoption of Minimally-Invasive Endovascular Surgeries

- 4.2.4 Rapid Shift To Radial Access & Lower-French Devices Boosting Demand For Low-Profile Valves

- 4.2.5 Proliferation of Day-Case Cath-Labs In Emerging Economies Requiring Reusable Kits

- 4.2.6 Commercialization of Pressure-Responsive Smart Hemostasis Valves Enabling Real-Time Monitoring

- 4.3 Market Restraints

- 4.3.1 Operational Complexity & Supervision Challenges In High-Throughput Cath-Labs

- 4.3.2 Availability of Alternative Vascular Closure Technologies

- 4.3.3 Volatile Supply of Medical-Grade Silicone & Polycarbonate Resins

- 4.3.4 Cost Escalation Linked To EU-MDR Class-Iib/III Re-Certification

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Hemostasis Valve Y-Connectors

- 5.1.2 Double Y-Connector Valves

- 5.1.3 One-Handed Hemostasis Valves

- 5.1.4 Integrated Extension-Line Valves

- 5.1.5 Push-Pull Hemostasis Valves

- 5.1.6 Others

- 5.2 By Application

- 5.2.1 Angiography

- 5.2.2 Angioplasty

- 5.2.3 Electrophysiology Procedures

- 5.2.4 Neuro-interventional Procedures

- 5.2.5 Peripheral Vascular Interventions

- 5.2.6 Other Applications

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Catheterization Laboratories

- 5.3.4 Specialty Clinics

- 5.3.5 Other End Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Boston Scientific Corporation

- 6.3.2 Merit Medical Systems

- 6.3.3 Teleflex Incorporated

- 6.3.4 Terumo Corporation

- 6.3.5 Freudenberg Medical

- 6.3.6 Argon Medical Devices

- 6.3.7 B. Braun Melsungen AG

- 6.3.8 Antmed Corporation

- 6.3.9 Abbott Laboratories

- 6.3.10 DeRoyal Industries Inc.

- 6.3.11 Minivalve International

- 6.3.12 Asahi Intecc Co. Ltd.

- 6.3.13 Cook Medical

- 6.3.14 Medtronic plc

- 6.3.15 Nipro Corporation

- 6.3.16 Qosina Corp.

- 6.3.17 Galt Medical Corp.

- 6.3.18 Becton Dickinson & Co.

- 6.3.19 Cardionovum GmbH

- 6.3.20 Nordson Medical

- 6.3.21 Smiths Medical (ICU Medical)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment