|

시장보고서

상품코드

1842619

아포토시스 어세이 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Apoptosis Assay - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

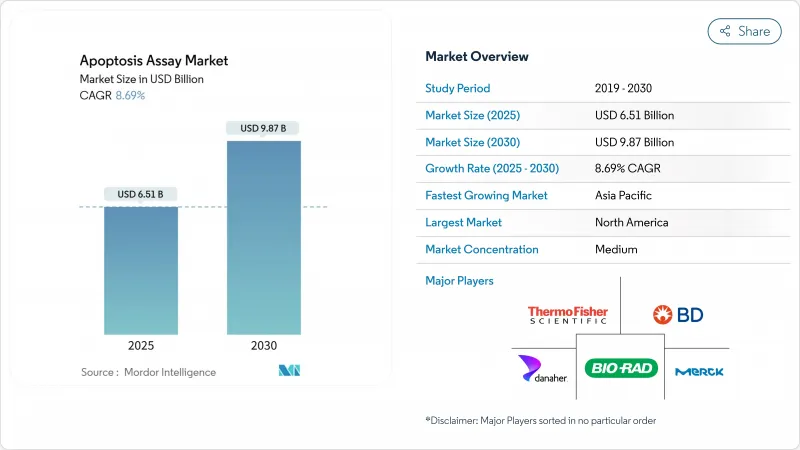

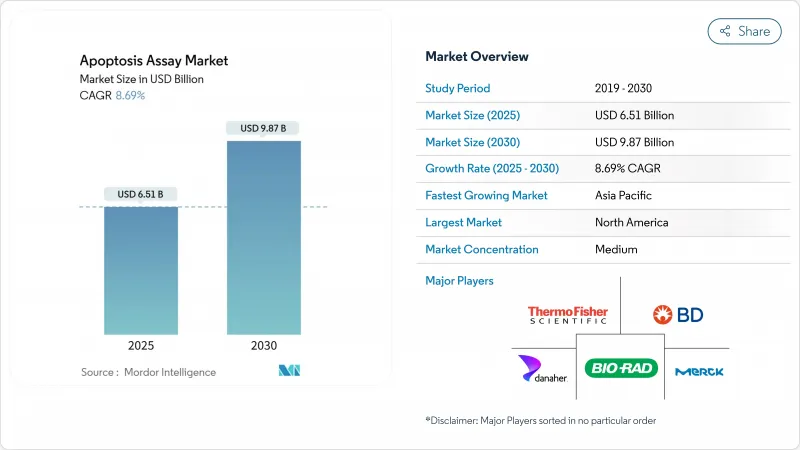

아포토시스 어세이 시장 규모는 2025년에 65억 1,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 8.69%를 나타내, 2030년에는 98억 7,000만 달러에 달할 것으로 예상됩니다.

이 광범위한 성장 호는 정밀 종양학, 면역학 및 재생 의료에서 정량적 세포 사멸 분석의 중심 역할을 뒷받침합니다. 3D 오가노이드 모델이 보급되고, 인공지능 플랫폼이 스크리닝 처리량을 향상시키고, 규제 당국이 검사실 개발 검사 요건을 조화시키면서, 그 보급은 가속화됩니다. 또한 만성질환의 이환율이 상승하고 세포 기반 연구개발에 대한 연방정부의 자금 지원이 지속되고 있는 것도 수요의 추풍이 되고 있습니다. 주요 공급업체는 높은 컨텐츠 이미징, 단일 셀 멀티오믹스, 클라우드 분석을 결합한 통합 워크플로우 솔루션으로 대응하여 스위칭 비용을 높여 차세대 감지 방법의 지적 재산을 강화합니다.

세계의 아포토시스 어세이 시장 동향과 인사이트

만성 질환과자가 면역 질환 증가

만성 질환의 유행은 아포토시스 정량화 수요 곡선을 재형성하고 있습니다. 490만 달러의 RNA Modifications Driving Oncogenesis 이니셔티브와 같은 국립 암 연구소의 보조금은 종양에서 트랜스레이셔널 재프로그래밍을 해독하는 세포사멸 경로 매핑을 우선합니다. 자가면역질환은 조절부전의 세포사가 염증캐스케이드를 유지하기 때문에 더욱 기세가 증가하고 있습니다. 세포 사멸 세포 외 소포의 조사는 암, 허혈성 손상, 염증성 질환에서 면역 조절의 가능성을 보여줍니다. 고령화가 진행되는 가운데 연구실에서는 현재 카스파제 활성, 미토콘드리아 탈분극, 포스파티딜세린 노출을 병행하여 측정하는 멀티플렉스 패널을 도입하여 만성질환의 다인자 생물학과 분석 워크플로우를 정합시키고 있습니다.

아포토시스 조절 치료제의 진보

BCL-2, IAP, MDM2-p53 제어 인자를 표적으로 하는 임상 파이프라인은 정확하고 경로에 특화된 분석이 필요합니다. Ascentage Pharma는 세 가지 클래스 모두에서 활발한 임상시험을 실시했으며 정확한 아포토시스 측정이 상업적으로 중요하다는 것을 보여줍니다. 암 영역 이외에서는 나비토크락스가 결핵에 있어서, 항생물질과 병용하는 것으로 감염 세포의 클리어런스를 촉진해, 숙주 지향성의 작용을 실증하고 있습니다. 따라서 의약품 개발자는 초기 단계의 미토콘드리아 이벤트, 카스파제 캐스케이드, 후기의 DNA 단편화를 단일 워크플로우로 포착하는 분석을 요구하고 있으며, 고콘텐트 이미징 플랫폼과 머신러닝 분석의 구입을 촉진하고 있습니다.

다중 관할구의 엄격한 규제 요건

FDA의 임상 실험실 개발 검사에 대한 최종 규칙은 5단계의 단계적 시행 계획을 적용하여 매년 5억 6,600만 달러에서 35억 6,000만 달러의 컴플라이언스 비용을 늘립니다. 유럽의 ATMP 지침은 세포 치료 분석과 병행하여 GMP 의무를 부과합니다. 따라서 공급업체는 서로 다른 문서 기준을 충족하는 검증 패키지를 설계해야 하며 제품의 상시를 지연시키고 소규모 개발자를 직접적인 상업화보다는 라이선스 제공으로 향하게 합니다.

부문 분석

어세이 키트는 2024년 아포토시스 어세이 시장 매출의 53.09%를 차지했으며, 버퍼, 컨쥬게이트, 컨트롤을 번들한 턴키 프로토콜의 매력이 부각되었습니다. 시약 및 소모품은 규모가 작은 것, CAGR은 9.84%를 나타낼 전망입니다. 이는 고처리량 플랫폼이 대량의 시약을 소비하고 실험실이 프로토콜을 사용자 정의할 수 있기 때문입니다. 장비는 AI 업그레이드와 광학 해상도 향상과 자본 사이클이 일치하기 때문에 완만한 성장이 됩니다.

개별 염료, 형광 형광 기질, 맞춤형 버퍼 세트로의 지출 이동은 공정의 성숙을 보여줍니다. Annexin V-FITC와 APC 접합체는 여전히 주력이며, 2세대 caspase-3/7 기질은 약물 스크리닝의 견인 역할을 하고 있습니다.

유동세포계측법은 단일 세포의 명료성과 다중 매개변수 기능을 통해 2024년 아포토시스 어세이 시장 점유율의 39.67%를 획득했습니다. 플레이트 레벨의 속도가 평가된 분광광도법은 CAGR 10.23%를 나타낼 전망입니다. 고컨텐츠 이미징과 3D 홀로토모그래피는 프리미엄 엔드를 차지하며 오가노이드 연구와 AI 분석에 기여하고 있습니다.

유동세포계측기는 아넥신 V/프로피듐-요오드화물의 이중 염색 프로토콜을 적용하여 초기 및 사후 아포토시스를 결정합니다. 분광광도법 카스파제 분석은 90분 이내에 384-웰 플레이트를 스크리닝할 수 있습니다. 첨단 이미징 시스템은 인공지능 알고리즘을 통합하여 3D 오가노이드 모델에서 세포 사멸의 정량화를 자동화하고 생리 학적으로 적절한 시스템에서 세포 사멸 분석의 복잡성을 해결합니다. 홀로토모그래피를 오가노이드 배양 시스템과 통합함으로써 형광 염색 없이 아포토시스 과정을 실시간으로 관찰할 수 있으며, 이는 중요한 기술적 진보입니다.

지역 분석

북미는 2024년 매출액의 48.06%를 차지했는데, 이는 NIH의 보조금과 견조한 벤처 캐피탈이 첨단 플랫폼의 지속적인 채용을 지원하고 있기 때문입니다. FDA의 실험실 개발 시험 규칙은 연간 35억 1,000만 달러의 이익을 가져오고, 균일한 품질에 대한 기대가 투자의 동기부여가 됩니다. 캐나다의 생명공학 회랑과 멕시코의 수탁 제조 허브가 더욱 성장하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 10.16%를 나타내 가장 급성장하는 지역입니다. 일본은 아포토시스 감시를 필요로 하는 신약 개발 프로그램에 직접 자금을 제공함으로써 생명공학 재생 전략의 규모를 확대하고 있습니다. 한국과 호주는 임상시험 인프라를 확대하고 인도는 시약과 데이터 서비스를 제공하기 위해 연구 위탁을 활용하고 있습니다.

유럽은 제약 대기업과 EU 전체의 연구 네트워크에 견인되어 균형 잡힌 성장을 유지하고 있습니다. EMA에 의한 전이성 대장암에 대한 Fruzaqla의 승인은 이 지역이 견고한 바이오마커 모니터링을 필요로 하는 첨단 치료제에 주력하고 있음을 강조합니다. 유럽 위원회의 생명공학 전략은 현지 생산과 트랜스레이셔널 리서치를 더욱 지원합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 만성 질환 및 자가면역 질환 증가

- 아포토시스 조절 치료제의 진보

- 세포 기반의 연구개발과 정밀의료에 대한 자금 제공 확대

- 하이 스루풋 스크리닝 플랫폼의 주류화

- 아포토시스 정량화를 필요로 하는 싱글 셀·멀티오믹스 워크플로우의 출현

- 이미징 대응 분석을 필요로 하는 3차원 오가노이드 모델로의 이동

- 시장 성장 억제요인

- 여러 법역에 걸친 엄격한 규제 요건

- 고급 검출 장치의 높은 자본 비용과 운영 비용

- 분석 키트 간의 재현성과 표준화의 과제

- 데이터의 신뢰성을 제한하는 생세포 이미징의 광독성 아티팩트

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 진입자의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측

- 제품별

- 분석 키트

- 애넥신 V 기반 분석법

- 카스파제 활성 분석법

- 미토콘드리아 막 전위 분석법

- DNA 단편화 분석법

- 시약 및 소모품

- 기기

- 분석 키트

- 검출 기술별

- 유세포 분석법

- 분광광도계법

- 하이콘텐츠/3D 세포 이미징 시스템

- 기타 기술

- 용도별

- 신약 개발 및 의약품 개발

- 임상 및 진단용

- 줄기세포 및 재생의학 연구

- 기타 용도

- 최종 사용자별

- 제약 및 바이오테크놀러지 기업

- 학술 및 연구 기관

- 병원 및 임상 연구소

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Thermo Fisher Scientific

- Merck KGaA(MilliporeSigma)

- Becton, Dickinson & Co.

- Danaher Corp.(Beckman Coulter, Molecular Devices)

- Bio-Rad Laboratories

- PerkinElmer Inc.

- Sartorius AG(Essen BioScience)

- Bio-Techne Corp.(R&D Systems)

- Promega Corporation

- Agilent Technologies

- Enzo Life Sciences

- Abcam plc

- Tecan Group AG

- Miltenyi Biotec

- BioTek Instruments(Agilent)

제7장 시장 기회와 전망

KTH 25.10.29The Apoptosis Assay Market size is estimated at USD 6.51 billion in 2025, and is expected to reach USD 9.87 billion by 2030, at a CAGR of 8.69% during the forecast period (2025-2030).

This wide growth arc underlines the central role of quantitative cell-death analytics in precision oncology, immunology and regenerative medicine. Uptake accelerates as 3D organoid models gain traction, artificial-intelligence platforms raise screening throughput and regulators harmonize laboratory-developed-test requirements. Demand also benefits from rising chronic-disease prevalence and sustained federal funding for cell-based R&D. Leading suppliers respond with integrated workflow solutions that combine high-content imaging, single-cell multi-omics and cloud analytics, creating higher switching costs and reinforcing the intellectual-property moat around next-generation detection methods.

Global Apoptosis Assay Market Trends and Insights

Rising Incidence of Chronic & Autoimmune Diseases

Chronic-disease prevalence reshapes demand curves for apoptosis quantification. National Cancer Institute grants such as the USD 4.9 million RNA Modifications Driving Oncogenesis initiative prioritize apoptosis pathway mapping to decode translational reprogramming in tumors. Autoimmune disorders add further momentum because dysregulated cell death sustains inflammatory cascades. Research into apoptotic extracellular vesicles shows potential for immune modulation across cancer, ischemic injury and inflammatory diseases. With aging populations, laboratories now deploy multiplex panels that read caspase activity, mitochondrial depolarization and phosphatidylserine exposure in parallel, aligning assay workflows with the multifactorial biology of chronic illness.

Advancements in Apoptosis-Modulating Therapeutics

Clinical pipelines that target BCL-2, IAP and MDM2-p53 regulators require precise, pathway-specific analytics. Ascentage Pharma runs active trials across all three classes, illustrating the commercial stake in accurate apoptosis measurement. Beyond oncology, navitoclax demonstrates host-directed action in tuberculosis by accelerating infected-cell clearance when paired with antibiotics. Drug developers therefore seek assays that capture early-stage mitochondrial events, caspase cascades and late DNA fragmentation within a single workflow, driving purchases of high-content imaging platforms and machine-learning analytics.

Stringent Multi-Jurisdictional Regulatory Requirements

The FDA's final rule for laboratory-developed tests applies a five-stage phased-enforcement plan, adding compliance costs between USD 566 million and USD 3.56 billion each year. European ATMP guidelines impose parallel GMP obligations for cell-therapy analytics. Vendors must therefore design validation packages that meet divergent documentary standards, slowing product launches and nudging smaller developers toward licensing rather than direct commercialization.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Funding for Cell-Based R&D & Precision Medicine

- Mainstream Adoption of High-Throughput Screening Platforms

- High Capital & Operating Cost of Advanced Detection Instruments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Assay kits generated 53.09% of apoptosis assay market revenue in 2024, underscoring the appeal of turnkey protocols that bundle buffers, conjugates and controls. Reagents and consumables, though smaller, are on track for a 9.84% CAGR because high-throughput platforms consume large reagent volumes and allow laboratories to tailor protocols. Instruments post moderate growth as capital cycles align with AI upgrades and optical-resolution gains.

Spending shifts toward individual dyes, fluorogenic substrates and customized buffer sets indicate process maturity. Annexin V-FITC and APC conjugates remain mainstays, while second-generation caspase-3/7 substrates gain drug-screening traction.

Flow cytometry captured 39.67% apoptosis assay market share in 2024 through its single-cell clarity and multi-parameter capability. Spectrophotometry, valued for plate-level speed, is advancing at a 10.23% CAGR. High-content imaging and 3D holotomography occupy the premium end, serving organoid research and AI analytics.

Flow cytometers apply dual-stain Annexin V/propidium-iodide protocols to resolve early versus late apoptosis. Spectrophotometric caspase assays can screen 384-well plates within 90 minutes. Advanced imaging systems are incorporating artificial intelligence algorithms to automate apoptosis quantification in 3D organoid models, addressing the complexity of analyzing cell death in physiologically relevant systems. The integration of holotomography with organoid culture systems enables real-time observation of apoptotic processes without fluorescent staining, representing a significant technological advancement.

The Apoptosis Assay Market Report is Segmented by Product (Assay Kits, Reagents and Consumables, and Instruments), Detection Technology (Flow Cytometry, Spectrophotometry and More), Application (Drug Discovery and Development, and More), End User (Pharmaceutical and Biotechnology Companies, and More) and Geography (North America, Europe and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 48.06% of 2024 revenue as NIH grants and robust venture capital support continuous adoption of advanced platforms. The FDA's laboratory-developed-test rule, offering USD 3.51 billion in annualized benefits, fosters uniform quality expectations that incentivize investment. Canada's biotech corridor and Mexico's contract-manufacturing hubs add incremental growth.

Asia Pacific is the fastest growing region at 10.16% CAGR through 2030. Japan scales its biotech revival strategy with direct funding for drug discovery programs that require apoptosis monitoring. South Korea and Australia expand clinical-trial infrastructure, while India leverages contract research depth to supply reagents and data services.

Europe maintains balanced growth, driven by pharmaceutical heavyweights and pan-EU research networks. The EMA's approval of Fruzaqla for metastatic colorectal cancer underscores the region's focus on advanced therapeutics that demand robust biomarker surveillance. The European Commission's biotechnology strategy further supports local production and translational research.

- Thermo Fisher Scientific

- Merck KGaA (MilliporeSigma)

- Beckton Dickinson

- Danaher Corp. (Beckman Coulter, Molecular Devices)

- Bio-Rad Laboratories

- PerkinElmer

- Sartorius AG (Essen BioScience)

- Bio-Techne Corp. (R&D Systems)

- Promega

- Agilent Technologies

- Enzo Life Sciences

- Abcam

- Tecan Group

- Miltenyi Biotec

- BioTek Instruments (Agilent)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising incidence of chronic & autoimmune diseases

- 4.2.2 Advancements in apoptosis-modulating therapeutics

- 4.2.3 Expanding funding for cell-based R&D & precision medicine

- 4.2.4 Mainstream adoption of high-throughput screening platforms

- 4.2.5 Emergence of single-cell multi-omics workflows needing apoptosis quantification

- 4.2.6 Shift to 3-D organoid models requiring imaging-compatible assays

- 4.3 Market Restraints

- 4.3.1 Stringent multi-jurisdictional regulatory requirements

- 4.3.2 High capital & operating cost of advanced detection instruments

- 4.3.3 Reproducibility & standardisation challenges across assay kits

- 4.3.4 Phototoxicity artefacts in live-cell imaging limiting data reliability

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Assay Kits

- 5.1.1.1 Annexin V-based Assays

- 5.1.1.2 Caspase activity Assays

- 5.1.1.3 Mitochondrial membrane potential Assays

- 5.1.1.4 DNA fragmentation Assays

- 5.1.2 Reagents and Consumables

- 5.1.3 Instruments

- 5.1.1 Assay Kits

- 5.2 By Detection Technology

- 5.2.1 Flow Cytometry

- 5.2.2 Spectrophotometry

- 5.2.3 High-Content / 3-D Cell Imaging Systems

- 5.2.4 Other Technologies

- 5.3 By Application

- 5.3.1 Drug Discovery and Development

- 5.3.2 Clinical and Diagnostic Use

- 5.3.3 Stem-cell and Regenerative Medicine Research

- 5.3.4 Other Applications

- 5.4 By End User

- 5.4.1 Pharmaceutical and Biotechnology Companies

- 5.4.2 Academic and Research Institutes

- 5.4.3 Hospitals and Clinical Laboratories

- 5.4.4 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia & New Zealand

- 5.5.3.6 Rest of Asia Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Thermo Fisher Scientific

- 6.3.2 Merck KGaA (MilliporeSigma)

- 6.3.3 Becton, Dickinson & Co.

- 6.3.4 Danaher Corp. (Beckman Coulter, Molecular Devices)

- 6.3.5 Bio-Rad Laboratories

- 6.3.6 PerkinElmer Inc.

- 6.3.7 Sartorius AG (Essen BioScience)

- 6.3.8 Bio-Techne Corp. (R&D Systems)

- 6.3.9 Promega Corporation

- 6.3.10 Agilent Technologies

- 6.3.11 Enzo Life Sciences

- 6.3.12 Abcam plc

- 6.3.13 Tecan Group AG

- 6.3.14 Miltenyi Biotec

- 6.3.15 BioTek Instruments (Agilent)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment