|

시장보고서

상품코드

1842627

휴대용 산소발생기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global Portable Oxygen Concentrators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

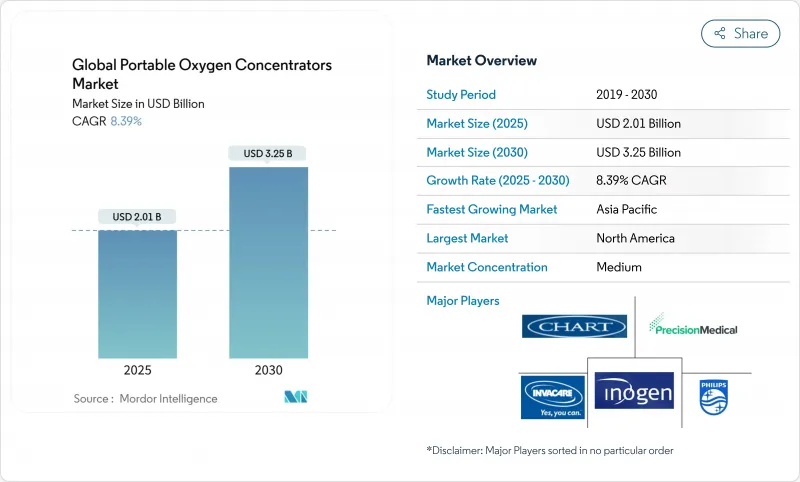

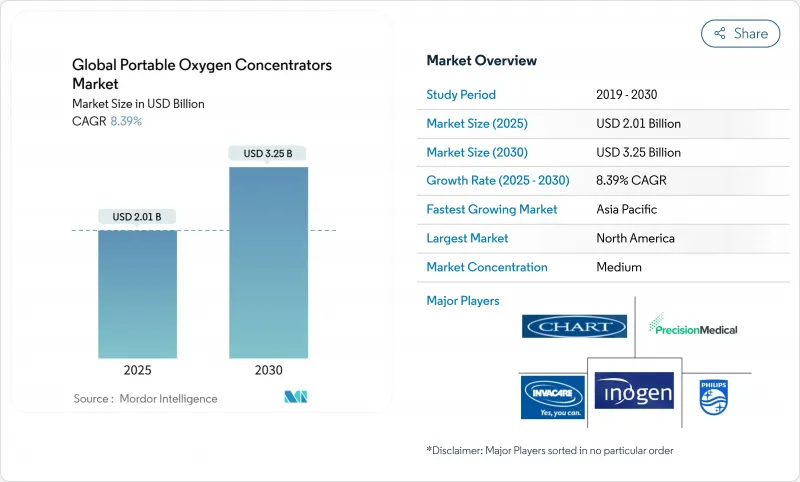

휴대용 산소발생기 시장 규모는 2025년에 20억 1,000만 달러에 이르고, 2030년에는 32억 5,000만 달러에 달하며, CAGR 8.39%를 나타낼 전망입니다.

기기의 소형화, 배터리의 고밀도화, 재택 산소 요법에 대한 폭넓은 상환 제도에 의해 팬데믹의 급성기가 끝난 후에도 수요는 높게 남아 있습니다. Philips 레스피로닉스의 2024년 철수로 2개의 주요 모델이 폐지되어 라이벌의 생산 능력이 개방되어 드라이브 데빌비스 헬스케어의 생산 규모 확대와 GCE 그룹의 신규 출시가 가속화되었습니다. 연속 흐름 장비는 여전히 처방전의 주류를 차지하지만 펄스 흐름 장비는 가벼운 폼 팩터와 더 긴 작동 시간 덕분에 급성장하고 있습니다. 만성 폐색성 폐질환(COPD)이 계속 휴대용 산소발생기 시장의 중심인 반면, COVID 후 호흡 곤란과 웰빙 여행 이용 사례가 고객 기반을 확대하고 있습니다. 중국과 인도가 의료기기 등록을 간소화하고 현지 생산 능력에 투자하고 있기 때문에 아시아태평양이 급성장 지역으로 부상하고 있습니다.

세계의 휴대용 산소발생기 시장 동향과 인사이트

재택 산소 요법에서 상환 확대

2024년 HCPCS 코드 업데이트로 청구가 간소화되고 임상의와 DME 공급업체의 관리 마찰이 줄어들었습니다. 재택 산소가 재입원을 감소시킨다는 증거가 축적됨에 따라 민간보험사도 이 틀을 모방하고 있습니다. COVID-19에서 처음으로 인정되고 현재 영구화된 원격 의료 평가를 통해 농촌과 이동이 어려운 환자는 직접 방문하지 않아도 자격을 얻을 수 있습니다. 이러한 정책 전환은 대응 가능한 환자층을 확대하고 휴대용 산소발생기 시장을 강화합니다.

소형화와 전지 밀도의 비약적 향상

리튬 제올라이트 컬럼은 산소 순도를 향상시키면서 캐니스터 크기를 줄이고, 제조업체는 유량을 손상시키지 않고 장비의 무게를 3파운드 이하로 줄일 수 있습니다. Inogen의 Rove 4는 최대 840ml/분의 산소를 공급하며, 1개의 배터리로 5시간 45분 지속합니다. OXFO 시스템은 임상시험에서 연속 흐름 공급에 비해 92.3%의 산소를 절약했습니다. FAA 호환 전자 장비는 10,000피트까지 고도의 안전한 기내 사용을 가능하게 하여 산소에 의존하는 여행자의 이동 수단의 선택을 넓혔습니다. Arduino 플랫폼에 구축된 실시간 순도 센서는 현재 사용 현황 분석을 제공하고, 예방 유지보수를 지원하며, 장비의 신뢰성을 향상시키고 있습니다.

리튬 이온 배터리 수입 관세

미국은 중국 제품에 125%의 관세를 부과하고 중국제 의료기기의 75%와 많은 POC 배터리 팩에 영향을 미쳤습니다. 병원은 예산의 10.5%를 의료용품에 충당하고 있기 때문에 관세에 의한 가격 인상으로 조달 예산이 핍박합니다. 제조업체는 비용 관리를 위해 조립을 멕시코로 옮겨 이중 조달 전략을 진행하고 있습니다. 이익률 저하를 피하기 위해 이전 가격을 검토하고 관세 평가를 최적화하는 것이 좋습니다. 단기적인 가격 변동은 휴대용 산소발생기 시장의 단기 성장을 둔화시킬 수 있지만, 장기적인 수요 기반은 유지되고 있습니다.

부문 분석

2024년 휴대용 산소발생기 시장 점유율의 53.82%는 연속 흐름 유닛이 차지했으며 휴대용 산소발생기 시장 규모에서 가장 큰 슬라이스를 만들었습니다. 첨단 컴프레서 설계와 고효율 체로 저소음으로 매분 토출 공기 유량이 계속 증가하고 있습니다. 펄스 흐름 장치는 케이싱의 경량화와 호흡 검출 알고리즘의 개선으로 액티브 사용자가 만족하게 되어 CAGR 9.47%를 나타내 성장을 지속하고 있습니다. 배터리 구동 시간이 5시간을 넘어서 펄스 모델은 하루 종일의 원출에도 대응할 수 있게 되었습니다. 업계는 사용자 중심의 설계를 강조하기 때문에 환자는 처방 매개 변수뿐만 아니라 라이프 스타일에 맞는 장비를 선택하게되었습니다.

휴대용 산소발생기 시장에서는 연속 송기와 펄스 송기를 자동으로 전환하는 하이브리드 모드가 출현하고 있습니다. 알고리즘 중심의 펄스 변조는 수면 중에 사용자를 일으키지 않고 산소를 절약하고 고정 시스템과의 임상 갭을 줄입니다. 텍사스 A&M 대학의 연구는 실시간 가속도계 데이터를 기반으로 필요한 유량을 예측하는 머신러닝 모델을 입증하고 수동 조정을 최소화하는 적응형 장치를 예측합니다. 이러한 기술 혁신은 지금까지 무거운 거치형 장비에 의존했던 중등증 환자층에서 휴대용 산소발생기 산업의 발자취를 확대해야 합니다.

COPD는 2024년 휴대용 산소발생기 시장 점유율의 62.67%를 차지했고 장기적인 치료 프로토콜이 확립되어 있기 때문에 휴대용 산소발생기 시장 규모의 중심적인 공헌자가 되었습니다. 여성과 노인의 진단률 상승으로 COPD 분야는 안정적입니다. 호흡 곤란 증후군은 임상 의사가 휴대용 요법을 만성 치료에서 급성기 후 조기 회복으로 확대하기 때문에 CAGR은 가장 빠른 10.06%를 나타낼 전망입니다. COVID 후 섬유증 환자는 간헐적이지만 이동 가능한 산소가 필요하며 새로운 코호트를 늘리고 있습니다.

천식과 간질성 폐 질환은 휴대용 산소발생기 시장에서 중간이지만 중요한 위치를 차지합니다. 현재 섬유화성 ILD 환자의 거의 38%가 산소 요법을 시작하고 있으며, 특히 특발성 폐 섬유증 환자가 많습니다. 2024년에 실시된 무작위화 시험의 증거에 따르면, 24시간 산소 투여와 15시간 산소 투여 사이에 결과의 차이는 없고, 휴대용 산소발생기에 유리한 단시간 투여 요법이 표준이 될 가능성을 시사하고 있습니다. 이러한 발견은 다양한 폐 질환에 대한 휴대용 장치에 대한 의사의 신뢰를 강화시킬 것입니다.

지역별 분석

북미는 휴대용 산소발생기 시장의 2024년 매출액의 43.70%를 차지했고, 메디케어의 예측 가능한 지불 상한과 승인 모델에 의한 국내 공수를 가능하게 하는 종합적인 FAA 규칙에 지지되었습니다. 미국 공급업체는 현재 다기능 호흡기용으로 개정된 CMS-855S 양식 범주에 등록해야 하며 보다 엄격한 모니터링 및 자격 증명 기준을 확보하고 있습니다. 캐나다는 재택 산소에 대한 주 보조금을 확대하고 하위 구성 요소의 국경을 넘어 무역을 촉진하는 반면, 멕시코는 관세의 영향을 받기 쉬운 리튬 이온 어셈블리의 대체 제조 허브로 자리를 잡고 있습니다.

아시아태평양은 CAGR 11.24%를 나타내 가장 급성장하고 있는 지역으로 2030년까지 휴대용 산소발생기 시장 규모에 가장 큰 증가를 가져올 것으로 예상됩니다. 중국은 규제당국이 심사경로를 앞당겼기 때문에 2023년 의료기기 등록건수가 25.4% 급증했습니다. 인도는 2025년까지 의료기기 시장이 500억 달러에 달할 것으로 전망하고 있지만, 아직 기기의 70%를 수입하고 있기 때문에 구미의 기술과 현지 조립을 조합한 합작 사업의 여지가 있습니다. 일본은 고령화 사회가 로봇을 활용한 재택치료와 보조를 맞추어 소형화 기기의 조기 도입을 리드하고 있습니다.

유럽은 의료기기 규제 프레임워크이 안전 기준을 조화시키면서 꾸준한 보급을 보이지만 공급망은 에너지 비용과 원료 인플레이션으로 인한 마진 압력을 느낍니다. 중동 및 아프리카는 걸프 국가가 국가 원격 의료 플랫폼에 투자하고 사하라 이남의 국가들이 유행 교훈에 대응하여 산소 인프라를 구축함에 따라 수요가 증가하고 있습니다. 남미는 완만한 성장을 기록하고, 브라질은 관민 조달의 틀을 활용하여 지방 클리닉에 휴대용 유닛을 공급하고, 아르헨티나는 통화 변동을 상쇄하기 위해 현지 생산을 장려하고 있습니다. 지역의 다양성은 직접 수입, 수탁 제조 및 전략적 파트너십을 결합한 유연한 시장 전략을 필요로 합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 재택 산소 요법에 있어서의 보험 상환의 확대

- 소형화와 배터리 밀도의 비약적 향상

- 만성 호흡기 질환 증가

- 휴대형 산소를 필요로 하는 어드벤처 & 웰니스 여행 증가

- 산소 의존도가 높은 고령화

- COVID 후 재택 장기 산소 요법 수요

- 시장 성장 억제요인

- 유지관리 불량에 의한 세균 오염의 위험

- 장시간의 캐뉼라 사용에 의한 피부에의 악영향

- 리튬 이온 배터리 수입 관세로 BOM 비용 상승

- 저가 POC의 위조품에 의한 브랜드 신용의 저하

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 진입자의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모·성장 예측

- 기술별

- 지속적 유량

- 맥박 유량

- 기타

- 용도별

- 만성 폐색성 폐질환(COPD)

- 천식

- 호흡곤란 증후군

- 기타

- 최종 사용자별

- 병원

- 재택치료

- 외래 수술 센터(ASC)

- 장기 간병 시설

- 응급 의료 서비스(EMS)

- 유통 채널별

- 내구성 의료장비(DME) 판매점

- 소비자 직접 판매(온라인)

- 병원 약국

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Koninklijke Philips NV

- CAIRE Inc.(Chart Industries)

- Inogen Inc.

- Invacare Corporation

- Drive DeVilbiss Healthcare

- ResMed Inc.

- O2 Concepts LLC

- Precision Medical Inc.

- Nidek Medical Products Inc.

- GCE Group

- Besco Medical

- Yuwell Jiangsu Medical

- OxyGo LLC

- Foshan Keyhub Electronic Industries

- Beijing North Star Sci-Tech

- Longfian Scitech

제7장 시장 기회와 전망

KTH 25.10.29The portable oxygen concentrators market size reached USD 2.01 billion in 2025 and is on track to reach USD 3.25 billion by 2030, advancing at an 8.39% CAGR.

Device miniaturization, higher-density batteries, and broader reimbursement for home oxygen therapy are keeping demand high even after the acute phase of the pandemic. Philips Respironics' 2024 withdrawal removed two major models and opened capacity for rivals, accelerating production scale-ups at Drive DeVilbiss Healthcare and new launches from GCE Group. Continuous flow devices still dominate prescriptions, yet pulse flow units are growing fast thanks to lighter form factors and longer runtimes. Chronic Obstructive Pulmonary Disease (COPD) continues to anchor the portable oxygen concentrators market, while post-COVID respiratory distress and wellness travel use cases expand the customer base. Asia-Pacific is emerging as the fastest-growing region as China and India simplify medical-device registration and invest in local production capacity.

Global Portable Oxygen Concentrators Market Trends and Insights

Reimbursement expansion in home oxygen therapy

Medicare caps monthly rentals at 36 months, after which suppliers must keep devices in service for the duration of medical need, giving providers predictable revenue while reducing payer outlays.HCPCS code updates in 2024 simplified billing and trimmed administrative friction for clinicians and DME suppliers. Commercial insurers are mirroring this framework as evidence mounts that home oxygen lowers readmissions. Telehealth assessments, first allowed during COVID-19 and now permanent, let rural or mobility-limited patients qualify without in-person visits. These policy shifts enlarge the addressable patient pool and reinforce the portable oxygen concentrators market.

Miniaturization and battery-density breakthroughs

Lithium-zeolite columns improve oxygen purity while shrinking canister size, letting manufacturers cut device weight below 3 pounds without compromising flow. Inogen's Rove 4 produces up to 840 ml/min and lasts 5 hours 45 minutes on a single battery, reflecting rapid gains in energy efficiency. The OXFO system conserved 92.3% oxygen compared with continuous flow delivery during clinical testing. FAA-compliant electronics allow safe in-flight use up to 10,000 feet, widening mobility options for oxygen-dependent travelers. Real-time purity sensors built on Arduino platforms now deliver usage analytics, supporting preventive maintenance and boosting device reliability.

Import tariffs on lithium-ion cells

The United States imposed 125% duties on Chinese goods, affecting 75% of Chinese-made medical devices and many POC battery packs. Hospitals devote 10.5% of budgets to medical supplies, so tariff-driven price hikes tighten procurement budgets. Manufacturers are moving assembly to Mexico and pursuing dual-sourcing strategies to manage costs. Transfer-pricing reviews and customs-valuation optimization are recommended to avoid margin erosion. Short-run price volatility may slow near-term growth in the portable oxygen concentrators market, yet long-term demand fundamentals remain intact.

Other drivers and restraints analyzed in the detailed report include:

- Rising prevalence of chronic respiratory diseases

- Adventure and wellness travel adoption

- Counterfeit low-cost POCs eroding trust

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Continuous flow units accounted for 53.82% of portable oxygen concentrators market share in 2024 and generated the largest slice of the portable oxygen concentrators market size, supported by clinician preference for uninterrupted delivery during severe hypoxemia. Advanced compressor designs and higher-efficiency sieves continue to raise L per minute output at lower noise levels. Pulse flow devices are posting a 9.47% CAGR as lighter casings and smarter breath-detection algorithms satisfy active users. Battery runtimes exceeding five hours make pulse models viable for day-long excursions. Industry emphasis on user-centric design means patients increasingly select devices that match lifestyle rather than just prescription parameters.

Hybrid modes that switch automatically between continuous and pulse delivery are emerging in the portable oxygen concentrators market. Algorithm-driven pulse modulation conserves oxygen during sleep without waking users, narrowing the clinical gap with stationary systems. Research at Texas A&M demonstrates machine-learning models that predict flow needs based on real-time accelerometer data, foreshadowing adaptive devices that minimize manual adjustments. These innovations should expand the portable oxygen concentrators industry footprint among moderate disease cohorts who previously relied on heavier stationary equipment.

COPD represented 62.67% of portable oxygen concentrators market share in 2024 and formed the core contributor to portable oxygen concentrators market size because of well-established long-term therapy protocols. Rising diagnosis rates in women and aging populations keep the COPD segment stable. Respiratory distress syndrome is registering the fastest 10.06% CAGR as clinicians extend portable therapy beyond chronic care into early post-acute recovery. Post-COVID fibrosis cases require intermittent yet mobile oxygen, adding new cohorts.

Asthma and interstitial lung disease together form a moderate but important slice of the portable oxygen concentrators market. Nearly 38% of fibrosing ILD patients now initiate oxygen therapy, especially those with idiopathic pulmonary fibrosis. Evidence from a 2024 randomized trial suggests no outcome difference between 24-hour versus 15-hour oxygen use, implying shorter dosing regimens that favor portable units could become standard. Such findings are likely to reinforce physician confidence in mobile devices for diverse pulmonary conditions.

The Portable Oxygen Concentrators Market is Segmented by Technology (Continuous Flow, Pulse Flow, Others), by Application (Chronic Obstructive Pulmonary Disease (COPD), Asthma, and More), by End-User (Hospitals, Home-Care Settings, and More), by Distribution Channel (Durable Medical Equipment (DME) Stores, and More), by Sales Channel (Direct Sales, and More), by Geography (North America, Europe, Asia-Pacific, and More).

Geography Analysis

North America generated 43.70% of 2024 revenue for the portable oxygen concentrators market, supported by Medicare's predictable payment ceilings and comprehensive FAA rules that enable unhindered domestic air travel with approved models. U.S. suppliers must now enroll in the revised CMS-855S form category for multifunction respiratory devices, ensuring tighter oversight and credentialing standards. Canada is expanding provincial funding for home oxygen and fostering cross-border trade in subcomponents, while Mexico positions itself as an alternative manufacturing hub for tariff-sensitive lithium-ion assemblies.

Asia-Pacific is the fastest-growing region at an 11.24% CAGR, contributing the largest incremental gain to portable oxygen concentrators market size through 2030. China recorded a 25.4% jump in medical device registrations in 2023 as regulators accelerated review pathways. India expects its medical-device market to hit USD 50 billion by 2025, yet still imports 70% of its devices, creating scope for joint ventures that combine Western technology with local assembly. Japan leads early adoption of miniaturized devices as an aging society aligns with robotics-enabled home care, and South Korea's reimbursement parity with cylinders accelerates POC penetration.

Europe shows steady uptake as the Medical Device Regulation framework harmonizes safety standards, although supply chains feel margin pressure from energy costs and raw-material inflation. Middle East and Africa experience rising demand as Gulf states invest in national telehealth platforms and sub-Saharan countries build oxygen infrastructure in response to pandemic lessons. South America registers moderate growth, with Brazil leveraging public-private procurement frameworks to supply portable units to rural clinics and Argentina encouraging local production to offset currency volatility. Regional heterogeneity necessitates flexible go-to-market strategies that mix direct imports, contract manufacturing, and strategic partnerships.

- Koninklijke Philips

- CAIRE Inc. (Chart Industries)

- Inogen Inc.

- Invacare

- Drive DeVilbiss Healthcare

- Resmed

- O2 CONCEPTS

- Precision Medical

- Nidek Medical Products Inc.

- GCE Group

- Besco Medical

- Yuwell Jiangsu Medical

- OxyGo LLC

- Foshan Keyhub Electronic Industries

- Beijing North Star Sci-Tech

- Longfian Scitech

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Re-imbursement expansion in home oxygen therapy

- 4.2.2 Miniaturisation & battery-density breakthroughs

- 4.2.3 Increasing prevalence of chronic respiratory diseases

- 4.2.4 Growth in adventure & wellness travel requiring portable oxygen

- 4.2.5 Ageing population with higher oxygen-dependency

- 4.2.6 Post-COVID home-based long-term oxygen therapy demand

- 4.3 Market Restraints

- 4.3.1 Risk of bacterial contamination from poor maintenance

- 4.3.2 Adverse dermatological effects from prolonged cannula use

- 4.3.3 Import tariffs on lithium-ion cells raising BOM costs

- 4.3.4 Counterfeit low-cost POCs eroding brand trust

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD million)

- 5.1 By Technology

- 5.1.1 Continuous Flow

- 5.1.2 Pulse Flow

- 5.1.3 Others

- 5.2 By Application

- 5.2.1 Chronic Obstructive Pulmonary Disease (COPD)

- 5.2.2 Asthma

- 5.2.3 Respiratory Distress Syndrome

- 5.2.4 Others

- 5.3 By End-User

- 5.3.1 Hospitals

- 5.3.2 Home-care Settings

- 5.3.3 Ambulatory Surgical Centers

- 5.3.4 Long-Term Care Facilities

- 5.3.5 Emergency Medical Services (EMS)

- 5.4 By Distribution Channel

- 5.4.1 Durable Medical Equipment (DME) Stores

- 5.4.2 Direct-to-Consumer (Online)

- 5.4.3 Hospital Pharmacies

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Koninklijke Philips N.V.

- 6.3.2 CAIRE Inc. (Chart Industries)

- 6.3.3 Inogen Inc.

- 6.3.4 Invacare Corporation

- 6.3.5 Drive DeVilbiss Healthcare

- 6.3.6 ResMed Inc.

- 6.3.7 O2 Concepts LLC

- 6.3.8 Precision Medical Inc.

- 6.3.9 Nidek Medical Products Inc.

- 6.3.10 GCE Group

- 6.3.11 Besco Medical

- 6.3.12 Yuwell Jiangsu Medical

- 6.3.13 OxyGo LLC

- 6.3.14 Foshan Keyhub Electronic Industries

- 6.3.15 Beijing North Star Sci-Tech

- 6.3.16 Longfian Scitech

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-needs Assessment