|

시장보고서

상품코드

1842658

심미치과 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global Cosmetic Dentistry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

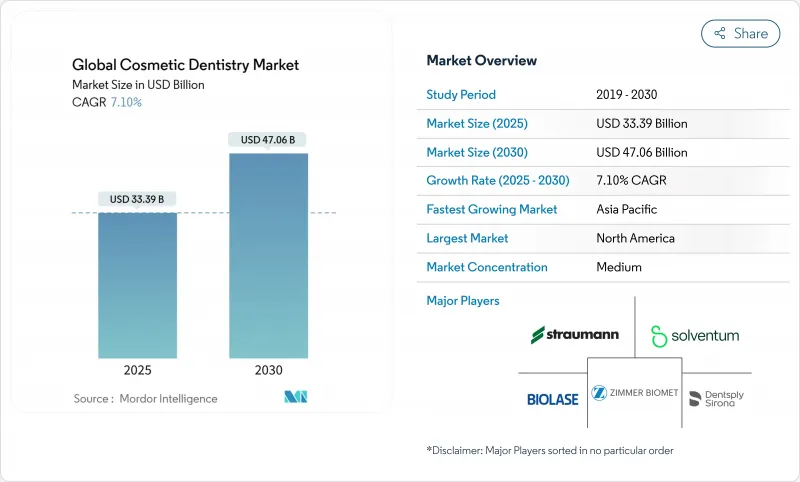

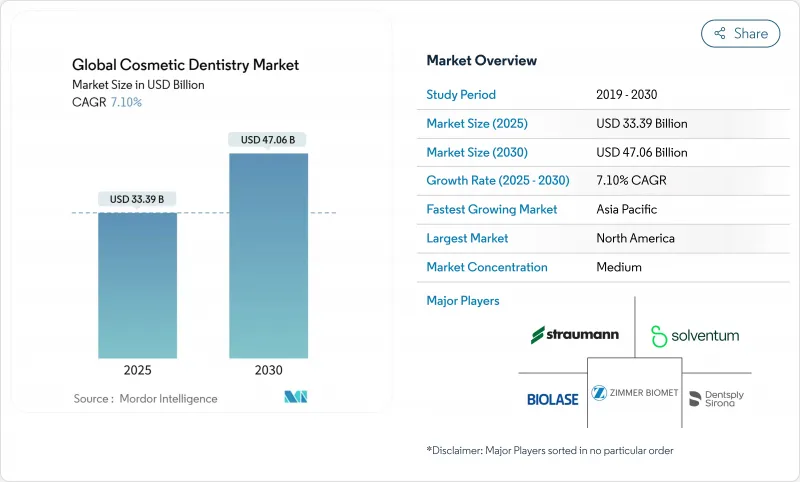

2025년 심미치과 시장 규모는 333억 9,000만 달러, 2030년에는 470억 6,000만 달러에 이를 것으로 예상되며, 예측 기간의 CAGR은 7.10%를 나타낼 전망입니다.

선택적 미소 개선에 대한 수요 증가, 소셜 미디어 시각화를 위한 라이프 스타일의 이동, 의자 사이드 디지털 워크플로우의 급속한 통합이 주요 성장 엔진입니다. 클리어 얼라이너 치료는 형상 기억 폴리머와 AI 가이드 부착 계획이 치료 시간을 단축하기 때문에 CAGR 9.31%를 나타낼 전망입니다. 아시아태평양은 중류 계급의 가처분소득 급증과 디지털 교정치과에 대한 적극적인 클리닉 투자로 CAGR 8.03%를 나타낼 것으로 예상되고, 북미는 수리 코드의 광범위한 보험 채용과 치과 서비스 기관(DSOs)의 치밀한 네트워크로 39.82%의 수익 기반을 유지하고 있습니다. 각 지역에서 수은 규제가 강화되고 아말감에서 세라믹과 복합으로의 전환이 가속화되어 소규모 치과 진료소는 현대화를 촉구하거나 기업 그룹과 제휴하여 CAD/CAM 업그레이드에 자금을 제공해야합니다.

세계의 심미치과 시장 동향과 인사이트

"줌 붐"소셜 미디어 가시성

소비자가 고해상도 화상회의를 접하면 미소에 대한 자기평가가 높아지고 심미치과 상담 건수가 증가하고 있습니다. 2024년 Journal of Dental Sciences의 조사에서는 "Zoom dysmorphia"와 관련된 선택적 문의가 43% 급증한 것으로 기록되었습니다. TikTok 및 Instagram과 같은 동영상 중심 플랫폼은 베니어, 화이트닝, 얼라이너의 변신을 지속적으로 소개하고, 개업의 아웃리치를 확대하고, 선택적 치료를 정상화했습니다. 다운스트림 효과로 동영상을 자주 사용하는 사용자들 사이에서 치아 미백 수요가 42% 증가했고 베니어 상담이 36% 급증했습니다. 인플루언서가 주도하는 마케팅은 현재 잠재고객을 가상 트리아지로 이끌고, 인지부터 예약까지의 사이클을 압축하며, 거시경제 연조에도 불구하고 안정적인 프리미엄 가격을 강화하고 있습니다.

DTC 클리어 얼라이너 플랫폼

DTC 얼라이너 기업은 원격 인상 키트와 가상 모니터를 1,200-3,500달러로 제공하고 사무실에서 3,000-8,000달러 미만으로 떨어지고 있습니다. 이 합리적인 가격으로 성인 교정의 첫 번째 전환이 가능하며 하이브리드 검토 모델을 통합하는 일반 개업의 약속 간격을 채울 수 있습니다. 2024년 스페인의 코호트 연구 (2)에서는 감독 불충분으로 인해 60%의 예상치 못한 보고가 있었으며, 규제 당국은 투명성과 정보화된 콘센트에 중점을 두었습니다. 그럼에도 불구하고, 착용 시간 준수를 추적하는 플랫폼 알고리즘은 활동적인 성인 치과 교정 풀을 확장하여 최초 예측 2년 CAGR에 1.7% 포인트를 기여했습니다.

선택적 심미에 대한 보험 상환 제한

대부분의 치과 의료 급여 제도는 미백, 베니어, 순수한 심미 크라운을 선택적 치료로 분류하고 있기 때문에 중소득자층에서는 보험외 진료에 의한 치료량에 제약이 있습니다. 메디케어는 의료치료와 일체화된 처치에 보험 적용을 제한하고 있으며, 단독 심미교정은 제외하고 있습니다. 그 결과 비용에 민감한 지역 클리닉은 이익률이 낮은 기본 치료를 선호하고 심미 시설에 대한 투자를 늦추고 있습니다. 미국에서는 새로운 정액제 치과 치료 계획이 확대되고 있지만, 보급률은 여전히 15% 미만이며 장기적인 억제요인이 되고 있습니다.

부문 분석

심미치과 시장 규모를 제품별로 보면, 치과용 시스템·기기가 톱으로, 2024년 매출의 34.18%를 나타냈습니다. 클리어 얼라이너는 절대 베이스에서는 작은 것, AI 주도의 스테이징 알고리즘이 예측 가능성을 높이기 위해, CAGR 9.31%를 나타낼 전망입니다. 열 성형된 형상 기억 트레이는 미세 조정을 줄이고 교정 치과 이외의 클리닉에서도 성인의 치료 개시를 촉진하고 있습니다. 반투명성과 내오염성에 있어서의 재료의 혁신에 의해 교환 간격이 연장되어, 제조업체와 개업의의 조리율이 상승하고 있습니다.

복합 수지와 고강도 세라믹의 급속한 보급은 수은 기반 아말감이 세계적으로 규제되었습니다는 사실을 겪고 있습니다. 체어사이드의 지르코니아 블록은 장석질 포셀렌에 필적하는 자연스러운 투광성을 실현해, 실험실에 의존하지 않고 수복 심미성을 높이고 있습니다. 심미치과 시장에서는 임시수복용 3D프린터용 레진의 흡수가 진행되어 치과기공소나 학술센터에서의 온디맨드 워크플로우가 촉진되고 있습니다. 치아 미백 키트는 소매 채널을 통해 관련성을 유지하고 있지만, 사무실에서 레이저 미백이 즉각적인 효능을 중시하는 고급 지향 사용자를 캡처하기 때문에 성장이 완만 해지고 있습니다.

치열 교정은 2024년 심미치과 시장 점유율의 32.67%를 유지하며 이미지에 민감한 성인들 사이에 클리어 얼라이너가 받아들여졌습니다. 그러나 미백, 베니어, 잇몸의 재형성을 포함한 심미적 강화는 낮은 침습 프로토콜이 심리적·경제적 장벽을 낮추기 때문에 CAGR 8.42%를 나타내 가장 급속한 성장을 보이고 있습니다. 디지털 스마일 디자인 플랫폼은 얼굴의 스캐닝과 모형의 오버레이를 융합시켜, 치료 결과를 실시간으로 시각화할 수 있기 때문에 치료의 수용성이 높아집니다.

수복 심미는 규제에 의한 아말감의 단계적 폐지로부터 혜택을 받아 자연적인 투광성을 모방한 접착성 세라믹에 대한 수요가 높아집니다. 모놀리식 지르코니아 풀 아치 브릿지는 뛰어난 강도를 달성하는 동시에 진정한 음영 레이어링을 실현합니다. 구강 스캐너와 교합 분석 소프트웨어의 통합은 조정 약속을 단축하고 보다 이익률이 높은 심미 사례에 의자 시간을 할애할 수 있습니다.

지역 분석

북미는 2024년 세계 매출의 39.82%를 차지하며 견조한 민간보험의 보급과 선택적 강화의 문화적 수용에 지지되었습니다. 미국에서는 CAD/CAM 모듈이 신속하게 채용되어 800개 이상의 오피스 네트워크에서 DSO가 동일한 디지털 워크플로우를 전개하고 있습니다. 캐나다는 규제된 요금 가이드를 반영한 증거 기반 최소한의 준비를 마련하는 접근법을 강조하고 있으며, 멕시코는 미국 동등품보다 60% 저렴한 요금으로 임플란트와 재활을 번들로 한 휴가를 제공함으로써 의료 관광을 활용하고 있습니다.

아시아태평양은 CAGR 8.03%를 나타낼 전망입니다. 중국은 사출 성형 레진 베니아에 대한 도시 중간층의 지출이 급증하고, 인도는 걸프 국가에서 귀국한 외국인 치과의사에 의해 지원되는 비용 효율적인 풀 아치 임플란트 센터로서의 지위를 확립하고 있습니다. 일본과 한국은 CAD 과정을 핵심 커리큘럼에 통합하여 디지털 치과 교육을 선도하고 있습니다. 베트남 등 동남아 시장은 스마트폰 추적 앱과 연동된 프랜차이즈의 얼라이너 숍을 통해 점유율을 늘리고 있습니다.

유럽은 독일, 영국, 프랑스가 2위를 차지하며, 각각 구강내 스캐너의 보급률을 높이고 있습니다. EU의 미나마타 조약 시행에 의해 세라믹의 도입이 가속되고, 국가의 의료 서비스에서는 심미성을 향상시키는 기능성 크라운에 일부 보조금이 지급됩니다. 중동 및 아프리카에서는 부유한 걸프 협력 회의(GCC) 국가에서 꾸준한 도입을 볼 수 있으며, 부유층 환자를 위한 유럽의 고급 기공물을 조달하는 클리닉이 있습니다. 남미 기세의 중심은 브라질이며, 브라질의 확립된 미용 성형 문화는 스마일 메이크업에도 이르렀으며, 인플루언서가 소셜 채널에서 턱 교정과 베니어를 결합한 패키지를 전파하고 있습니다. 라틴아메리카와 아프리카의 농촌에 있어서의 인프라 격차는 치료 건수의 성장을 억제하고 있지만, 모바일 CAD/CAM 유닛이나 휴대용 스캐너의 도입에는 미개척의 기회가 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 스마일 메이크업에 대한 소비자의 욕구를 증폭시키는 소셜 미디어에 의한 "Zoom-Boom" 동향

- 국경을 넘은 덴탈 투어리즘의 비즈니스 모델에 의한 시술 비용의 저하와 액세스의 확대

- 기업 치과 그룹에 의한 의자 사이드 CAD/CAM 시스템의 채용 가속

- 성인의 치열 교정 환자수를 증가시키는 클리어 얼라이너의 소비자용 직접 판매 플랫폼

- 아말감으로부터 세계의 규제 변화에 의한 세라믹 및 복합 수지 수복물의 보급

- 저침습 기술의 등장에 의해 선택적 처치에 대한 환자의 수용이 증가

- 시장 성장 억제요인

- 선택적 치과 심미에 대한 보험 상환은 세계적으로 한정적

- 숙련된 디지털 치과기공사의 부족에 의한 실험실의 처리 능력의 제약

- E-Commerce 플랫폼에 있어서의 화이트닝이나 얼라이너 키트의 위조품의 만연에 의한 환자의 신뢰 저하

- 오피스내 CAD/CAM나 3D프린터에 필요한 고액의 설비 투자가 소규모 진료소의 부담

- 공급망 분석

- 규제 전망

- 기술적 전망

- Porter's Five Forces 분석

- 신규 진입자의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측

- 제품 유형별

- 치과 시스템 및 장비

- 치과 임플란트

- 치과 크라운 및 브릿지

- 교정 장치

- 투명 교정 장치

- 치아 미백 제품

- 치과용 베니어

- 미용 보조 액세서리

- 시술 유형별

- 수복 미용

- 교정 치료

- 보철 재활

- 미적 개선

- 연령층별

- 성인

- 청소년

- 어린이

- 유통 채널별

- 오프라인

- 온라인

- 최종 사용자별

- 치과 진료소

- 치과 병원

- DSO/그룹 진료소

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Align Technology Inc.

- Bego GmbH & Co. KG

- BIOLASE Inc.

- Coltene Holding AG

- Dentsply Sirona Inc.

- Envista Holdings

- GC Corporation

- Henry Schein Inc.

- Institut Straumann AG

- Ivoclar Vivadent AG

- Kuraray Noritake Dental Inc.

- Nobel Biocare Services AG

- Osstem Implant Co. Ltd.

- Planmeca Oy

- Shofu Inc.

- Solventum Corporation

- Sunstar Suisse SA

- Ultradent Products Inc.

- Vatech Co. Ltd.

- Vita Zahnfabrik H. Rauter GmbH

- Young Innovations Inc.

- ZimVie Inc

제7장 시장 기회와 전망

KTH 25.10.29The cosmetic dentistry market size is valued at USD 33.39 billion in 2025 and is projected to reach USD 47.06 billion by 2030, reflecting a 7.10% CAGR over the forecast period.

Rising demand for elective smile enhancements, lifestyle shifts toward social-media visibility, and rapid integration of chairside digital workflows are the primary growth engines. Clear aligner therapy is expanding at a 9.31% CAGR as shape-memory polymers and AI-guided planning shorten treatment times. Asia Pacific is advancing at 8.03% CAGR, driven by surging middle-class disposable incomes and aggressive clinic investment in digital orthodontics, while North America retains a 39.82% revenue foothold through widespread insurance adoption of restorative codes and a dense network of dental service organizations (DSOs). Across regions, tighter mercury regulations hasten the transition from amalgam to ceramic and composite solutions, pressing small practices to modernize or partner with corporate groups to fund CAD/CAM upgrades.

Global Cosmetic Dentistry Market Trends and Insights

"Zoom-Boom" Social-Media Visibility

Consumer exposure to high-resolution video meetings has heightened self-scrutiny of smiles and propelled cosmetic consultation volumes. A 2024 Journal of Dental Sciences study recorded a 43% surge in elective inquiries linked to "Zoom dysmorphia". Video-centric platforms such as TikTok and Instagram continuously showcase veneer, whitening, and aligner transformations, expanding practitioner outreach and normalizing elective treatment. The downstream effect includes a notable 42% rise in teeth-whitening demand and a 36% jump in veneer consultations among high-frequency video users. Influencer-led marketing now funnels prospective patients to virtual triage, compressing the awareness-to-appointment cycle and reinforcing steady premium pricing despite macro-economic softness.

Direct-to-Consumer Clear-Aligner Platforms

DTC aligner companies offer remote impression kits and virtual monitoring priced at USD 1,200-3,500, undercutting in-office ranges of USD 3,000-8,000. This affordability unlocks first-time adult orthodontic conversions and fills appointment gaps for general practitioners who integrate hybrid review models. A 2024 Spanish cohort study[2] reported 60% unmet expectations due to insufficient supervision, placing regulatory focus on transparency and informed consent. Nonetheless, platform algorithms that track wear-time compliance have broadened the active adult orthodontic pool, contributing 1.7 percentage points to CAGR during the first forecast biennium.

Limited Insurance Reimbursement for Elective Aesthetics

Most dental benefit plans classify whitening, veneers, and purely cosmetic crowns as elective, leading to out-of-pocket financing that constrains volume in middle-income segments. Medicare restricts coverage to procedures integral to medical therapies, excluding stand-alone esthetic corrections. Consequently, clinics in cost-sensitive geographies prioritize lower-margin basic care, delaying cosmetic equipment investment. Emerging subscription-style dental plans are expanding in the United States, yet their penetration remains below 15%, sustaining the restraint's long-term drag.

Other drivers and restraints analyzed in the detailed report include:

- Chairside CAD/CAM Adoption by Corporate Groups

- Cross-Border Dental Tourism

- High Capital Requirements for Digital Equipment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The cosmetic dentistry market size for product offerings shows dental systems and equipment at the helm, delivering 34.18% of 2024 revenue. Clear aligners, though smaller in absolute terms, are scaling swiftly with a 9.31% CAGR as AI-driven staging algorithms boost predictability. Thermoformed shape-memory trays reduce refinements, encouraging adults to initiate treatment even in non-orthodontic clinics. Material innovations in translucency and stain resistance are extending replacement intervals, raising gross margins for manufacturers and practitioners alike.

Rapid uptake of composite resins and high-strength ceramics follows global restrictions on mercury-based amalgam. Chairside zirconia blocks achieve natural translucency that rivals feldspathic porcelain, elevating restorative aesthetics without lab dependency. The cosmetic dentistry market continues to absorb 3-D printable resins for temporary restorations, fostering on-demand workflows in DSOs and academic centers. Teeth-whitening kits maintain relevance through retail channels, although growth moderates as in-office laser whitening captures premium seekers who value immediate results.

Orthodontic correction maintained 32.67% of the cosmetic dentistry market share in 2024, anchored by clear aligner acceptance among image-conscious adults. Yet, esthetic enhancement, encompassing whitening, veneers, and gingival re-contouring, exhibits the quickest 8.42% CAGR as minimally invasive protocols lower psychological and financial barriers. Digital smile-design platforms blend facial scanning and mock-up overlays, enabling real-time outcome visualization that lifts treatment acceptance.

Restorative aesthetics benefit from regulatory amalgam phaseouts, lifting demand for adhesive ceramics that mimic natural translucency. Prosthodontic rehabilitation procedures now converge functional and esthetic goals; monolithic zirconia full-arch bridges achieve superior strength while delivering lifelike shade layering. Integration of intraoral scanners with occlusal analysis software reduces adjustment appointments, preserving chair time for higher-margin cosmetic cases.

The Cosmetic Dentistry Market Report is Segmented by Product Type (Dental Systems and Equipment and More), Procedure Type (Restorative Aesthetics and More), Age Group (Adults and More), Distribution Channel (Online and Offline), End-User (Dental Clinics and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 39.82% of global revenue in 2024, supported by robust private insurance penetration and cultural acceptance of elective enhancements. The United States adopts CAD/CAM modules swiftly, with DSOs rolling out identical digital workflows across networks of more than 800 offices. Canada emphasizes evidence-based minimal-preparation approaches, reflective of its regulated fee guides, while Mexico capitalizes on medical tourism through bundled implant-rehabilitation vacations that cost 60% less than U.S. equivalents.

Asia Pacific stands as the growth engine at an 8.03% CAGR. China witnesses a boom in urban middle-class spending on injection-molded resin veneers, while India positions itself as a cost-effective full-arch implant center supported by expatriate dentists returning from Gulf states. Japan and South Korea lead in digital dental education, embedding CAD courses into core curricula. Southeast Asian markets such as Vietnam gain share through franchise aligner shops linked to smartphone tracking apps.

Europe ranks second, propelled by Germany, the United Kingdom, and France, each fostering dense intraoral-scanner adoption rates. EU enforcement of the Minamata Convention accelerates ceramic uptake, while national health services offer partial subsidies for functional crowns that incidentally improve aesthetics. The Middle East & Africa demonstrate steady adoption in affluent Gulf Cooperation Council (GCC) states, where clinics source premium European lab work for high-net-worth patients. South America's momentum centers on Brazil, whose established cosmetic surgery culture extends to smile makeovers, with influencers popularizing combined orthognathic and veneer packages on social channels. Infrastructure gaps in rural Latin American and African markets temper volume growth but present untapped opportunity for mobile CAD/CAM units and portable scanner deployments.

- Align Technology

- Bego GmbH & Co. KG

- BIOLASE Inc.

- Coltene Holding

- Dentsply Sirona

- Envista Holdings

- GC Corporation

- Henry Schein

- Straumann Group

- Ivoclar Vivadent

- Kuraray Noritake Dental Inc.

- Nobel Biocare Services

- Osstem Implant Co. Ltd.

- Planmeca

- Shofu Inc.

- Solventum Corporation

- Sunstar Suisse

- Ultradent Products

- Vatech Co. Ltd.

- Vita Zahnfabrik H. Rauter GmbH

- Young Innovations

- ZimVie

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Social-media "Zoom-Boom" trend amplifying consumer desire for smile makeovers

- 4.2.2 Cross-border dental-tourism business models lowering procedure costs and widening access

- 4.2.3 Accelerated adoption of chairside CAD/CAM systems by corporate dental groups

- 4.2.4 Direct-to-consumer clear-aligner platforms enlarging adult orthodontic patient pool

- 4.2.5 Global regulatory shifts away from amalgam driving ceramic and composite restorative uptake

- 4.2.6 Emergence of minimally-invasive techniques increasing patient acceptance of elective procedures

- 4.3 Market Restraints

- 4.3.1 Limited insurance reimbursement for elective dental aesthetics worldwide

- 4.3.2 Shortage of skilled digital dental technicians constraining laboratory throughput

- 4.3.3 Proliferation of counterfeit whitening and aligner kits on e-commerce platforms eroding patient trust

- 4.3.4 High capital expenditure requirements for in-office CAD/CAM and 3-D printers burden small practices

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry Intensity

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Dental Systems & Equipment

- 5.1.2 Dental Implants

- 5.1.3 Dental Crowns & Bridges

- 5.1.4 Orthodontic Braces

- 5.1.5 Clear Aligners

- 5.1.6 Teeth-Whitening Products

- 5.1.7 Dental Veneers

- 5.1.8 Cosmetic Ancillary Accessories

- 5.2 By Procedure Type

- 5.2.1 Restorative Aesthetics

- 5.2.2 Orthodontic Correction

- 5.2.3 Prosthodontic Rehabilitation

- 5.2.4 Esthetic Enhancement

- 5.3 By Age Group

- 5.3.1 Adults

- 5.3.2 Teenagers

- 5.3.3 Children

- 5.4 By Distribution Channel

- 5.4.1 Offline

- 5.4.2 Online

- 5.5 By End-User

- 5.5.1 Dental Clinics

- 5.5.2 Dental Hospitals

- 5.5.3 DSO / Group Practices

- 5.5.4 Other End-Users

- 5.6 By Geography (Value)

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Product Portfolio Analysis

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Align Technology Inc.

- 6.4.2 Bego GmbH & Co. KG

- 6.4.3 BIOLASE Inc.

- 6.4.4 Coltene Holding AG

- 6.4.5 Dentsply Sirona Inc.

- 6.4.6 Envista Holdings

- 6.4.7 GC Corporation

- 6.4.8 Henry Schein Inc.

- 6.4.9 Institut Straumann AG

- 6.4.10 Ivoclar Vivadent AG

- 6.4.11 Kuraray Noritake Dental Inc.

- 6.4.12 Nobel Biocare Services AG

- 6.4.13 Osstem Implant Co. Ltd.

- 6.4.14 Planmeca Oy

- 6.4.15 Shofu Inc.

- 6.4.16 Solventum Corporation

- 6.4.17 Sunstar Suisse S.A.

- 6.4.18 Ultradent Products Inc.

- 6.4.19 Vatech Co. Ltd.

- 6.4.20 Vita Zahnfabrik H. Rauter GmbH

- 6.4.21 Young Innovations Inc.

- 6.4.22 ZimVie Inc

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment