|

시장보고서

상품코드

1842664

셀룰라이트 치료 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Cellulite Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

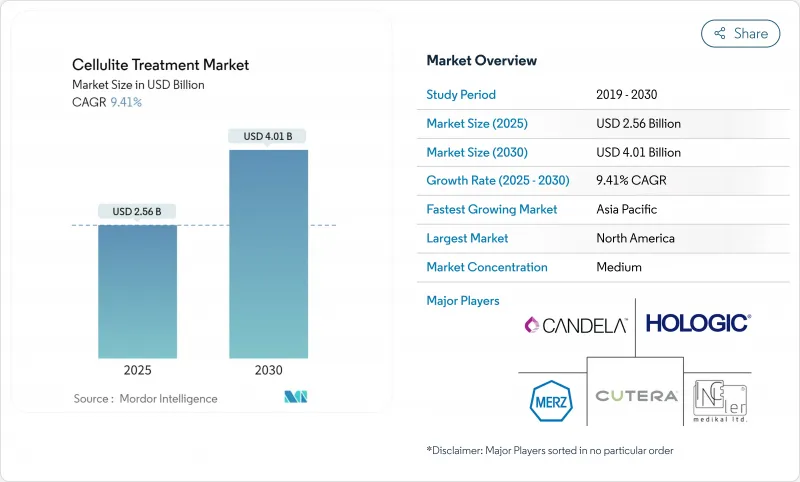

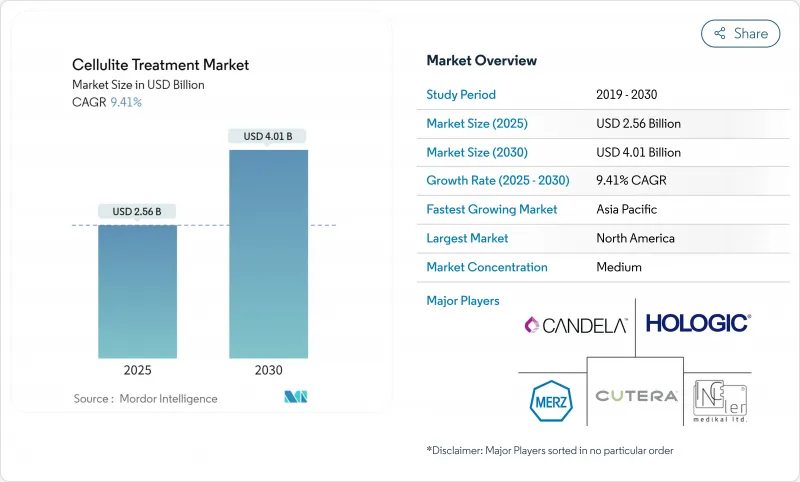

셀룰라이트 치료 시장은 2025년에 25억 6,000만 달러에 이르고, 2030년에는 40억 1,000만 달러로 상승하며, CAGR 9.41%를 나타낼 것으로 예측됩니다.

이 확대는 세계 비만률 상승, AI 대응 에너지 기반 장비 채택 가속화, 미용 시술을 환불하는 기업용 웰니스 패키지로의 꾸준한 이동을 배경으로 한 견조한 환자 수요를 반영합니다. 비침습적인 고주파 및 초음파 시스템은 환자의 가동 중지 시간을 최소화하고 Aveli와 같은 새롭게 FDA 승인된 낮은 침습 플랫폼은 회복 기간을 더욱 단축합니다. 의료 제공업체의 차별화는 이제 치료 프로토콜 데이터 가이드를 통한 개별화에 달려 있으며, 클리닉은 한 세션에서 여러 양식을 결합하여 환자 1인당 수익을 올릴 수 있습니다. 셀룰라이트 치료 시장은 급속한 기기 개발, 시술자 트레이닝 프로그램의 확충, 외견 중시의 치료에 대한 소비자의 의욕이 높아짐에 따라 선진국과 신흥 경제 국가를 불문하고 여러 해에 걸친 확대가 전망되고 있습니다.

세계의 셀룰라이트 치료 시장 동향과 인사이트

세계 비만과 과체중 유병률 상승

비만 지수가 높아지면 눈에 보이는 움푹 들어간 곳을 만드는 진피와 지방의 상호 작용이 강해지고 비만이 셀룰라이트 치료 시장의 주요 촉매가됩니다. 미용 클리닉 전문가의 평가에서 셀룰라이트 환자의 78%가 BMI 상승을 인정하고 중증도 등급과 직접 상관 관계가 있습니다. 과도한 지방은 림프의 흐름을 방해하고 콜라겐의 격벽을 얇게 하기 때문에 시술자는 고주파, 초음파, 주사 가능한 콜라게나아제를 하나의 플랜에 중첩하게 됩니다. 이러한 복합 전략은 높은 가격대를 요구하기 때문에 평균 치료 수입은 사례 수와 함께 증가하고 있습니다. 이 동향은 가공 식품의 소비와 앉기 쉬운 라이프 스타일이 뿌리 깊은 미국과 서유럽에서 특히 두드러지며 의료 제공업체에게 지속적인 임상 파이프라인을 제공합니다.

비 침습적 미용 절차에 대한 선호도 증가

소셜미디어 제창과 점심시간 시술의 주류 수용으로 수요는 비외과적 케어에 크게 기울어지고 있습니다. 업계 단체의 데이터에 따르면 비침습적 바디 콘팅은 2024년에 170억 달러에 달했으며 셀룰라이트 치료가 최전선에 있었습니다. 젊은 층은 위험 허용도가 현저히 낮고 그 날에 일을 재개 할 수있는 에너지 기반 플랫폼이 지원됩니다. 고주파와 고밀도 초점 초음파의 기술적 개선으로, 한때 수술과 표면 치료를 분리했던 효능의 격차가 많이 묻혀 있습니다. 클리닉의 보고에 따르면, 진료의 약 85%가 비침습적인 옵션에 특화되어 있으며, 이는 셀룰라이트 치료 시장을 계속 확대하는 공급자 서비스 믹스의 근본적인 재설계입니다.

신흥 시장에서 낮은 인지도

더 나은 소비력에도 불구하고, APAC 또는 라틴아메리카의 잠재적 환자 중 국소 크림 이외의 셀룰라이트 치료법을 들 수 있는 것은 15% 미만이며, 북미의 67% 브랜드 기대와는 대조적입니다. 전문 교육 프로그램의 부족과 제한된 지역 워크샵은 시술자 채용을 지연시키고 장비 공급업체의 지역 확대를 제한합니다. 그 결과 수요의 격차는 지속적인 교육 캠페인이 견인력을 얻기 전까지 셀룰라이트 치료 시장의 세계 수익 가능성을 깎고 있습니다.

부문 분석

비침습적 플랫폼은 2024년 매출의 48.62%를 차지했으며, 이는 다운타임이 적은 솔루션을 선호하는 소비자의 기호의 증거입니다. 고주파는 더 깊은 열 침투와 표피 위험을 최소화하는 지능형 온도 제어로이 부문을 선도합니다. 고강도 초음파는 실시간 열 이미징이 정확한 에너지 조사를 지원함으로써 그 지위를 확립하고 있습니다. 이러한 개선으로 비침습적 셀룰라이트 치료 시장 규모는 상승세에 있습니다.

낮은 침습성 옵션은 2030년까지 연평균 복합 성장률(CAGR) 10.35%를 나타낼 전망이며 FDA에 의한 Aveli의 인가와 마이크로블레이드를 사용하여 적은 패스 수로 섬유성 격벽을 절단하는 차세대 서브시전 툴에 뒷받침됩니다. QWO가 선구자를 붙인 주사용 콜라게나아제는 약물과 디바이스의 하이브리드라는 틈새 분야를 개척하여 임상의에게 기계적 방출과 동시에 화학적 용해를 제공합니다. 효능 데이터가 축적됨에 따라 클리닉은 시술 메뉴를 다양화하고 셀룰라이트 치료 시장을 특징으로 하는 양식의 수렴을 강화하고 있습니다.

지역 분석

북미는 부유한 환자층, 폭넓은 디바이스의 이용가능성, 혁신적인 플랫폼에 대한 규제 당국의 투명성이 높은 경로를 통해 2024년 매출에서 42.19%의 선두를 유지했습니다. 이 지역에서는 2023년에 약 1,600개의 메디컬 스파가 추가되어 시술에 대한 액세스 포인트가 증가했습니다. 미용서비스를 환불하는 기업의 복리후생제도는 허영심에 의한 소비를 넘어 수요를 확대하고 다양한 직원층에 걸쳐 셀룰라이트 치료 시장을 확대하고 있습니다.

유럽은 독일, 프랑스, 영국을 중심으로 기술적으로 성숙한 지역입니다. 유럽 의약청(EEA)의 엄격한 임상 데이터 요구사항은 자본 장애물을 높이고 있지만 일단 클리어하면 의료기기는 의사의 신뢰와 대규모 민간 지불 시장에서 이익을 얻을 수 있습니다. 셀룰라이트 치료와 피부 타이트닝과 지방 감소를 결합한 다중 양식 포장은 일반적이며 교차 판매를 지원하고 환자 1인당 지갑 점유율을 높입니다. 지적 재산권 보호와 견고한 임상시험 네트워크는 미국과 아시아 제조업체를 유럽 제휴에 계속 끌어들이고 셀룰라이트 치료 산업의 생태계를 풍부하게 만듭니다.

아시아 태평양 지역은 중산층 확대와 소셜 미디어로 촉진된 미적인식에 힘입어 2030년까지 연평균 11.34%의 가장 높은 성장률을 나타낼 전망입니다. 중국의 Tier-1 도시에서는 고급 미용 클리닉이 연간 2자리 성장하고 인도의 메트로 허브에서는 의료 관광객을 유치하기 위해 AI가이드 RF 시스템에 투자하고 있습니다. 한국은 여전히 기술 혁신의 깃발이며 특허에 뒷받침된 핸드피스와 라이선스가 부여된 알고리즘을 세계에 수출하고 있습니다. 한편, 휴가 여정에 번들된 가격 경쟁력 있는 패키지는 외국인 환자를 태국과 말레이시아 병원으로 유도하여 이 지역의 셀룰라이트 치료 시장 규모를 확대하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계의 비만과 과체중의 유병률 상승

- 비침습적인 미용 시술에의 기호 고조

- 에너지 기반 기기의 기술 진보

- 가처분 소득 증가와 미용 의식 증가

- Ai 주도의 개별 치료 프로토콜

- 기업의 웰니스·스텝

- 시장 성장 억제요인

- 신흥 시장에서의 낮은 인지도

- 고액의 시술 비용과 한정된 상환

- 기기의 안전성에 관한 규제 강화

- 위조 가정용 기기의 확산

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모·성장 예측

- 시술별

- 비침습적 시술

- 고주파 기반

- 레이저 기반

- 초음파 기반

- 음향파

- 냉동지방분해술

- 저침습

- 서브시전

- 주사형 콜라게나제

- 레이저 보조 지방분해술

- 국소

- 레티놀 크림

- 카페인 크림

- 펩티드계 제형

- 비침습적 시술

- 셀룰라이트 유형별

- 연성 셀룰라이트

- 경성 셀룰라이트

- 부종성 셀룰라이트

- 최종 사용자별

- 병원

- 피부과 전문 클리닉

- 메디컬 스파 및 뷰티 센터

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Hologic Inc.

- Candela Corporation

- Cutera Inc.

- Merz Pharma GmbH & Co KGaA

- Allergan Aesthetics(AbbVie)

- Sisram Medical(Alma Lasers)

- Venus Concept Inc.

- BTL Aesthetics

- Endo International plc(Qwo)

- Lumenis Ltd.

- Sciton Inc.

- Fotona doo

- Lutronic Corporation

- Zimmer Aesthetics

- Cynosure LLC

- Inceler Medikal Co. Ltd.

- Beijing Nubway S&T Co. Ltd.

- cymedics GmbH & Co KG

- BeautyBio Inc.

- Tanceuticals LLC

- Solta Medical

제7장 시장 기회와 전망

KTH 25.10.30The cellulite treatment market reached USD 2.56 billion in 2025 and is forecast to climb to USD 4.01 billion by 2030, advancing at a 9.41% CAGR.

This expansion reflects steady patient demand driven by rising global obesity rates, accelerating adoption of AI-enabled energy-based devices, and a steady shift toward corporate wellness packages that reimburse aesthetic procedures. Non-invasive radiofrequency and ultrasound systems keep patient downtime to a minimum, while newly FDA-cleared minimally invasive platforms such as Aveli shorten recovery windows even further. Provider differentiation now hinges on data-guided personalization of treatment protocols, allowing clinics to combine multiple modalities in a single session and lift per-patient revenue. Rapid device innovation, broader practitioner training programs, and growing consumer willingness to finance appearance-oriented care positions the cellulite treatment market for multi-year expansion across developed and emerging economies alike.

Global Cellulite Treatment Market Trends and Insights

Rising Global Obesity & Overweight Prevalence

Higher body mass index intensifies dermal-adipose interactions that create visible dimpling, cementing obesity as a prime catalyst for the cellulite treatment market. A peer-reviewed evaluation of aesthetic clinics found 78% of cellulite patients present with elevated BMI, correlating directly with severity grades. Excess adiposity disrupts lymphatic flow and thins collagen septae, prompting practitioners to layer radiofrequency, ultrasound and injectable collagenase in one plan. Because such multimodal strategies command higher price points, average treatment revenue is rising alongside case volumes. The trend is particularly enduring in the United States and Western Europe, where processed-food consumption and sedentary lifestyles remain entrenched, providing a sustained clinical pipeline for providers.

Growing Preference for Non-Invasive Aesthetic Procedures

Social media advocacy and mainstream acceptance of lunchtime procedures have tilted demand sharply toward non-surgical care. Industry association data show non-invasive body contouring reached USD 17 billion in 2024, with cellulite therapies at the forefront . Younger demographics display markedly lower risk tolerance, favoring energy-based platforms that let them resume work the same day. Technical refinements in radiofrequency and high-intensity focused ultrasound now close much of the efficacy gap that once separated surgery and surface treatments. Clinics report that roughly 85% of consultations revolve exclusively around non-invasive options, a fundamental redesign of provider service mix that continues to widen the cellulite treatment market.

Low Awareness in Emerging Markets

Despite better spending power, fewer than 15% of prospective APAC or Latin American patients can name a cellulite therapy beyond topical creams, contrasting with 67% brand recall in North America. Lack of professional training programs and limited regional workshops slow practitioner adoption, capping territory expansion for device vendors. The resulting demand gap undercuts global revenue potential for the cellulite treatment market until sustained education campaigns gain traction.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advances in Energy-Based Devices

- Increasing Disposable Income & Aesthetic Consciousness

- AI-Driven Personalised Treatment Protocols

- High Procedure Cost & Limited Reimbursement

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Non-invasive platforms commanded 48.62% of 2024 revenue, a testament to consumer preference for low-downtime solutions. Radiofrequency leads within this bracket thanks to deeper heat penetration and intelligent temperature controls that minimize epidermal risk. High-intensity ultrasound is closing ground as real-time thermal imaging supports precise energy deposition. Together, these improvements keep the cellulite treatment market size for non-invasive solutions on an uptrend.

Minimally invasive options accelerate at a 10.35% CAGR to 2030, buoyed by FDA greenlights for Aveli and next-generation subcision tools that use micro-blade designs to sever fibrous septae with fewer passes . Injectable collagenase, spearheaded by QWO, inaugurates a drug-device hybrid niche, offering clinicians chemical lysis alongside mechanical release. As efficacy data pile up, clinics diversify procedure menus, reinforcing the modality convergence that now characterizes the cellulite treatment market.

The Cellulite Treatment Market Report is Segmented by Procedure (Minimally Invasive, Non-Invasive, and Topical), Cellulite Type (Soft Cellulite, Hard Cellulite, and Edematous Cellulite), End User (Hospitals, Specialized Dermatology Clinics, and More), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 42.19% revenue leadership in 2024 thanks to affluent patient cohorts, broad device availability and a regulatorily transparent pathway for innovative platforms. The region added nearly 1,600 medical spas in 2023, increasing procedure access points. Corporate wellness stipends that reimburse aesthetic services extend demand beyond vanity-driven consumption, expanding the cellulite treatment market across diverse employee bases.

Europe follows as a technology-mature arena, anchored by Germany, France and the United Kingdom. The European Medicines Agency's stringent clinical-data requirements elevate capital hurdles, yet once cleared, devices benefit from physician confidence and sizeable private-pay markets. Multi-modality packages that marry cellulite therapy with skin-tightening and fat-reduction are commonplace, supporting cross-selling and deepening wallet share per patient. Intellectual property protections and robust clinical trial networks continue to draw U.S. and Asian manufacturers into European partnerships, enriching the cellulite treatment industry ecosystem.

Asia-Pacific posts the highest 11.34% CAGR to 2030, riding middle-class expansion and social media-fueled aesthetic awareness. China's tier-1 cities see double-digit annual growth in high-end cosmetic clinics, while India's metro hubs invest in AI-guided RF systems to attract medical tourists. South Korea remains an innovation bellwether, exporting patent-backed handpieces and licensed algorithms worldwide. Meanwhile, price-competitive packages bundled with vacation itineraries funnel international patients into Thai and Malaysian hospitals, broadening the cellulite treatment market size in the region.

- Hologic

- Candela Medical

- Cutera

- Merz Pharma

- Allergan Aesthetics (AbbVie)

- Sisram Medical

- Venus Concept Inc.

- BTL

- Endo International plc (Qwo)

- Lumenis

- Sciton

- Fotona d.o.o.

- Lutronic

- Zimmer Aesthetics

- Cynosure LLC

- Inceler Medikal Co. Ltd.

- Beijing Nubway S&T Co. Ltd.

- Cymedics

- BeautyBio Inc.

- Tanceuticals

- Solta Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Obesity & Overweight Prevalence

- 4.2.2 Growing Preference For Non-Invasive Aesthetic Procedures

- 4.2.3 Technological Advances In Energy-Based Devices

- 4.2.4 Increasing Disposable Income & Aesthetic Consciousness

- 4.2.5 Ai-Driven Personalised Treatment Protocols

- 4.2.6 Corporate Wellness Aesthetic Stipends

- 4.3 Market Restraints

- 4.3.1 Low Awareness In Emerging Markets

- 4.3.2 High Procedure Cost & Limited Reimbursement

- 4.3.3 Regulatory Tightening On Device Safety

- 4.3.4 Counterfeit Home-Use Device Proliferation

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Procedure

- 5.1.1 Non-invasive

- 5.1.1.1 Radiofrequency-based

- 5.1.1.2 Laser-based

- 5.1.1.3 Ultrasound-based

- 5.1.1.4 Acoustic-wave

- 5.1.1.5 Cryolipolysis

- 5.1.2 Minimally Invasive

- 5.1.2.1 Subcision

- 5.1.2.2 Injectable collagenase

- 5.1.2.3 Laser-assisted lipolysis

- 5.1.3 Topical

- 5.1.3.1 Retinol creams

- 5.1.3.2 Caffeine creams

- 5.1.3.3 Peptide-based formulations

- 5.1.1 Non-invasive

- 5.2 By Cellulite Type

- 5.2.1 Soft Cellulite

- 5.2.2 Hard Cellulite

- 5.2.3 Edematous Cellulite

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Specialized Dermatology Clinics

- 5.3.3 Medical Spas & Beauty Centers

- 5.3.4 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Hologic Inc.

- 6.3.2 Candela Corporation

- 6.3.3 Cutera Inc.

- 6.3.4 Merz Pharma GmbH & Co KGaA

- 6.3.5 Allergan Aesthetics (AbbVie)

- 6.3.6 Sisram Medical (Alma Lasers)

- 6.3.7 Venus Concept Inc.

- 6.3.8 BTL Aesthetics

- 6.3.9 Endo International plc (Qwo)

- 6.3.10 Lumenis Ltd.

- 6.3.11 Sciton Inc.

- 6.3.12 Fotona d.o.o.

- 6.3.13 Lutronic Corporation

- 6.3.14 Zimmer Aesthetics

- 6.3.15 Cynosure LLC

- 6.3.16 Inceler Medikal Co. Ltd.

- 6.3.17 Beijing Nubway S&T Co. Ltd.

- 6.3.18 cymedics GmbH & Co KG

- 6.3.19 BeautyBio Inc.

- 6.3.20 Tanceuticals LLC

- 6.3.21 Solta Medical

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment