|

시장보고서

상품코드

1842678

외과용 드릴 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global Surgical Drills - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

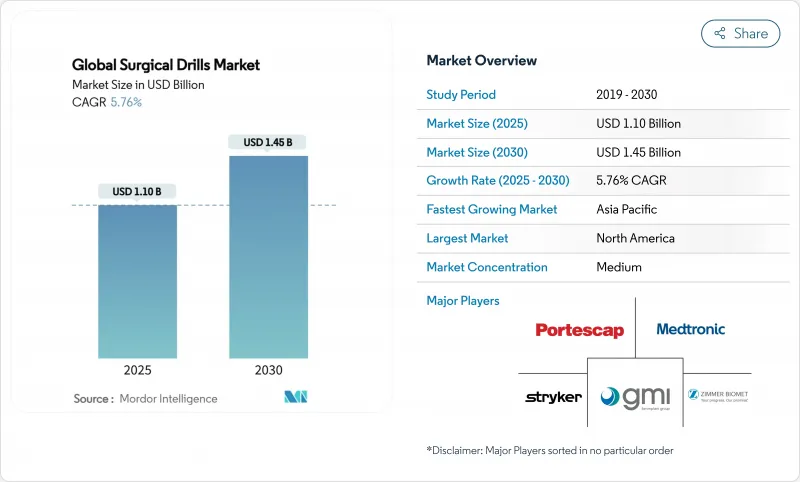

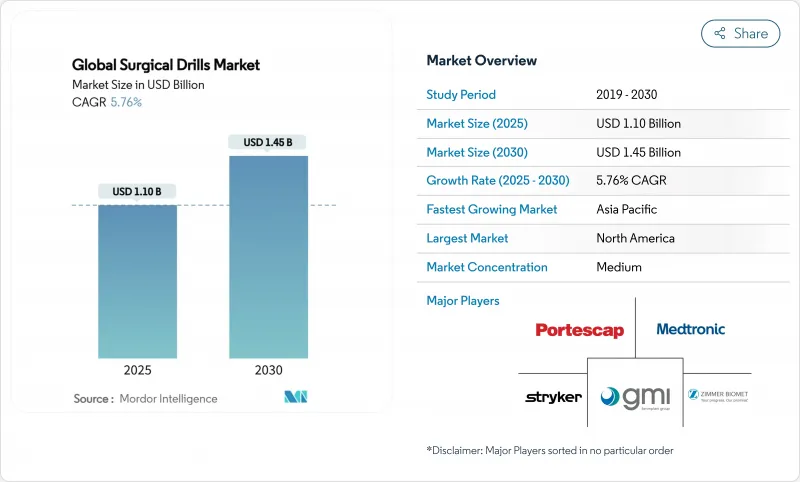

외과용 드릴 시장은 2025년에 11억 달러, 2030년에는 14억 5,000만 달러에 이를 전망으로, CAGR 5.76%로 성장할 전망입니다.

수요의 원동력이 되고 있는 것은 수술 건수 증가, 배터리의 화학적 성질의 급속한 개선, 드릴링 공차를 최소화할 필요가 있는 저침습 수술로의 이행입니다. 병원은 장비 예산을 공기압식에서 무선 시스템으로 이동합니다. 이는 스마트 배터리가 회전 시간을 단축하고 소프트웨어 가이드 드릴 프로파일이 골밀도에 관계없이 외과의에게 재현 가능한 정밀도를 제공하기 때문입니다. 희토류로 효율적인 모터, 더 가벼운 복합 하우징, 오토클레이브 가능한 리튬 팩은 유선기기와 동등한 성능을 제공하여 무선 우위의 시장을 형성하였습니다. 인구동태의 고령화와 로봇 및 네비게이션 플랫폼의 꾸준한 상승으로 드릴의 성능과 수술 워크플로우 전체의 효율성과의 관련성이 더욱 강화되어 단순한 판매 대수의 성장보다 엔지니어링의 질 향상에 박차를 가하고 있습니다.

세계의 외과용 드릴 시장의 동향과 인사이트

정형외과 및 외상 수술 건수 증가

미국에서만 무릎 관절 전치환술의 1차 수술 건수는 2030년까지 673% 증가하고 고관절 치환술은 174% 증가할 것으로 예측되어 정밀 드릴 시스템에 전례 없는 수요가 발생하고 있습니다. 도시화가 급속히 진행되는 아시아 경제권에서도 교통사고로 인한 외상이 골절 수복을 증가시키고 있습니다. 사례가 입원 환자 수술실에서 외래 환자 수술실로 이동함에 따라, 내장 압축기 라인을 우회하는 배터리 구동 플랫폼이 특히 두 자릿수의 성장을 기록하는 외래 정형외과 센터에서 인기를 얻게 됩니다. 노인의 뼈는 치료가 복잡하기 때문에 미세 균열을 피하는 토크 제어 드릴이 필요하며 프로그래밍 가능한 속도 프로파일에 대한 수요가 증가하고 있습니다. 이러한 요인들이 결합되어 외과용 드릴 시장은 견조한 상승 곡선을 그릴 전망입니다.

인체공학과 파워트레인의 급속한 혁신

차세대 무선 드릴은 무균 필드를 오염시킬 수 있는 호스 끌림 없이 공기압 토크에 필적하는 힘을 제공하며 작업에 따라 이를 넘어서기도 합니다. CONMED의 홀 리튬 배터리 시스템은 30분 내에 충전할 수 있어 오토클레이브 사이클의 반복에도 견디며, 한때 리튬 팩의 장애가 되었던 내구성의 갭을 해결합니다. 스트라이커의 시그니처 2는 외과 의사의 피로를 줄이는 슬림한 핸들로 75,000 RPM을 실현하며, 소프트웨어를 통해 팀은 특정 뼈 유형에 맞는 속도 토크 곡선을 미리 설정할 수 있습니다. 병원은 이와 같은 장점을 증례당 분 단위로 측정함으로써 자본 설비의 논의를 순수한 가격 비교가 아니라 워크플로우 결정으로 바꾸고 있습니다. AI 오버레이가 깊이와 각도를 안내하므로 드릴은 더 넓은 디지털 OR 생태계의 데이터 노드가 됩니다.

드릴과 관련된 수술 후 합병증

기존의 드릴로는 치밀한 피질골에서 100°C를 초과하여 골괴사 구역이 확대될 수 있습니다. 연구에 의하면, 연속적인 리밍으로도 열 외상을 완전히 제거할 수 없고, 병원에 있어서 법적 및 비용적인 우려가 심해지고 있습니다. 초음파 어시스트 드릴링은 힘과 열을 낮추지만 비용이 많이 들고 외과 의사의 재교육이 필요하기 때문에 보급이 늦어집니다. 내장형 냉각 장치와 보다 스마트한 토크 거버너가 주류가 될 때까지 신흥 시장의 위험을 꺼려하는 구매자는 업그레이드를 선호할 수 있어 외과용 드릴 시장의 일부를 억제할 전망입니다.

부문 분석

전동 드릴은 현재 매출의 55.78%를 차지하며 수십년에 걸친 OR에서의 익숙함과 안정적인 성능을 반영합니다. 그러나 무선 유닛은 배터리 교체가 30초 이내이고 오토클레이브 세이프 팩에 의해 고정 콘센트에서 해제되기 때문에 CAGR 6.36%로 상승하고 있습니다. 공기압식 드릴은 이미 센트럴 에어를 소유하고 있는 대량의 외상 센터에서 틈새를 유지하고 있지만, 컴프레서의 노후화와 함께 점유율이 저하되고 있습니다. 액세서리 키트(멸균 비트, 백업 배터리, 도킹 카트)는 안정적인 현금 흐름을 형성하기 때문에 공급업체는 채널 프로그램을 통합하고 병원에 플랫폼 생태계를 제공합니다. 무선 플랫폼의 외과용 드릴 시장 규모는 하이브리드 OR의 절차 기동성으로 인해 2020년대 후반에 유선기기의 수익을 초과할 것으로 예측됩니다.

커스텀 튜닝된 전원 관리 칩은 한 번의 충전으로 복잡한 정형외과 수술 8증례 이상의 가동 시간을 실현하여 이전의 다운타임 단점을 보완하고 있습니다. Arthrex가 2025년에 발표한 무선기기는 탄소섬유 쉘과 AI 기반 셀 헬스 분석을 결합하여 예기치 못한 정지를 최소화하는 예측 유지보수에 대한 동향을 보여줍니다. 기존 샤프트에 호환 슬리브를 개조하는 공급업체는 스위칭 마찰을 줄이고 예산에 제약이 있는 시스템 내에서 기기 전환을 가속화합니다.

60,000RPM을 초과하는 고속 드릴의 점유율은 61.42%이며 CAGR은 6.14%로 예상됩니다. 이는 저침습 경로에서 선명한 절삭을 선호하는 외과의의 선호도를 뒷받침하고 있습니다. 이 핸드피스에는 마찰열을 방출하고 뼈의 생존력을 유지하기 위한 마이크로벤트 채널과 세라믹 베어링이 내장되어 있습니다. 이비인후과와 척추 외과에서는 삐걱거리는 소리 없이 좁은 해부학적 구조를 통과하는 능력이 요구되기 때문에 고속 모델의 외과용 드릴 시장의 규모는 2030년까지 9억 달러에 달할 것으로 예측됩니다. 표준 속도의 드릴은 조밀한 유합조직으로 인해 통제된 진입을 필요로 하는 외상 유닛 및 재치환 관절 성형술에서 여전히 중요합니다.

최근의 설계 시프트에서는 센서가 얇은 피질층을 검출하면 자동으로 회전수를 낮추고, 하층의 조직을 보호하는 적응형 스피드 컨트롤러가 선호되고 있습니다. 스트라이커의 서보 루프는 50마이크로초 이내에 오버슈트에 상한을 설정하고, 펌웨어 업데이트는 보안 Wi-Fi를 통해 이루어지며 핸드피스는 중앙 장비 관리 대시보드에 연결됩니다.

외래 수술 드릴 시장은 제품별(공기압 드릴, 전동 드릴, 기타), 회전수별(고속 회전(60,000 Rpm 이상), 표준 회전(60,000) Rpm 이하)), 용도별(정형외과, 치과, 기타), 최종 사용자별(병원 및 클리닉, 외래수술센터(ASC), 기타), 지역별(북미, 유럽, 아시아태평양, 기타)로 분류됩니다.

지역별 분석

북미는 2024년 매출의 40.74%를 차지하였고 통합 디지털 OR의 조기 도입, 견실한 환급, 인구 1인당 가장 높은정형외과증례 수가 성장 요인입니다. 미국의 주요 센터는 무선 드릴을 로봇 워크스테이션에 통합하여 생태계 호환성을 둘러싼 공급업체와의 제휴를 강화하고 있습니다. 캐나다의 단일 지불 국가는 틈새 혁신성보다 플랫폼의 폭을 선호하는 그룹 입찰을 통해 구매하고 멕시코 사립 병원은 의료 관광의 흐름을 끌어들이기 위해 미국의 고급 장비를 수입하고 있습니다. 이 지역에서는 비록 성숙기이고 AI를 활용한 업그레이드에 대한 왕성한 의욕이 외과용 드릴 시장을 활성화하고 있지만 연간 성장률은 신흥 시장의 페이스보다 완만합니다.

유럽은 안정적이지만 지속 가능성에 민감한 시장입니다. 독일, 프랑스, 영국은 여전히 중심적인 구매자이지만, 환경 지침과 브렉시트 후 규제의 괴리가 컴플라이언스 층을 늘리고 있습니다. 이탈리아와 스페인의 병원은 입찰에서 저폐기물 포장과 재활용 계획을 규정합니다. 동유럽 국가들은 EU의 구조 기금에 힘입어 노후화된 공기압식 드릴에서 벗어나기 위해 무선 드릴로 교체하고 있습니다. CE 플러스와 UKCA의 듀얼 마킹이 표준화됨에 따라 벤더는 제품 출시 지연을 피하기 위해 신청을 간소화하고 대륙에서 경쟁력을 유지하고 있습니다.

아시아태평양의 CAGR은 7.48%로 세계에서 가장 빠른 성장을 이룰 전망입니다. 중국은 공적 자금을 외상 센터에 투입하여 사내 로봇 에코시스템에 투자하고 있습니다. 일본의 초고령화 사회는 인공관절 치환술의 대기자를 계속 늘리고, 병원은 골다공증의 뼈의 피질 연소를 최소화하는 토크 제어 드릴의 채용을 체감하고 있습니다. 인도 Tier-I의 민간 체인은 새로운 ASC에 배터리 스위트를 갖추고 있지만, 정부 시설은 여전히 저렴한 전기 세트를 선호하여 Tier-II 부문을 나눕니다. 호주와 한국은 기술의 최전선에 있으며 클라우드 기반 서비스 로그가 있는 75,000회 회전 핸드피스의 지역 벤치마크 역할을 합니다. 이들을 종합하면 외과용 드릴 시장은 다양화된 지역별 제품 로드맵을 추진하게 될 것으로 예상됩니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 도입

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 정형외과 및 외상 수술 건수 증가

- 드릴에 있어서의 인체공학과 파워트레인의 급속한 혁신

- 저침습 수술과 로봇 지원 수술의 급증

- 고령자의 근골격계 부담 증가

- 감염 억제를 위한 일회용 드릴로의 시프트

- 3D 프린팅에 의한 커스텀 드릴 가이드가 채용을 가속

- 시장 성장 억제요인

- 드릴과 관련된 수술 후 합병증

- 전원 시스템의 취득 및 라이프 사이클 비용 증가

- 멸균 폐기물과 지속가능성에 대한 압력

- 고토크 모터용 희토류 자석 공급의 병목

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품별

- 공기압 드릴

- 전기 드릴

- 배터리 드릴

- 액세서리

- 회전수별

- 고속(60,000 rpm 이상)

- 표준 속도(60,000 rpm 미만)

- 용도별

- 정형외과

- 치과 수술

- 이비인후과 수술

- 뇌신경외과

- 기타 용도

- 최종 사용자별

- 병원 및 클리닉

- 외래수술센터(ASC)

- 치과 및 이비인후과 전문센터

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Stryker Corporation

- Medtronic plc

- Zimmer Biomet Holdings Inc.

- Johnson & Johnson(DePuy Synthes)

- CONMED Corporation

- De Soutter Medical Ltd.

- Brasseler USA

- NSK Nakanishi Inc.

- Adeor Medical AG

- B. Braun SE

- Arthrex Inc.

- Joimax GmbH

- Shanghai Bojin Electric Instrument

- Portescap US Inc.

- GMI Ilerimplant

- Hubly Surgical

The surgical drills market stands at USD 1.10 billion in 2025 and is on course to reach USD 1.45 billion by 2030, growing at a 5.76% CAGR.

Demand is powered by climbing surgical volumes, rapid improvements in battery chemistry, and the migration of procedures toward minimally invasive techniques that call for ever-tighter drilling tolerances. Hospitals are shifting capital budgets from pneumatic lines to cordless systems because smart batteries cut turnover time, while software-guided drill profiles give surgeons repeatable accuracy regardless of bone density. Rare-earth-efficient motors, lighter composite housings, and autoclavable lithium packs have pushed performance parity with corded gear, setting the stage for cordless dominance. Aging demographics and the steady rise of robotic and navigation platforms further tighten the link between drill performance and overall surgical workflow efficiency, elevating engineering quality over simple unit sales growth.

Global Surgical Drills Market Trends and Insights

Rising Orthopedic & Trauma Surgery Volume

Primary total knee arthroplasties in the United States alone are forecast to jump 673% by 2030, while hip replacements rise 174%, creating an unprecedented load for precision drilling systems. Similar trajectories play out in fast-urbanizing Asian economies where traffic-related trauma lifts fracture repairs. As cases migrate from inpatient theaters to outpatient suites, battery-powered platforms that bypass built-in compressor lines win favor, especially in ambulatory orthopedic centers posting double-digit growth. High procedure complexity in elderly bone drives torque-controlled drills that avoid micro-cracks, raising demand for programmable speed profiles. These factors combine to keep the surgical drills market on a sturdy upward arc.

Rapid Ergonomics & Power-Train Innovation

New generations of cordless drills match, and in some tasks exceed, pneumatic torque while eliminating hose drag that can contaminate sterile fields. CONMED's Hall Lithium Battery system recharges in 30 minutes and withstands repeated autoclave cycles, solving the durability gap that once hampered lithium packs. Stryker's Signature 2 delivers 75,000 RPM from a slim handle that reduces surgeon fatigue, and its software lets teams preload speed-torque curves for specific bone types. Hospitals measure such gains in minutes saved per case, turning capital-equipment debates into workflow decisions rather than pure price comparisons. As AI overlays guide depth and angle, drills become data nodes in the wider digital OR ecosystem.

Post-Surgery Complications Linked to Drilling

Bone temperatures above 47 °C impair osteogenesis; conventional drills can exceed 100 °C in dense cortical bone, expanding osteonecrosis zones.Studies show even sequential reaming fails to eliminate heat trauma entirely, fueling legal and cost concerns for hospitals. Ultrasonic-assisted drilling lowers force and heat but costs more and requires surgeon retraining, slowing uptake. Until embedded cooling or smarter torque governors become mainstream, risk-averse buyers in emerging markets may postpone upgrades, restraining part of the surgical drills market.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Minimally Invasive & Robot-Assisted Procedures

- Growing Geriatric Musculoskeletal Burden

- High Acquisition & Lifecycle Cost of Power Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electric drills currently generate 55.78% of revenue, reflecting decades of OR familiarity and steady performance. Yet cordless units are climbing at 6.36% CAGR as battery swaps under 30 seconds and autoclave-safe packs free teams from fixed power outlets. Pneumatic drills retain a niche in high-volume trauma centers that already own central air, but their share erodes as compressors age out. Accessory kits-sterile bits, backup batteries, docking carts-form a steady annuity stream, so vendors align channel programs to lock hospitals into platform ecosystems. The surgical drills market size for cordless platforms is forecast to eclipse corded revenue by the late 2020s, driven by procedure mobility in hybrid ORs.

Custom-tuned power management chips now stretch runtime past eight complex orthopedic cases per charge, erasing prior downtime criticism. Arthrex's 2025 cordless launch paired a carbon-fiber shell with AI-based cell-health analytics, signaling a trend toward predictive maintenance that minimizes unplanned stoppages. Suppliers that retrofit compatibility sleeves for legacy shafts lower switching friction, accelerating fleet conversion within budget-sensitive systems.

High-speed drills topping 60,000 RPM hold 61.42% share and still grow at 6.14% CAGR, underscoring surgeon preference for crisp cutting in minimally invasive corridors. These handpieces integrate micro-vent channels and ceramic bearings to dissipate friction heat and preserve bone viability. The surgical drills market size for high-speed models is projected to reach USD 900 million by 2030 as ENT and spine teams demand burrs that navigate tight anatomy without chatter. Standard-speed drills remain important in trauma units and revision arthroplasty where dense callus calls for controlled advancement.

Recent design shifts favor adaptive-speed controllers that drop rpm automatically when sensors detect thin cortical layers, protecting underlying tissue. Stryker's servo loop caps overshoot within 50 microseconds, and firmware updates ship over secure Wi-Fi, linking handpieces to central device-management dashboards.

The Surgical Drills Market is Segmented by Product (Pneumatic Drills, Electric Drills, and More), by Speed (High-Speed (above 60, 000 Rpm), Standard Speed (below 60, 000 Rpm)), by Application (Orthopedic Surgeries, Dental Surgeries, and More), by End User (Hospitals and Clinics, Ambulatory Surgery Centers, and More), by Geography (North America, Europe, Asia-Pacific, and More).

Geography Analysis

North America holds 40.74% of 2024 revenue, powered by early adoption of integrated digital ORs, solid reimbursement, and the world's highest orthopedic caseload per capita. Leading U.S. centers embed cordless drills into robotic workstations, tightening vendor partnerships around ecosystem compatibility. Canada's single-payer provinces purchase through group tenders that favor platform breadth over niche innovation, while Mexico's private hospitals import premium U.S. gear to capture medical-tourism flows. Despite maturity, the region's keen appetite for AI-enabled upgrades keeps the surgical drills market vibrant, though annual growth moderates below emerging-market pace.

Europe offers a stable but sustainability-sensitive landscape. Germany, France, and the United Kingdom remain the anchor buyers, yet environmental directives and post-Brexit regulatory divergence add compliance layers. Hospitals in Italy and Spain increasingly stipulate low-waste packaging and end-of-life recycling plans in tenders. Eastern European states, buoyed by EU structural funds, retrofit theaters with cordless drills to leapfrog aging pneumatic lines. With CE-plus-UKCA dual marking now standard, vendors streamline filings to avoid product-launch lags, keeping continental share competitive.

Asia-Pacific is set to grow at 7.48% CAGR, the fastest worldwide. China funnels public funding into trauma centers and invests in in-house robotic ecosystems, often pairing domestic drill makers with locally built arms to reduce import spend. Japan's super-aged population continues to swell arthroplasty lists, compelling hospitals to adopt torque-controlled drills that minimize cortical burn in osteoporotic bone. India's tier-I private chains equip new ASCs with battery suites, while government facilities still favor budget electric sets, carving a two-tier segment. Australia and South Korea, at technology frontiers, serve as regional reference sites for 75,000 RPM handpieces with cloud-based service logs. Collectively, this mix pushes the surgical drills market toward diversified, region-specific product roadmaps.

- Stryker

- Medtronic

- Zimmer Biomet

- Johnson & Johnson

- Conmed

- De Soutter Medical Ltd.

- Brasseler USA

- NSK Nakanishi Inc.

- Adeor Medical

- B. Braun

- Arthrex

- Joimax

- Shanghai Bojin Electric Instrument

- Portescap US Inc.

- GMI Ilerimplant

- Hubly Surgical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising volume of orthopedic & trauma surgeries

- 4.2.2 Rapid ergonomics & power-train innovation in drills

- 4.2.3 Surge in minimally invasive & robot-assisted procedures

- 4.2.4 Growing geriatric musculoskeletal burden

- 4.2.5 Shift toward single-use drills to curb infection

- 4.2.6 3-D-printed custom drill guides accelerating adoption

- 4.3 Market Restraints

- 4.3.1 Post-surgery complications linked to drilling

- 4.3.2 High acquisition & lifecycle cost of power systems

- 4.3.3 Sterilization waste & sustainability pressures

- 4.3.4 Rare-earth magnet supply bottlenecks for high-torque motors

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Pneumatic Drills

- 5.1.2 Electric Drills

- 5.1.3 Battery-Powered Drills

- 5.1.4 Accessories

- 5.2 By Speed

- 5.2.1 High-Speed (above 60,000 rpm)

- 5.2.2 Standard Speed (below 60,000 rpm)

- 5.3 By Application

- 5.3.1 Orthopedic Surgeries

- 5.3.2 Dental Surgeries

- 5.3.3 ENT Surgeries

- 5.3.4 Neurosurgery

- 5.3.5 Other Applications

- 5.4 By End User

- 5.4.1 Hospitals and Clinics

- 5.4.2 Ambulatory Surgery Centers

- 5.4.3 Specialty Dental and ENT Centers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Stryker Corporation

- 6.3.2 Medtronic plc

- 6.3.3 Zimmer Biomet Holdings Inc.

- 6.3.4 Johnson & Johnson (DePuy Synthes)

- 6.3.5 CONMED Corporation

- 6.3.6 De Soutter Medical Ltd.

- 6.3.7 Brasseler USA

- 6.3.8 NSK Nakanishi Inc.

- 6.3.9 Adeor Medical AG

- 6.3.10 B. Braun SE

- 6.3.11 Arthrex Inc.

- 6.3.12 Joimax GmbH

- 6.3.13 Shanghai Bojin Electric Instrument

- 6.3.14 Portescap US Inc.

- 6.3.15 GMI Ilerimplant

- 6.3.16 Hubly Surgical