|

시장보고서

상품코드

1842679

원소 분석 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Elemental Analysis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

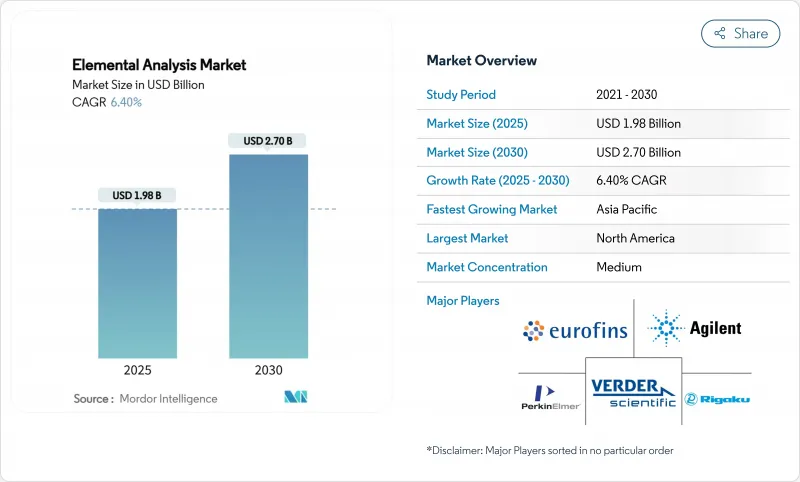

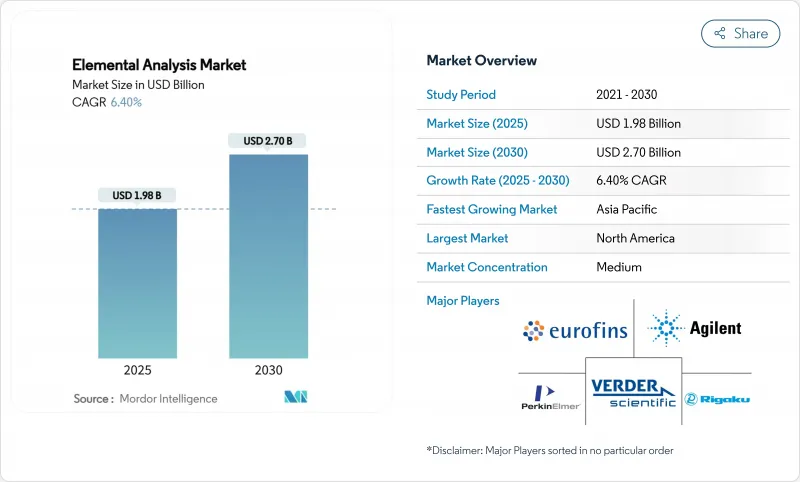

원소 분석 시장은 2025년 19억 8,000만 달러, CAGR 6.4%로 성장하여, 2030년에는 27억 달러로 확대될 것으로 예측됩니다.

이 성장은 정상적인 품질 관리에서 반도체 공장에서 요구되는 초미량 특성화로의 전환, 엄격한 의약품 불순물 규제 및 환경 규제의 확대를 반영합니다. AI 대응 자동화, 헬륨 절약 워크플로우, 하이브리드 멀티테크닉 플랫폼에 대한 투자가 벤더의 차별화를 강화합니다. 아시아 전역의 급속한 반도체 증설, PFAS 및 니트로소아민 규제 확대, 견고한 생명 과학 연구 개발 예산은 장기적인 수요를 강화합니다. 한편, 자본 집약, 숙련 노동자 부족, 불안정한 캐리어 가스 시장은 단기적인 기세를 약화시키고 있습니다.

세계 원소 분석 시장 동향과 통찰

생명과학 분야 연구개발 예산 증가

세계의 제약 및 바이오테크놀러지 연구개발비는 2024년에 2,000억 달러를 넘어, ICH Q3D 가이드라인에 근거한 원소 불순물 시험 수요가 높아지고 있습니다. Thermo Fisher의 여러 해에 걸쳐 400억-500억 달러의 M&A 파이프라인은 장비 수요 지속에 대한 벤더의 자신감을 뒷받침하고 있습니다. 의약품 분석시험 시장 자체는 2025년 97억 4,000만 달러에서 2030년에는 145억 8,000만 달러에 달하고, CAGR 8.41%로 확대되어 분석 화학 전체의 지출을 상회할 것으로 예측되고 있습니다. 이러한 투자는 ICP-MS, ICP-OES, 연소 분석기의 장기적인 주문을 확고하게 합니다. 턴어라운드 시간을 단축하고 샘플당 비용을 낮추는 자동화 모듈은 분광계에 번들링되는 경우가 많습니다. 공급업체는 USP 232/233 한도에 직접 보고를 맞추는 규정 준수 소프트웨어도 배포합니다.

세계 약전에서 엄격한 원소 불순물 한계

미국 FDA의 2024년 니트로소아민 갱신은 미량 금속 분류 시스템을 강화했기 때문에 즉각적인 컴플라이언스 압박이 되었습니다. USP는 의약품 분석 불순물 라이브러리를 약 3,000원의 약에 걸쳐 약 1,000개의 PAI로 확장하였으며, 실험실은 다원소 패널을 확대해야 했습니다. 2025년 3월, FDA는 Chemical Contaminants Transparency Tool을 시작하여 식품 내 금속 모니터링에 대한 FDA의 지속적인 주력을 제시했습니다. 바로 사용할 수 있는 검량선 표준과 클라우드 기반 기준 라이브러리의 급속한 도입이 이에 이어졌습니다. 장비 제조업체는 의약품 제조업체의 검증 오버헤드를 줄이기 위해 21 CFR Part 11에 따른 시스템 인증을 점점 늘리고 있습니다. 이러한 동향으로 원소분석시장은 진화하는 약국방지령과 제대로 연결되어 있습니다.

높은 자본 비용과 유지 보수 비용

싱글 사중극 ICP-MS 유닛은 통상 10만-20만 달러, 트리플 사중극 또는 고분해능 모델은 40만 달러를 넘을 수 있어 중규모 실험실에서는 초기 투자가 큰 부담이 됩니다. 가스, 전력 및 소모품으로 인해 ICP-MS의 연간 런닝 비용은 약 13,250달러가 되며, ICP-OES 설정의 2배 이상이 됩니다. 공급업체는 일반적으로 검색기 교체, 예방 유지보수 및 소프트웨어 업데이트를 다루기 위해 매년 구매 금액의 10% 풀 서비스 계약을 권장합니다. 자금 조달로 자본 지출을 분산시키는 경우에도 배기 처리나 클린 전력을 위한 설비 업그레이드 등의 숨겨진 비용이 프로젝트 예산에 추가로 15-20% 상승할 가능성이 있어 신흥 시장에서의 채택이 늦어집니다. 헬륨 가격이 상승하고 공급이 가까워짐에 따라 실험실은 직접적인 영업 지출의 추가 증가에 직면하여 많은 실험실이 장비의 업데이트 사이클을 연기하거나 임대 모델로 전환해야 합니다.

부문별 분석

2024년 원소 분석 시장 점유율은 무기 분석이 56.1%를 차지했으며 USP 232/233 준거와 반도체 오염 관리가 뒷받침됐습니다. ICP-MS와 ICP-OES 플랫폼이 이 부문을 지배하고 의약품 및 고순도 화학물질 중의 As, Pb, Cd를 서브 NG/L로 검출합니다. 반도체 주조는 9N 등급 공정 화학물질의 일상적인 인증을 요구하며 장비 배치를 더욱 고정하고 있습니다. 벤더는 무기 금속 검출과 할로겐 및 유황 매핑 옵션을 번들로 묶은 하이브리드 시스템에 중점을 옮기고 있으며, QA 실험실 전반에 걸쳐 플랫폼의 유용성을 넓히고 있습니다. 자본 투자는 1ppt 미만의 기준선 드리프트를 보장하는 연장 서비스 계약에 의해 유지되며 공장은 장기적인 분석 재현성을 보장합니다.

유기 원소 분석은 규모는 작지만 CAGR 7.9%로 성장하고 있으며 원소 분석 시장 전체보다 빠릅니다. 연소 기반의 CHNSO 분석기는 분자식 확인이라는 의약품 개발의 요구에 대응하고 현재는 5분의 사이클 타임을 제공하는 90 포지션의 오토샘플러를 장비하고 있습니다. 식품 안전 실험실은 단백질, 지방 및 수분의 정량에 동일한 플랫폼을 채택하여 고객 기반을 제약 및 석유 화학 이외에도 확대하고 있습니다. 벤더는 듀얼 오븐 구성을 도입하고 고온 폴리머와 저온 농산물 샘플을 동시에 측정하여 유휴 시간을 단축합니다. 조인 소프트웨어는 LIMS 메타데이터를 원활하게 가져오고 실행 후 검증을 줄입니다.

지역 분석

북미는 FDA의 불순물 가이드라인, EPA의 PFAS 의무화, 세계를 선도하는 제약회사의 생산고를 배경으로 2024년 매출의 35.7%를 차지했습니다. 미국 제약 회사는 세계 임상 파이프라인의 40% 이상을 차지하고 안정되어 있는 장비 주문을 유지하는 반면, 캐나다 광업 분야는 급료 관리를 위한 XRF 순서를 승진시킵니다. 멕시코에서는 시마즈 제작소의 새로운 자회사에 힘입어 수탁 제조의 움직임이 활발해지고 있으며, 지역 유저의 밑단이 퍼지고 있습니다.

아시아태평양의 CAGR은 7.5%를 나타내고 세계 최고 속도로 예측되며 정부가 선진적인 칩팹과 국내 의약품 생산 능력을 조성하고 있기 때문입니다. 일본의 2nm 파일럿 라인과 인도의 1,002억 달러의 반도체 로드맵은 초미량 순도 사양으로 대응 가능한 원소 분석 시장을 확대합니다. 중국은 재료의 자급 자족을 추진하고 있으며 ICP-MS 수요를 견인하고 있습니다. 한편 한국의 배터리 기가 공장은 인라인 캐소드 검사용 LIBS 시스템을 구입하고 있습니다. 호주에서는 광업 수출이 벌크 광석 선별용 XRF 판매를 지원합니다.

유럽은 엄격한 PFAS 규정과 독일과 프랑스의 강력한 백신 제조 클러스터를 배경으로 꾸준히 성장하고 있습니다. EU의 배터리 재활용 지령은 2030년까지 생산능력을 50배로 하는 것을 목표로 하고 있으며, 초미량 금속분석장치의 수주를 증가시킵니다. 영국은 헬륨의 휘발성을 완화하기 위해 질소 가압 ICP-MS를 중시하고, 북유럽 국가들은 그린 스틸 파일럿 플랜트에서 슬래그를 신속하게 모니터링하기 위해 LIBS를 도입합니다. 또한 중동의 구리 프로젝트와 남미의 리튬 염수 사업에서는 새로운 판로가 개척되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트·지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 생명과학 분야에서 R&D 자금 증가

- 세계의 약국방에 있어서의 원소 불순물 규제의 엄격화

- 식품 및 환경 안전 규정 확대

- 첨단 칩에 대한 반도체 등급의 순도 요건

- AI 지원 자동 다중 요소 매핑으로 처리량 향상

- 초미량 금속 탐지를 주도하는 배터리 재활용 붐

- 시장 성장 억제요인

- 하이 엔드 분광계의 높은 자본 비용과 유지 보수 비용

- 크로스 트레이닝된 분석 화학자의 부족

- 복잡한 샘플 전처리 워크플로우로 인한 턴어라운드 시간 지연

- ICP-MS의 운용 예산을 부풀리는 세계의 헬륨 부족

- 공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 유형별

- 유기 원소 분석

- 무기 원소 분석

- 기술별

- 파괴 기술

- ICP-원자 발광 분광법(ICP-AES)

- ICP-질량 분석(ICP-MS)

- 연소 분석(CHNS/O)

- 기타

- 비파괴 기술

- 형광 X선 분광법(XRF)

- 푸리에 변환 적외선 분광법(FTIR)

- 레이저 유도 브레이크다운 분광법(LIBS)

- 기타

- 파괴 기술

- 최종 사용자별

- 제약 및 바이오테크놀러지 기업

- 연구 및 학술기관

- 환경 및 식품 시험소

- 산업 및 제조업

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Thermo Fisher Scientific

- Agilent Technologies

- PerkinElmer

- Shimadzu Corporation

- Bruker Corporation

- Rigaku Corporation

- HORIBA Ltd

- Analytik Jena(Endress Hauser)

- SPECTRO Analytical(AMETEK)

- Hitachi High-Tech Analytical Science

- Malvern Panalytical

- Elementar

- LECO Corporation

- Oxford Instruments

- Eurofins Scientific

- Element Materials Technology

- Verder Scientific(ELTRA)

- Anton Paar GmbH

- JEOL Ltd

- SciAps Inc.

- Micromeritics Instrument

- LECO Corporation

- Metrohm AG

제7장 시장 기회와 전망

SHW 25.11.03The elemental analysis market was valued at USD 1.98 billion in 2025 and is forecast to expand to USD 2.7 billion by 2030, registering a 6.4% CAGR.

Growth reflects a shift from routine quality control toward ultra-trace characterization demanded by semiconductor fabs, stringent pharmaceutical impurity limits, and widening environmental regulations. Investments in AI-enabled automation, helium-saving workflows, and hybrid multi-technique platforms strengthen vendor differentiation. Rapid semiconductor buildouts across Asia, expanding PFAS and nitrosamine limits, and robust life-science R&D budgets reinforce long-term demand. Meanwhile, capital intensity, skilled-labor shortages, and volatile carrier-gas markets temper near-term momentum.

Global Elemental Analysis Market Trends and Insights

Growing R&D Funding in Life Sciences

Global pharma-biotech R&D spending crossed USD 200 billion in 2024, intensifying demand for elemental impurity testing under ICH Q3D guidelines. Thermo Fisher's multi-year USD 40-50 billion M&A pipeline underscores vendor confidence in sustained instrumentation demand. The pharmaceutical analytical-testing market itself is projected to rise from USD 9.74 billion in 2025 to USD 14.58 billion by 2030 at 8.41% CAGR, outpacing broader analytical chemistry spending. These investments solidify long-term orders for ICP-MS, ICP-OES, and combustion analyzers. Automation modules that shrink turnaround times and lower per-sample cost are increasingly bundled with spectrometers. Vendors also roll out compliance-ready software that aligns reporting directly with USP 232/233 limits.

Stringent Elemental-Impurity Limits in Global Pharmacopeias

The US FDA's 2024 nitrosamine update created immediate compliance pressure as it tightened classification systems for trace metals. USP expanded its pharmaceutical analytical impurity library to nearly 1,000 PAIs spanning 300 APIs, compelling laboratories to broaden multi-element panels. In March 2025, the FDA launched the Chemical Contaminants Transparency Tool, signaling a persistent agency focus on metals monitoring in foods. Rapid adoption of ready-to-use calibration standards and cloud-based reference libraries has followed. Instrument makers increasingly certify systems per 21 CFR Part 11 to reduce validation overhead for drug manufacturers. These trends keep the elemental analysis market firmly linked to evolving pharmacopeial directives.

High capital & maintenance costs

Single-quadrupole ICP-MS units typically list between USD 100,000 and USD 200,000, while triple-quadrupole or high-resolution models can exceed USD 400,000, placing a heavy upfront burden on mid-size laboratories. Annual operating expenses compound the challenge: gas, power, and consumables push yearly running costs for an ICP-MS to about USD 13,250, more than double the bill for an ICP-OES setup. Vendors generally recommend full-service contracts priced at 10% of the purchase value each year to cover detector replacement, preventive maintenance, and software updates. Even where financing spreads capital outlays, hidden costs such as facility upgrades for exhaust handling and clean power can add another 15-20% to project budgets, slowing adoption in emerging markets. As helium prices rise and supply tightens, labs face further escalation in direct operating expenditures, prompting many to postpone instrument refresh cycles or pivot to rental models.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Food & Environmental Safety Regulations

- Semiconductor-Grade Purity Requirements for Advanced Chips

- Global Helium Shortages Inflating ICP-MS Operating Budgets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Inorganic analysis captured 56.1% of the elemental analysis market share in 2024, buoyed by USP 232/233 compliance and semiconductor contamination control. ICP-MS and ICP-OES platforms dominate this segment, delivering sub-ng/L detection of As, Pb, and Cd in drug products and high-purity chemicals. Semiconductor foundries demand routine certification of 9N-grade process chemicals, further anchoring instrument placements. Vendor emphasis is shifting toward hybrid systems that bundle inorganic metals detection with options for halogen and sulfur mapping, extending platform utility across QA labs. Capital expenditure is sustained by extended service contracts that guarantee <1 ppt baseline drift, assuring fabs of long-term analytical reproducibility.

Organic elemental analysis, while smaller, is growing at 7.9% CAGR-faster than the overall elemental analysis market. Combustion-based CHNSO analyzers address drug-development needs for molecular formula confirmation and are now equipped with 90-position autosamplers offering 5-minute cycle times. Food-safety labs adopt the same platforms to quantify protein, fat, and moisture, expanding the customer base beyond pharma and petrochemicals. Vendors introduce dual oven configurations that measure high-temperature polymers alongside low-temperature agro-samples, reducing idle time. Coupled software allows seamless import of LIMS metadata, trimming post-run validation.

The Elemental Analysis Market is Segmented by Type (Organic Elemental Analysis and Inorganic Elemental Analysis), Technology (Destructive {ICP-AES, ICP-MS, and More} and Nondestructive {XRF, FTIR, and More), End User (Pharmaceutical & Biotechnology Companies, Research & Academic, and More), and Geography (North America, Europe, Asia Pacific, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 35.7% of revenue in 2024 on the strength of FDA impurity guidelines, EPA PFAS mandates, and world-leading pharma output.]US drugmakers account for over 40% of global clinical pipelines, sustaining steady instrument orders, while Canada's mining sector fuels XRF placements for grade control. Mexico's rising contract-manufacturing activity, supported by Shimadzu's new subsidiary, widens the regional user base.

Asia-Pacific is projected to deliver a 7.5% CAGR, the fastest worldwide, as governments subsidize advanced chip fabs and domestic drug production capabilities. Japan's 2-nm pilot lines and India's USD 100.2 billion semiconductor roadmap enlarge the addressable elemental analysis market through ultratrace purity specifications. China's push for materials self-sufficiency drives demand for ICP-MS, while South Korea's battery gigafactories purchase LIBS systems for inline cathode inspection. Australia's mining exports sustain XRF sales for bulk-ore screening.

Europe grows steadily on the back of stringent PFAS restrictions and strong vaccine manufacturing clusters in Germany and France. The EU's battery-recycling directive, targeting a 50-fold capacity increase by 2030, lifts orders for ultratrace metals analyzers. The United Kingdom emphasizes nitrogen-pressurized ICP-MS to mitigate helium volatility, and Nordic nations deploy LIBS for rapid slag monitoring in green-steel pilot plants. Eastern European mining expansions in Poland and Serbia add new sales channels, while Middle East copper projects and South American lithium brine operations open supplementary opportunities.

- Thermo Fisher Scientific

- Agilent Technologies

- PerkinElmer

- Shimadzu

- Bruker

- Rigaku

- HORIBA

- Analytik Jena (Endress+Hauser)

- SPECTRO Analytical (AMETEK)

- Hitachi High-Tech Analytical Science

- Malvern Panalytical

- Elementar

- LECO

- Oxford Instruments

- Eurofins

- Element Materials Technology

- Verder Scientific (ELTRA)

- Anton Paar

- JEOL

- SciAps Inc.

- Micromeritics Instrument

- LECO

- Metrohm

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing R&D Funding In Life Sciences

- 4.2.2 Stringent Elemental-Impurity Limits In Global Pharmacopeias

- 4.2.3 Expanding Food & Environmental Safety Regulations

- 4.2.4 Semiconductor-Grade Purity Requirements For Advanced Chips

- 4.2.5 AI-Enabled Automated Multi-Element Mapping Boosts Throughput

- 4.2.6 Battery-Recycling Boom Driving Ultratrace Metals Detection

- 4.3 Market Restraints

- 4.3.1 High Capital & Maintenance Costs Of High-End Spectrometers

- 4.3.2 Shortage Of Cross-Trained Analytical Chemists

- 4.3.3 Complex Sample-Prep Workflows Delay Turnaround Time

- 4.3.4 Global Helium Shortages Inflating ICP-MS Operating Budgets

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Organic Elemental Analysis

- 5.1.2 Inorganic Elemental Analysis

- 5.2 By Technology

- 5.2.1 Destructive Technologies

- 5.2.1.1 ICP-Atomic Emission Spectroscopy (ICP-AES)

- 5.2.1.2 ICP-Mass Spectrometry (ICP-MS)

- 5.2.1.3 Combustion Analysis (CHNS/O)

- 5.2.1.4 Others

- 5.2.2 Nondestructive Technologies

- 5.2.2.1 X-Ray Fluorescence Spectroscopy (XRF)

- 5.2.2.2 Fourier Transform Infrared Spectroscopy (FTIR)

- 5.2.2.3 Laser-Induced Breakdown Spectroscopy (LIBS)

- 5.2.2.4 Others

- 5.2.1 Destructive Technologies

- 5.3 By End User

- 5.3.1 Pharmaceutical & Biotechnology Companies

- 5.3.2 Research & Academic Institutions

- 5.3.3 Environmental & Food Testing Laboratories

- 5.3.4 Industrial & Manufacturing

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Thermo Fisher Scientific

- 6.3.2 Agilent Technologies

- 6.3.3 PerkinElmer

- 6.3.4 Shimadzu Corporation

- 6.3.5 Bruker Corporation

- 6.3.6 Rigaku Corporation

- 6.3.7 HORIBA Ltd

- 6.3.8 Analytik Jena (Endress+Hauser)

- 6.3.9 SPECTRO Analytical (AMETEK)

- 6.3.10 Hitachi High-Tech Analytical Science

- 6.3.11 Malvern Panalytical

- 6.3.12 Elementar

- 6.3.13 LECO Corporation

- 6.3.14 Oxford Instruments

- 6.3.15 Eurofins Scientific

- 6.3.16 Element Materials Technology

- 6.3.17 Verder Scientific (ELTRA)

- 6.3.18 Anton Paar GmbH

- 6.3.19 JEOL Ltd

- 6.3.20 SciAps Inc.

- 6.3.21 Micromeritics Instrument

- 6.3.22 LECO Corporation

- 6.3.23 Metrohm AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment