|

시장보고서

상품코드

1842683

유방 재건 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Breast Reconstruction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

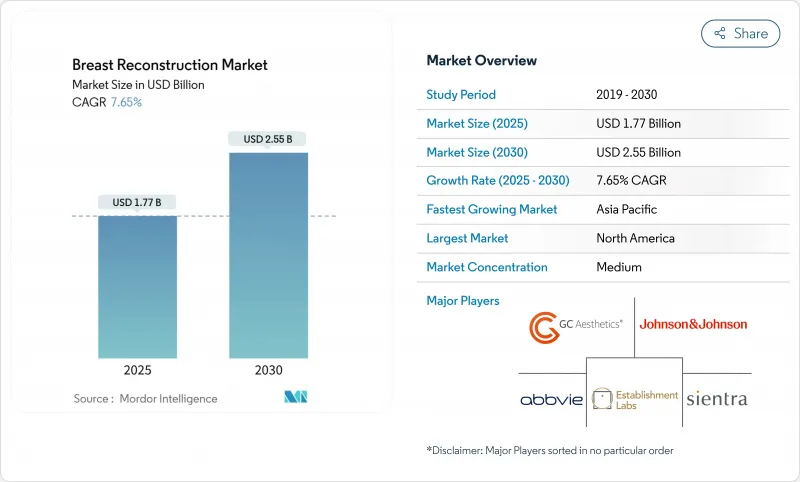

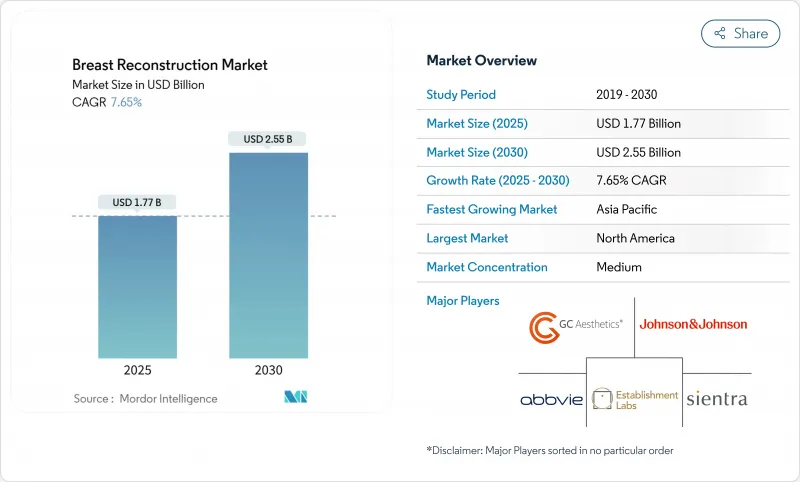

유방 재건 시장은 2025년에 17억 7,000만 달러, 2030년에는 25억 5,000만 달러에 이르고, CAGR 7.65%로 성장할 전망입니다.

이 성장은 유방암 이환율 상승, 상환 의무 확대, 인공지능(AI) 이미징과 3D 바이오프린트 비계 등의 기술 혁신에 직결됩니다. 주요 암 영역에서 5년 생존율은 91%로, 대상이 되는 환자층이 확대되는 한편, 새로운 조직공학 플랫폼은 재수술을 줄이고 장기적인 결과를 개선합니다. 시장의 주도권은 현재 임플란트가 잡고 있지만, 재생제품과 생물학적 메쉬의 급속한 성장으로 외과의의 선호는 형태의 안정성과 자연조직과의 통합을 융합시킨 하이브리드 수술로 이행하고 있습니다. 지역적으로는 북미가 2024년 유방 재건시장 점유율의 37.72%를 차지했고, 아시아태평양은 CAGR 9.22%로 성장하고 있으며, 2050년까지 세계 유방암 환자가 38% 증가한다는 세계보건기관의 예측에 뒷받침되고 있습니다.

세계 유방 재건시장 동향과 통찰

유방암 이환율 상승

세계보건기구(WHO)는 2050년까지 연간 320만 명이 새롭게 유방암으로 진단되어 현재 수준에서 38% 증가할 것으로 예측했습니다. 2022년 신규 증례 수는 아시아가 98만 5,400명으로, 2050년에는 140만명을 넘을 것으로 예상되고 있습니다. 50세 미만의 젊은 여성과 아시아계 미국인/태평양 제도민의 집단은 이환율이 가장 급상승하고 생존기간의 연장과 재건률의 상승으로 이어지고 있습니다. 중국과 인도에서는 가치 주도형 병원 시스템이 임플란트를 이용한 수술과 하이브리드 수술을 위한 새로운 수술실 테두리를 열고 있으며, 비용 효율적인 솔루션을 대규모로 제공할 수 있는 장비 제조업체들에게 화이트 스페이스의 성장 포켓을 만들어 내고 있습니다. 따라서 인구동태의 확대는 단순한 수치적인 것이 아니라 평생 재치환의 위험을 최소화하는 내구성이 있어 합병증이 적은 임플란트로 제품 믹스 수요를 시프트시키고 있습니다.

상환의 의무화와 의식의 향상

여성의 건강과 암의 권리에 관한 법률(Women's Health and Cancer Rights Act)은 종합적인 재건술 혜택을 미국의 단체의료보험제도에 보증하는 것이며, 2025년 2월에는 DIEP플랩과 GAP플랩의 청구코드가 보호되며 고급 자가기술에 대한 규제당국의 헌신 2024년 7월 캘리포니아 주 의료 보험(Medi-Cal) 정책 업데이트와 같은 주 수준의 조치는 저소득 환자에 대한 임플란트 수술에 대한 접근을 확대합니다. 주요 민간지급기관은 재건을 의료상 필요한 것으로 재정의하여 좌우대칭 수술 및 합병증 관리에 적용하고 있습니다. 외래 센터가 가치 기반 지불 모델을 채택함에 따라 외과의사는 수술 시간과 다운스트림 재수술을 줄이는 기술을 채택하는 경제적 인센티브를 얻게 되었으며, 코히시브 젤 임플란트와 결합한 AI 가이드가 있는 사이징 소프트웨어에 대한 수요가 가속화되고 있습니다.

신흥 시장에서 높은 수술 비용과 장치 비용

동남아시아에서의 임플란트 재건의 평균 자기부담액은 연봉 중앙값의 45%를 넘어 주요 도시 이외의 보급은 한정적입니다. 현지 지급자가 첨단 생체재료에 상환을 하는 경우는 거의 없기 때문에 외과의사는 재치환의 위험이 높은 생리식염수 임플란트에 의지할 수밖에 없습니다. 다국적 의료기기 기업은 이러한 비용에 민감한 지역에 침투하기 위해서는 현지에서 제조하거나 단계적인 가격 체계를 제공해야 합니다. 인도와 태국에서는 저소득 환자에게 재건 비용을 보조하는 정부의 시험 프로그램이 시행되었고 초기 단계에서 좋은 결과를 얻었지만 그 범위는 여전히 제한적입니다.

부문 분석

유방 재건 시장에서 유방 임플란트의 점유율은 2024년 43.55%를 유지했습니다. 그러나 3D 바이오프린트 스캐폴드와 재생 임플란트는 15.25%의 연평균 복합 성장률(CAGR)로 성장하고 있으며, 이물질 반응을 최소화하고 개인에 맞는 형상을 가능하게 하는 조직공학 플랫폼에 대한 축발을 보여줍니다. 기존의 조직 확장기는 여전히 단계적 재건의 교량을 하고 있지만, 대흉근 전치법이나 단단계법이 인기를 끌면서 그 역할은 좁아지고 있습니다.

유방 재건업계에서는 재수술률을 저감시키는 기구에 대한 평가가 높아지고 있습니다. AI 가이드 사이징 소프트웨어는 코히시브 젤 임플란트와 쌍을 이루고 사용자 정프로파일을 제공하며, 폴리-4-하이드록시부티레이트 스캐폴드는 자연 조직의 성장을 지원합니다. BD의 GalaFLEX LITE에 대한 STANCE 시험은 재수술에서 54% 코팅 구축 재발을 다루는 생체 흡수성 메쉬를 강조합니다. 이러한 기술 혁신은 장기적인 비용 절감과 환자 보고에 의한 결과를 목표로 병원 조달 기준을 재구성하고 있습니다.

실리콘은 2024년 유방 재건 시장 점유율의 45.53%를 차지했지만, 이는 수십년에 걸친 개선과 최근의 대용량 옵션 FDA 허가에 의해 지원되고 있습니다. 그러나 외과의사는 혈관 조직 통합을 촉진하고 만성 염증을 완화시키는 재료를 찾고 있기 때문에 생물학적 메쉬가 CAGR 9.15%에서 성장을 이끌고 있습니다. 생리 식염수 임플란트는 안전에 우려가 있는 환자에게는 적합하지만 점차적으로 그 위치를 잃고 있습니다.

이와 병행하여, 합성 메쉬는 지속성과 감염 위험에 대한 감시의 눈을 강화하고 생분해성 대체품에 대한 수요에 박차를 가하고 있습니다. 임플란트 공급망의 환경 실적에 대한 조사에서도 탄소 부하가 낮은 생물학적 재료와 생분해성 재료가 선호되고 있으며, 조달 정책과 병원의 ESG 목표가 일치하고 있습니다.

지역 분석

북미는 2024년에 37.72%의 점유율로 유방 재건시장을 선도해 연방정부의 보험적용 의무와 인증형성외과의의 치밀한 네트워크에 지지를 받고 있습니다. 이 지역에서는 많은 중요한 임상시험도 실시되어 차세대 임플란트와 생물학적 메쉬에 조기 액세스가 가능해지고 있습니다. 인공지능 가이드 플래닝 툴이 대병원 시스템과 외래수술센터(ASC)에 침투함에 따라 시장 확대가 견고해질 것으로 예측됩니다.

아시아태평양은 가장 급성장하고 있는 지역으로, 2030년까지의 CAGR은 9.22%로 예측되고 있습니다. 유방암 이환율 상승, 중간소득층 소득 확대, 재건의 문화적 정상화가 수술 건수 증가에 박차를 가하는 한편, 일본의 즉각 재건률 11.2%는 잠재적인 상승을 나타냅니다. 중국과 인도에서는 유방절제술에 보조금을 내는 정부의 이니셔티브가 서서히 재건술로 확대되고, 비용에 최적화된 임플란트와 현지 제조 메쉬의 길이 열리고 있습니다.

유럽은 수술의 이행률은 국가마다 다르며, 기본적인 접근을 보장하는 국민 모두 보험의 틀 아래에서 완만한 성장을 유지하고 있습니다. 라틴아메리카와 중동 및 아프리카는 외과 수술 인프라 정비와 임상 의학 양성의 파트너십에 따라 성장하는 아직 개발 도상 시장입니다. 생산을 현지화하고 제품 포트폴리오를 각 지역의 상환 수준에 맞추는 다국적 기업은 선행자 이익을 얻을 수 있다고 생각됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트·지원

목차

제1장 도입

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 유방암 이환율의 상승

- 보험 상환의 의무화와 의식의 고조

- 결합형 젤 및 거미베어 보형물의 발전

- 유두절개술과 대흉근 전 유방절제술의 급증

- 3D 바이오프린트 재생 임플란트의 임상시험 개시

- 인공지능 가이드 이미징 및 크기 조정으로 수정 수술 감소

- 시장 성장 억제요인

- 신흥 시장에서 높은 수술 비용과 장치 비용

- 임플란트의 안전성에 관한 우려(BIA-ALCL, 피막 구축)

- 자가 플랩을 위한 미세수술 전문인력의 부족

- ESG에 의한 실리콘 및 ADM 공급 체인의 혼란

- 기술적 전망

- Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품별

- 유방 임플란트

- 조직 확장제

- 세포성 진피 매트릭스(생물학적, 합성)

- 3D 바이오프린트 스캐폴드와 재생 임플란트

- 기타 보조제품(NAC 보철물, 고정장치)

- 재료 유형별

- 실리콘

- 생리 식염수

- 자기조직

- 생물학적 메쉬

- 합성 메쉬

- 재건술식별

- 임플란트

- 자가 조직

- 하이브리드

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 미용 전문 클리닉

- 용도별

- 유방 절제 후 암 재건

- 예방적 유방절제술

- 외상과 선천성 기형

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- AbbVie(ALLERGAN)

- Johnson & Johnson(Mentor Worldwide)

- Sientra Inc.

- Establishment Labs SA

- GC Aesthetics plc

- Polytech Health & Aesthetics GmbH

- RTI Surgical Inc.

- Groupe Sebbin SAS

- Integra LifeSciences

- Silimed

- Laboratories Arion

- Ideal Implant Inc.

- BellaSeno GmbH

- CollPlant Biotechnologies

- Stratasys Ltd.

- HansBiomed Co. Ltd.

- Motiva USA LLC

- Tissue Regenix Group plc

- Decomedical Srl

- Implantech Associates

제7장 시장 기회와 전망

SHW 25.11.03The breast reconstruction market is valued at USD 1.77 billion in 2025 and is on track to reach USD 2.55 billion by 2030, advancing at a 7.65% CAGR.

This growth links directly to rising breast-cancer incidence, expanding reimbursement mandates, and innovations such as artificial-intelligence (AI) imaging and 3-D bioprinted scaffolds. A 91% five-year survival rate in major oncology regions enlarges the eligible patient pool, while emerging tissue-engineering platforms reduce revision surgeries and improve long-term outcomes. Market leadership currently rests with implants, yet rapid gains in regenerative products and biologic meshes are shifting surgeon preference toward hybrid procedures that blend form stability with natural tissue integration. Geographically, North America holds a 37.72% breast reconstruction market share in 2024, and Asia-Pacific is advancing at 9.22% CAGR, supported by the World Health Organization's forecast of a 38% global breast-cancer case rise by 2050.

Global Breast Reconstruction Market Trends and Insights

Rising Incidence Of Breast Cancer

The World Health Organization projects 3.2 million new breast-cancer diagnoses per year by 2050, up 38% from current levels. Asia accounted for 985,400 new cases in 2022, a number expected to cross 1.4 million by 2050. Younger women under 50 and Asian American/Pacific Islander populations have shown the steepest incidence upticks, leading to longer survivorship and higher reconstruction uptake. In China and India, value-driven hospital systems are opening new operating-room slots for implant-based and hybrid procedures, creating white-space growth pockets for device makers able to offer cost-effective solutions at scale. The demographic expansion is therefore not merely numerical; it also shifts product-mix demand toward durable, low-complication implants that minimize lifetime revision risk.

Growing Reimbursement Mandates & Awareness

The Women's Health and Cancer Rights Act guarantees comprehensive reconstruction benefits across US group health plans, and February 2025 billing-code preservation for DIEP and GAP flaps underscores regulator commitment to advanced autologous techniques. State-level actions, such as California's July 2024 Medi-Cal policy update, broaden access to implant procedures for lower-income patients. Major private payers have redefined reconstruction as medically necessary, covering symmetry surgeries and complication management. As ambulatory centers embrace value-based payment models, surgeons gain financial incentives to adopt technologies that reduce operative time and downstream revisions, accelerating demand for AI-guided sizing software paired with cohesive-gel implants.

High Procedure & Device Costs In Emerging Markets

Average out-of-pocket costs for implant reconstruction in Southeast Asia exceed 45% of median annual income, limiting uptake outside major urban centers. Local payers seldom reimburse advanced biomaterials, forcing surgeons to rely on saline implants that carry higher revision risk. Multinational device firms must localize manufacturing or offer tiered price structures to penetrate these cost-sensitive regions. Government pilot programs in India and Thailand to subsidize reconstruction for low-income patients have shown positive early results but remain limited in scope.

Other drivers and restraints analyzed in the detailed report include:

- Advancements In Cohesive-Gel & Gummy-Bear Implants

- Surge In Nipple-Sparing & Pre-Pectoral Mastectomies

- Implant-Safety Concerns (BIA-ALCL, Capsular Contracture)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Breast implants retained 43.55% share of the breast reconstruction market in 2024, driven by broad surgeon familiarity and predictable outcomes. Yet 3-D bioprinted scaffolds and regenerative implants are growing at a 15.25% CAGR, signaling a pivot to tissue-engineering platforms that minimize foreign-body responses and enable personalized shapes. Traditional tissue expanders still bridge staged reconstructions, but their role is narrowing as pre-pectoral, single-stage procedures gain popularity.

The breast reconstruction industry increasingly values devices that reduce revision rates. AI-guided sizing software pairs with cohesive-gel implants to deliver custom profiles, while poly-4-hydroxybutyrate scaffolds support natural tissue ingrowth. BD's STANCE trial on GalaFLEX LITE highlights bioabsorbable meshes that address the 54% capsular-contracture recurrence in revision surgeries. Such innovations are reshaping hospital procurement criteria toward long-term cost savings and patient-reported outcomes.

Silicone held 45.53% of breast reconstruction market share in 2024, backed by decades of refinement and recent FDA clearances for larger-volume options. Biologic mesh, however, leads growth at 9.15% CAGR as surgeons seek materials that promote vascularized tissue integration and reduce chronic inflammation. Saline implants remain relevant for patients with specific safety concerns but are gradually losing ground.

In parallel, synthetic meshes face heightened scrutiny over permanence and infection risk, spurring demand for biodegradable alternatives. Research into environmental footprints of implant supply chains also favors biologic and biodegradable materials with lower carbon impacts, aligning procurement policies with hospital ESG targets.

The Breast Reconstruction Market Report is Segmented by Product (Breast Implants, Tissue Expanders, and More), Material Type (Silicone, Saline, and More), Reconstruction Technique (Implant-Based, and More), End User (Hospitals, Ambulatory Care Centers, and More), Application (Post-Mastectomy Cancer Reconstruction, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the breast reconstruction market with 37.72% share in 2024, underpinned by federal coverage mandates and a dense network of board-certified plastic surgeons. The region also hosts many pivotal trials, allowing earlier access to next-generation implants and biologic meshes. Market expansion is expected to remain steady as AI-guided planning tools penetrate large hospital systems and ambulatory surgery centers.

Asia-Pacific is the fastest-growing region, forecast at 9.22% CAGR through 2030. Rising breast-cancer prevalence, expanding middle-class incomes, and cultural normalization of reconstruction fuel procedure volumes, while Japan's immediate-reconstruction rate of 11.2% illustrates latent upside. Government initiatives to subsidize mastectomy care in China and India are slowly being extended to reconstruction, opening a path for cost-optimized implants and locally manufactured meshes.

Europe sustains moderate growth under universal healthcare frameworks that ensure baseline access, though procedure uptake varies by country. Latin America and the Middle East/Africa remain nascent markets, with growth contingent on surgical-infrastructure build-out and clinician-training partnerships. Multinational firms that localize production and align product portfolios with regional reimbursement tiers will capture early mover advantages.

- AbbVie (ALLERGAN)

- Johnson & Johnson

- Sientra

- Establishment Labs

- GC Aesthetics plc

- Polytech Health & Aesthetics

- RTI Surgical

- Groupe Sebbin

- Integra LifeSciences

- Silimed

- Laboratoires Expanscience

- Ideal Implant Inc.

- BellaSeno GmbH

- CollPlant Biotechnologies

- Stratasys

- HansBiomed Co. Ltd.

- Motiva USA LLC

- Tissue Regenix

- Decomedical S.r.l.

- Implantech Associates

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence Of Breast Cancer

- 4.2.2 Growing Reimbursement Mandates & Awareness

- 4.2.3 Advancements In Cohesive-Gel & Gummy-Bear Implants

- 4.2.4 Surge In Nipple-Sparing & Pre-Pectoral Mastectomies

- 4.2.5 3-D Bioprinted Regenerative Implants Entering Clinical Trials

- 4.2.6 AI-Guided Imaging & Sizing Reducing Revision Surgeries

- 4.3 Market Restraints

- 4.3.1 High Procedure & Device Costs In Emerging Markets

- 4.3.2 Implant-Safety Concerns (BIA-ALCL, Capsular Contracture)

- 4.3.3 Shortage Of Microsurgical Expertise For Autologous Flaps

- 4.3.4 ESG-Driven Silicone & ADM Supply-Chain Disruptions

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Breast Implants

- 5.1.2 Tissue Expanders

- 5.1.3 Acellular Dermal Matrices (Biologic, Synthetic)

- 5.1.4 3-D Bioprinted Scaffolds & Regenerative Implants

- 5.1.5 Other Adjunct Products (NAC prosthetics, fixation devices)

- 5.2 By Material Type

- 5.2.1 Silicone

- 5.2.2 Saline

- 5.2.3 Autologous Tissue

- 5.2.4 Biologic Mesh

- 5.2.5 Synthetic Mesh

- 5.3 By Reconstruction Technique

- 5.3.1 Implant-based

- 5.3.2 Autologous Tissue

- 5.3.3 Hybrid

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgery Centers

- 5.4.3 Specialty Aesthetic Clinics

- 5.5 By Application

- 5.5.1 Post-mastectomy Cancer Reconstruction

- 5.5.2 Prophylactic Mastectomy

- 5.5.3 Trauma & Congenital Deformity

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AbbVie (ALLERGAN)

- 6.3.2 Johnson & Johnson (Mentor Worldwide)

- 6.3.3 Sientra Inc.

- 6.3.4 Establishment Labs SA

- 6.3.5 GC Aesthetics plc

- 6.3.6 Polytech Health & Aesthetics GmbH

- 6.3.7 RTI Surgical Inc.

- 6.3.8 Groupe Sebbin SAS

- 6.3.9 Integra LifeSciences

- 6.3.10 Silimed

- 6.3.11 Laboratories Arion

- 6.3.12 Ideal Implant Inc.

- 6.3.13 BellaSeno GmbH

- 6.3.14 CollPlant Biotechnologies

- 6.3.15 Stratasys Ltd.

- 6.3.16 HansBiomed Co. Ltd.

- 6.3.17 Motiva USA LLC

- 6.3.18 Tissue Regenix Group plc

- 6.3.19 Decomedical S.r.l.

- 6.3.20 Implantech Associates

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment