|

시장보고서

상품코드

1842687

길랭 바레 증후군 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Guillain-Barre Syndrome - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

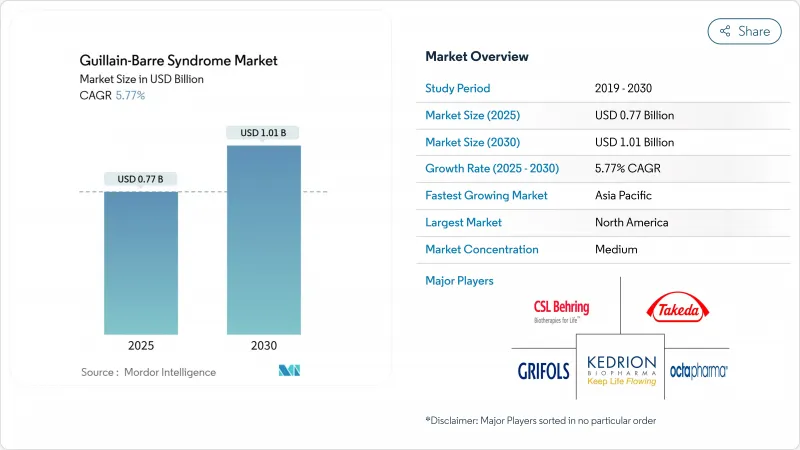

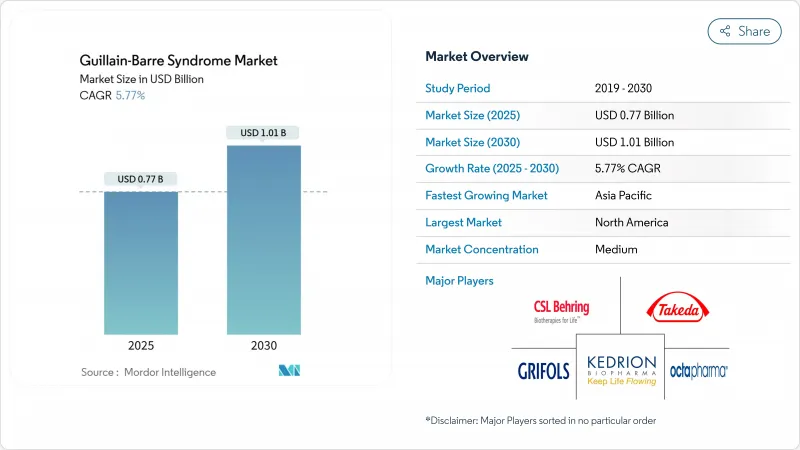

길랭 바레 증후군 시장은 2025년에는 7억 6,700만 달러에 이르고, 2030년에는 10억 1,000만 달러로 확대될 것으로 예상되며, CAGR은 5.77%를 나타낼 전망입니다.

보체 억제제의 획기적인 개발, 메디케어에 의한 재택 주입의 보험 적용, COVID 후의 신경학적 합병증에 의한 환자층의 확대 등의 영향을 받아, 수요는 종래의 면역조절제로부터 정밀 표적 생물 제제로 이행하고 있습니다. IVIG는 여전히 주도하고 있지만, 생물학적 제형의 채용이 증가하고 있다는 것은 임상 진료가 질병 특이적 억제 전략으로 전환되고 있음을 보여줍니다. 특히 아시아태평양의 분획 공장의 능력 증강은 지역 간 경쟁을 격화시키는 한편 공급 병목 현상을 완화하고 있습니다. 그럼에도 불구하고, 유럽이 미국 혈장 기증자에 의존하고 있는 것은 임상 요구 증가에도 불구하고 세계적인 성장을 억제할 수 있는 구조적인 취약성을 부각시키고 있습니다.

세계의 길랭 바레 증후군 시장 동향과 인사이트

세계 GBS 유병률 상승과 인구 고령화

노인(65세 이상)이 2030년까지 연평균 복합 성장률(CAGR) 8.83%에서 가장 급성장하는 그룹이기 때문에 세계적인 인구통계학적 변화가 길랭 바레 증후군 시장을 재구축하고 있습니다. NIH는 개인화 프로토콜을 개선할 수 있는 유전적 감수성 마커를 확인하기 위해 300만 달러를 기록했습니다. 2020년부터 2021년에 걸쳐, GBS의 장애와 함께 사는 연수가 거의 두배로 되어, 팬데믹이 질병 부담을 증폭시키고 있는 것을 나타냈습니다. WHO가 푸네에서 실시한 감시에서는 저·중소득 지역에서 환자수가 증가하고 있는 것을 계속 확인하고 있으며, 개별화된 면역요법 경로의 필요성을 강조하고 있습니다.

혈장 분획기의 지속적인 능력 향상은 IVIG 공급을 뒷받침

IVIG의 만성적인 공급 부족을 해소하기 위해, 혈장 분획 제제 제조 시설의 증설이 진행되고 있습니다. CSL사의 면역글로불린 매출은 15% 증가해 과거공급 부족에도 불구하고 견조한 흡수를 반영하고 있습니다. 인도네시아의 60만 리터 분획 플랜트는 동남아시아 최대의 증설로 지역의 수입 의존도를 저하시킵니다. 케돌리온의 FDA 인증 시설은 치료 단백질 수율을 안정화시키는 품질 향상을 강조합니다. 그러나 유럽에서는 추가로 200만 명의 혈장 기증자가 필요하며 구조적 부족이 계속되고 있습니다.

만성 IVIG 부족과 고가의 치료비

IVIG의 풀코스에는 5,000-1만 달러의 비용이 들고, 특히 품질과 관련된 로트의 취하에 의한 공급의 중단이 발생한 경우에는 큰 예산 압박 요인이 됩니다. 카타르의 10년간의 감사는 단 669명의 환자에게 1,000만 달러가 소비되었음을 기록하고 있으며, 신흥국의 경제적 부담이 부각되고 있습니다.

부문 분석

2024년 길랭 바레 증후군 시장은 면역글로불린 정주제제가 72.32%의 점유율로 선도했지만 보체 억제제 및 기타 신규 생물제제는 2030년까지 연평균 복합 성장률(CAGR) 9.46%를 나타낼 전망입니다. ANX005의 양호한 3단계 데이터가 위약에 비해 2.4배 향상된 기능을 보였기 때문에 이러한 표적 생물학적 제제의 길랭 바레 증후군 시장 규모는 2030년까지 3억 1,000만 달러 이상에 달할 것으로 예상됩니다. 에프가르티기모드는 난치성 AMAN 증례에서 설득력 있는 결과를 내고 있으며, 기전 특이적 개입으로의 변화가 확인되고 있습니다.

전통적인 혈장 교환은 비용 제약 환경에서 여전히 필수적이며, 길랭 바레 증후군 시장 점유율은 기증자 혈장 이용 가능성과 치료 프로토콜이 일치하는 경우 안정적입니다. 물리치료 및 인공 호흡 지원과 같은 보조 지원 요법은 최적의 생물학적 노출을 보장하기 위해 정밀 투여 분석과 통합되어 있습니다. 이러한 추세를 종합하면 길랭 바레 증후군 시장이 광범위한 면역 조절에서 표적 경로 억제로 전환하고 있음을 알 수 있습니다.

정맥내 투여는 2024년 길랭 바레 증후군 시장의 79.21%를 차지하며, 병원 인프라와 임상의의 숙련도에 의해 지원되었습니다. 한편, 피하 면역글로불린 제형은 CAGR 7.78%로 급성장하고 있으며, 이는 XEMBIFY의 확대 라벨에 의한 격주 투여 요법이 뒷받침하고 있습니다. 수동 푸시 Ig20Gly는 자체 투여를 단순화하고 펌프 비용을 줄이기 때문에 안정적인 환자들 사이에서 채택이 확산되고 있습니다.

재택치료는 치료 물류를 재형성하고 가치 기반 모델과의 무결성을 촉진합니다. 정밀 투여는 낭비를 최소화함으로써 피하 섭취를 추가로 지원합니다. 길랭 바레 증후군의 피하 투여 시장 규모는 새로운 제형이 승인됨에 따라 꾸준히 확대될 것으로 예측됩니다.

지역 분석

북미는 2024년에 44.65%의 점유율로 길랭 바레 증후군 시장을 선도해, 메디케어에 의한 재택 주입의 상환과 정밀 분석 플랫폼에의 유비쿼터스 액세스에 지지되었습니다. 미세한 전자 의료 기록은 조기 진단 및 결과 추적을 용이하게 하며, 높은 비용의 생물학적 제형에 대한 지불자의 신뢰를 강화하고 있습니다. NIH가 주도하는 설문조사 컨소시엄은 지역 전반에 걸쳐 혁신을 파급하는 획기적인 발견 프로그램에 자금을 모으고 있습니다.

유럽은 2위를 차지하고 있지만, 혈장 유래 의약품의 약 40%를 미국으로부터 수입하고 있으며, 공급의 취약성에 직면하고 있습니다. 규제 당국은 국내 기증자 모집을 장려하고 있지만 인구 역학의 고령화는 수집 목표를 복잡하게 만듭니다. 헬스케어 인프라는 발전하고 있는 것, 새로운 생물제제에 대한 상환이 불투명하기 때문에 성장이 억제될 가능성이 있습니다.

아시아태평양은 CAGR 8.58%로 가장 급속히 확대되고 있으며, 인도네시아의 60만 리터 신 플랜트와 같은 현지 분획 능력에 대한 대규모 투자가 그 원동력이 되고 있습니다. 도시화의 발전과 감시 개선으로 잠재적인 환자층이 확대되고 있습니다. 중국의 이질적인 이환 프로파일은 지역에 맞는 제품 포트폴리오의 필요성을 강조합니다.

라틴아메리카, 중동, 아프리카가 틈새 시장에서 계속됩니다. 소량의 플라스마 페레시스 프로토콜과 이동식 주입 장치는 인프라의 장벽을 줄여 자원이 제한된 환경에서 비용 효율적인 옵션을 제공합니다. 이들 지역을 총칭하면 길랭 바레 증후군 시장이 지역 밀착형의 제조·판매 체제를 추진하고 있는 것을 알 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계 GBS 유병률 상승과 인구 고령화

- 혈장 분획 제제 제조업체의 지속적인 생산 능력 증강이 정맥내 면역글로불린(IVIG) 공급을 뒷받침

- 보다 신속한 약사 규제(미국 FDA의 패스트 트랙, 브레이크 스루 등)가 신규 생물 제제를 뒷받침

- 혈장 분획 제제 제조업체에 의한 IVIG/PLEX의 능력 증강 증가

- COVID-19와 관련된 감염 후 GBS 발병률의 급증

- 정밀 투여 분석이 낭비를 삭감해, 지불측의 채용을 가능

- 시장 성장 억제요인

- 만성적인 IVIG 부족과 높은 치료비

- 부작용 및 혈전 색전증 우려로 인한 IVIG의 반복 투여 제한

- LMICs의 적응 외 IVIG에 관한 상환 감사의 강화

- 혈장 교환에 있어서 재발 리스크의 높이 근거와 비용 대비 효과 우려

- 가치/공급망 분석

- 규제 상황

- 기술 전망

- Porter's Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모와 성장 예측

- 치료제별

- 정맥 내 면역글로불린(IVIG)

- 혈장 교환 요법(PLEX)

- 보체 억제제 및 신개념 생물학적 제제

- 기타 보조/지지 요법

- 투여 경로별

- 정맥 내

- 피하

- 경구/장내

- 유통 채널별

- 병원 약국

- 전문 및 소매 약국

- 가정 주입 서비스 제공자

- 환자 연령층별

- 소아(18세 미만)

- 성인(18-64세)

- 노년(65세 이상)

- 질환 유형별

- AIDP(급성 염증성 탈수초성 다발성 경화증)

- AMAN(급성 운동 축삭성 다발성 경화증)

- AMSAN(급성 운동-감각 축삭성 다발성 경화증)

- 밀러-피셔 증후군

- 기타 희귀 유형(PCB, PNC 등)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- CSL Ltd.

- Takeda Pharmaceutical

- Grifols SA

- Octapharma AG

- Kedrion Biopharma

- Baxter International

- Biotest AG

- China Biologic Products Holdings

- Bio Products Laboratory(BPL)

- Sanquin Plasma Products

- Annexon Biosciences

- Argenx SE

- Hansa Biopharma

- Haemonetics Corp.

- Fresenius Medical Care

- Terumo BCT

- Octapharma Plasma(US)

- Cellenkos Inc.

- ImmunoForge Inc.

- Sobi(Swedish Orphan Biovitrum)

제7장 시장 기회와 전망

KTH 25.11.05The Guillain-Barre Syndrome market stood at USD 767 million in 2025 and is forecast to advance to USD 1.01 billion by 2030, translating into a 5.77% CAGR.

Demand is pivoting from traditional immunomodulators toward precision-targeted biologics, influenced by complement inhibitor breakthroughs, Medicare-backed home infusion coverage, and post-COVID neurological complications that have widened patient pools. IVIG still leads today, yet rising biologic adoption signals an inflection in clinical practice toward disease-specific inhibition strategies. Capacity expansions at fractionation plants, especially in Asia-Pacific, are easing supply bottlenecks while sharpening regional competition. Even so, Europe's continued reliance on US plasma donors underscores structural fragility that may temper global growth despite rising clinical need.

Global Guillain-Barre Syndrome Market Trends and Insights

Rising Global Prevalence of GBS & Ageing Population

Global demographic shifts are reshaping the Guillain-Barre Syndrome market as geriatric patients (>=65 years) represent the fastest-growing group at 8.83% CAGR through 2030. NIH has earmarked USD 3 million to pinpoint genetic susceptibility markers that may refine personalized protocols. Years lived with disability for GBS almost doubled from 2020 to 2021, showing the pandemic's amplifying effect on disease burden. WHO's surveillance in Pune continues to confirm elevated case counts in low-to-middle-income regions, emphasizing the need for tailored immunotherapy pathways.

Sustained Capacity Additions by Plasma Fractionators Are Boosting IVIG Supply

Plasma fractionators are expanding to alleviate chronic IVIG shortages. CSL posted 15% immunoglobulin sales growth, reflecting robust uptake despite historical supply gaps. Indonesia's 600,000-liter fractionation plant marks Southeast Asia's largest build-out and trims regional dependence on imports. Kedrion's FDA-cleared facility underscores quality gains that help stabilize therapeutic protein yields. Yet Europe's need for 2 million more plasma donors shows that structural shortages persist.

Chronic IVIG Shortages & High Therapy Cost

A full IVIG course costs USD 5,000-10,000, imposing heavy budget pressure, especially when supply disruptions arise from quality-related lot withdrawals. Qatar's 10-year audit logged USD 10 million spent on just 669 patients, highlighting economic burdens in emerging systems.

Other drivers and restraints analyzed in the detailed report include:

- Faster Regulatory Pathways Boosting Novel Biologics

- Adverse-Event & Thrombo-Embolism Concerns Limiting Repeat-Dose IVIG

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Intravenous immunoglobulin led the Guillain-Barre Syndrome market with a 72.32% share in 2024, yet complement-inhibitors and other novel biologics are growing at 9.46% CAGR through 2030. The Guillain-Barre Syndrome market size for these targeted biologics is projected to surpass USD 310 million by 2030 as positive Phase 3 data from ANX005 show 2.4-fold functional improvements over placebo. Efgartigimod has delivered compelling results in refractory AMAN cases, confirming the shift toward mechanism-specific intervention.

Traditional plasma exchange remains vital in cost-constrained settings, and its share of the Guillain-Barre Syndrome market is steady where donor plasma availability aligns with treatment protocols. Adjunct supportive care-such as physiotherapy and ventilatory support-continues to integrate with precision dosing analytics to ensure optimal biological exposure. Collectively, these trends illustrate how the Guillain-Barre Syndrome market is transitioning from broad immunomodulation to targeted pathway inhibition.

The intravenous route accounted for 79.21% of the Guillain-Barre Syndrome market in 2024, supported by hospital infrastructure and clinician familiarity. Subcutaneous immunoglobulin, however, is the fastest-growing at 7.78% CAGR, propelled by biweekly dosing regimens under the expanded XEMBIFY label. Manual push Ig20Gly simplifies self-administration and reduces pump costs, broadening adoption among stable patients.

Home-based care is reshaping therapeutic logistics and driving payer alignment with value-based models. Precision dosing further supports subcutaneous uptake by minimizing wastage. The Guillain-Barre Syndrome market size for subcutaneous modalities is forecast to grow steadily as new formulations reach regulatory approval.

Guillain-Barr Syndrome Market Report is Segmented by Therapeutics (Intravenous Immunoglobulin, Plasma Exchange, and More), Route of Administration (Intravenous, Subcutaneous and More), Distribution Channel (Hospital Pharmacies and More), Patient Age Group (Pediatric, Adults and More), Disease Variant (Acute Inflammatory Demyelinating, AMAN and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the Guillain-Barre Syndrome market with a 44.65% share in 2024, supported by Medicare reimbursement for home infusion and ubiquitous access to precision analytics platforms. Granular electronic health records facilitate earlier diagnosis and outcome tracking, reinforcing payer confidence in high-cost biologics. Research consortia, such as those spearheaded by NIH, continue to draw funding into breakout discovery programs that amplify innovation spill-overs across the region.

Europe trails at second but confronts supply fragility, importing roughly 40% of its plasma-derived medicines from the United States. Regulatory agencies are encouraging domestic donor recruitment, yet demographic aging complicates collection targets. Despite advanced healthcare infrastructure, uncertain reimbursement for newer biologics could temper growth.

Asia-Pacific is the fastest-expanding at 8.58% CAGR, powered by large investments in local fractionation capacity such as Indonesia's new 600,000-liter plant. Rising urbanization and improved surveillance reveal a larger underlying patient pool. China's heterogeneous incidence profiles emphasize the need for regionally tailored product portfolios.

Latin America, the Middle East, and Africa follow with niche opportunities. Small-volume plasmapheresis protocols and mobile infusion units reduce infrastructure barriers, offering cost-effective alternatives in resource-limited settings. Collectively, these regions underscore the Guillain-Barre Syndrome market's drive toward localized manufacturing and distribution resilience.

- CSL Behring

- Takeda Pharmaceuticals

- Grifols

- Octapharma

- Kedrion Biopharma

- Baxter

- Biotest

- China Biologic Products Holdings

- Bio Products Laboratory (BPL)

- Sanquin Plasma Products

- Annexon Biosciences

- Argenx SE

- Hansa Biopharma

- Haemonetics Corp.

- Fresenius

- Terumo

- Octapharma Plasma (US)

- Cellenkos Inc.

- ImmunoForge Inc.

- Sobi (Swedish Orphan Biovitrum)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Prevalence Of GBS & Ageing Population

- 4.2.2 Sustained Capacity Additions By Plasma-Fractionators Are Boosting Intravenous Immunoglobulin (IVIG) Supply

- 4.2.3 Faster Regulatory Pathways (E.G., US FDA Fast-Track, Breakthrough) Boosting Novel Biologics

- 4.2.4 Growing IVIG/PLEX Capacity Expansions By Plasma-Fractionators

- 4.2.5 COVID-19-Linked Spike In Post-Infectious GBS Incidence

- 4.2.6 Precision-Dosing Analytics Reducing Wastage & Enabling Payor Uptake

- 4.3 Market Restraints

- 4.3.1 Chronic IVIG Shortages & High Therapy Cost

- 4.3.2 Adverse-Event & Thrombo-Embolism Concerns Limiting Repeat-Dose IVIG

- 4.3.3 Tighter Reimbursement Audits On Off-Label IVIG In LMICs

- 4.3.4 Evidence Of Higher Relapse Risk And Cost-Effectiveness Concerns For Plasma Exchange

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Therapeutics

- 5.1.1 Intravenous Immunoglobulin (IVIG)

- 5.1.2 Plasma Exchange (PLEX)

- 5.1.3 Complement-inhibitors & Novel Biologics

- 5.1.4 Other Adjunct / Supportive Care

- 5.2 By Route of Administration

- 5.2.1 Intravenous

- 5.2.2 Sub-cutaneous

- 5.2.3 Oral / Enteral

- 5.3 By Distribution Channel

- 5.3.1 Hospital Pharmacies

- 5.3.2 Specialty & Retail Pharmacies

- 5.3.3 Home-Infusion Providers

- 5.4 By Patient Age Group

- 5.4.1 Pediatric (<18 yrs)

- 5.4.2 Adult (18 - 64 yrs)

- 5.4.3 Geriatric (>=65 yrs)

- 5.5 By Disease Variant

- 5.5.1 AIDP (Acute Inflammatory Demyelinating)

- 5.5.2 AMAN (Acute Motor Axonal)

- 5.5.3 AMSAN (Acute Motor-Sensory Axonal)

- 5.5.4 Miller-Fisher Syndrome

- 5.5.5 Other rare variants (PCB, PNC, etc.)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 CSL Ltd.

- 6.3.2 Takeda Pharmaceutical

- 6.3.3 Grifols S.A.

- 6.3.4 Octapharma AG

- 6.3.5 Kedrion Biopharma

- 6.3.6 Baxter International

- 6.3.7 Biotest AG

- 6.3.8 China Biologic Products Holdings

- 6.3.9 Bio Products Laboratory (BPL)

- 6.3.10 Sanquin Plasma Products

- 6.3.11 Annexon Biosciences

- 6.3.12 Argenx SE

- 6.3.13 Hansa Biopharma

- 6.3.14 Haemonetics Corp.

- 6.3.15 Fresenius Medical Care

- 6.3.16 Terumo BCT

- 6.3.17 Octapharma Plasma (US)

- 6.3.18 Cellenkos Inc.

- 6.3.19 ImmunoForge Inc.

- 6.3.20 Sobi (Swedish Orphan Biovitrum)

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment