|

시장보고서

상품코드

1842688

의료용 특수 의자 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Specialty Medical Chairs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

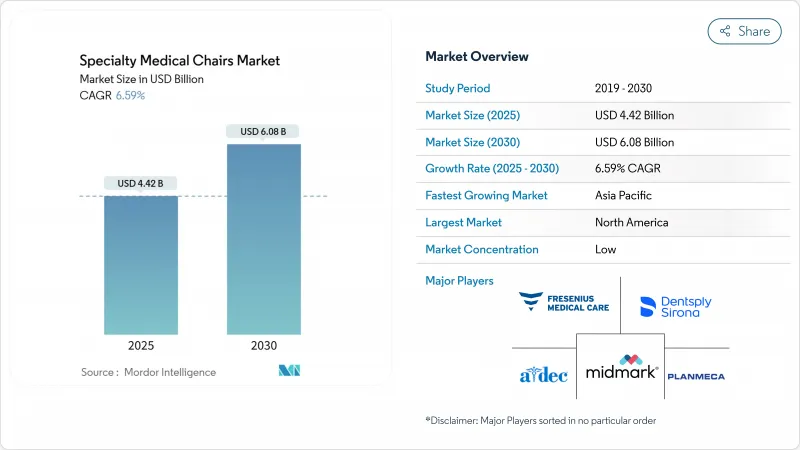

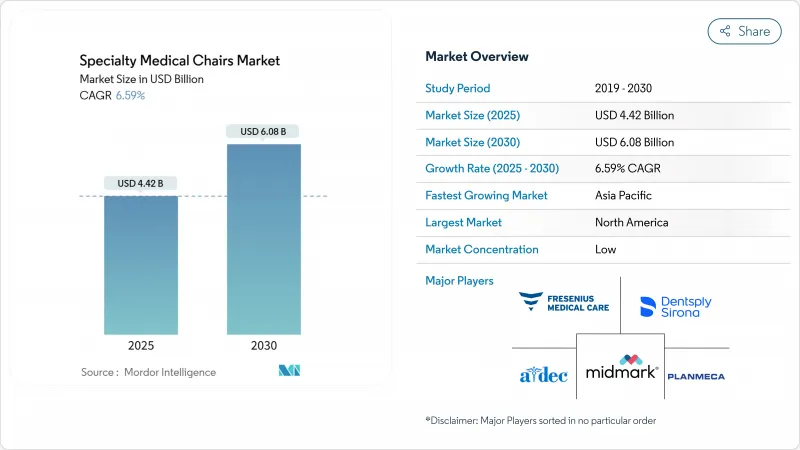

의료용 특수 의자 시장은 2025년에 44억 2,000만 달러, 2030년에는 60억 8,000만 달러에 달하고, CAGR 6.59%로 성장할 전망입니다.

이 기세는 인구의 고령화, 다질환 합병증, 복잡한 절차의 외래 및 재택으로의 이동의 충돌을 반영하며, 이들 모두는 인체 공학적 기술의 풍부한 의자에 대한 수요를 높입니다. 의료 제공업체는 보다 엄격한 욕창 예방 프로토콜을 준수하면서 처리량을 최적화하는 완전 전기, IoT 호환 모델에 끌려가고 있습니다. 자본 예산은 유행 시대의 동결을 통해 점차 완화되고 있지만, 교체 결정은 입증 가능한 ROI, 규제 의무, 사이버 보안에 대한 대응과 밀접하게 관련되어 있습니다. 동시에 의료용 특수 의자 시장은 유럽의 MDR규칙과 화재안전기준에 의한 비용 상승의 역풍에 직면하고 있으며, 의자장비는 12-15% 상승하기 때문에 기존 제조업체의 스케일 메리트가 강화되고 있습니다.

세계 의료용 특수 의자 시장 동향과 통찰

고령화와 다질환의 부담이 투석, 화학요법, 비만치료용 의자 수요를 가속

85세 이상의 고령자는 65-74세의 3배의 헬스케어 자원을 사용하고 있으며, 미국의 백세인구는 2054년까지 4배가 될 것으로 예측되고 있습니다. 이 인구 역학의 급증은 투석, 종양, 비만 치료 부문에 장기간의 치료, 높은 체중 제한, 정밀한 포지셔닝에 대응하는 의자의 도입을 촉진하고 있습니다. 메디케어 인정을 받은 ASC는 연령에 연동한 처치에 대응할 수 있도록 용량을 계속 확대하고 있으며, 고급 의자의 지속적인 수요를 확보하고 있습니다. 의료 시스템은 또한 회전 시간을 단축하고, 간병인의 부담을 줄이고, 감염 제어의 마무리를 통합한 설계로 총 소유 비용을 절감하는 것을 고려합니다.

풀 파워 IoT 지원 의자로의 기술 이동은 의료 기관의 ROI 향상

연결된 의자는 사용 상황과 유지 보수 데이터를 병원의 자산 관리 플랫폼에 직접 공급하여 다운 타임을 줄이는 예측 서비스를 가능하게합니다. 구급부에서는 IoT 통합으로 Mt. Sinai가 대기 시간을 50% 단축했습니다. 특히 안과 및 치과에서는 사전 설정으로 환자 간의 설정 시간을 단축하고 표준화된 케어 경로를 지원합니다. 사이버 공격의 위험이 증가함에 따라 암호화 된 펌웨어와 네트워크 파티셔닝을 갖춘 완전 전기 시스템은 필수적인 자본 구임베디드니다.

COVID 후 자본 예산 동결로 교체주기 감소

병원의 영업 이익률은 2024년에 1-2%로 압축되며 장비 수명주기는 이전 벤치마크를 크게 초과해야 합니다. 이익 풀은 2027년까지 연평균 복합 성장률(CAGR) 7%로 회복될 것으로 예상되지만, 의사결정자는 여전히 규제적 의무 또는 측정 가능한 처리량 향상 중 하나에 연결된 구매에만 권한을 부여하고 있습니다. 대규모 의료 시스템일수록 자금 조달이 쉽기 때문에 의자 업그레이드를 다음 사이클로 앞으로 밀어낼 수 있는 지방 독립 병원과의 기술 격차가 확산되고 있습니다.

부문 분석

치료용 의자는 혁신의 템포를 만들어 이 부문의 의료용 특수 의자 시장 규모는 2025-2030년에 CAGR 7.41%로 상승할 것으로 예측됩니다. 치과, 이비인후과, 안과 클리닉이 이미징 포트, AI 가이드 부착 포지셔닝, 항균 천을 결합한 모델을 채택한 것이 수익의 성장으로 이어지고 있습니다. 진찰 의자는 2024년에 38.67% 시장 점유율을 유지하며 순환기과와 투석과 같은 핵심 전문과에 서비스를 제공합니다. 폭넓은 설치 베이스가 교체 수요를 지지하고 있지만, 현재는 치료용 의자가 비싼 이폭의 선진을 끊고 있습니다.

시뮬레이션 조사에 따르면, 치과용 의자의 인체공학을 기반으로 한 첨단 디자인은 환자의 시야를 넓히는 동시에 임상의의 허리에 대한 부담을 42% 완화할 수 있어 비싼 정가를 정당화할 수 있습니다. 제조업체 각 사는 측와위 분만을 서포트해, 수술 모드에의 신속한 긴급 변환을 가능하게 하는 디자인으로, 분만 센터를 타겟으로 하고 있습니다. 체중 400 파운드의 휴대용 채혈용 의자는 지역에 뿌리를 둔 검진 프로그램에 계속 침투하여 포트폴리오의 가치 엔드 볼륨을 강화하고 있습니다.

재활용 의자는 환자 리프트 통합, 제로 엔트리 시트 높이, 보강 프레임이 필요한 노인과 비만 환자를 지원합니다. 2025년에는 세계 비만이 10억 명을 넘어 비만용 의자는 2자리수의 하위부문 성장을 달성합니다. 투석용 리클라이닝 의자는 재택 요법의 확대로부터 혜택을 받아 일부 모델에는 블루투스 연동 혈압 커프와 자동 팔걸이 회전 기능이 탑재되어 주사 바늘에 대한 액세스가 효율화되고 있습니다.

의료용 특수 의자 세계 시장은 제품 유형에는 진료용 의자(심장 진료용 의자, 분만용 의자 등), 치료용 의자, 재활용 의자가 포함됩니다. 기술 측면에서는 수동, 반전동, 전동 의자가 있으며, 최종 사용처로는 병원, 의원 및 치과, 그 외 다양한 시설이 있습니다. 지역적으로는 북미, 유럽, 아시아태평양 등을 포함하며, 시장 예측은 미국 달러(USD) 기준의 가치로 제공됩니다.

지역별 분석

북미는 ASC의 보급, 적극적인 IoT 도입, 재택투석의 조기상환을 반영하여 2024년 매출액의 41.23%를 창출했습니다. 미국의 의료 제공업체는 ESKD 치료 옵션의 인센티브와 고급 좌석이 필요한 VHA의 압력 상해 의무로부터 혜택을 받고 있습니다. 캐나다 주 계획에서는 투석실의 현대화가 진행되고 있으며, 멕시코의 민간 병원 그룹은 인바운드 의료 투어리즘을 캡처하기 위해 수술실을 업그레이드하고 있습니다. 이러한 요인이 결합되어 자본 예산은 하이 엔드의 완전 전기 모델을 지향하고 있으며, 연결성과 연관된 반복적인 소프트웨어 지원 계약이 촉진됩니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 7.34%를 기록하는 가장 빠르게 성장하는 지역입니다. 중국, 인도, 인도네시아의 각 정부는 병원 건설 및 종양 데이 케어 센터에 기록적인 자금을 투입하고 있으며, 각각은 점적 극 통합형 종양 리클라이닝 의자와 체중 적응형 센서 매트를 요구하고 있습니다. 호주 아이콘 그룹은 국경을 넘은 합작투자를 활용하여 말레이시아의 의자 수요를 개척하고 일본은 하이브리드 테라피 의자를 가정에 배치하는 원격 재활 프로그램을 가속화하고 있습니다. 현지 조달 전략과 기술 이전 협정이 납품 사이클을 단축하고 있지만, 제3차 의료시설에서는 여전히 일류 수입품이 높은 점유율을 차지하고 있습니다.

유럽은 MDR과 화재 안전 규정이 까다로운 가운데 성장이 느리지만 견고한 성장을 유지하고 있습니다. 독일, 프랑스, 영국은 체압 부상 방지 대책과 종양 데이 케어 업그레이드에 자금을 투입하여 미기후 관리 기능이 있는 스마트 리클라이너의 보급을 유지하고 있습니다. 노티파이드 바디의 용량 부족이 인증 취득 기간을 연장하고 소규모 공급업체의 의욕을 늘리고 평균 단가를 상승시킵니다. BREXIT 후 영국 제조업체는 이중 규제 트럭을 처리하고 공급 비용은 상승하지만 시장 접근은 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 도입

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 고령화와 다질환 부담이 투석, 화학요법, 비만치료 의자 수요를 가속

- 풀 파워, IoT 대응 의자에의 기술 변화가 의료 기관의 ROI를 개선

- OECD 회원국 병원에서의 압박 상해 방지 프로토콜의 의무화

- 재택 신장 케어 모델(미국 ESKD 치료 선택)이 주택용 투석 리클라이닝 의자에 박차를 가한다

- APAC의 Tier-2 도시에서의 종양 데이케어의 확대

- 치과 및 안과의 처리 건수 증가가 전문 의자의 업그레이드를 촉진

- 시장 성장 억제요인

- COVID 후의 자본 예산의 동결에 의한 임베디드 사이클의 감소

- 병원 외부 검사 의자에 대한 환급 격차

- 난연성과 MDR(EU) 의자장의 컴플라이언스에 의해 12-15%의 비용 증가

- 특수 의자의 높은 자본 비용으로 소규모 관행 채택 제한

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측(금액-달러)

- 제품 유형별

- 진찰 의자

- 심장 의자

- 분만 의자

- 채혈 의자

- 투석 의자

- 기타

- 치료의자

- 이비인후과 의자

- 안과 의자

- 치과 의자

- 기타 치료의자

- 재활 의자

- 노인 의자

- 소아 의자

- 비만 의자

- 기타

- 진찰 의자

- 기술별

- 수동식

- 반전동/유압

- 완전 전동/프로그램 가능

- 최종 사용자별

- 병원

- 진료소 및 치과의원

- 외래수술센터(ASC)

- 재택 간병 및 장기 간호

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Dentsply Sirona

- A-dec Inc.

- PLANMECA OY

- Midmark Corporation

- ATMOS MedizinTechnik GmbH & Co. KG

- G. Heinemann Medizintechnik GmbH

- DentalEZ

- Hill Laboratories Company

- Topcon Medical Systems Inc.

- Forest Dental

- Fresenius Medical Care AG & Co. KGaA

- Champion Manufacturing Inc.

- Invacare Corporation

- Stryker Corporation

- Danaher Corporation(Kavo Dental)

- Hill-Rom Holdings Inc.

- Digiterm Ltd.

- Drive DeVilbiss Healthcare

- Likamed GmbH

- Accora Ltd.

제7장 시장 기회와 전망

SHW 25.11.03The specialty medical chairs market stood at USD 4.42 billion in 2025 and is on track to reach USD 6.08 billion by 2030, advancing at a 6.59% CAGR.

This momentum reflects the collision of population aging, multimorbidity, and the shift of complex procedures into outpatient and home settings, all of which raise demand for ergonomic, technology-rich seating. Providers are gravitating toward fully-electric, IoT-enabled models that optimize throughput while complying with stricter pressure-injury prevention protocols. Capital budgets are gradually loosening after pandemic-era freezes, yet replacement decisions remain tightly linked to demonstrable ROI, regulatory mandates, and cybersecurity readiness. At the same time, the specialty medical chairs market faces cost headwinds from European MDR rules and fire-safety standards that add 12-15% to upholstery costs, reinforcing the advantage of scale for established manufacturers.

Global Specialty Medical Chairs Market Trends and Insights

Aging & Multimorbidity Burden Accelerates Demand for Dialysis, Chemo & Bariatric Chairs

People aged 85+ use triple the healthcare resources of the 65-74 cohort, and the U.S. centenarian population is projected to quadruple by 2054. This demographic surge pushes dialysis, oncology, and bariatric departments to install chairs engineered for lengthy therapies, higher weight limits, and precision positioning. Medicare-certified ASCs continue to expand capacity to handle age-linked procedures, ensuring sustained pull for premium seating. Health systems also factor in total-cost-of-ownership savings from designs that cut turnover time, lower caregiver strain, and integrate infection-control finishes.

Technology Shift to Fully-Powered, IoT-Enabled Chairs Improves ROI for Providers

Connected chairs feed utilization and maintenance data directly to hospital asset-management platforms, allowing predictive servicing that trims downtime. In emergency departments, IoT integration helped Mt. Sinai cut wait times by 50%. Preset configurations reduce setup time between patients and support standardized care pathways, especially in ophthalmology and dental suites. As cyberattack risks escalate, fully-electric systems equipped with encrypted firmware and network partitioning become essential capital purchases.

Capital-Budget Freezes Post-COVID Reduce Replacement Cycles

Hospital operating margins compressed to 1-2% in 2024, forcing equipment lifecycles to stretch well past prior benchmarks. Although profit pools are forecast to rebound at 7% CAGR by 2027, decision-makers still green-light only purchases tied to either regulatory obligation or measurable throughput gains. Larger health systems secure financing more easily, widening the technology gap with stand-alone rural hospitals that may postpone chair upgrades into the next cycle.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Pressure-Injury Prevention Protocols in OECD Hospitals

- Home-Based Kidney-Care Models Spur Residential Dialysis Recliners

- Fire-Retardancy & EU MDR Upholstery Compliance Adds 12-15% Cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Treatment chairs set the innovation tempo, and the specialty medical chairs market size for this segment is projected to climb at 7.41% CAGR between 2025-2030. Revenue growth stems from dental, ENT, and ophthalmic clinics adopting models that combine imaging ports, AI-guided positioning, and antimicrobial upholstery. Examination chairs retained 38.67% market share in 2024, serving core specialties such as cardiology and dialysis. Their broad installed base anchors replacement demand, yet treatment chairs now spearhead premium margins.

Simulation studies show advanced dental-chair ergonomics can cut lower-back stress on clinicians by 42% while expanding the patient visual field, justifying premium list prices. Manufacturers also target birthing centers with designs that support lateral delivery positions and quick emergency conversion to operating mode. Portable blood-drawing chairs with 400-lb capacities keep penetrating community-based screening programs, reinforcing volume at the value end of the portfolio.

Rehabilitation chairs cater to geriatric and bariatric populations that require patient-lift integration, zero-entry seat heights, and reinforced frames. With global obesity crossing 1 billion adults in 2025, bariatric variants achieve double-digit sub-segment growth. Dialysis recliners benefit from home-therapy expansion, and some models now include Bluetooth-linked blood-pressure cuffs and automated armrest rotation to streamline needle access.

Global Specialty Medical Chairs Market is Segmented by Product Type (Examination Chairs[Cardiac Chairs, Birthing Chairs, and More], Treatment Chairs, and Rehabilitation Chairs), Technology (Manual, Semi-Electric, and Fully-Electric), End-User (Hospitals, Clinics & Dental Practices, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 41.23% of 2024 revenue, reflecting widespread ASC penetration, aggressive IoT adoption, and early reimbursement for home dialysis. U.S. providers benefit from ESKD Treatment Choices incentives and from VHA pressure-injury mandates that require advanced seating. Canada's provincial plans modernize dialysis units, and Mexican private hospital groups upgrade operatories to capture inbound medical tourism. Collectively, these factors keep capital budgets oriented toward high-end, fully-electric models and fuel recurring software-support contracts tied to connectivity.

Asia-Pacific is the quickest-expanding territory, registering a 7.34% CAGR through 2030. Governments in China, India, and Indonesia are funneling record sums into hospital construction and oncology-day-care centers, each demanding oncology recliners with IV-pole integration and weight-adaptive sensor mats. Australia's Icon Group leveraged cross-border joint ventures to seed chair demand in Malaysia, while Japan accelerates tele-rehabilitation programs that deploy hybrid therapy chairs to homes. Local sourcing strategies and technology-transfer pacts shorten delivery cycles, yet top-tier imports still command premium share in tertiary facilities.

Europe maintains solid, though slower, growth amid stringent MDR and fire-safety compliance. Germany, France, and the United Kingdom channel funds into pressure-injury prevention initiatives and oncology-day-care upgrades, sustaining uptake of smart recliners with microclimate management. Shortage of notified-body capacity extends certification timelines, discouraging smaller suppliers and nudging average unit prices upward. Post-Brexit, UK manufacturers juggle dual regulatory tracks, raising cost-to-serve but preserving market access.

- Dentsply Sirona

- A-dec

- Planmeca

- Midmark

- ATMOS MedizinTechnik

- G. Heinemann Medizintechnik

- DentalEZ

- Hill Laboratories Company

- Topcon Medical Systems Inc.

- Forest Dental

- Fresenius

- Champion Manufacturing Inc.

- Invacare

- Stryker

- Danaher Corporation (Kavo Dental)

- Hill-Rom

- Digiterm Ltd.

- Drive DeVilbiss Healthcare

- Likamed GmbH

- Accora Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging & Multimorbidity Burden Accelerates Demand for Dialysis, Chemo & Bariatric chairs

- 4.2.2 Technology Shift to Fully-powered, IoT-enabled Chairs Improves ROI for Providers

- 4.2.3 Mandatory Pressure-injury Prevention Protocols in OECD Hospitals

- 4.2.4 Home-based Kidney-care Models (ESKD Treatment Choices, US) Spur Residential Dialysis Recliners

- 4.2.5 Oncology-day-care Expansion in Tier-2 APAC Cities

- 4.2.6 Rising Dental & Ophthalmic Procedure Volumes Drive Specialty Chair Upgrades

- 4.3 Market Restraints

- 4.3.1 Capital-budget Freezes Post-COVID Reduce Replacement Cycles

- 4.3.2 Reimbursement Gaps for Examination Chairs Outside Hospitals

- 4.3.3 Fire-retardancy & MDR (EU) Upholstery Compliance Adds 12-15 % Cost

- 4.3.4 High Capital Cost of Specialty Chairs Limits Adoption by Small Practices

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value - USD)

- 5.1 By Product Type

- 5.1.1 Examination Chairs

- 5.1.1.1 Cardiac Chairs

- 5.1.1.2 Birthing Chairs

- 5.1.1.3 Blood Drawing Chairs

- 5.1.1.4 Dialysis Chairs

- 5.1.1.5 Others

- 5.1.2 Treatment Chairs

- 5.1.2.1 ENT Chairs

- 5.1.2.2 Ophthalmic Chairs

- 5.1.2.3 Dental Chairs

- 5.1.2.4 Other Treatment Chairs

- 5.1.3 Rehabilitation Chairs

- 5.1.3.1 Geriatric Chairs

- 5.1.3.2 Pediatric Chairs

- 5.1.3.3 Bariatric Chairs

- 5.1.3.4 Others

- 5.1.1 Examination Chairs

- 5.2 By Technology

- 5.2.1 Manual

- 5.2.2 Semi-Electric / Hydraulic

- 5.2.3 Fully-Electric / Programmable

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Clinics & Dental Practices

- 5.3.3 Ambulatory Surgery Centers

- 5.3.4 Home-Care Settings & Long-Term Care

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Dentsply Sirona

- 6.3.2 A-dec Inc.

- 6.3.3 PLANMECA OY

- 6.3.4 Midmark Corporation

- 6.3.5 ATMOS MedizinTechnik GmbH & Co. KG

- 6.3.6 G. Heinemann Medizintechnik GmbH

- 6.3.7 DentalEZ

- 6.3.8 Hill Laboratories Company

- 6.3.9 Topcon Medical Systems Inc.

- 6.3.10 Forest Dental

- 6.3.11 Fresenius Medical Care AG & Co. KGaA

- 6.3.12 Champion Manufacturing Inc.

- 6.3.13 Invacare Corporation

- 6.3.14 Stryker Corporation

- 6.3.15 Danaher Corporation (Kavo Dental)

- 6.3.16 Hill-Rom Holdings Inc.

- 6.3.17 Digiterm Ltd.

- 6.3.18 Drive DeVilbiss Healthcare

- 6.3.19 Likamed GmbH

- 6.3.20 Accora Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment