|

시장보고서

상품코드

1940601

약물 용출 스텐트(DES) : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Drug Eluting Stent - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

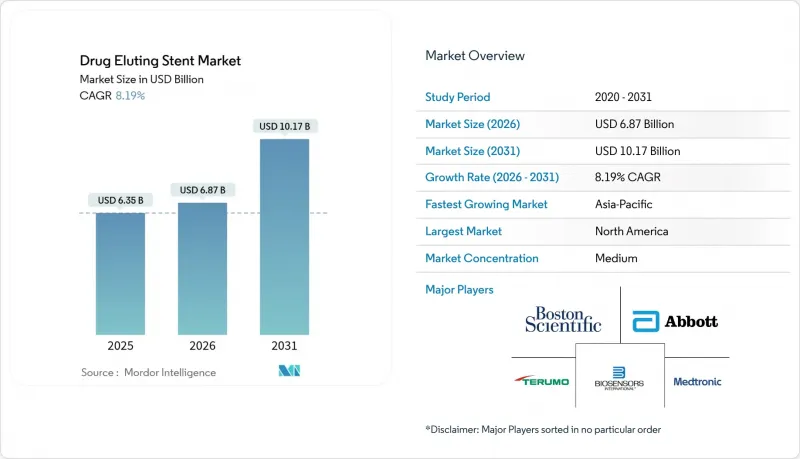

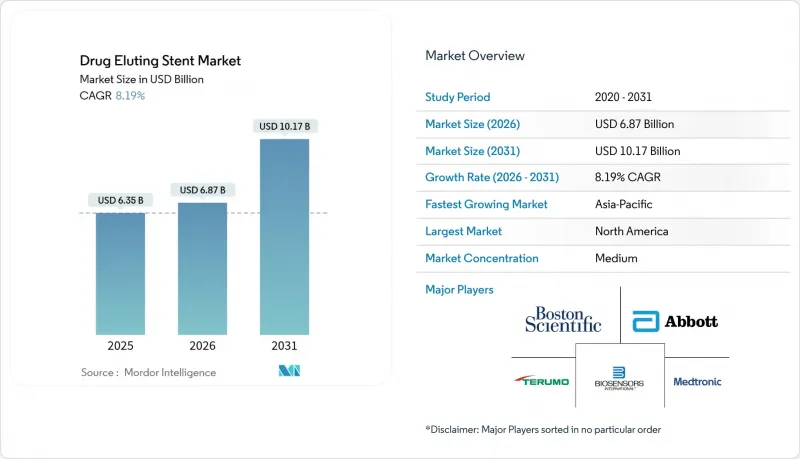

약물 용출 스텐트(DES) 시장은 2025년에 63억 5,000만 달러로 평가되었고, 2026년 68억 7,000만 달러에서 2031년까지 101억 7,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 8.19%로 예상됩니다.

저침습적 관상동맥 및 말초혈관 치료 적응증 확대로 인해 단일 제품 수요가 증가하는 한편, 특히 생체적합성 코팅이 적용된 미세 직경의 스트럿 설계 등 장치의 급속한 진화가 장기 재협착률 감소를 지속적으로 촉진하여 병원의 조달처를 새로운 플랫폼으로 전환하고 있습니다. 동시에 고령화로 인해 복잡한 케이스가 증가하고, 의료 시스템은 스텐트 고도화에 발맞추어 영상진단 장비와 카테터 검사실 인프라를 업데이트해야 하는 상황에 직면해 있습니다. 신흥 경제국에서의 상환제도 개혁으로 고가 스텐트에 대한 접근성이 확대되면서 기존 기업과 비용 최적화를 위해 노력한 지역 공급업체 간의 경쟁이 심화되고 있습니다. 마지막으로, 공동구매 조직에 의한 가격 압력으로 인해 제조업체들은 하드웨어와 재고관리 서비스를 세트 판매하는 방향으로 방향을 틀어 단가가 하락하는 상황에서도 수익률을 유지하려고 노력하고 있습니다.

세계 약물 용출 스텐트(DES) 시장 동향 및 인사이트

심장 진료 대기 환자 해소에 따른 PCI 건수 급증

연기된 선택적 수술의 적체 해소로 인해 PCI 시술 건수는 팬데믹 이전 기준치를 크게 상회하고 있으며, 스텐트 구매자의 조달 일정을 재구성하고 있습니다. 당일 퇴원이 일상화되는 가운데, 케이스 스케줄은 기존 블록 예약에서 수요 주도형 슬롯 할당으로 전환되고 있으며, 이에 따라 유통업체는 잘 팔리는 SKU의 재고를 늘리고 잘 팔리지 않는 품목의 비중을 낮추고 있습니다. 요골동맥 접근 훈련에 일찍이 투자한 통합 의료 네트워크는 분산형 의료 그룹보다 몇 퍼센트 더 높은 시술 성장률을 기록하여 기술 습득이 기기 수요를 어떻게 증폭시킬 수 있는지를 보여주고 있습니다. 업계 분석가들은 현재 외래환자 전환을 단순한 비용 절감 수단이 아닌 볼륨 창출 엔진으로 인식하고 있습니다. 시설 사용료의 감소는 경계선상의 적응증에 대한 PCI 시행을 승인할 의향이 있는 지불자 층을 넓혀주기 때문입니다.

2세대 및 3세대 약물 용출 스텐트(DES)로의 선호도 변화

여러 세대의 디바이스를 비교한 임상 결과 데이터는 생분해성 또는 폴리머 프리 코팅으로 인해 안전성이 눈에 띄게 향상되었으며, 이는 시장을 차세대 플랫폼으로 전환하는 촉매제 역할을 하고 있습니다. 병원의 약제 및 치료위원회는 이중항혈소판요법(DAPT) 기간 단축에 대한 근거를 약제 채택의 조건으로 삼는 경향이 강해지고 있습니다. DAPT 기간 단축은 출혈 관련 재입원을 줄여 포괄수가제 수익률을 저해하는 요인을 감소시키기 때문입니다. 이에 따라 2세대 DES는 이미 약 70%의 점유율을 차지하고 있으며, 3세대 솔루션은 약 12%의 연평균 복합 성장률(CAGR)로 확대되고 있습니다. 전략적으로 카테터실 관리자는 저장 공간을 재조정하고 수요가 적은 1세대 SKU를 단계적으로 폐지하여 급성기 치료용 플랫폼의 재고 자본을 확보하고 있습니다. 실제로는 3차 의료기관이 두 단계의 처방집을 운영한다는 것을 의미합니다. 즉, 표준적인 케이스에는 가치 중심의 장치를, 복잡한 해부학적 구조에는 프리미엄 스텐트를 적용하고, 획일적인 표준화를 하지 않는다는 것입니다.

스텐트 후 혈전증에 대한 안전성 우려

여러 세대에 걸친 설계의 발전에도 불구하고, 특히 1세대 내구성 폴리머 장치의 경우, 후기 스텐트 혈전증은 여전히 임상적으로 우려되는 문제입니다. 규제 당국은 신규 플랫폼에 대해 더 긴 추적 기간을 요구하고 있으며, 이로 인해 개발 주기가 길어지고 중소 혁신 기업의 자본 요구 사항이 증가하고 있습니다. 임상적으로, 지속적인 내피화에 대한 관심은 혈관 내 이미징의 광범위한 채택을 촉진하고 있습니다. 광간섭단층촬영기(OCT)의 사용은 3차 의료기관에서 눈에 띄게 증가하여 스트럿 피복의 정밀한 평가를 촉진하고 있습니다. 흥미롭게도, OCT 사용 증가는 재료 선택에도 영향을 미치고 있으며, 영상진단을 많이 사용하는 워크플로우와 잘 어울리기 때문에 더 높은 방사선 불투과성을 가진 스텐트가 선호되고 있습니다. 그 결과, 가시성이 조금만 개선되어도 가동률이 높은 의료기관에서 불균형적으로 점유율을 확대할 수 있습니다.

부문 분석

2025년 현재, 폴리머 기반 코팅이 세계 점유율의 약 78.65%를 차지하고 있지만, 내부 판매 대시보드에 따르면 생체 흡수성 층의 성장이 꾸준히 확대되고 있는 것으로 나타났습니다. 의료진은 약물 방출 종료 후 사라지는 폴리머의 임상적 편의성을 강조하며, 이를 통해 기존 화학물질에 오랫동안 수반되었던 염증성 후유증을 완화할 수 있다고 주장하고 있습니다.

선견지명이 있는 제조업체들은 기존의 솔벤트 기반 코팅 라인을 보다 얇고 균일한 층을 형성할 수 있는 차세대 스프레이 드롭렛 시스템으로 전환하기 시작했습니다. 생산 기술자에 따르면, 이러한 업그레이드 라인은 환자 이익 외에도 생산성 향상과 용제 사용량 감소를 실현하여 점진적인 연구 개발 비용을 상쇄하는 비용 효율화를 촉진하고 있다고 합니다.

에베로리무스 용출 스텐트는 2025년 세계 출하량의 약 37.60%를 차지할 것으로 예상되며, 가장 빠르게 성장하는 하위 부문은 바이오리무스 계열 디바이스로 CAGR 약 12.75%를 나타낼 것으로 예측됩니다. 현재 약동학 연구는 조직 노출 기간을 최대 9개월까지 연장하는 결정 구조에 초점을 맞추고 있으며, 이를 통해 전신 이중 항혈소판요법(DAPT)의 기간을 단축할 수 있습니다.

출혈 위험이 높은 환자가 많은 의료기관에서는 이러한 고기능 모델을 구매함으로써 직접적인 경제적 가치를 인식하고 있습니다. 출혈 관련 재입원을 줄임으로써 포괄수가제에서 수익률을 유지할 수 있기 때문입니다. 이에 따라 약제-치료위원회(P&T위원회)에서는 입찰 평가에서 스텐트 관련 항응고제 비용 절감 효과를 정량화하려는 움직임이 시작되고 있습니다. 이는 미묘하지만 영향력 있는 평가 프레임워크의 변화라고 할 수 있습니다.

2025년에는 코발트 크롬 합금이 약 46.55%의 점유율로 1위를 유지할 것으로 예상되지만, 백금 크롬 합금이 가장 빠르게 성장하여 연평균 약 11.08%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예측됩니다. 백금 크롬 합금의 방사선 불투과성 향상은 조영제 사용량 감소로 이어지며, 많은 PCI 환자가 신장 질환을 동반하고 있다는 점을 고려할 때 신장 전문의에게는 환영할 만한 특성입니다.

디바이스 엔지니어들은 합금의 강도를 활용하여 스트럿의 두께를 줄임으로써 방사형 방향의 성능 저하 없이 전달성을 향상시켰습니다. 이러한 설계를 통해 통과 프로파일을 최소화함으로써 기존에는 도달할 수 없었던 병변에 접근이 가능해져 저침습적 재관류 치료의 잠재적 시장이 확대되고 있습니다. 그 결과, 병원의 서비스 라인 책임자는 기존에 수술이 필요했던 사례를 카테터 치료로 전환함으로써 매출 증가를 예상하고 있으며, 합금의 상업적 매력을 더욱 높이고 있습니다.

지역별 분석

북미는 2025년 기준 전 세계 DES 매출의 약 38.72%를 차지할 것으로 예측됩니다. 이 지역은 선진적인 상환제도, 방사선 불투과성 합금의 조기 도입, 말초혈관 적응증에 대한 신속한 승인 등의 이점을 가지고 있습니다. 특히 주목할 만한 점은 비응급 PCI의 50% 이상이 외래 진료 환경에서 이루어지고 있으며, 조달 일정이 재구성되고 있다는 점입니다. 외래수술센터(ASCs)는 조달 주기를 연간이 아닌 분기별로 설정하기 때문에 신속한 공급이 요구됩니다. 최근 미국 식품의약국(FDA)의 말초혈관용 약물용출형 스텐트 승인으로 이 분야 수요층이 추가되어 전체 시술 기반을 확대할 수 있게 되었습니다.

아시아태평양은 가장 빠르게 성장하는 시장으로 2031년까지 약 10.55%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 중국 및 인도 국내 기업들은 비용 최적화 설계를 통해 수입품보다 낮은 가격을 실현하고 있지만, 다국적 기업들은 장기 데이터 패키지 및 의사 교육 제휴를 통해 고가 시장을 지키고 있습니다. 이 지역의 다양성이 두드러집니다. 일본은 포화상태의 보급률을 보이며 코팅 기술의 점진적 혁신에 집중하는 반면, 인도와 인도네시아는 베어 메탈 스텐트에서 DES로의 전환이 지속되고 있으며, 가격 중시층과 성능 중시층 모두를 지지하는 양극화된 시장을 형성하고 있습니다. 비동기식 지방 입찰 일정을 능숙하게 조정하는 제조업체는 지속적인 생산라인을 유지하고, 공장 가동률 향상으로 비용 효율화를 실현하고 있습니다.

유럽의 혼합 조달 모델은 중앙집권적 국가 입찰과 병원 수준의 자율성을 결합하여 30개 이상의 DES 브랜드가 처방전 목록에 등재되기 위해 경쟁하는 독특한 경쟁 환경을 조성하고 있습니다. 이 지역의 임상 학회는 전 세계 동료들보다 앞서서 진료 관행을 변화시키는 증거를 발표하는 경우가 많으며, 이는 허용 가능한 안전 마진에 대한 인식에 영향을 미치고 있습니다. 최근 10년간의 다기관 임상시험 결과 데이터에 따르면, 다양한 고분자 전략 간 장기 주요 심혈관 부작용에 유의미한 차이가 나타나지 않아, 지불기관은 코팅의 화학적 특성뿐만 아니라 비용과 전달성(삽입 기술)을 중요하게 고려하는 경향이 강화되고 있습니다. 이러한 환경은 가격 압축을 가속화하는 한편, 디바이스 제조업체들이 심각한 석회화 환경 하에서의 전달성 등 플랫폼의 범용성 향상에 투자하여 상품화의 함정을 피하도록 유도하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.10The drug eluting stent (DES) market was valued at USD 6.35 billion in 2025 and estimated to grow from USD 6.87 billion in 2026 to reach USD 10.17 billion by 2031, at a CAGR of 8.19% during the forecast period (2026-2031).

Widening indications for minimally invasive coronary and peripheral procedures are elevating unit demand, while rapid device iteration, particularly thinner strut designs with biocompatible coatings, continues to decrease long-term restenosis and drive hospital purchasing preference toward newer platforms. At the same time, an aging population is expanding the pool of complex cases, prompting health systems to refresh imaging and cath-lab infrastructure in lock-step with stent upgrades. Reimbursement reforms in several emerging economies are broadening access to premium stents, intensifying competition between incumbents and cost-optimized regional suppliers. Finally, price pressure from group-purchasing organizations is nudging manufacturers to bundle inventory-management services with hardware, helping to defend margins even as unit prices edge lower.

Global Drug Eluting Stent Market Trends and Insights

Accelerated PCI Volumes After Cardiac Care Backlog Clearance

Clearing the backlog of deferred elective procedures has lifted PCI throughput well above pre-pandemic baselines, reshaping procurement calendars for stent buyers. As same-day discharge becomes routine, case scheduling is moving from legacy block booking toward demand-driven slotting, which in turn prompts distributors to stock faster-moving SKUs and down-weight slow sellers. Integrated delivery networks that invested early in radial-access training recorded procedure growth that was several percentage points above fragmented provider groups, illustrating how skills acquisition magnifies device pull-through. Industry analysts now view outpatient migration not simply as a cost-containment lever but as a volume-creation engine, because lower facility fees broaden the pool of payers willing to authorize PCI for borderline indications.

Preference Shift to Second- & Third-Generation Drug Eluting Stents (DES)

Clinical-outcome data comparing device generations show conspicuous safety gains with biodegradable or polymer-free coatings, catalyzing a market pivot toward newer platforms. Hospital pharmacy & therapeutics committees increasingly condition formulary approval on evidence of reduced dual-antiplatelet therapy (DAPT) duration, because shorter DAPT lowers bleeding-related readmissions that erode bundled-payment margins. Accordingly, second-generation DES already hold about 70 % share, whereas third-generation solutions are expanding at nearly 12 % CAGR. Tactically, cath-lab managers are rebalancing shelf space: low-traffic first-generation SKUs are being phased out, freeing inventory capital for high-acuity platforms. In practice, this means that tertiary centers run two-tier formularies, value-oriented devices for routine cases and premium stents for complex anatomies, rather than one-size standardization.

Safety Concerns Around Late-Stent Thrombosis

Despite generational design progress, late-stent thrombosis remains a clinical concern, especially for first-generation durable-polymer devices. Regulatory agencies mandate longer follow-up periods for novel platforms, extending development cycles and increasing capitalization requirements for smaller innovators. Clinically, the focus on durable endothelialization is encouraging broader adoption of intravascular imaging. Use of optical coherence tomography (OCT) has grown noticeably in tertiary centers, fostering precise assessments of strut coverage. Interestingly, rising OCT utilization is also shaping material selection: stents offering higher radiopacity gain favor because they pair better with imaging-intensive workflows. Consequently, even marginal improvements in visibility can translate into disproportionate share gains in high-volume centers.

Other drivers and restraints analyzed in the detailed report include:

- National Reimbursement Expansion for DES

- Rapidly-Ageing Global Population

- Margin Compression from Group Purchasing Organizations (GPOs)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polymer-based coatings currently hold roughly 78.65% of global share in 2025, yet internal sales dashboards show that bioresorbable layers are capturing a steadily larger growth. Operators emphasize the clinical comfort of a polymer that vanishes once drug delivery ends, which, they argue, mitigates inflammatory sequelae long associated with durable chemistries.

Forward-looking manufacturers have begun converting traditional solvent-based coating lines to next-generation spray-droplet systems compatible with thinner, uniform layers. Production engineers note that apart from patient benefits, these upgraded lines yield higher throughput and lower solvent use, driving a cost-efficiency agenda that often offsets incremental R&D outlays.

Everolimus-eluting stents control about 37.60% of global unit shipments in 2025, but the fastest ascendant subsegment is biolimus-based devices at roughly 12.75% CAGR. Pharmacokinetic research now centers on crystalline structures that prolong tissue exposure out to nine months, thereby facilitating shorter systemic DAPT.

Hospitals with a high case mix of bleeding-risk patients perceive direct economic value in buying these premium models because reducing bleed-related readmissions preserves bundled-payment margins. As a corollary, P&T committees have begun quantifying stent-related anticoagulant cost offsets when weighing tender responses-a subtle yet influential shift in value-assessment frameworks.

Cobalt-chromium alloys lead at around 46.55% share in 2025, but platinum-chromium is the fastest riser, expanding near 11.08% CAGR. Radiopacity gains with platinum-chromium translate into lower contrast volumes, which nephrologists welcome given the renal comorbidity profile of many PCI patients.

Device engineers further exploit alloy strength to trim strut thickness, improving deliverability without radial compromise. By minimizing crossing profiles, such designs unlock otherwise unreachable lesions, expanding the total addressable market for minimally invasive revascularization. Consequently, hospital service-line directors anticipate incremental revenue from converting previously surgical cases to cath-lab interventions, reinforcing the alloy's commercial appeal.

The Drug Eluting Stent Market is Segmented by Coating (Polymer Based Coating [Biodegradable and More] and More), Drug Type (Everolimus, and More), Material (Cobalt-Chromium, and More), Stent Generation (First Generation, and More), Deployment Technique (Self-Expandable, and More) Application (Coronary Artery Disease, and More), End-User (Hospitals, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commands about 38.72% of global DES revenue in 2025. The region benefits from advanced reimbursement mechanisms, early adoption of radiopaque alloys, and rapid peripheral indication approvals. Notably, more than 50% of non-urgent PCI now occurs in outpatient settings, reshaping procurement timeframes: ASCs schedule tender cycles quarterly rather than annually, demanding agile fulfillment. The U.S. Food and Drug Administration's recent nod to peripheral drug-eluting scaffolds adds another demand layer, expanding the region's total procedure base.

Asia-Pacific represents the fastest-growing market, forecast near 10.55% CAGR through 2031. Domestic players in China and India leverage cost-optimized engineering to undercut imports, yet multinationals defend premium tiers via long-term data packages and physician-training alliances. The region's heterogeneity is striking: Japan exhibits saturated penetration and focuses on incremental coating innovation, while India and Indonesia continue migrating from bare metal stents to DES, creating a bifurcated market that supports both price-sensitive and performance-oriented tiers. Manufacturers adept at navigating asynchronous provincial tender calendars maintain continuous production runs, enhancing factory utilization rates that translate into cost efficiencies.

Europe's blended procurement model, featuring centralized national tenders alongside hospital-level autonomy, produces a uniquely competitive environment where over 30 DES brands jostle for formulary inclusion. Clinical societies in the region often publish practice-changing evidence ahead of global counterparts, influencing perception of acceptable safety margins. Recent ten-year outcome data from multicenter trials revealed negligible differences in long-term major adverse cardiac events between various polymer strategies, encouraging payers to base purchasing decisions more on cost and deliverability than on coating chemistry alone. This environment accelerates price compression yet stimulates device makers to invest in platform versatility, such as deliverability in severe calcification, to escape the commodity trap.

- Abbott Laboratories

- Boston Scientific

- Medtronic

- Terumo

- BIOTRONIK

- Biosensors International Group, Ltd.

- MicroPort

- Cook Group

- Lepu Medical

- Meril Life Science

- Cordis

- Sahajanand Medical Technologies Ltd.

- OrbusNeich Medical Group

- Hexacath

- B. Braun

- SINOMED

- Alvimedica Medical Technologies Inc.

- Balton Sp. z o.o.

- Relisys Medical Devices Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapidly-Ageing Global Population

- 4.2.2 Accelerated PCI Volumes After Cardiac Care Backlog Clearance

- 4.2.3 Preference Shift to Second- & Third-Generation Drug Eluting Stents (DES)

- 4.2.4 National Reimbursement Expansion for DES

- 4.2.5 Domestic Manufacturing Incentives for DES

- 4.2.6 Hospital-Owned Cath-Lab Network Growth Across Global Countries

- 4.3 Market Restraints

- 4.3.1 Safety Concerns Around Late-Stent Thrombosis

- 4.3.2 Margin Compression from Group Purchasing Organisations (GPOs)

- 4.3.3 Scarcity of Interventional Cardiologists

- 4.3.4 Long Device Approval Timelines for New DES

- 4.4 Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Coating

- 5.1.1 Polymer-Based Coating

- 5.1.1.1 Biodegradable

- 5.1.1.2 Non-biodegradable

- 5.1.2 Polymer-Free Coating

- 5.1.1 Polymer-Based Coating

- 5.2 By Drug Type

- 5.2.1 Everolimus

- 5.2.2 Zotarolimus

- 5.2.3 Sirolimus

- 5.2.4 Paclitaxel

- 5.2.5 Biolimus

- 5.2.6 Others

- 5.3 By Material

- 5.3.1 Cobalt-Chromium

- 5.3.2 Platinum-Chromium

- 5.3.3 Stainless Steel

- 5.3.4 Nickel-Titanium (Nitinol)

- 5.3.5 Others

- 5.4 By Stent Generation

- 5.4.1 First Generation

- 5.4.2 Second Generation

- 5.4.3 Third Generation

- 5.5 By Deployment Technique

- 5.5.1 Balloon-Expandable

- 5.5.2 Self-Expandable

- 5.6 By Application

- 5.6.1 Coronary Artery Disease

- 5.6.2 Peripheral Artery Disease

- 5.7 By End-User

- 5.7.1 Hospitals

- 5.7.2 Cardiac Catheterization Labs

- 5.7.3 Ambulatory Surgical Centers

- 5.8 Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 Europe

- 5.8.2.1 Germany

- 5.8.2.2 United Kingdom

- 5.8.2.3 France

- 5.8.2.4 Italy

- 5.8.2.5 Spain

- 5.8.2.6 Rest of Europe

- 5.8.3 Asia-Pacific

- 5.8.3.1 China

- 5.8.3.2 Japan

- 5.8.3.3 India

- 5.8.3.4 Australia

- 5.8.3.5 South Korea

- 5.8.3.6 Rest of Asia-Pacific

- 5.8.4 Middle East and Africa

- 5.8.4.1 GCC

- 5.8.4.2 South Africa

- 5.8.4.3 Rest of Middle East and Africa

- 5.8.5 South America

- 5.8.5.1 Brazil

- 5.8.5.2 Argentina

- 5.8.5.3 Rest of South America

- 5.8.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Boston Scientific Corporation

- 6.3.3 Medtronic PLC

- 6.3.4 Terumo Corporation

- 6.3.5 Biotronik SE & Co. KG

- 6.3.6 Biosensors International Group, Ltd.

- 6.3.7 MicroPort Scientific Corporation

- 6.3.8 Cook Medical

- 6.3.9 Lepu Medical Technology Co., Ltd.

- 6.3.10 Meril Life Sciences Pvt. Ltd.

- 6.3.11 Cordis

- 6.3.12 Sahajanand Medical Technologies Ltd.

- 6.3.13 OrbusNeich Medical Group

- 6.3.14 Hexacath

- 6.3.15 B. Braun Melsungen AG

- 6.3.16 SINOMED

- 6.3.17 Alvimedica Medical Technologies Inc.

- 6.3.18 Balton Sp. z o.o.

- 6.3.19 Relisys Medical Devices Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment