|

시장보고서

상품코드

1842694

다관절 로봇 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Articulated Robot - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

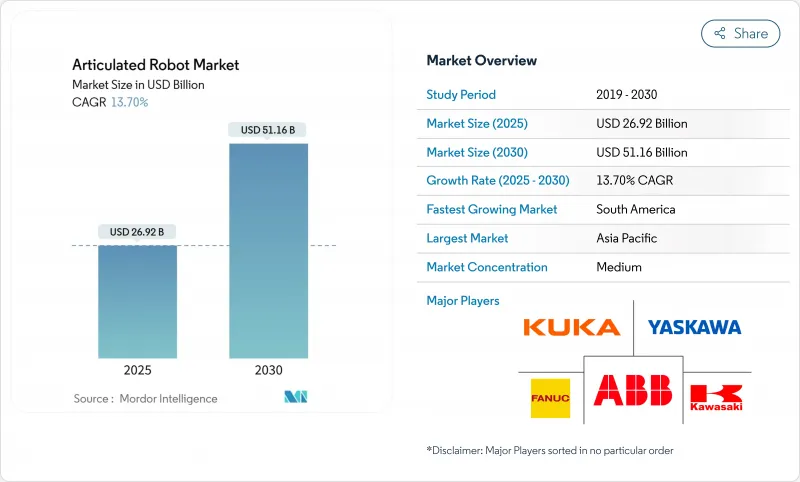

다관절 로봇 시장 규모는 2025년에 269억 2,000만 달러, 예측 기간(2025-2030년)의 CAGR은 13.70%를 나타내고, 2030년에는 511억 6,000만 달러에 달할 것으로 예측됩니다.

스마트 제조 솔루션, 주권 생산 정책, AI 대응 협조 시스템에 대한 수요의 급증이 이 확대를 뒷받침하고 있습니다. 전기자동차 생산의 설비투자 강화, 전자상거래 대기업의 지속적인 창고 자동화 전개, 정밀 지향 식품 용도의 확대가 기세를 더욱 강화하고 있습니다. 한편 부품 제조업체는 반도체 및 서보 모터의 병목에 수직 통합 전략으로 대응하고 에너지 효율적인 로봇 설계는 사용자가 운영 비용 절감을 추구하는 가운데 지지를 모으고 있습니다. 경쟁 전략은 이분화하고 있습니다. ABB와 같은 기존 기업은 구조적인 분사화를 추진해 집중력을 높이고, 신흥 기업은 클라우드 연결 플랫폼을 활용하여 배포 시간을 단축하고 있습니다.

세계의 다관절 로봇 시장 동향과 통찰

인더스트리 4.0 주도 자동화로 이동

제조업체는 다관절 로봇을 AI 분석 및 IoT 센서와 연동시켜 품질, 가동 시간 및 에너지 소비를 자체 최적화하는 폐루프 생산 생태계를 구축하고 있습니다. 폭스콘의 소등 사이트에서는 로봇 워크셀에 예측 유지보수 알고리즘을 통합하여 인원을 15만명 삭감하면서도 생산량을 유지하고 있습니다. 샤오미의 24시간 365일 운영 스마트폰 공장은 이러한 어두운 곳 공장 모델의 확장성을 입증합니다. 이러한 도입은 자동화의 경제성을 사람의 대안에서 제품 믹스의 민첩성으로 이동시켜 맞춤형 로트 및 변형의 도입을 위한 빠른 단계 교체를 가능하게 합니다.

인건비 상승과 숙련공 부족

시간당 1.60-2달러의 로봇의 운전 비용은 현재 많은 지역에서 5.50달러를 넘는 인간의 임금 미만으로 ROI 계산은 결정적으로 자동화에 기울고 있습니다. 제너럴 모터스와 존 디어사는 로봇 용접 셀을 채택한 후 용접 인건비를 50% 삭감하고 불량품을 25% 삭감했습니다. GXO 물류와 같은 창고업체는 안전 지표를 개선하면서 인력 갭을 메우기 위해 아폴로 휴머노이드에 눈을 돌리고 있습니다. 유럽과 동아시아의 인구동태의 고령화는 장기적으로 이 원동력이 됩니다.

높은 초기 도입 비용과 통합 비용

다관절 로봇 셀의 총 비용은 통합, 안전 장치, 훈련을 포함하면 두배로 증가할 수 있으며 중소기업의 의욕을 깎아냅니다. 라틴아메리카의 중소기업은 통합자와 금융 기관에 대한 접근이 제한되어 있음을 채택의 주요 장벽으로 꼽았습니다. Formic사는 99.8%의 가동률로 20만 시간의 계약 생산 시간을 보고하고 투자자의 사용량에 따른 자동화에 대한 의욕을 부각시켰습니다.

부문 분석

<=16kg 클래스는 전자, 제약, 협동 로봇의 도입을 배경으로 CAGR16.1%로 다른 것을 능가할 것으로 예측되는 한편, 16-60kg 부문은 2024년에 다관절 로봇 시장 점유율의 32.6%를 유지합니다. 사용자는 속도, 에너지 절약, 인간과 인접한 안전성을 위해 더 가벼운 플랫폼을 선호합니다. 프리덤 프레쉬 호주 마카다미아 라인은 경량의 스칼라 유닛으로 0.39초 사이클을 실현하여 식품 포장의 생산성 향상을 강조하고 있습니다.

60-225kg 및 225kg 이상의 로봇에 대한 수요는 자동차 바디샵이나 주조 작업에서는 안정적이지만, OEM이 설치 면적을 확대하는 것보다 설치 자산을 삭감하기 때문에 성장은 감속하고 있습니다. 고가반 질량의 암은 공기압의 에너지 사용량을 90% 삭감하는 형상 기억 합금의 그리퍼와의 통합이 진행되고 있습니다.

2025년부터 2030년까지 헤비 듀티 클래스의 다관절 로봇 시장 규모는 EV 배터리 팩 리프팅과 풍력 터빈 부품의 취급에 힘입어 1자리대로 확대될 것으로 예측되고 있습니다.

6축 모델은 2024년 수익의 51.8%를 차지했으며, 다관절 로봇 시장은 용접, 페인트, 정밀 조립의 근본적인 작업 호스로 정착되었습니다. 비용면에서는 5,000달러 이하의 소형기부터 50만 달러를 넘는 클린룸 대응기까지 다양한 유형이 등장하고 있습니다.

7축 및 초기용 형식은 가장 빠르게 성장하는 틈새 분야이며 16.5%의 연평균 복합 성장률(CAGR)을 기록하고 있습니다. 야마하의 YA 시리즈 엘보는 제한된 지그 주위를 회전하여 밀집된 생산 셀에서 택트 타임 단축을 가능하게 합니다. MDPI가 연구하는 병렬 토폴로지 로봇은 픽앤플레이스 사이클에서 더 높은 강성 대 중량비를 약속합니다.자동차 인테리어가 더욱 복잡해지고 가전제품도 소형화의 경향이 있기 때문에 좁은 범위를 이동하기 위한 추가 축 수요가 점점 높아질 것으로 보입니다.

다관절 로봇 시장은 가반 중량(16Kg까지, 16-60Kg, 기타), 축 유형(4축, 5축, 기타), 용도(자재관리, 용접·납땜, 조립, 도장·도포, 기타), 최종사용자 산업(자동차, 전기 및 전자, 금속 및 기계, 의약품 및 의료기기, 기타), 지역에 의해 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

아시아태평양이 2024년 매출 42.4%로 매출을 기록하며 지배력을 유지했습니다, 중국 규모와 일본의 혁신 생태계가 뒷받침. 지역정부는 중소기업 도입을 촉진하는 등대 프로젝트에 자금을 제공해 국내 임금 상승이 비용 우위성을 억제하는 가운데 다관절 로봇 시장 규모 확대를 안정시키고 있습니다. 일본의 로봇세액공제와 한국의 AI 바우처제도는 파이프라인 활동을 견고하게 유지합니다.

남미는 2030년까지 연평균 복합 성장률(CAGR) 15.3%로 가장 급성장할 것으로 예측되며 자동차의 전동화와 농업 자동화에 대한 해외 직접 투자가 그 밑바탕이 됩니다. 브라질의 농장 로봇 SOLIX는 AI 비전이 노지 작물 관리에 관절 설계를 확장하는 방법을 보여줍니다. 사례 IH의 2,000만 달러를 투입한 솔로카바의 업그레이드는 AI를 통합하여 90% 수확기 기능을 지휘하는 것으로, 이 지역의 첨단 로봇에 대한 의욕을 나타냈습니다.

북미에서는 2024년의 설치 대수가 전년대비 12% 증가한 4만 4,303대가 되어 연방 정부에 의한 리쇼어링 인센티브와 EV 서플라이 체인 프로젝트에 지지를 받았습니다. 야스카와 전기의 3,150만 유로를 투입한 슬로베니아의 허브는 2027년까지 EMEA의 로봇 납품의 80%를 현지 생산할 예정입니다. 중동 및 아프리카는 아직 개발도상이지만 건설과 석유화학제품의 유지보수로 파일럿 사업을 유치하여 장기적인 다관절 로봇 시장 도입의 기초를 쌓았습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- Industry 4.0 주도의 자동화로의 전환

- 인건비 상승과 숙련노동자 부족

- 스마트 제조에 대한 정부의 인센티브

- 자동차 e-모빌리티의 설비투자 붐

- AI 대응 적응형 다관절 코봇

- E-Commerce 대기업에 의한 풀필먼트 센터의 자동화

- 시장 성장 억제요인

- 높은 선행 투자와 통합 비용

- 시스템 통합 인재 부족

- 커넥티드 로봇 컨트롤러의 사이버 보안 리스크

- 서보 모터와 반도체 공급의 병목 현상

- 산업 밸류체인 분석

- 규제 상황

- 기술적 전망

- 업계의 매력 - Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 거시경제 요인이 시장에 미치는 영향

제5장 시장 규모와 성장 예측(금액)

- 페이로드 용량별

- 16kg 미만

- 16-60 kg

- 60-225 kg

- 225kg 이상

- 축 유형별

- 4축

- 5축

- 6축

- 7축 이상

- 용도별

- 자재관리

- 용접과 납땜

- 조립

- 페인팅 및 디스펜싱

- 포장과 팔레타이징

- 검사 및 품질 보증

- 기타

- 최종 사용자 산업별

- 자동차

- 전기 및 전자

- 금속 및 기계

- 의약품 및 의료기기

- 식음료

- 전자상거래와 물류

- 기타 최종 사용자 산업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 싱가포르

- 말레이시아

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장의 집중

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- ABB Ltd.

- FANUC Corporation

- Yaskawa Electric Corp.

- KUKA AG

- Kawasaki Heavy Industries Ltd.

- Mitsubishi Electric Corp.

- Nachi-Fujikoshi Corp.

- DENSO Corp.

- Seiko Epson Corp.

- Staubli International AG

- 현대 Robotics Co., Ltd.

- Comau SpA

- Omron Adept Technology Inc.

- Universal Robots A/S

- Durr AG(Paint Robots)

- Estun Automation Co., Ltd.

- SIASUN Robot & Automation Co.

- JAKA Robotics Ltd.

- Techman Robot Inc.

- Precise Automation Inc.

- CMA Robotics SpA

- Gudel Group AG

- IAI Corporation

- Aubo Robotics Inc.

- Robot Industrial Association(RIA)

제7장 시장 기회와 앞으로의 동향

SHW 25.11.03The Articulated Robot Market size is estimated at USD 26.92 billion in 2025, and is expected to reach USD 51.16 billion by 2030, at a CAGR of 13.70% during the forecast period (2025-2030).

Surging demand for smart manufacturing solutions, sovereign production policies, and AI-enabled collaborative systems underpin this expansion. Intensifying capital expenditure in electric-vehicle production, sustained warehouse automation roll-outs by e-commerce majors, and growing precision-oriented food applications further reinforce momentum. Meanwhile, component makers are responding to semiconductor and servo-motor bottlenecks with vertical-integration strategies, and energy-efficient robotic designs are gaining traction as users chase lower operating costs. Competitive strategies are bifurcating: incumbents such as ABB pursue structural spin-offs to sharpen focus, while start-ups leverage cloud-connected platforms to shorten deployment times.

Global Articulated Robot Market Trends and Insights

Shift toward Industry 4.0-led automation

Manufacturers are linking articulated robots with AI analytics and IoT sensors to create closed-loop production ecosystems that self-optimise quality, uptime, and energy consumption. Foxconn's lights-off sites cut headcount by 150,000 yet sustained output by embedding predictive-maintenance algorithms in robotic workcells. Xiaomi's 24/7 smartphone facility demonstrates the scalability of such dark-factory models. These deployments shift automation economics from manpower substitution to product-mix agility, enabling rapid re-tooling for customised lots and variant introductions.

Rising labor cost and skilled-worker shortage

Robot operating costs of USD 1.60-2.00 per hour now undercut human wages exceeding USD 5.50 in many regions, tilting ROI calculations decisively toward automation. General Motors and John Deere trimmed welding labor expenses by 50% and defects by 25% after adopting robotic welding cells. Warehouse operators such as GXO Logistics have turned to Apollo humanoids to bridge head-count gaps while improving safety metrics. Ageing demographics in Europe and East Asia anchor this driver for the long term.

High upfront acquisition and integration cost

Total cost of an articulated robot cell can double once integration, safety equipment, and training are included, discouraging smaller enterprises. Latin American SMEs cite limited access to integrators and finance as key barriers to adoption. Robots-as-a-Service models mitigate this restraint by converting cap-ex into opex; Formic reported 200,000 contracted production hours at 99.8% uptime, highlighting investor appetite for pay-per-use automation.

Other drivers and restraints analyzed in the detailed report include:

- Government incentives for smart manufacturing

- Automotive e-mobility cap-ex boom

- Servo-motor and semiconductor supply bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The <= 16 kg class is projected to outpace all others at a 16.1% CAGR on the back of electronics, pharma, and collaborative deployments, whereas the 16-60 kg segment retained 32.6% of articulated robot market share in 2024. Users favour lighter platforms for speed, energy thrift, and human-adjacent safety. Freedom Fresh Australia's macadamia line runs 0.39-second cycles with a lightweight SCARA unit, underscoring productivity gains in food packing. Energy-efficiency pressures are driving material innovations: carbon-fibre arms from Cognibotics cut consumption by 90% while maintaining rigidity.

Demand for 60-225 kg and > 225 kg robots remains stable in automotive body-shop and foundry tasks, yet growth decelerates as OEMs sweat installed assets rather than expand footprint. High-payload arms increasingly integrate shape-memory alloy grippers that slash pneumatic energy use by 90%. Over 2025-2030, the articulated robot market size for heavy-duty classes is forecast to expand at single-digit rates, supported by EV battery pack lifting and wind-turbine component handling.

Six-axis models captured 51.8% of revenue in 2024, anchoring the articulated robot market as the de-facto workhorse for welding, painting and precision assembly. Cost points now span under USD 5,000 for light units to beyond USD 500,000 for clean-room variants. Modular controllers are shrinking installation footprints, a boon for SMEs with space constraints.

Seven-axis and hyper-dexterous formats are the fastest-rising niche, charting a 16.5% CAGR. Yamaha's YA series elbows rotate around confined fixtures, enabling shorter takt times in dense production cells. Parallel-topology robots studied by MDPI promise higher stiffness-to-weight ratios for pick-and-place cycles. As automotive interiors grow more complex and consumer electronics trend toward miniaturisation, demand for extra axes to navigate tight envelopes will intensify.

Articulated Robot Market is Segmented by Payload Capacity (Up To 16 Kg, 16 - 60 Kg, and More), Axis Type (4-Axis, 5-Axis, and More), Application (Material Handling, Welding and Soldering, Assembly, Painting and Dispensing, and More), End-User Industry (Automotive, Electrical and Electronics, Metals and Machinery, Pharmaceutical and Medical Devices, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained its dominance with 42.4% revenue in 2024, propelled by China's scale and Japan's innovation ecosystems. Regional governments fund lighthouse projects that accelerate SME uptake, stabilising articulated robot market size gains even as domestic wage growth tempers cost advantages. Japan's Robot Tax Credit and Korea's AI Voucher Scheme keep pipeline activity robust.

South America is forecast to grow the fastest at 15.3% CAGR through 2030, underwritten by foreign direct investments in automotive electrification and agri-automation. Brazil's SOLIX field robot shows how AI vision extends articulated design into open-field crop management. Case IH's USD 20 million Sorocaba upgrade embeds AI to command 90% harvester functions, demonstrating regional appetite for advanced robotics.

North America posted 12% year-on-year installation growth in 2024-totaling 44,303 units-supported by federal reshoring incentives and EV supply-chain projects. Europe faces energy-price headwinds yet invests in local capacity; Yaskawa's EUR 31.5 million Slovenian hub will localise 80% of EMEA robot deliveries by 2027. The Middle East and Africa remain nascent but attract pilots in construction and petrochemical maintenance, laying the groundwork for long-run articulated robot market adoption.

- ABB Ltd.

- FANUC Corporation

- Yaskawa Electric Corp.

- KUKA AG

- Kawasaki Heavy Industries Ltd.

- Mitsubishi Electric Corp.

- Nachi-Fujikoshi Corp.

- DENSO Corp.

- Seiko Epson Corp.

- Staubli International AG

- Hyundai Robotics Co., Ltd.

- Comau SpA

- Omron Adept Technology Inc.

- Universal Robots A/S

- Durr AG (Paint Robots)

- Estun Automation Co., Ltd.

- SIASUN Robot & Automation Co.

- JAKA Robotics Ltd.

- Techman Robot Inc.

- Precise Automation Inc.

- CMA Robotics SpA

- Gudel Group AG

- IAI Corporation

- Aubo Robotics Inc.

- Robot Industrial Association (RIA)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift toward Industry 4.0-led automation

- 4.2.2 Rising labor cost and skilled-worker shortage

- 4.2.3 Government incentives for smart manufacturing

- 4.2.4 Automotive e-mobility cap-ex boom

- 4.2.5 AI-enabled adaptive articulated cobots

- 4.2.6 Fulfilment-center automation by e-commerce majors

- 4.3 Market Restraints

- 4.3.1 High upfront acquisition and integration cost

- 4.3.2 Scarcity of system-integration talent

- 4.3.3 Cyber-security risk in connected robot controllers

- 4.3.4 Servo-motor and semiconductor supply bottlenecks

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Payload Capacity

- 5.1.1 Up to 16 kg

- 5.1.2 16 - 60 kg

- 5.1.3 60 - 225 kg

- 5.1.4 Above 225 kg

- 5.2 By Axis Type

- 5.2.1 4-Axis

- 5.2.2 5-Axis

- 5.2.3 6-Axis

- 5.2.4 7-Axis and Above

- 5.3 By Application

- 5.3.1 Material Handling

- 5.3.2 Welding and Soldering

- 5.3.3 Assembly

- 5.3.4 Painting and Dispensing

- 5.3.5 Packaging and Palletizing

- 5.3.6 Inspection and Quality Assurance

- 5.3.7 Others

- 5.4 By End-user Industry

- 5.4.1 Automotive

- 5.4.2 Electrical and Electronics

- 5.4.3 Metals and Machinery

- 5.4.4 Pharmaceutical and Medical Devices

- 5.4.5 Food and Beverages

- 5.4.6 E-commerce and Logistics

- 5.4.7 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Singapore

- 5.5.4.6 Malaysia

- 5.5.4.7 Australia

- 5.5.4.8 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 FANUC Corporation

- 6.4.3 Yaskawa Electric Corp.

- 6.4.4 KUKA AG

- 6.4.5 Kawasaki Heavy Industries Ltd.

- 6.4.6 Mitsubishi Electric Corp.

- 6.4.7 Nachi-Fujikoshi Corp.

- 6.4.8 DENSO Corp.

- 6.4.9 Seiko Epson Corp.

- 6.4.10 Staubli International AG

- 6.4.11 Hyundai Robotics Co., Ltd.

- 6.4.12 Comau SpA

- 6.4.13 Omron Adept Technology Inc.

- 6.4.14 Universal Robots A/S

- 6.4.15 Durr AG (Paint Robots)

- 6.4.16 Estun Automation Co., Ltd.

- 6.4.17 SIASUN Robot & Automation Co.

- 6.4.18 JAKA Robotics Ltd.

- 6.4.19 Techman Robot Inc.

- 6.4.20 Precise Automation Inc.

- 6.4.21 CMA Robotics SpA

- 6.4.22 Gudel Group AG

- 6.4.23 IAI Corporation

- 6.4.24 Aubo Robotics Inc.

- 6.4.25 Robot Industrial Association (RIA)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-Space and Unmet-Need Assessment