|

시장보고서

상품코드

1842706

소아용 휠체어 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Pediatric Wheelchairs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

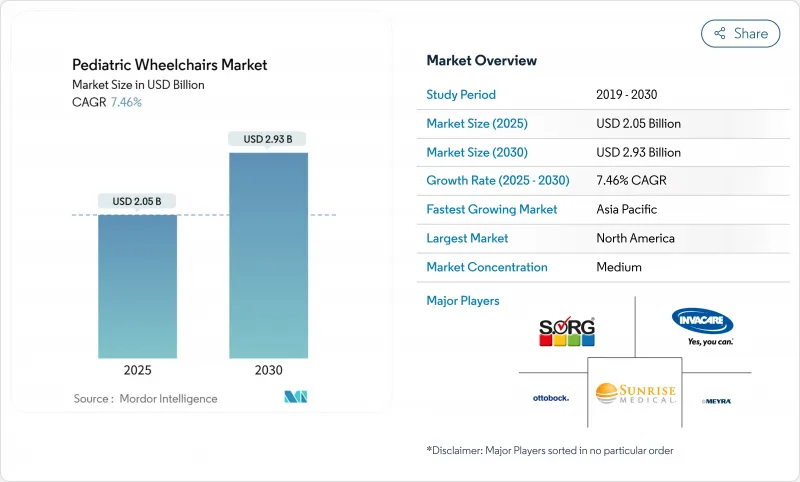

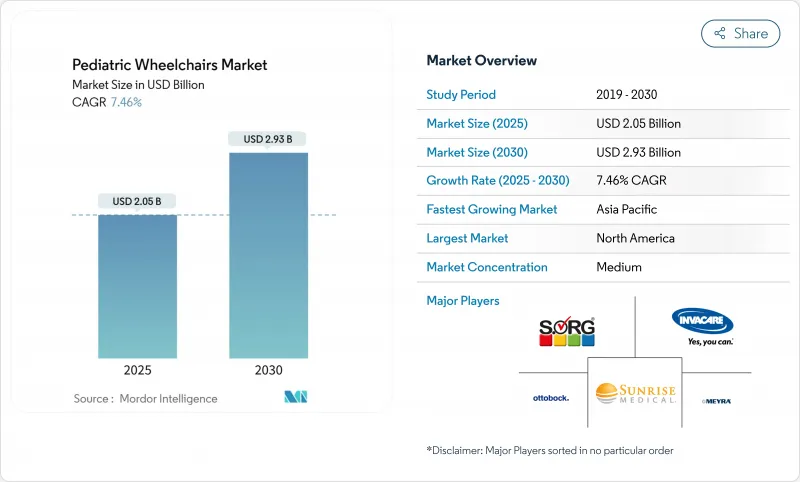

소아용 휠체어 시장 규모는 2025년에 20억 5,000만 달러, 예측기간(2025-2030년)의 CAGR은 7.46%를 나타내고, 2030년에는 29억 3,000만 달러에 달할 것으로 예측됩니다.

이동과 관련된 장애의 신속한 식별, 미숙아 및 의료적으로 복잡한 유아의 생존 기간 연장, 재택 관리로의 명확한 변화가 소아용 휠체어 시장을 확대하고 있습니다. 공급업체는 첨단 소재, 디지털 연결성, 성장에 대응하는 모듈 설계에 의해 차별화를 도모하고 있으며, 고소득국가의 지불자는 커스텀 기기에 대한 상환을 계속 확대하고 있습니다. 온라인 설정 플랫폼은 리드 타임을 단축하고 3D 프린터를 사용한 시트는 제조 비용을 증가시키지 않고 임상의가 개별 해부학적 요구를 충족시키는 데 도움이 됩니다. 그러나 지속적인 반도체 부족과 희토류 의존은 전동 휠체어 제조업체를 공급 변동에 노출시켜 니어 쇼어링 및 듀얼 소싱 전략을 장려하고 있습니다.

세계 소아용 휠체어 시장 동향과 통찰

소아장애 발생률 상승

신생아 의료의 개발로 더 많은 초미숙아가 생존할 수 있게 되었으나, 그 중 상당수가 뇌성 마비와 신경근 질환을 발병하여 장기적인 이동 보조를 필요로 하고 있습니다. 현재는 정기적인 유아 건강 진단으로 조기 진단을 실시하기 때문에 임상의는 휠체어를 더 빨리 처방하고 사용 수명을 늘릴 수 있습니다. 소아용 휠체어는 성장에 따라 여러 번 교체가 필요하기 때문에 이 인구 동향은 소아용 휠체어 시장을 확대합니다. 미국 아카데미는 적시 지원 기술이 활동 참여와 후속 고용 전망을 향상시킬 것이라고 강조합니다.

지원기술에 대한 정부의 자금 지원 프로그램

장애인 교육법(Individuals with Disabilities Education Act)과 같은 연방 정부의 의무는 자격을 갖춘 자녀가 개별 교육 프로그램에 명시되어 있는 경우 이동 기구를 무료로 받을 수 있도록 합니다. 2024년 504조의 갱신으로 제공업체의 의무가 명확해졌으며, 메디케이드, 학교구, 비영리 대금업자에 대한 보상이 강화되었습니다. 48개 주 지원기술 프로그램은 저금리 대출과 장비 교환을 제공하여 소비자의 자기 부담액을 낮추고 있습니다. 자금 제공의 확대는 보다 높은 사양의 모델의 채택을 촉진하고 소아용 휠체어 시장을 더욱 활성화시킵니다.

신흥 시장에서 높은 가격과 제한된 보험

많은 저소득 국가에서 소아용 휠체어는월소득의 중앙값의 3배에서 5배나 많기 때문에 가족은 현지의 저기능 대체품을 선택하게 됩니다. 장애인 지원이 국가의 의료보험제도에 내장되어 있지 않은 국가에서는 보험격차가 존재하고, 고가의 기기의 이용이 제한되어, 소아용 휠체어 시장의 성장 궤도를 억제하고 있습니다. 자금원이 세분화됨에 따라 가족은 여러 기관에 걸쳐 복잡한 신청 절차를 수행해야 하며, 이는 지연 및 관리 부담이 되어 이동 수단에 적시에 액세스하지 못하게 합니다. 이러한 시장에서는 가격에 민감하기 때문에 고급 기능에는 부족한 것, 기본적인 이동 기능을 이용하기 쉬운 가격으로 제공하는 간소화된 현지 제조의 대체품에 대한 수요가 높아지고 있습니다.

부문 분석

수동 모델이 2024년 매출의 61.58%를 차지합니다. 합리적인 가격, 유지 보수의 용이성, 상체에 충분한 근력이있는 아이들에게 치료 운동을 제공할 수 있기 때문에 여전히 지지되고 있습니다. 이 부문의 설치 대수는 많아, 쿠션, 바퀴, 성장 키트의 애프터마켓도 안정되어 있습니다.

전동 휠체어는 CAGR 9.57%를 기록하여 심한 신경근력 제한이 있는 이용자에게 대응합니다. 최근 출시된 제품은 비례 조이스틱, 헤드 어레이, 쉽 & 퍼프 제어 등 미세한 운동 변화에 대응한 것입니다. 클라우드 텔레매틱스는 주행거리, 배터리의 건강 상태, 착석 각도를 기록하여 임상의가 원격 조작으로 파라미터를 조정하거나 예방 서비스를 스케줄할 수 있게 되었습니다. 2024년 스마트 드라이브의 스피드 다이얼 버그가 수정된 후 OEM은 소프트웨어 검증을 강화하고 중복 브레이크 회로를 도입하여 간병인의 신뢰성을 높였습니다.

컴팩트한 인산철 리튬 전지의 기술 혁신에 의해 경량화와 항속 거리의 연장이 실현되어, 지금까지 유모차에 의지하고 있던 취학 전 아동이 전동 의자를 이용할 수 있게 되었습니다. 예측 기간 동안 전동 모델의 소아용 휠체어 시장 규모는 다른 카테고리보다 빠르게 확대될 것으로 예상되지만 일부 지역에서는 상환 장애물이 보급을 억제할 수 있습니다.

접이식 프레임은 일상적인 휴대성으로 2024년 매출의 49.29%를 차지합니다. 업데이트된 퀵 릴리스 크로스 브레이스는 접이식 깊이를 줄여 가족이 작은 세단에 의자를 수납할 수 있도록 했습니다. 선택적 원핸드 폴드 래치는 여러 어린이를 관리하는 간병인을 지원합니다.

틸트 인 스페이스 시스템은 욕창과 호흡 곤란의 위험이있는 어린이에게 처방되며 연간 9.09%의 성장을 나타냅니다. 임상의는 45도 후경과 20도 전경을 평가하여 섭식과 이상을 촉진합니다. 전자 액추에이터가 일반적인 자세를 기억하기 때문에 교사는 수동 없이 하루 종일 자세를 바꿀 수 있습니다. 가격이 높음에도 불구하고 입원 감소에 대한 임상 증명은 지불자를 납득시키고 있습니다. 그 결과, 틸트 인 스페이스의 소아용 휠체어 시장 점유율은 2030년까지 꾸준히 확대될 것으로 예측됩니다.

지역별 분석

2024년 매출은 북미가 39.41%의 매출을 기록하며 선두를 차지했습니다. 메디케이드의 조기 및 정기 검진, 진단 및 치료 조항, 개인 지급자 평가법에 따른 광범위한 보험 적용 범위는 높은 보급률을 유지합니다. ADA의 준수에 의해 학교나 공원에서는 이동용 리프트나 배리어 프리 놀이기구와 일체화한 의자의 구입이 진행되고 있습니다. 그러나 공급망의 스트레스는 배터리와 반도체의 가격을 상승시키고 공급자를 현지 조달로 향하게 합니다.

아시아태평양의 CAGR은 가장 빠른 12.06%로 중국, 일본, 호주 등 국가에서 국민 모두 보험 제도의 전개와 적극적인 장애인 수용 정책이 뒷받침되고 있습니다. 국가 보조금과 세액 공제로 중소득 가구가 전동 모델을 구입할 수 있게 되었고, 도시 지역의 소아용 휠체어 시장이 확대되었습니다. 말레이시아와 베트남의 조립 공장을 포함한 현지화 전략은 관세 부담을 줄이고 현지 조달 규칙을 충족함으로써 국내 판매를 촉진하고 있습니다.

유럽은 한 자릿수 초반의 꾸준한 성장세를 보이고 있습니다. 사회 보험은 고비용 틸트 인 스페이스 시스템을 다루고 있지만 일부 회원국에서는 긴축 재정이 보험료 업그레이드를 억제하고 있습니다. EU 의료기기 규제의 지속적인 개선으로 컴플라이언스 비용은 계속 증가하고 있지만 엄격한 시판 후 조사로 사용자도 보호하고 있습니다. 남미와 중동 및 아프리카는 인도 지원단체와 신흥의 원격 재활 프로그램이 향후 성장을 위한 토대를 구축하고 있지만 아직 충분히 침투하고 있지 않습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 도입

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 소아장애 발생률 증가

- 지원기술에 대한 정부의 자금 지원 프로그램

- 경량화와 파워 어시스트 시스템의 기술 진보

- 헬스케어 지출 증가와 재택 케어의 보급

- 교체 수요를 가속시키는 3D 인쇄 커스텀 시트

- 현장 이동 장치를 요구하는 포괄적 학교 의무 사항

- 시장 성장 억제요인

- 신흥 시장에서의 고가격과 한정된 보험

- 복잡한 병원 조달 규제

- 급속한 아이의 성장에 의한 제품 라이프 사이클의 단기화

- 동력 모델의 희토류 모터 공급 변동성

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측(단위 : 달러)

- 제품 유형별

- 수동식

- 전동

- 프레임 유형별

- 리지드

- 접이식

- 틸트 인 스페이스

- 최종 사용자별

- 병원

- 재택 간병

- 재활센터

- 기타 최종 사용자

- 유통 채널별

- 오프라인

- 온라인

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Sunrise Medical

- Invacare

- Permobil

- Ottobock

- MEYRA GmbH

- Ki Mobility

- Leckey

- Drive DeVilbiss Healthcare

- R82(Etac)

- SORG Rollstuhltechnik GmbH

- AKCES-MED sp. z oo

- Medline Industries

- VELA Medical

- Smirthwaite

- Motion Composites

- Panthera

- Karma Medical

- Nissin Medical

- Karma Mobility

- Momentum Healthcare

제7장 시장 기회와 전망

SHW 25.11.03The Pediatric Wheelchairs Market size is estimated at USD 2.05 billion in 2025, and is expected to reach USD 2.93 billion by 2030, at a CAGR of 7.46% during the forecast period (2025-2030).

Rapid identification of mobility-related disabilities, longer survival of premature and medically complex infants, and a clear shift toward home-based care are expanding the pediatric wheelchairs market. Suppliers are differentiating through advanced materials, digital connectivity, and modular designs that accommodate growth, while payers in high-income countries continue to widen reimbursement for custom devices. Online configuration platforms shorten lead-times, and 3D-printed seating helps clinicians meet individual anatomical needs without raising production costs. Persistent semiconductor shortages and rare-earth dependence, however, expose powered chair makers to supply volatility, prompting near-shoring and dual-sourcing strategies.

Global Pediatric Wheelchairs Market Trends and Insights

Rising Incidence of Pediatric Disabilities

Improved neonatal care is enabling more extremely premature infants to survive, yet many develop cerebral palsy or neuromuscular conditions that require long-term mobility assistance. Earlier diagnosis now occurs during routine well-baby visits, allowing clinicians to prescribe wheelchairs sooner and extend total years of use. This demographic trend enlarges the pediatric wheelchairs market because multiple chair replacements are required as children grow. The National Academies underline that timely assistive technology improves activity participation and later employment prospects.

Government Funding Programs for Assistive Technologies

Federal mandates such as the Individuals with Disabilities Education Act ensure that qualified children receive mobility devices at no cost when listed in their Individualized Education Program. The 2024 update to Section 504 clarified provider obligations, strengthening coverage across Medicaid, school districts, and nonprofit lenders. Forty-eight state assistive-technology programs additionally supply low-interest loans or equipment exchanges, lowering consumer out-of-pocket expenses. Expanded funding encourages adoption of higher-specification models, further stimulating the pediatric wheelchairs market.

High Price & Limited Insurance in Emerging Markets

A pediatric wheelchair can cost three to five times median monthly income in many lower-income countries, pushing families toward local, low-feature alternatives. Insurance gaps persist where disability support is not embedded in national health plans, limiting uptake of premium devices and tempering the pediatric wheelchairs market trajectory. The fragmented nature of funding sources requires families to navigate complex application processes across multiple agencies, creating delays and administrative burdens that can prevent timely access to mobility solutions. Price sensitivity in these markets has driven demand for simplified, locally-manufactured alternatives that may lack advanced features but provide basic mobility functionality at accessible price points.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advances in Lightweight & Power-Assist Systems

- Higher Healthcare Spending and Home-Based Care Adoption

- Complex Hospital Procurement Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manual models generated 61.58% of 2024 revenue. They remain favored for affordability, ease of maintenance, and the therapeutic exercise they provide to children with sufficient upper-body strength. The segment's large installed base sustains a steady aftermarket for cushions, wheels, and growth kits.

Powered wheelchairs, posting a 9.57% CAGR, address users with severe neuromuscular limitations. Recent releases offer proportional joystick, head-array, and sip-and-puff controls tailored to fine motor variability. Cloud telematics now logs mileage, battery health, and seating angles, allowing clinicians to adjust parameters remotely and schedule preventive service. After the 2024 correction of SmartDrive speed-dial faults, OEMs reinforced software validation and introduced redundant braking circuits, boosting caregiver confidence.

Innovation in compact lithium-iron-phosphate batteries cuts weight and extends range, making powered chairs viable for early-school children who previously relied on strollers. Over the forecast period, the pediatric wheelchairs market size for powered models is projected to compound faster than any other category, though reimbursement hurdles in some regions may temper penetration.

Foldable frames controlled 49.29% sales in 2024 due to everyday portability. Updated quick-release cross-braces trimmed folding depth, letting families stow chairs in small sedans. Optional one-hand fold latches support caregivers managing multiple children.

Tilt-in-space systems, growing 9.09% annually, are prescribed for children at risk of pressure ulcers or respiratory compromise. Clinicians value 45-degree posterior tilt and 20-degree anterior tilt to facilitate feeding and engagement. Electronic actuators memorize common positions, helping teachers shift posture throughout the school day without manual effort. Despite higher price, clinical proof of reduced hospitalization is convincing payers. Consequently, the pediatric wheelchairs market share for tilt-in-space is expected to widen steadily through 2030.

The Pediatric Wheelchairs Market Report Segments the Industry Into by Product Type (Manual and Powered), Frame Type (Rigid Foldable, and Tilt-In-Space), End User (Hospitals, Homecare Settings, Rehabilitation Centers, and Other End Users), Distribution Channel (Offline and Online), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 39.41% revenue in 2024. Broad insurance coverage under Medicaid Early and Periodic Screening, Diagnostic and Treatment provisions and private payer parity laws sustain high penetration. ADA compliance drives schools and parks to purchase chairs that integrate with transfer lifts and accessible playground structures. Supply chain stress, however, has raised battery and semiconductor prices, nudging providers toward local sourcing.

Asia-Pacific posts the fastest 12.06% CAGR, bolstered by universal health scheme rollouts and aggressive disability inclusion policy in countries such as China, Japan, and Australia. National subsidies and tax credits helped middle-income households afford powered models, enlarging the pediatric wheelchairs market in urban hubs. Localization strategies, including assembly plants in Malaysia and Vietnam, lower tariff exposure and meet local content rules, aiding domestic uptake.

Europe shows steady, low-single-digit expansion. Social insurance covers high-cost tilt-in-space systems, but austerity in certain member states restrains premium upgrades. Continuous improvement to EU Medical Device Regulation keeps compliance costs elevated, yet also protects users through strict post-market surveillance. South America and the Middle East & Africa remain underpenetrated, though humanitarian organizations and emerging tele-rehab programs are laying groundwork for future growth.

- Sunrise Medical

- Invacare

- Permobil

- Ottobock

- Meyra

- Ki Mobility

- Leckey

- Drive DeVilbiss Healthcare

- R82 (Etac)

- SORG Rollstuhltechnik

- AKCES-MED sp. z o.o.

- Medline Industries

- VELA Medical

- Smirthwaite

- Motion Composites

- Panthera

- Karma Medical

- Nissin Medical

- Karma Mobility

- Momentum Healthcare

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence of Pediatric Disabilities

- 4.2.2 Government Funding Programs for Assistive Technologies

- 4.2.3 Technological Advances in Lightweight & Power-Assist Systems

- 4.2.4 Higher Healthcare Spending and Home-Based Care Adoption

- 4.2.5 3d-Printed Custom Seating Accelerating Replacement Demand

- 4.2.6 Inclusive-School Mandates Requiring On-Site Mobility Devices

- 4.3 Market Restraints

- 4.3.1 High Price & Limited Insurance in Emerging Markets

- 4.3.2 Complex Hospital Procurement Regulations

- 4.3.3 Rapid Child Growth Shortening Product Life Cycle

- 4.3.4 Rare-Earth Motor Supply Volatility for Powered Models

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Manual

- 5.1.2 Powered

- 5.2 By Frame Type

- 5.2.1 Rigid

- 5.2.2 Foldable

- 5.2.3 Tilt-in-Space

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Homecare Settings

- 5.3.3 Rehabilitation Centers

- 5.3.4 Other End Users

- 5.4 By Distribution Channel

- 5.4.1 Offline

- 5.4.2 Online

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Sunrise Medical

- 6.3.2 Invacare

- 6.3.3 Permobil

- 6.3.4 Ottobock

- 6.3.5 MEYRA GmbH

- 6.3.6 Ki Mobility

- 6.3.7 Leckey

- 6.3.8 Drive DeVilbiss Healthcare

- 6.3.9 R82 (Etac)

- 6.3.10 SORG Rollstuhltechnik GmbH

- 6.3.11 AKCES-MED sp. z o.o.

- 6.3.12 Medline Industries

- 6.3.13 VELA Medical

- 6.3.14 Smirthwaite

- 6.3.15 Motion Composites

- 6.3.16 Panthera

- 6.3.17 Karma Medical

- 6.3.18 Nissin Medical

- 6.3.19 Karma Mobility

- 6.3.20 Momentum Healthcare

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment