|

시장보고서

상품코드

1842712

각막 토포그래퍼 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Corneal Topographers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

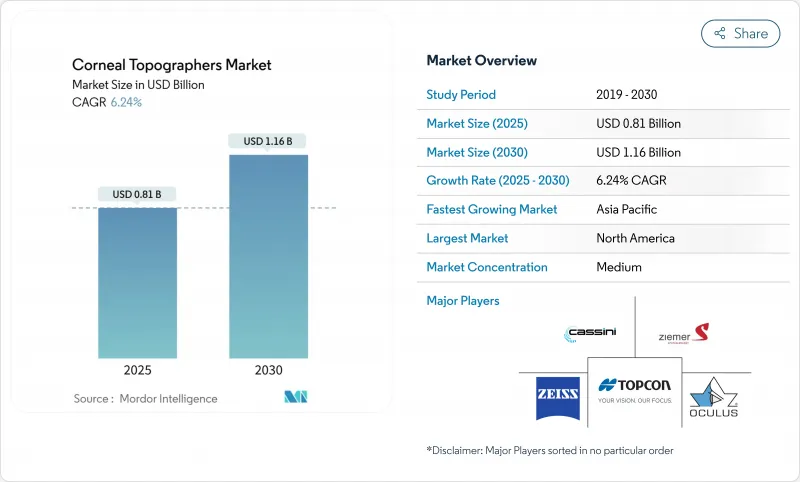

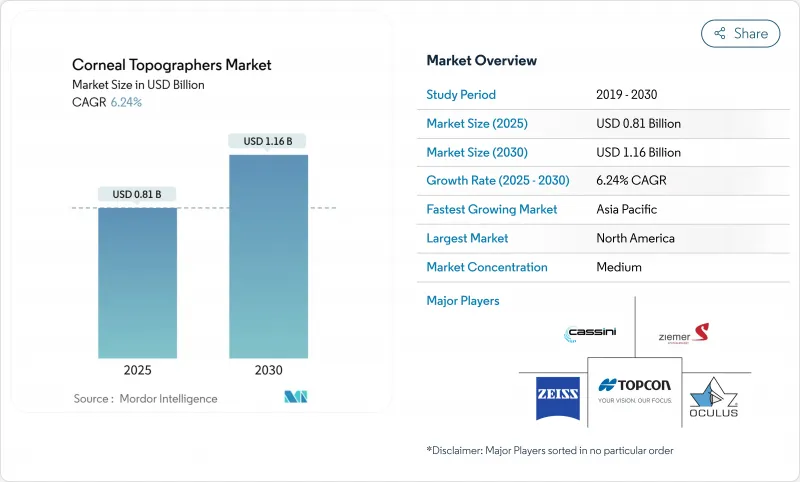

각막 토포그래퍼 시장은 2025년에 8억 1,000만 달러, 2030년에는 11억 6,000만 달러에 이르고, CAGR 6.24%로 성장할 것으로 예상됩니다.

성장을 뒷받침하는 것은 단일 목적 케라토메트리에서 형태학적 평가와 생체역학적 평가를 통합한 종합적인 전안부 이미징으로의 전환입니다. 세계적인 근시율 상승, 고급 백내장 수술과 굴절 교정 수술을 요구하는 고령화, 인공지능의 급속한 통합이 채택의 주요 원동력이 되고 있습니다. 클라우드로 연결된 스마트폰 기반 장비는 각막 분석을 1차 진료에 도입하고, 정부가 지원하는 시력 검사 프로그램은 새로운 구매 채널을 창출하고 있습니다. 경쟁 강도는 중간 정도를 유지합니다. 기존 기업은 샤인프루프, 플라시드, OCT 기술을 결합한 포트폴리오의 확대와 워크플로우 통합을 목표로 한 전략적 인수를 통해 지위를 지키고 있습니다.

세계 각막 토포그래퍼 시장 동향과 통찰

소아 및 청소년층의 근시 및 원추 각막의 부담 증가

2050년까지 세계 인구의 절반이 근시가 될 것으로 예측되고 있으며, 최근 중국의 횡단 조사에서는 이미 초등학생들 사이에서 50.93%의 유병률이 보고되고 있습니다. 소아의 이환율에서 진단되지 않은 질병이 밝혀져 임상 의사에게 스크리닝 프로토콜의 확대를 촉구하고 있기 때문에 조기 원뿔 각막의 발견이 급선무가 되고 있습니다. 오르소케라톨로지의 피팅은 근시 억제 효과를 검증하기 위한 정확한 앙각 맵과 축 길이 측정이 필요하기 때문에 각막 토포그래퍼 시장은 혜택을 받습니다. OCULUS는 2025년 Pentacam AXL Wave 소프트웨어를 발표하고 근시 관리를 통합하기 위해 토모그래피와 축 길이를 통합했습니다. 청년층에서의 평생 모니터링의 필요성으로 인해 반복적인 영상 진단에 대한 수요가 발생하여 1차 케어 및 전문 클리닉에서의 기기 이용이 촉진됩니다.

백내장과 굴절 교정 수술에 박차를 가하는 고령화 인구 통계

미국의 65세 이상 인구는 2020년 5,610만명에서 2030년에는 7,310만명으로 증가할 것으로 예측되어 수술량이 증가할 것으로 예상됩니다. 세계 백내장 수술 건수는 2024년 3,100만 건에서 2029년에는 3,700만 건으로 증가하며, 각 사례에서는 토릭 렌즈나 다초점 렌즈의 선택을 최적화하기 위한 각막 매핑이 필수가 됩니다. Pentacam AXL로 대표되는 각막 단층 촬영과 광학 생체 측정의 통합은 수술 시간을 단축하고 굴절률 예측 가능성을 높입니다. 프리미엄 IOL의 채택은 더 높은 자기 부담을 요구하고, 오류가 없는 결과에 대한 환자의 기대를 높이고, 고해상도 지형에 대한 수요를 유지합니다. 그 결과, 각막 토포그래퍼 시장은 고령화가 진행되는 선진국에서 안정적인 수익 기반을 확보하고 있습니다.

고급 시스템의 높은 취득 및 유지 비용

플래그십 하이브리드 플랫폼은 8만 달러에서 15만 달러로 판매되며, 가격에 민감한 시장에서는 수입 관세를 고려하면 25-40% 상승할 수 있습니다. 2024년 매출을 3-5% 삭감한 제조업체도 있는 반도체 부족은 부품 비용을 높여주고, 고급 광학계는 정기적인 교정과 독자적인 소프트웨어 구독을 요구합니다. 총 소유 비용(Total Cost of Ownership)은 소규모 클리닉의 시스템 업그레이드를 억제하여 구매 연기 및 낮은 사양 대체품 선택을 촉구합니다. 임대 및 사용 기반 모델은 초기 지출을 줄이지만 정기적인 사용료는 운영 예산을 압박합니다. 각막 토포그래퍼 시장이 클라우드 전달 분석에 기울어짐에 따라 운영 비용이 자본 투자 절약을 상쇄하고 장기적인 억제요인으로 가격을 유지할 위험이 있습니다.

부문 분석

프라시드 반사 시스템은 2024년에 35.82%의 압도적인 점유율을 차지하며, 저렴하고 정착한 임상 워크플로우의 혜택을 받고 있습니다. 그러나 곡선 기반 알고리즘은 각막 후면의 요철에 고전하기 때문에 안과 의사는 앙각 기반 이미징을 선택할 수밖에 없습니다. 플라시드를 샤인프루프나 OCT와 융합시킨 하이브리드 멀티모달 플랫폼은 CAGR 8.82%를 기록해 각막 토포그래퍼 시장에서 가장 빠른 페이스입니다. 이 워크스테이션은 한 번의 촬영으로 패티메트리, 후방 곡률 및 전안부 단층 촬영을 수행하여 수술 전 평가를 몇 분으로 응축합니다. Scheimpflug 전용 시스템은 고급 안구 렌즈 계획과 관련이 있지만 벤더는 경쟁력을 유지하기 위해 AI 모듈로 강화되었습니다. Cassini와 같은 LED 컬러 반사 솔루션은 눈물 아티팩트를 보정하여 수술 후 긁힌 각막의 정확성을 향상시킵니다. 스마트폰용 어태치먼트나 컴팩트한 슬릿 스캔 유닛은 1차 케어나 모바일 아웃리치를 타겟으로 한 틈새 위치를 차지하고 있습니다. 지속적인 펌웨어 업그레이드는 새로운 분석을 가능하게 하여 하드웨어의 진부화를 연장하고 사용자는 브랜드 에코시스템에 묶여 각막 토포그래퍼 업계 전체의 점성을 강화합니다.

공급업체 상황은 단일 장비가 아닌 통합된 이미징 제품군에 집중되어 있습니다. Carl Zeiss Meditec의 Cirrus 플랫폼은 토포그래피와 OCT를 결합하여 Topcon은 켈라토미터와 슬릿 램프 카메라를 번들로 제공합니다. 경쟁은 광학 하드웨어와 마찬가지로 알고리즘의 정확도에 있으며, 각 회사는 딥러닝 데이터 세트에 많은 투자를 하고 있습니다. 공급망 회복력, 특히 고품질 이미지 센서에 대한 액세스는 2024년 공급 부족 이후 차별화 요인이 되었습니다. 클라우드 연결이 보급됨에 따라 광학적 충실도와 함께 안전한 데이터 파이프라인과 HIPAA 호환 스토리지가 구매 기준으로 부상하고 있습니다. 전반적으로 각막 토포그래퍼 시장의 기술 다양화는 올인원 수술 계획 스테이션의 프리미엄 틈새를 유지하면서 시설 예산에 맞는 단계적 가격을 가속화합니다.

지역 분석

북미의 2024년 점유율 38.81%는 성숙한 지불자 환경, 풍부한 R&D 생태계, 조기부터 AI 장비 도입을 뒷받침하고 있습니다. 원뿔 각막과 복잡한 안구 렌즈를 계획하는 데 사용되는 지형에 대한 Medicare 보험 적용은 자기 부담의 영향을 완화시키고 민간 보험 회사는 점차 적응을 확대하고 있습니다. 알콘은 2023년에 8억 2,800만 달러를 연구개발비에 충당해, 지속적인 기술 혁신에의 업계의 헌신을 나타내고 있습니다. 규제 당국의 감시는 엄격하지만, FDA의 2025년 AI 지침이 투명성을 가져와 제조업체에 알고리즘 제출을 신속하게 촉구하고 있습니다. 시장 포화는 성장을 억제하지만 10년 전에 설치된 시스템의 교체 사이클은 안정적인 수요를 유지합니다. 의료기관은 사이버 보안을 선호하고 구매 전에 데이터 보호 프로토콜을 인증하도록 공급업체에 일하고 있습니다. 병원 예산의 압박은 계속되고 있지만, 진료 보수의 조정에 의해 각막 토포그래퍼 시장의 북미의 수익 기반은 유지되고 있습니다.

아시아태평양은 2025년부터 2030년의 CAGR 가장 빠른 9.14%를 기록할 것으로 예상됩니다. 동아시아의 일부 도시에서는 80%가 넘는 도시의 어린이들의 근시율이 급상승하고 있으며, 부모들이 정형외과 평가와 조기 검진에 기꺼이 비용을 지불하도록 유도하고 있습니다. 중국의 기기 승인 기관은 2025년 2월, 자이스의 Visumax 800을 SMILE pro용으로 승인해, 고도 굴절 교정 기술에 대한 규제 당국의 개방성을 나타냈습니다. 인도 중산계급은 가처분소득 상승에 따라 예방안과 의료 지출을 늘리고 아시아개발은행의 7,500만 달러의 의료기술 투자 시설은 공립병원에 대한 대출을 완화했습니다. Shenzhen, Pune에 위치한 현지 제조 클러스터는 리드 타임을 단축하고 수입 관세를 줄여 가격 경쟁력을 높이고 있습니다. 그러나 임상의 부족과 불균등한 상환으로 인해 지방의 도입이 늦어지고 각막 토포그래퍼 시장을 더욱 다양화하는 이동검진 유닛과 원격안과 허브가 필요합니다.

유럽은 예방 의료와 노인 인구 역학에 힘입어 완만한 확대를 유지하고 있습니다. 일관된 MDR 규정은 적합성 평가를 간소화하지만 Brexit은 영국 시장 진입에 복잡성을 추가합니다. 공공의료제도는 백내장과 원추각막의 적응증 때문에 각막영상 진단에 자금을 제공하고 있지만, 긴축예산은 남유럽에서의 프리미엄 기기의 보급을 억제하고 있습니다. 중동 및 아프리카는 아직 개발도상이지만 석유수출국이 의료지출을 다각화하고 연수 프로그램이 확대됨에 따라 기세를 보이고 있습니다. 남미에서는 최근 경기침체로부터의 회복이 브라질과 아르헨티나의 안과기기 입찰을 지원하고 있습니다. 지역 전체에서 조기 개입과 디지털 건강을 평가하는 정책 지침은 각막 토포그래퍼 시장의 일관된 상승을 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 도입

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 소아 및 젊은 성인에서의 근시 및 원추 각막의 부담 증가

- 백내장 및 굴절 교정 수술에 박차를 가하는 인구 동태의 고령화

- 정부 자금에 의한 시력 검사와 원격 안과의 전개

- AI를 활용한 각막 단층 촬영에 의한 안구 외반의 조기 발견

- 클라우드 연결 스마트폰 토포그래퍼, 1차 진료 채널 개설

- Ortho-K 피팅 데이터 통합을 위한 콘택트렌즈 산업 수요

- 시장 성장 억제요인

- 고급 시스템의 고액의 구입비와 유지비

- EM에서 숙련된 안과 의사와 검안사의 부족

- 단체의 각막 이미징에 대한 상환의 제한

- 멀티모달의 전안부 OCT 장치에 의한 대체품의 위협

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 기술별

- 플라시드 반사 시스템

- 스캐닝 슬릿 시스템

- Scheimflug 이미징 시스템

- 하이브리드 멀티 모달 시스템

- 기타 기술

- 용도별

- 굴절 교정 수술 계획

- 백내장 수술 IOL의 선택

- 각화증 및 외반성 진단

- 각막 부종과 이영양증의 평가

- 콘택트렌즈 피팅

- 소프트 렌즈와 RGP 렌즈의 피팅

- 각막교정렌즈(Ortho-K) 피팅

- 안구건조증와 안표면의 평가

- 학술 및 연구 기관

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 안과 클리닉

- 검안 및 시력 케어 센터

- 학술기관 및 연구기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Topcon Medical Systems Inc

- Carl Zeiss Meditec AG

- NIDEK Co., Ltd.

- Oculus Optikgerate GmbH

- Haag-Streit AG

- Cassini Technologies BV

- Ziemer Ophthalmic Systems AG

- Luneau Technology Group(Visionix)

- Medmont International Pty Ltd

- Tomey Corporation

- Optos plc

- Alcon Inc(WaveLight)

- Canon Inc

- Bausch & Lomb Incorporated

- Essilor Instruments

- Tracey Technologies Corp.

- Eyenuk Inc

제7장 시장 기회와 전망

SHW 25.11.03The corneal topographers market is valued at USD 0.81 billion in 2025 and is expected to reach USD 1.16 billion by 2030, advancing at a 6.24% CAGR.

Growth is propelled by the shift from single-purpose keratometry to comprehensive anterior-segment imaging that unites morphological and biomechanical assessment. Rising global myopia prevalence, an aging population demanding premium cataract and refractive procedures, and rapid integration of artificial intelligence are the chief engines of adoption. Cloud-connected, smartphone-based devices are bringing corneal analysis into primary care, while government-backed vision-screening programs create new purchase channels. Competitive intensity stays moderate; incumbents defend positions through portfolio expansions that combine Scheimpflug, Placido, and OCT technologies and through strategic acquisitions targeting workflow integration.

Global Corneal Topographers Market Trends and Insights

Rising burden of myopia and keratoconus in paediatric and young-adult cohorts

Half the global population is projected to be myopic by 2050, and recent Chinese cross-sectional surveys already report 50.93% prevalence among schoolchildren, with urban rates even higher. Early-stage keratoconus detection is gaining urgency as paediatric incidence reveals under-diagnosed disease, prompting clinicians to widen screening protocols. The corneal topographers market benefits because orthokeratology fitting requires precise elevation maps and axial length measurement to validate myopia-control efficacy. OCULUS introduced Pentacam AXL Wave software in 2025, merging tomography with axial length for integrated myopia management. Lifelong monitoring needs in younger cohorts yield recurrent imaging demand, bolstering device utilization across primary care and specialty clinics.

Aging demographic fuelling cataract and refractive surgeries

The United States 65-plus population is forecast to climb from 56.1 million in 2020 to 73.1 million by 2030, pushing surgical volumes upward. Global cataract procedures are set to rise from 31 million in 2024 to 37 million in 2029, each case mandating corneal mapping to optimise toric and multifocal lens selection. Integration of corneal tomography with optical biometry, exemplified by Pentacam AXL, cuts chair time and heightens refractive predictability. Premium IOL adoption, which commands higher out-of-pocket spending, raises patient expectations for error-free outcomes, preserving demand for high-resolution topography. Consequently, the corneal topographers market secures a stable revenue base in advanced economies with aging demographics.

High acquisition and maintenance cost of advanced systems

Flagship hybrid platforms list between USD 80,000 and USD 150,000, a figure that can climb 25-40% after import duties in price-sensitive markets. Semiconductor shortages, which shaved 3-5% off some manufacturers' 2024 revenue, keep component costs elevated, while sophisticated optics demand periodic calibration and proprietary software subscriptions. Total cost of ownership discourages smaller practices from system upgrades, nudging them to defer purchases or select lower-spec alternatives. Leasing and usage-based models relieve upfront expenditure, yet recurring fees stretch operating budgets. As the corneal topographers market tilts toward cloud-delivered analytics, operating costs risk offsetting capex savings, sustaining price as a long-run restraint.

Other drivers and restraints analyzed in the detailed report include:

- Government-funded vision screening and tele-ophthalmology roll-outs

- AI-enhanced corneal tomography for early ectasia detection

- Shortage of skilled ophthalmologists and optometrists in emerging markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Placido reflection systems held a commanding 35.82% share in 2024, benefiting from affordability and entrenched clinical workflows. However, their curve-based algorithms struggle with posterior corneal irregularities, nudging ophthalmologists toward elevation-based imaging. Hybrid multi-modal platforms that meld Placido with Scheimpflug or OCT record an 8.82% CAGR, the fastest pace within the corneal topographers market. These workstations deliver pachymetry, posterior curvature, and anterior-segment tomography in a single capture, condensing pre-surgical evaluation into minutes. Scheimpflug-only systems retain relevance for premium intraocular lens planning, yet vendors augment them with AI modules to maintain competitiveness. LED color reflection solutions such as Cassini improve accuracy for post-surgical or scarred corneas by compensating for tear-film artefacts. Smartphone attachments and compact slit-scanning units occupy niche positions targeting primary care and mobile outreach. Continuous firmware upgrades that unlock new analytics postpone hardware obsolescence, binding users to brand ecosystems and reinforcing stickiness across the corneal topographers industry.

The vendor landscape coalesces around integrated imaging suites rather than stand-alone devices. Carl Zeiss Meditec's Cirrus platform combines topography with OCT; Topcon bundles keratometers with slit-lamp cameras. Competitive stakes lie in algorithmic precision as much as optical hardware, prompting players to invest heavily in deep-learning datasets. Supply chain resilience, particularly access to high-grade image sensors, has become a differentiator after 2024 shortages. As cloud connectivity spreads, secure data pipelines and HIPAA-compliant storage emerge as purchase criteria alongside optical fidelity. Overall, technology diversification within the corneal topographers market fosters tiered pricing that aligns with facility budgets while preserving a premium niche for all-in-one surgical planning stations.

The Corneal Topographers Market is Segmented by Technology (Placido Reflection Systems, Scanning Slit Systems, and More), Application (Refractive Surgery Planning, Contact Lens Fitting [Soft & RGP Lens Fitting, Orthokeratology Lens Fitting], End User (Hospitals, Ambulatory Surgical Centers, and More], and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's 38.81% share in 2024 underscores its mature payer environment, rich R&D ecosystem, and early AI device adoption. Medicare coverage for topography when used for keratoconus or complex IOL planning softens out-of-pocket impact, while private insurers gradually expand indications. Alcon devoted USD 828 million to R&D in 2023, demonstrating industry commitment to continuous innovation. Regulatory scrutiny is rigorous, yet the FDA's 2025 AI guidance lends transparency, encouraging manufacturers to accelerate algorithm submissions. Market saturation tempers growth, but replacement cycles for systems installed a decade earlier sustain steady demand. Institutions prioritise cybersecurity, pushing vendors to certify data-protection protocols before purchase. Although hospital budget pressure persists, reimbursement alignment preserves the corneal topographers market's North American revenue base.

Asia-Pacific records the fastest 9.14% CAGR between 2025 and 2030. Skyrocketing myopia prevalence in urban children, exceeding 80% in some East Asian cities, drives parental willingness to pay for ortho-K assessments and early screening. China's device-approval agency cleared Zeiss Visumax 800 for SMILE pro in February 2025, signalling regulatory openness to advanced refractive technology. India's middle class spends more on preventive eye care as disposable income rises, while the Asian Development Bank's USD 75 million health-tech investment facility eases financing for public hospitals. Local manufacturing clusters in Shenzhen and Pune shorten lead times and cut import tariffs, enhancing price competitiveness. However, clinician shortages and uneven reimbursement slow adoption in rural provinces, necessitating mobile screening units and tele-ophthalmology hubs that further diversify the corneal topographers market.

Europe maintains moderate expansion anchored in preventive medicine and ageing demographics. Harmonised MDR regulations streamline conformity assessment, yet Brexit adds complexity for UK market entry. Public health systems fund corneal imaging for cataract and keratoconus indications, though austerity budgets cap premium device penetration in Southern Europe. Middle East and Africa remain nascent but show momentum as oil-exporting nations diversify health spending and training programs expand. South America's rebound from recent economic soft patches supports ophthalmology equipment tenders in Brazil and Argentina. Across regions, policy directives that valorise early intervention and digital health bolster a consistent upswing in the corneal topographers market.

- Topcon

- Carl Zeiss

- Nidek

- Oculus Optikgerate GmbH

- Haag-Streit AG

- Cassini Technologies B.V.

- Ziemer Group

- Luneau Technology Group (Visionix)

- Medmont International

- Tomey

- Optos

- Alcon Inc (WaveLight)

- Canon

- Bausch Health

- Essilor Instruments

- Tracey Technologies Corp.

- Eyenuk

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising burden of myopia & keratoconus in paediatric & young-adult cohorts

- 4.2.2 Aging demographic fuelling cataract & refractive surgeries

- 4.2.3 Government-funded vision-screening & tele-ophthalmology roll-outs

- 4.2.4 AI-enhanced corneal tomography for early ectasia detection

- 4.2.5 Cloud-connected smartphone topographers opening primary-care channel

- 4.2.6 Contact-lens industry demand for ortho-K fitting data integration

- 4.3 Market Restraints

- 4.3.1 High acquisition & maintenance cost of advanced systems

- 4.3.2 Shortage of skilled ophthalmologists & optometrists in EMs

- 4.3.3 Limited reimbursement for standalone corneal imaging

- 4.3.4 Substitution threat from multi-modal anterior-segment OCT devices

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Placido Reflection Systems

- 5.1.2 Scanning Slit Systems

- 5.1.3 Scheimpflug Imaging Systems

- 5.1.4 Hybrid Multi-modal Systems

- 5.1.5 Other Technologies

- 5.2 By Application

- 5.2.1 Refractive Surgery Planning

- 5.2.2 Cataract Surgery IOL Selection

- 5.2.3 Keratoconus & Ectasia Diagnosis

- 5.2.4 Corneal Edema & Dystrophy Assessment

- 5.2.5 Contact Lens Fitting

- 5.2.5.1 Soft & RGP Lens Fitting

- 5.2.5.2 Orthokeratology Lens Fitting

- 5.2.6 Dry Eye & Ocular Surface Evaluation

- 5.2.7 Research & Academic Use

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Ophthalmology Clinics

- 5.3.4 Optometry & Vision-care Centers

- 5.3.5 Academic & Research Institutes

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Topcon Medical Systems Inc

- 6.3.2 Carl Zeiss Meditec AG

- 6.3.3 NIDEK Co., Ltd.

- 6.3.4 Oculus Optikgerate GmbH

- 6.3.5 Haag-Streit AG

- 6.3.6 Cassini Technologies B.V.

- 6.3.7 Ziemer Ophthalmic Systems AG

- 6.3.8 Luneau Technology Group (Visionix)

- 6.3.9 Medmont International Pty Ltd

- 6.3.10 Tomey Corporation

- 6.3.11 Optos plc

- 6.3.12 Alcon Inc (WaveLight)

- 6.3.13 Canon Inc

- 6.3.14 Bausch & Lomb Incorporated

- 6.3.15 Essilor Instruments

- 6.3.16 Tracey Technologies Corp.

- 6.3.17 Eyenuk Inc

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment