|

시장보고서

상품코드

1844475

벤조산 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Benzoic Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

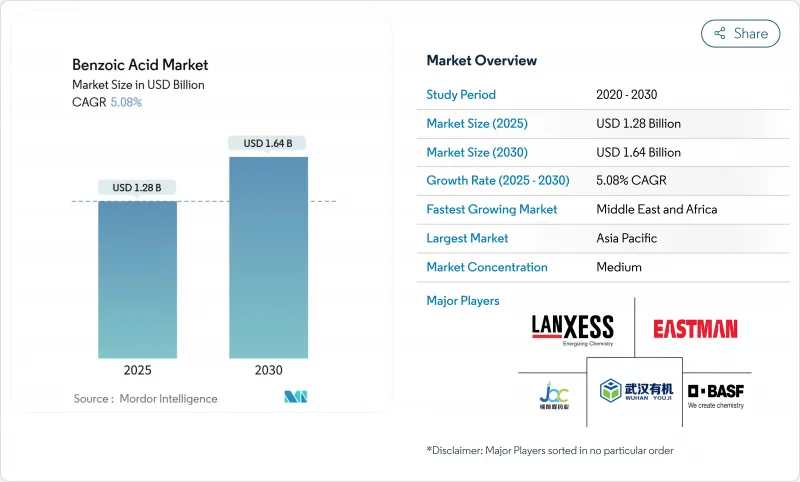

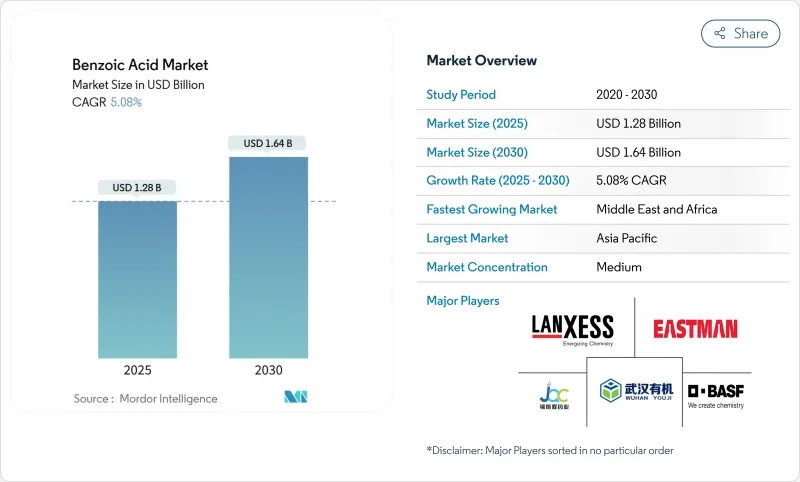

벤조산 시장 규모는 2025년에 12억 8,000만 달러에 달하고, 2030년에는 16억 4,000만 달러로 성장하며, CAGR 5.08%를 나타낼 것으로 예측됩니다.

시장 성장의 원동력이 되는 것은 유통 기한의 연장 요건, 프탈레이트 대체, 고순도 제조 공정에 중점을 둔 규제입니다. 유럽연합(EU)에 의한 식품 접촉 규제의 엄격화와 미국 식품의약국(FDA)에 의한 25유형의 오르토프탈산계 가소제의 사용 금지는 식품, 의약품, 가소제 용도에 새로운 기회를 만들어 냅니다. 아시아태평양은 생산 우위를 유지하고 있지만 중동 및 아프리카는 식품 가공 산업화로 인해 가장 높은 성장률을 보이고 있습니다. 이 시장에서는 취급의 용이성, 의약품의 품질 요건, 규제상의 지원 등을 배경으로 액체 제제, 초고순도 등급, 벤조산염가소제의 채용이 증가하고 있습니다. 경쟁 구도는 부드럽고 세계 기업과 지역 공급업체가 시장 존재를 공유하고 그린 케미컬 및 연속 처리의 진보로 이어지고 있습니다.

세계의 벤조산 시장 동향과 인사이트

신흥국의 보존 기간이 긴 의약품의 규제 강화

신흥 시장의 의약품 규제 당국은 보다 엄격한 유통기한 요건을 도입하고 있어 벤조산 수요가 증가하고 있습니다. 벤조산이 미생물의 번식을 방지하고 세균이나 진균의 오염을 억제함으로써 보존 기간을 연장하는 액체 제제에서는 제품의 안정성 연장이 중시되고 있습니다. 이러한 규제 동향은 특히 의료규제가 엄격해지고 있는 중국, 인도, 브라질 등 국가에서 의약품 부문의 일관된 수요 증가를 이끌고 있습니다. 아시아태평양 시장 전체의 규제의 무결성에 의해 벤조산은 특히 원료의약품과의 적합성이 요구되는 경구제나 비경구제에 있어서, 중요한 방부제로서 자리매김되고 있습니다. 이러한 제형은 내복액, 현탁액, 주사제 및 기타 액체 의약품을 포함합니다. 신생아 용도의 안전 요건으로 순도 사양의 고순도 등급에 대한 수요가 높아지고 있으며, 초고순도 부문의 성장을 지원하고 있습니다. 이 수요는 또한 소아용 의약품에 대한 주목 증가, 섬세한 의약품 용도에서 오염이 없는 방부제의 필요성, 신규 약물전달 시스템에서 벤조산의 채용 증가에 의해 견인되고 있습니다. 제약 업계는 품질 관리와 규정 준수를 중시하고 있기 때문에 벤조산이 이러한 엄격한 요구 사항을 충족하는지 확인하기 위해 고급 정제 기술 및 시험 방법에 대한 투자가 증가하고 있습니다.

농약 합성에서 염화 벤조일의 사용 확대

벤조산 유도체인 벤조일 클로라이드는 제초제 및 살균제, 특히 저항성 잡초를 방제하고 작물의 수율을 향상시키는 클로란벤 아날로그의 제조에 중요한 성분입니다. 이 화합물의 특성을 통해 제조업체는 작물의 안전성을 유지하면서 해충 저항성을 다루는 특정 제형을 개발할 수 있습니다. 인도 제제 제조업체와 중국 계약 제조업체는 특정 불순물 프로파일을 가진 제품에 대한 세계 농약 기업의 요구에 부응하기 위해 개선된 공정 관리 및 품질 시스템을 도입하여 생산 능력을 확대하고 있습니다. 이러한 생산 강화에는 더 나은 여과 시스템, 자동화된 모니터링, 종합적인 품질 테스트 프로토콜 등이 포함됩니다. 아미드기 함유 술폰산 유도체의 조사는 농업 부문의 지속가능성 중점의 관점에서 증가하고 있습니다. 실험실 연구에 따르면 이러한 유도체는 기존 활성 성분에 비해 표적 유기체에 대한 치사 농도가 높아 해충 방제 효율을 유지하면서 살포량을 줄일 수 있습니다. 시장 성장은 환경 규제와 안전 요건을 충족하면서 비용 효과를 달성하고 농약 공급망에서 벤조산의 안정적인 수요를 유지할 수 있는지 여부에 달려 있습니다. 업계는 새로운 농작물 보호 제품을 개발하기 위해 염화 벤조일을 기반으로 한 솔루션에 대한 투자를 계속하고 있습니다.

클린 라벨 방부제로의 전환은 합성 벤조산염의 채용을 제한합니다.

천연 성분에 대한 소비자의 선호도가 높아짐에 따라 식품 제조업체는 벤조산 나트륨을 포함한 합성 보존제의 대체품을 요구할 수밖에 없습니다. 유럽 시장 데이터는 소비자가 제품 라벨을 점점 더 음미하고 천연 대체품을 추구하기 때문에 성분 조달 및 제조 공정 투명성을 제공하는 클린 라벨 제품에 대한 수요가 증가하고 있음을 보여줍니다. 식물 추출물, 에센셜 오일, 미생물 대사산물과 같은 천연 항균 화합물은 합성 보존제를 대체할 가능성이 있습니다. 이 천연 화합물은 깨끗한 라벨 제품을 요구하는 소비자의 선호도에 따라 식품 유래 병원체의 제어에 효과적임을 입증합니다. 식육 업계는 천연 보존제에 큰 관심을 보이고 있으며 합성 화학 물질의 대안으로 박테리오파지, 박테리오신, 항균 펩타이드 등의 선택을 폭넓게 모색하고 있습니다. 이 대용품은 실험실 및 상업 환경에서 유망한 결과를 보여줍니다. 그러나 표준화 과제, 높은 생산 비용, 식품 용도에 따라 다른 항균 효과 등의 이유로 천연 대체 물질의 보급에는 한계가 있습니다. 규제 환경, 특히 EU에서는 합성 보존제에 대한 보다 엄격한 지침과 승인 과정을 통해 천연 성분을 지지하는 방향으로 변화하고 있으며, 이는 벤조산 제조업체에게 시장 적응과 제품 개척의 기회와 과제를 모두 가져왔습니다.

부문 분석

무수 등급의 벤조산 시장은 2024년에 53.21%의 압도적인 시장 점유율을 차지하며, 산업 전반에 걸친 광범위한 용도에 지지되었습니다. 무수 분말은 흡습성이 낮고 벌크 보관이 효율적이므로 건조 혼합 식품, 고분자 촉매 및 미립자 동물사료 블렌드에 적합합니다. 이러한 특성은 보관 기간 동안 제품의 안정성과 품질을 유지하는 데 도움이 됩니다. 액상 제품 부문은 가공 효율과 작업상의 이점으로 견인되며 CAGR 6.34%를 나타낼 전망입니다. 의약품 시럽 제조업체는 액체 벤조산 용액을 사용하여 현장에서의 용해 공정을 생략하고 정확한 분석 공차를 유지함으로써 제조 공정을 합리화하고 배치의 편차를 억제하여 제품의 일관성을 향상시키고 있습니다. 산업용 코팅 제조업체는 고전단 반응기에서 액체를 사용하여 보다 신속한 균질화를 달성하고 생산 시간을 단축하고 효율을 향상시킵니다.

공정 강화는 제조 공정에서 액체의 흡수 능력을 현저하게 향상시켰습니다. 종합적인 실험실 테스트에 따르면, 액체 벤조산은 알키드 수지의 연쇄 정지제로서 보다 효과적으로 기능하여 광택 유지 및 표면 마감 품질을 향상시켰습니다. 이러한 성능의 대폭적인 향상은 취급이나 가공시의 분진 배출의 저감과 함께 벤조산 시장 전체에 비해 이 부문의 성장 궤도의 힘을 지지하고 있습니다. 또한 액상에서의 효율 향상은 처리 시간의 단축과 다양한 산업용도에의 보다 나은 통합으로 이어져 시장에서의 입지를 더욱 강화하고 있습니다.

순도 99.5-99.9%의 부문은 주로 중요한 제조 공정에서 널리 사용되고 있기 때문에 2024년 시장 점유율은 62.78%로 압도적이었습니다. 99.9% 이상의 초고순도 등급은 엄격한 품질 사양이 요구되는 특수 코팅 및 의약품 용도 수요 증가에 견인되어 2030년까지 연평균 복합 성장률(CAGR) 7.22%를 나타낼 전망입니다. 제약 업계는 특히 환자의 안전성과 규정 준수를 위해 엄격한 약전 기준을 충족해야 하는 비경구 제형으로 인해 높은 순도 등급을 요구합니다. 바이오 생산 방법의 연구는 막 분리 및 크로마토그래피 기술을 포함한 고급 정제 기술에 의해 지원되며 비용 효율성을 유지하면서 초고순도 수준의 혁신적인 프로세스를 개발하고 있습니다.

순도 99.0-99.5%의 등급은 식품 보존 및 기본 산업용도에 필수적인 요구 사항을 충족하며 경쟁력 있는 가격대에서 신뢰할 수 있는 성능을 제공합니다. 이 등급은 초고순도가 중요하지 않은 일반적인 제조 공정에서 널리 사용됩니다. 제조업체는 보다 높은 순도 사양을 일관되게 달성하기 위해 정교한 분석 기법과 종합적인 품질 관리 시스템을 도입하여 업무 효율과 생산 수율을 최적화하면서 프리미엄 부문의 성장을 지원합니다.

지역 분석

아시아태평양은 2024년 세계 시장의 42.19%를 차지하며 절강 석유화학의 1,180만 톤 시설을 포함한 중국의 대규모 방향족 콤플렉스가 실질적인 톨루엔 원료 공급을 공급했습니다. 이 지역의 가공업자는 수출 지향 규제와 통합 물류 네트워크를 활용하여 유통 경로를 최적화하고 운영 비용을 절감하고 있습니다. 인도의 확대하는 제약·식품 가공 섹터는 방부제나 중간체 등 복수의 용도를 통해 수요를 확대해, 일본의 기술력은 전자 도료나 특수 산업용도용의 고품질 그레이드의 생산을 가능하게 하고 있습니다. ASEAN 국가들은 면세무역협정을 이용하여 유럽과 북미로의 수출을 위한 유통센터를 설립하고, 벤조산 시장을 지역공급망에 통합하고, 현지 제조업체에 부가가치의 기회를 창출하고 있습니다.

중동 및 아프리카는 CAGR 6.83%로 가장 높은 성장률을 보이고 있는데, 이는 도시화의 진전이 보존 식품, 식음료, 퍼스널케어 아이템 수요를 견인하고 있는 것에 더해, 세제 우대 조치나 인프라 정비를 통해 폴리머 제조업체를 유치하는 정부의 이니셔티브에 지지되고 있습니다. 사우디아라비아의 시험 시설에서는 PVC 케이블 절연체 제조용 벤조산염 가소제가 평가되어 국내 제조 요건을 지원하고 수입 의존도를 줄이고 있습니다.

북미는 FDA 규제 프레임워크과 식품, 음식, 소비재의 각 분야에서 프탈산에스테르 프리의 패키징 솔루션을 요구하는 제조업체의 기호로부터 혜택을 받고 있습니다. 유럽 시장은 비스페놀 제한에 관한 규칙(EU) 2024/3190에 적응하고, 포장 제조업체가 식품 접촉 재료 및 소비자 포장에 벤조산염 대체품을 채택하도록 촉구하는 반면, 재활용 요건은 비용 검토 및 재료 선택 프로세스에 영향을 미칩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 신흥국의 보존 기간이 긴 의약품의 규제 강화

- 농약 합성에 있어서 염화벤조일의 사용 확대

- 프탈산계 가소제를 벤조산계 대체품으로 대체

- 특수 도료용 고순도 벤조산 수요 증가

- 포장 식품 및 편의점 식품 수요 증가

- 생산기술의 진보

- 시장 성장 억제요인

- 합성벤조산염의 채용을 제한하는 클린 라벨 방부제로의 변화

- 원료 가격의 변동

- 건강과 안전에 대한 우려

- 천연 방부제와의 경쟁

- 공급망 분석

- 규제 전망

- Porter's Five Forces

- 신규 진입업자의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모와 성장 예측

- 형태별

- 액체

- 무수물

- 분말 및 결정

- 순도 등급별

- 99.0-99.5%

- 99.5-99.9%

- 99.9% 이상

- 유도체별

- 벤조산나트륨

- 벤조산칼륨

- 벤조산벤질

- 벤조일 클로라이드

- 벤조산 가소제

- 기타 유도체

- 용도별

- 식음료

- 제빵

- 과자류

- 유제품

- 음료

- 소스 및 드레싱

- 기타

- 의약품

- 화학 제품

- 퍼스널케어 및 화장품

- 동물 사료

- 기타

- 식음료

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미

- 유럽

- 영국

- 독일

- 프랑스

- 러시아

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 인도

- 중국

- 일본

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장의 집중

- 전략적인 동향

- 시장 랭킹 분석

- 기업 프로파일

- Lanxess AG

- Eastman Chemical Company

- Wuhan Youji Industry Co., Ltd.

- JQC(Huayin) Pharmaceutical Co., Ltd.

- BASF SE

- IG Petrochemicals Ltd.

- Chemcrux Enterprises Ltd.

- Ganesh Benzoplast Ltd.

- FUSHIMI Pharmaceutical Co., Ltd.

- Jiangsu Sanmu Group Co., Ltd.

- Thermo Fisher Scientific Inc.

- The Merck Group

- Smart Chemicals Group Co., Ltd.

- San Fu Chemical Co., Ltd.

- Mitsui Bussan Chemicals Co., Ltd.

- Spectrum Laboratory Products, Inc.

- Tokyo Chemical Industry Co., Ltd

- Sisco Research Laboratories Pvt Ltd

- Central Drug House(P) Ltd

- Otto Chemie Pvt. Ltd.

제7장 시장 기회와 전망

KTH 25.11.05The benzoic acid market size is expected to reach USD 1.28 billion in 2025 and is expected to grow to USD 1.64 billion by 2030, growing at a CAGR of 5.08%.

The market growth is driven by regulations that focus on extended shelf-life requirements, phthalate replacement, and high-purity manufacturing processes. The European Union's stricter food-contact regulations and the United States Food and Drug Administration's removal of 25 ortho-phthalate plasticizers create new opportunities in food, pharmaceutical, and plasticizer applications. The Asia-Pacific region maintains its production dominance, while the Middle East and Africa show the highest growth rate due to food processing industrialization. The market sees increasing adoption of liquid formulations, ultra-high purity grades, and benzoate plasticizers, driven by ease of handling, pharmaceutical quality requirements, and regulatory support. The competitive landscape remains moderate, with global companies and regional suppliers sharing market presence, leading to advancements in green chemistry and continuous processing.

Global Benzoic Acid Market Trends and Insights

Regulatory push for longer shelf-life pharmaceuticals in emerging economies

Pharmaceutical regulators in emerging markets are implementing stricter shelf-life requirements, increasing the demand for benzoic acid. The focus on extended product stability is significant in liquid formulations, where benzoic acid prevents microbial growth and extends shelf life by inhibiting bacterial and fungal contamination. This regulatory trend drives consistent demand growth in the pharmaceutical sector, particularly in countries like China, India, and Brazil, where healthcare regulations are becoming more stringent. The alignment of regulations across Asia-Pacific markets positions benzoic acid as a key preservative, particularly in oral and parenteral formulations that require compatibility with active pharmaceutical ingredients. These formulations include oral solutions, suspensions, injectable medications, and other liquid pharmaceutical products. The safety requirements for neonatal applications are increasing demand for higher purity grades, with specifications of purity, supporting growth in ultra-high purity segments. This demand is further driven by the growing focus on pediatric medications, the need for contamination-free preservatives in sensitive pharmaceutical applications, and the increasing adoption of benzoic acid in novel drug delivery systems. The pharmaceutical industry's emphasis on quality control and regulatory compliance has led to increased investment in advanced purification technologies and testing methods to ensure benzoic acid meets these stringent requirements.

Expansion of benzoyl chloride usage in agrochemical synthesis

Benzoyl chloride, a benzoic acid derivative, is a key component in manufacturing herbicides and fungicides, particularly chloramben analogs that control resistant weeds and improve crop yields. The compound's properties allow manufacturers to develop specific formulations that address pest resistance while maintaining crop safety. Indian formulators and Chinese contract manufacturers are expanding their production capabilities by implementing improved process controls and quality systems to meet global agrochemical companies' requirements for products with specific impurity profiles. These manufacturing enhancements include better filtration systems, automated monitoring, and comprehensive quality testing protocols. Research into amide-bearing sulfonate derivatives has increased due to the agricultural sector's sustainability focus. Laboratory studies show these derivatives achieve higher lethal-concentration effectiveness against target organisms compared to conventional active ingredients, potentially reducing application rates while maintaining pest control efficiency. The market growth depends on achieving cost-effectiveness while meeting environmental regulations and safety requirements, and maintaining consistent demand for benzoic acid in the agricultural chemical supply chain. The industry continues to invest in benzoyl chloride-based solutions for developing new crop protection products.

Shift towards clean-label preservatives limiting synthetic benzoate adoption

The growing consumer preference for natural ingredients is compelling food manufacturers to seek alternatives to synthetic preservatives, including sodium benzoate. European market data indicates rising demand for clean-label products that offer transparency in ingredient sourcing and manufacturing processes, with consumers increasingly scrutinizing product labels and demanding natural alternatives. Natural antimicrobial compounds, including plant extracts, essential oils, and microbial metabolites, have emerged as potential replacements for synthetic preservatives. These natural compounds demonstrate effectiveness in controlling foodborne pathogens while aligning with consumer preferences for clean-label products. The meat industry has shown significant interest in natural preservatives, extensively exploring options such as bacteriophages, bacteriocins, and antimicrobial peptides as substitutes for synthetic chemicals. These alternatives have demonstrated promising results in laboratory and commercial settings. However, the widespread adoption of natural alternatives faces limitations due to standardization challenges, higher production costs, and varying antimicrobial efficacy across different food applications. The regulatory environment, particularly in the EU, is shifting toward favoring natural ingredients through stricter guidelines and approval processes for synthetic preservatives, which presents both opportunities and challenges for benzoic acid manufacturers in terms of market adaptation and product development.

Other drivers and restraints analyzed in the detailed report include:

- Substitution of phthalate plasticizers with benzoate-based alternatives

- Growing demand for high-purity benzoic acid for specialty coatings

- Price volatility of raw materials

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The benzoic acid market for anhydrous grades held a dominant 53.21% market share in 2024, supported by its extensive applications across industries. Anhydrous powders serve as the preferred choice for dry-mix foods, polymer catalysts, and granular animal-feed blends, owing to their low moisture absorption and efficient bulk storage properties. These characteristics help maintain product stability and quality during storage periods. The liquid forms segment is growing at a 6.34% CAGR, driven by processing efficiency and operational benefits. Pharmaceutical syrup manufacturers use liquid benzoic acid solutions to streamline production processes by eliminating on-site dissolution steps and maintaining precise assay tolerances, which reduces batch variations and improves product consistency. Industrial coating manufacturers achieve faster homogenization by using liquids in high-shear reactors, reducing production time and improving efficiency.

Process intensification has significantly improved liquid uptake capabilities in manufacturing processes. Comprehensive laboratory tests indicate that liquid benzoic acid functions more effectively as a chain-stop agent in alkyd resins, resulting in enhanced gloss retention and surface finish quality. These substantial performance improvements, combined with reduced dust emissions during handling and processing, support the segment's stronger growth trajectory compared to the overall benzoic acid market. The improved efficiency in liquid form has also led to reduced processing times and better integration in various industrial applications, further strengthening its market position.

The 99.5-99.9% purity segment dominates with 62.78% market share in 2024, primarily due to its widespread use in critical manufacturing processes. Ultra-high purity grades above 99.9% are growing at 7.22% CAGR through 2030, driven by increasing demand from specialty coating and pharmaceutical applications requiring stringent quality specifications. The pharmaceutical industry requires higher purity grades, especially for parenteral formulations that must meet strict pharmacopeial standards for patient safety and regulatory compliance. Research into bio-based production methods is developing innovative processes for ultra-high purity levels while maintaining cost efficiency, supported by advanced purification technologies including membrane separation and chromatographic techniques.

The 99.0-99.5% purity grade meets essential requirements for food preservation and basic industrial applications, offering reliable performance at competitive price points. This grade finds extensive use in general manufacturing processes where ultra-high purity is not critical. Manufacturers are implementing sophisticated analytical methods and comprehensive quality control systems to achieve higher purity specifications consistently, supporting premium segment growth while optimizing operational efficiency and production yields.

The Benzoic Acid Market Report is Segmented by Form (Liquid, Anhydrous, and More), Purity Grade (99. 0-99. 5%, 99. 5-99. 9%, and More), Derivative (Sodium Benzoate, Potassium Benzoate, and More), Application (Food and Beverage, Pharmaceuticals, Chemicals, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 42.19% of the global market in 2024, with China's large-scale aromatic complexes, including Zhejiang Petroleum & Chemical's 11.8 million-ton facility, providing substantial toluene feedstock supply. The region's processors utilize export-oriented regulations and integrated logistics networks to optimize distribution channels and reduce operational costs. India's expanding pharmaceutical and food-processing sectors increase demand through multiple applications, including preservatives and intermediates, while Japan's technological capabilities enable the production of high-quality grades for electronic coatings and specialized industrial applications. ASEAN countries utilize duty-free trade agreements to establish distribution centers for exports to Europe and North America, integrating the benzoic acid market into regional supply chains and creating value-added opportunities for local manufacturers.

The Middle East and Africa region exhibits the highest growth rate at 6.83% CAGR, supported by increasing urbanization driving demand for preserved food products, beverages, and personal care items, alongside government initiatives attracting polymer manufacturers through tax incentives and infrastructure development. Saudi Arabia's test facilities assess benzoate plasticizers for PVC cable insulation production, supporting domestic manufacturing requirements and reducing import dependency.

North America benefits from FDA regulatory framework and manufacturer preferences for phthalate-free packaging solutions across food, beverage, and consumer goods sectors. Europe's market adapts to Regulation (EU) 2024/3190 on bisphenol limitations, encouraging packaging manufacturers to adopt benzoate alternatives in food contact materials and consumer packaging, while recycling requirements affect cost considerations and material selection processes.

- Lanxess AG

- Eastman Chemical Company

- Wuhan Youji Industry Co., Ltd.

- JQC(Huayin) Pharmaceutical Co., Ltd.

- BASF SE

- I G Petrochemicals Ltd.

- Chemcrux Enterprises Ltd.

- Ganesh Benzoplast Ltd.

- FUSHIMI Pharmaceutical Co., Ltd.

- Jiangsu Sanmu Group Co., Ltd.

- Thermo Fisher Scientific Inc.

- The Merck Group

- Smart Chemicals Group Co., Ltd.

- San Fu Chemical Co., Ltd.

- Mitsui Bussan Chemicals Co., Ltd.

- Spectrum Laboratory Products, Inc.

- Tokyo Chemical Industry Co., Ltd

- Sisco Research Laboratories Pvt Ltd

- Central Drug House (P) Ltd

- Otto Chemie Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory push for longer shelf-life pharmaceuticals in emerging economies

- 4.2.2 Expansion of benzoyl chloride usage in agrochemical synthesis

- 4.2.3 Substitution of phthalate plasticizers with benzoate-based alternatives

- 4.2.4 Growing demand for high-purity benzoic acid for specialty coatings

- 4.2.5 Rise in demand for packaged and convenience foods

- 4.2.6 Technological advancements in production

- 4.3 Market Restraints

- 4.3.1 Shift towards clean-label preservatives limiting synthetic benzoate adoption

- 4.3.2 Price volatality of raw materials

- 4.3.3 Healh and safetu concerns

- 4.3.4 Competition from natural preservatives

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Form

- 5.1.1 Liquid

- 5.1.2 Anhydrous

- 5.1.3 Powder/Crystal

- 5.2 By Purity Grade

- 5.2.1 99.0-99.5%

- 5.2.2 99.5-99.9%

- 5.2.3 Above 99.9%

- 5.3 By Derivative

- 5.3.1 Sodium Benzoate

- 5.3.2 Potassium Benzoate

- 5.3.3 Benzyl Benzoate

- 5.3.4 Benzoyl Chloride

- 5.3.5 Benzoate Plasticizers

- 5.3.6 Other Derivatives

- 5.4 By Application

- 5.4.1 Food and Beverage

- 5.4.1.1 Bakery

- 5.4.1.2 Confectionery

- 5.4.1.3 Dairy

- 5.4.1.4 Beverage

- 5.4.1.5 Sauces and Dressings

- 5.4.1.6 Others

- 5.4.2 Pharmaceuticals

- 5.4.3 Chemicals

- 5.4.4 Personal Care and Cosmetics

- 5.4.5 Animal Feed

- 5.4.6 Others

- 5.4.1 Food and Beverage

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Italy

- 5.5.2.6 Spain

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Lanxess AG

- 6.4.2 Eastman Chemical Company

- 6.4.3 Wuhan Youji Industry Co., Ltd.

- 6.4.4 JQC(Huayin) Pharmaceutical Co., Ltd.

- 6.4.5 BASF SE

- 6.4.6 I G Petrochemicals Ltd.

- 6.4.7 Chemcrux Enterprises Ltd.

- 6.4.8 Ganesh Benzoplast Ltd.

- 6.4.9 FUSHIMI Pharmaceutical Co., Ltd.

- 6.4.10 Jiangsu Sanmu Group Co., Ltd.

- 6.4.11 Thermo Fisher Scientific Inc.

- 6.4.12 The Merck Group

- 6.4.13 Smart Chemicals Group Co., Ltd.

- 6.4.14 San Fu Chemical Co., Ltd.

- 6.4.15 Mitsui Bussan Chemicals Co., Ltd.

- 6.4.16 Spectrum Laboratory Products, Inc.

- 6.4.17 Tokyo Chemical Industry Co., Ltd

- 6.4.18 Sisco Research Laboratories Pvt Ltd

- 6.4.19 Central Drug House (P) Ltd

- 6.4.20 Otto Chemie Pvt. Ltd.