|

시장보고서

상품코드

1844492

폴리머 나노복합재 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Polymer Nanocomposite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

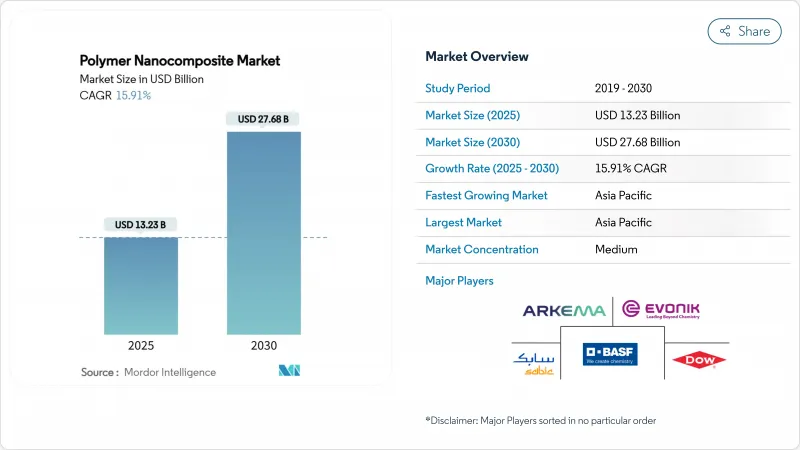

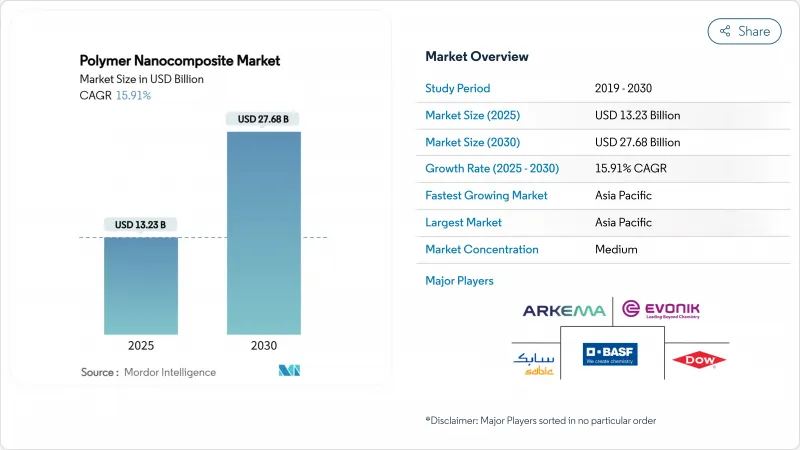

폴리머 나노복합재 시장 규모는 2025년에 132억 3,000만 달러로 평가되었고, 예측기간 중(2025-2030년) CAGR은 15.91%를 나타낼 것으로 예측되며, 2030년에 276억 8,000만 달러에 이를 것으로 예측됩니다.

나노 스케일 충전재가 강도, 열전도율, 차단 성능을 동시에 향상시켜 수요가 가속화되며, 이 소재는 경량 전기차 부품, 고밀도 전자기기, 차세대 포장재의 핵심 소재로 자리매김하고 있습니다. 자동차 프로그램이 단기 물량을 주도하는 한편, 빠르게 성장하는 5G 인프라와 할로겐 프리 난연 규제가 고객 기반을 확대하고 있습니다. 그래핀 및 탄소나노튜브 생산 비용 절감으로 경제성이 개선되고, 아시아태평양 지역의 공급망이 리드타임을 단축하여 성장 모멘텀을 유지할 전망입니다. 재활용 친화적 열가소성 수지 매트릭스에 대한 투자는 폴리머 나노복합재 시장을 순환경제 목표 달성을 위한 선호 솔루션으로 더욱 자리매김할 것입니다.

세계의 폴리머 나노복합재 시장 동향 및 인사이트

식품 및 제약 분야의 고차단성 포장 수요 증가

폴리머 나노복합재는 산소 투과율을 0.1 cc/m2/day 미만으로 낮춰 다층 라미네이트와 동등한 성능을 제공하면서도 필름 두께를 최대 40%까지 줄입니다. 항균성 금속 산화물 나노입자는 유통기한을 연장하여 식품 가공업체들이 화학 방부제에서 능동형 포장 방식으로 전환하도록 유도합니다. 수분에 민감한 의약품도 혜택을 보며, 재활용을 단순화하는 단일층 블리스터 설계를 가능하게 합니다. 나노물질 위험 평가에 관한 FDA 지침은 승인 주기를 단축하고, 라인 통합은 라미네이션 단계를 제거하여 처리량과 폐기물 비율을 개선합니다.

자동차 및 모빌리티 복합재의 경량화 목표

탄소섬유 강화 열가소성 나노복합재는 강철 대비 40%의 중량 절감 효과를 제공하며 자동 섬유 배치 라인을 지원해 대량 생산이 필요한 전기 모빌리티 프로그램과 부합합니다. 재활용성은 전체 수명 주기 경제성을 향상시켜 순환 경제 요구사항을 충족시킵니다. 중량 감소 외에도 나노스케일 충전재는 충돌 에너지 흡수 성능을 강화하고 NVH(소음·진동·거친 느낌)를 저감시켜 얇은 벽체 설계가 가능해집니다. 유럽 OEM 업체들은 2030년까지 20-25%의 중량 감축을 계획 중이며, 이는 수지 및 보강재 투자를 촉진하고 있습니다.

높은 배합 및 분산 비용

높은 종횡비 충전재의 균일한 분포를 위해서는 강화 전단 기능을 갖춘 이축 압출기가 필요하며, 이는 표준 폴리머 대비 가공 비용을 200-400% 증가시킵니다. 나노튜브 응집을 억제하기 위한 기능화 공정은 추가 단계와 라이선스 비용을 발생시킵니다. 건조 분말 및 마스터배치 방식은 설비 투자 비용을 낮추지만 공급망 복잡성을 증가시킵니다. 규모의 경제가 실현되기 전까지는 가격 민감도가 높은 포장재 및 소비재 시장 진출이 비용 압박으로 제한됩니다.

부문 분석

나노클레이는 저비용과 확립된 필름 압출 노하우를 바탕으로 2024년 폴리머 나노복합재 시장의 38.13% 점유율을 차지했습니다. 차단 성능 향상으로 스낵 포장재의 두께를 5-7 μm까지 줄여도 유통기한을 유지할 수 있습니다. 탄소 나노튜브는 10^3 S/m 전도도로 가격을 상쇄하는 프리미엄 틈새 시장을 차지하는 반면, 금속 산화물 충전재는 자외선 차단, 항균 및 난연 요구를 해결합니다. 그라핀 및 나노다이아몬드 등급의 확장성으로 전자파 차폐 및 열 경로가 가능해지면서 기타 충전재 카테고리는 19.44%의 연평균 성장률(CAGR)을 기록했습니다. 이러한 추세들은 단일 충전재의 지배보다는 제형 다양성의 확대를 시사합니다.

지역 분석

2024년 아시아태평양 지역의 폴리머 나노복합재 시장 점유율 40.35%는 깊은 제조 생태계와 적극적인 국가 프로그램을 반영합니다. 중국의 그래핀 나노튜브 생산 규모는 비용 곡선을 압축하는 반면, 인도의 적층 제조 로드맵은 글로벌 시장 점유율 5%를 목표로 하여 하류 수요를 자극합니다. 일본은 지속가능성과 고탄성을 결합한 셀룰로오스 나노섬유 파일럿 프로젝트에 투자하여 가전 및 자동차 1차 공급업체를 유치하고 있습니다.

북미는 자동차 경량화 법규와 항공우주 인증 파이프라인을 활용합니다. USMCA 무역 체제는 복합 펠릿의 국경 간 공급을 용이하게 하여 멕시코에서 조립되지만 미국에서 판매되는 차량 플랫폼을 지원합니다. 유럽은 엄격한 환경·보건·안전(EHS) 규정과 순환경제 목표를 결합하여 건축 패널 및 철도 내장재에 할로겐 프리 나노복합재 채택을 가속화합니다. 중동 및 아프리카는 친환경 건축 규정과 석유화학 다각화를 통해 수요를 창출하는 반면, 남미의 진전은 브라질 포장 변환업체와 신생 전기차 부품 라인에 달려 있습니다. 종합적으로 지역별 차별화는 예측 기간 동안 폴리머 나노복합재 시장의 균형 잡힌 확장을 보장합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 식품 및 제약 분야의 고차단 포장 수요 증가

- 자동차 및 모빌리티 복합재의 경량화 목표

- 5G 및 전력 전자 분야의 열 관리 요구

- 난연성, 무할로겐 재료에의 규제 강화

- 전기차용 배터리 하우징 소재

- 시장 성장 억제요인

- 높은 배합 및 분산 비용

- 나노독성/환경·보건·안전(EHS) 규정 준수 불확실성

- 그래핀 및 탄소나노튜브(CNT) 공급 확대 과제

- 밸류체인 분석

- 기술적 전망

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

- 특허 분석

제5장 시장 규모와 성장 예측

- 충전재 유형별

- 탄소 나노튜브

- 금속 산화물

- 나노클레이

- 나노섬유

- 기타 충전재

- 폴리머 매트릭스별

- 열가소성 플라스틱

- 열경화성 수지

- 바이오 기반 폴리머

- 최종 사용자 산업별

- 자동차

- 포장

- 항공우주 및 방위

- 전기 및 전자

- 에너지 및 저장

- 기타 최종 사용자 산업

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 이집트

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- 3D Systems Inc.

- Altana

- Arkema

- AxiPolymer Inc.

- BASF

- Birla Carbon

- Dow

- DuPont

- Evonik Industries AG

- Foster, LLC

- Hybrid Plastics Inc.

- Inframat Corporation

- Mitsubishi Chemical Group Corporation

- Nanocyl SA

- Powdermet Inc.

- RTP Company

- SABIC

- ShayoNano Singapore Private Ltd.

- Solesence

- Sumitomo Chemical Co. Ltd.

- TORAY INDUSTRIES, INC.

제7장 시장 기회와 전망

HBR 25.11.03The Polymer Nanocomposite Market size is estimated at USD 13.23 billion in 2025, and is expected to reach USD 27.68 billion by 2030, at a CAGR of 15.91% during the forecast period (2025-2030).

Demand accelerates as nanoscale fillers unlock simultaneous gains in strength, thermal conductivity, and barrier performance, making the material central to lightweight electric-vehicle parts, high-density electronics, and next-generation packaging. Automotive programs anchor near-term volumes, while fast-moving 5G infrastructure and halogen-free flame-retardant regulations broaden the customer base. Cost-down progress in graphene and carbon-nanotube production improves economics, and regional supply chains in Asia-Pacific shorten lead times, sustaining momentum. Investments in recycling-friendly thermoplastic matrices further position the polymer nanocomposites market as a preferred solution for circular-economy goals.

Global Polymer Nanocomposite Market Trends and Insights

Growing Demand for High-Barrier Packaging in Food and Pharma

Polymer nanocomposites lower oxygen transmission below 0.1 cc/m2/day, matching multilayer laminates while cutting film thickness by up to 40%. Antimicrobial metal-oxide nanoparticles extend shelf life, so food processors shift from chemical preservatives to active-packaging formats. Moisture-sensitive pharmaceuticals also benefit, allowing single-layer blister designs that simplify recycling. FDA guidance on nanomaterial risk assessment shortens approval cycles, and line integration eliminates lamination steps, improving throughput and waste ratios.

Lightweighting Targets in Automotive and Mobility Composites

Carbon-fiber-reinforced thermoplastic nanocomposites yield 40% mass savings versus steel and support automated fiber-placement lines, aligning with high-volume e-mobility programs. Recyclability boosts total-life economics, meeting circular mandates. Beyond mass reduction, nanoscale fillers enhance crash energy absorption and damp NVH, enabling thin-wall designs. European OEMs plan 20-25% weight cuts by 2030, catalyzing resin and reinforcement investment.

High Compounding and Dispersion Costs

Uniform distribution of high-aspect-ratio fillers demands twin-screw extruders with intensified shear, adding 200-400% to processing cost versus standard polymers. Functionalization to curb nanotube agglomeration introduces extra steps and licensing fees. Dry-powder and masterbatch routes lower capex but widen supply-chain complexity. Cost pressure limits penetration into price-sensitive packaging and consumer goods until scale economies materialize.

Other drivers and restraints analyzed in the detailed report include:

- Thermal Management Needs in 5G and Power Electronics

- Regulatory Push for Flame-Retardant, Halogen-Free Materials

- Nanotoxicity/EHS Compliance Uncertainty

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Nanoclay held 38.13% polymer nanocomposites market share in 2024 on the strength of low cost and established film-extrusion know-how. Barrier gains allow 5-7 µm downgauging in snack packaging without compromising shelf life. Carbon nanotubes occupy premium niches where 10^3 S/m conductivity offsets price, while metal-oxide fillers address UV, antimicrobial, and flame-retardant needs. The other-filler category captures 19.44% CAGR as scalable graphene and nanodiamond grades unlock EMI shielding and thermal paths. Combined, these trends suggest widening formulation diversity rather than one-filler dominanc.

The Polymer Nanocomposites Market Report is Segmented by Filler Type (Carbon Nanotube, Metal Oxide, Nanoclay, and More), Polymer Matrix (Thermoplastics, Thermosets, and Bio-Based Polymers), End-User Industry (Automotive, Packaging, Aerospace and Defense, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific's 40.35% polymer nanocomposites market share in 2024 mirrors deep manufacturing ecosystems and proactive state programs. China's scale in graphene nanotube production compresses cost curves, while India's additive-manufacturing roadmap targets a 5% global stake, stimulating downstream demand. Japan funds cellulose nanofiber pilots that blend sustainability with high modulus, drawing appliance and auto tier-ones.

North America leverages automotive lightweighting legislation and aerospace certification pipelines. The USMCA trade framework eases cross-border supply of compounded pellets, aiding vehicle platforms assembled in Mexico yet sold in the United States. Europe couples stringent EHS rules with circular-economy targets, accelerating halogen-free nanocomposite adoption in building panels and rail interiors. The Middle East and Africa open pockets of demand through green-building codes and petrochemical diversification, while South America's progress hinges on Brazilian packaging converters and nascent EV component lines. Collectively, regional differentiation ensures balanced expansion for the polymer nanocomposites market over the forecast horizon.

- 3D Systems Inc.

- Altana

- Arkema

- AxiPolymer Inc.

- BASF

- Birla Carbon

- Dow

- DuPont

- Evonik Industries AG

- Foster, LLC

- Hybrid Plastics Inc.

- Inframat Corporation

- Mitsubishi Chemical Group Corporation

- Nanocyl SA

- Powdermet Inc.

- RTP Company

- SABIC

- ShayoNano Singapore Private Ltd.

- Solesence

- Sumitomo Chemical Co. Ltd.

- TORAY INDUSTRIES, INC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for High-Barrier Packaging in Food and Pharma

- 4.2.2 Lightweighting Targets in Automotive and Mobility Composites

- 4.2.3 Thermal Management Needs in 5G and Power Electronics

- 4.2.4 Regulatory Push for Flame-Retardant, Halogen-Free Materials

- 4.2.5 Battery-Housing Materials for Electric Vehicles

- 4.3 Market Restraints

- 4.3.1 High Compounding and Dispersion Costs

- 4.3.2 Nanotoxicity/EHS Compliance Uncertainty

- 4.3.3 Scale-Up Challenges for Graphene and CNT Supply

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

- 4.7 Patent Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Filler Type

- 5.1.1 Carbon Nanotube

- 5.1.2 Metal Oxide

- 5.1.3 Nanoclay

- 5.1.4 Nanofiber

- 5.1.5 Other Filler Types

- 5.2 By Polymer Matrix

- 5.2.1 Thermoplastics

- 5.2.2 Thermosets

- 5.2.3 Bio-based Polymers

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Packaging

- 5.3.3 Aerospace and Defense

- 5.3.4 Electrical and Electronics

- 5.3.5 Energy and Storage

- 5.3.6 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3D Systems Inc.

- 6.4.2 Altana

- 6.4.3 Arkema

- 6.4.4 AxiPolymer Inc.

- 6.4.5 BASF

- 6.4.6 Birla Carbon

- 6.4.7 Dow

- 6.4.8 DuPont

- 6.4.9 Evonik Industries AG

- 6.4.10 Foster, LLC

- 6.4.11 Hybrid Plastics Inc.

- 6.4.12 Inframat Corporation

- 6.4.13 Mitsubishi Chemical Group Corporation

- 6.4.14 Nanocyl SA

- 6.4.15 Powdermet Inc.

- 6.4.16 RTP Company

- 6.4.17 SABIC

- 6.4.18 ShayoNano Singapore Private Ltd.

- 6.4.19 Solesence

- 6.4.20 Sumitomo Chemical Co. Ltd.

- 6.4.21 TORAY INDUSTRIES, INC.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment