|

시장보고서

상품코드

1844527

장식 콘크리트 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Decorative Concrete - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

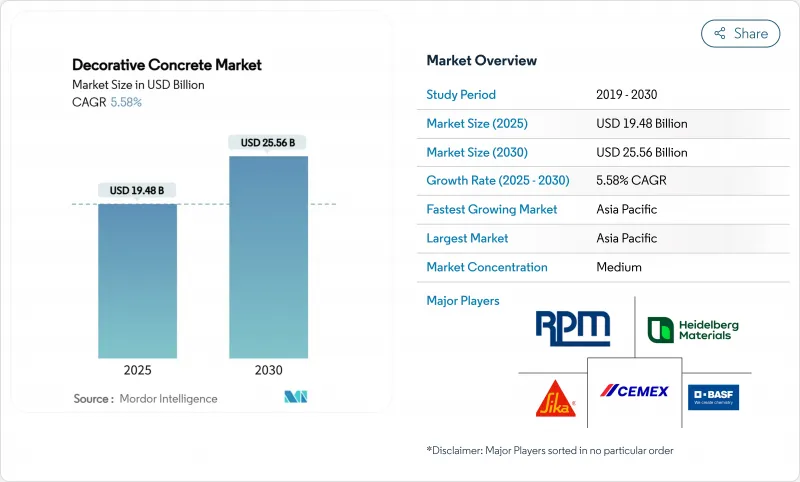

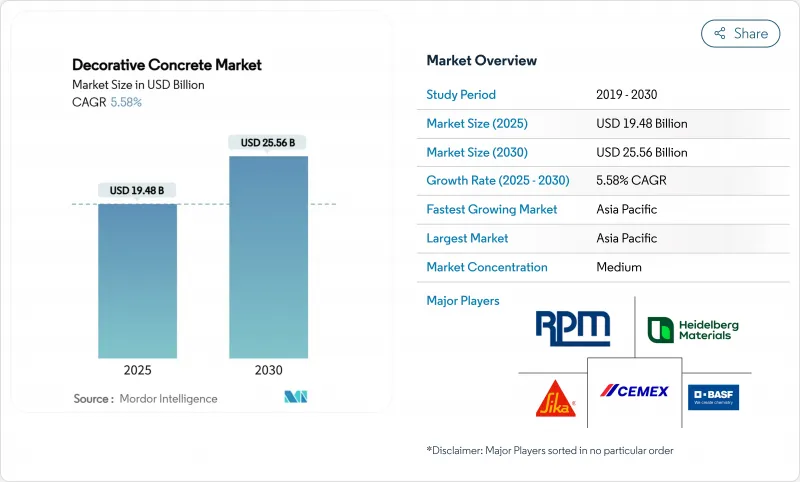

2025년 장식 콘크리트 시장 규모는 194억 8,000만 달러로 평가되었고, 예측 기간(2025-2030년)의 CAGR은 5.58%를 나타낼 것으로 예측되며, 2030년에 255억 6,000만 달러에 달할 전망입니다.

이러한 지속적인 성장은 장기적인 내구성과 디자인 유연성을 겸비한 소재로 글로벌 건설 우선순위가 결정적으로 전환되고 있음을 반영합니다. 특히 주거용 리모델링 예산이 높은 수준을 유지하고 상업 시설의 현대화가 지속되면서 더욱 두드러집니다. 팬데믹 이후 증가한 주택 개조 지출, 평균 연령 41년의 노후화된 주택 재고, 그리고 유지보수가 적은 마감재에 대한 선호도 증가가 수요를 강화하고 있습니다. 이와 동시에 상업용 리모델링에서는 보행 내구성 목표를 충족시키기 위해 광택 처리 및 스탬프 콘크리트를 채택하고 있으며, 탄소중립 건물 의무화는 생물 기반 혼합제와 저휘발성 유기화합물(VOC) 혼합재로 생산자들을 이끌고 있습니다. 수입 시멘트에 대한 관세와 불안정한 안료 공급은 비용 압박을 가중시키지만, 동시에 수직 통합 공급업체와 탄소 저감 제형 혁신 기업들에게 기회를 열어주고 있습니다.

세계의 장식 콘크리트 시장 동향 및 인사이트

팬데믹 이후 증가하는 주거용 리모델링 및 리노베이션 지출

리모델링 예산 증가는 더 적은 수의 고가치 프로젝트로 전환되며, 미적 요소와 긴 수명을 결합한 표면 업등급 수요를 강화하고 있습니다. 전체 프로젝트 규모가 일시적으로 감소했음에도 2023년 평균 주택 소유자 지출은 12% 증가하여, 자산 가치를 높이고 노후 대비 주거 환경을 지원하는 프리미엄 마감재에 대한 지불 의사를 시사합니다. 장식용 콘크리트는 20-30년의 수명으로 대체 포장재보다 우수하여 향후 보수 주기를 제한합니다는 점에서 적합합니다. 노후화된 주택 재고는 스탬프 슬래브와 폴리싱 바닥이 빠른 시각적 효과를 제공하는 광범위한 실외 및 지하실 리모델링을 촉진합니다. 2025년 중반까지 5.5%로 향하는 모기지 금리는 리모델링 자금 조달을 더욱 활성화하여 예측 기간 내 수요를 증폭시킬 것입니다.

신축 실외 생활 공간에서의 스탬프 콘크리트 선호도

스탬핑 매트와 일체형 착색 기술의 발전으로 스탬프 표면에 대한 구식 인식이 사라졌으며, 적절한 밀봉 시 20년 이상 지속되는 자연스러운 질감을 구현할 수 있게 되었습니다. 단위 설치 비용은 채석 석재 대비 유리한 가격 차이를 유지하여 시공사가 더 넓은 인구층을 대상으로 할 수 있게 합니다. 쿨톤 안료와 기하학적 템플릿은 현대적 조경 트렌드와 부합하며, 투수성 변형 제품은 밀집된 도시 프로젝트의 우수 처리 규정을 충족시킨다. 통합 LED 채널과 금속성 하이라이트는 프리미엄 설치의 차별화 요소로, 특히 수영장 데크 주변에서 표면 온도 저하와 미끄럼 방지 기능으로 안전성을 높입니다.

특수 안료, 몰드 및 실러의 높은 초기 비용

장식용 콘크리트는 표준 혼합물(100-150달러/입방야드) 대비 200-300달러/입방야드의 가격을 형성하며, 이 차이는 고가의 산화철 안료, 실리콘 몰드, 다층 실링 시스템에 기인합니다. 시공사는 이러한 비용을 주택 소유자와 소규모 개발자에게 전가하여 가격 민감 지역에서의 도입을 저해합니다. 스탬핑 또는 폴리싱 마감은 더 느린 시공 속도와 전문적인 마감 기술이 필요하기 때문에 인건비도 추가로 발생합니다. 소규모 시공사는 독점 스탬프 라이브러리나 다이아몬드 연마 장비 구매를 주저하여 2선 도시에서의 서비스 가용성을 제한하고 농촌 지역 진출을 늦추고 있습니다.

부문 분석

스탬프 콘크리트는 진입로, 파티오, 상업 광장 등 다양한 적용 가능성 덕분에 2024년 장식용 콘크리트 시장 점유율 40.21%를 유지했습니다. 향상된 도구 라이브러리는 슬레이트, 목재, 심지어 통합 로고 인상을 제공하여 계약업체가 호텔 및 브랜드 소매 체인을 유치할 수 있게 합니다. 폴리싱 콘크리트는 기반이 작지만, 시설 관리자들이 지게차 마모에 강하고 청소 절차를 용이하게 하는 매끄러운 바닥을 선호함에 따라 2030년까지 6.19%의 연평균 성장률(CAGR)로 성장할 것으로 예상됩니다. 장식용 콘크리트 시장 규모는 구조물 철거 없이 표면 수명을 연장하는 오버레이와 미세 균열을 봉합해 유지보수 주기를 연장하는 신개념 자가 치유 캡슐 기술의 부상으로 혜택을 보고 있습니다. 전반적으로 다양한 유형 옵션은 공급업체가 예산과 성능 요구사항을 모두 충족하도록 지원하여 장식용 콘크리트 시장의 회복탄력성을 강화합니다.

지속적인 연구개발은 색상 변색 방지 염료와 작업 주기를 단축하는 신속 경화형 실러 개발을 목표로 합니다. 유색 혼합물은 줄무늬 현상을 방지하기 위해 미세한 안료 분산을 활용하는 반면, 반투명 염료 시스템은 부티크 공간에서 선호되는 예술적 그라데이션을 구현합니다. 섬유 보강 설계는 수축 균열을 완화하고, 자외선 차단 탑코트는 야외 엔터테인먼트 공간에서의 퇴색을 방지합니다. 이러한 발전들은 종합적으로 적용 사례를 확대하고 가시성이 높은 건축 요소에 대한 침투를 심화시켜 장기간 장식용 콘크리트 시장 성장을 뒷받침합니다.

지역 분석

아시아태평양 지역은 2024년 매출의 37.83%를 차지했으며, 2030년까지 6.53%의 연평균 복합 성장률(CAGR)을 기록하며 시장 선도자이자 주요 성장 동력이라는 이중 역할을 강화하고 있습니다. 중국은 2011-2013년 사이 6.6기가톤의 시멘트를 소비하여 20세기 미국 사용량을 압도했으며, 여전히 전 세계 생산량의 절반 이상을 차지합니다. 대규모 주택 이전 계획과 인도네시아의 50억 달러 규모 산업단지 같은 메가 프로젝트는 구조적 수요를 부각시키며, 투수성 장식 슬래브는 급속히 도시화되는 도시들의 엄격한 우수 처리 규정에 대응합니다. 국내 생산자들은 국가적 탈탄소화 공약에 부합하기 위해 저클링커 결합제 생산을 확대하며 제품 포트폴리오를 다양화하고 수입 의존도를 낮추고 있습니다.

북미는 2025년 이후 수입 관세로 인해 비용 변동성이 두드러지지만, 모기지 금리 완화와 지속적인 공공 부문 지출에 힘입어 성장 잠재력을 유지합니다. 노후화된 주택 재고는 주거용 재포장 수요를 촉진하며, 양당 합의 인프라 법안은 공공 광장과 교통 허브에서의 기회를 확대합니다. 공급망 역풍으로 통합 공급업체들은 자사 채석장 및 터미널 역량 확장을 통해 원자재 확보와 장식용 콘크리트 시장 가격 안정화를 도모하고 있습니다.

유럽의 엄격한 탄소 지침은 저탄소 함유 재료로 규격을 재조정하여 바이오 기반 혼합제 및 재생 골재 채택을 촉진합니다. 폐열 회수 가마 및 바이오숯 혼소 기술에 투자하는 생산자들은 EU 분류 체계 규정에 따른 조달 우대 혜택을 얻어 지역 경쟁 우위를 강화하고 있습니다. 한편 중동, 아프리카, 남미 지역은 도시 인구 증가에 힘입어 꾸준한 성장을 기록하고 있으나, 통화 변동성과 제한된 시공업체 역량이 당장의 상승 잠재력을 제약하고 있습니다. 전 지역에서 장식용 콘크리트 시장은 지역 정책 요구사항 및 건설 부문 사이클에 부응할 수 있는 역량을 보여주며 광범위한 수요 기반을 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 팬데믹 이후 주거용 리모델링 및 리노베이션 지출 증가

- 신축 실외 생활 공간에서 스탬프 콘크리트 선호도

- 탄소중립 및 친환경 건축 인증으로 인한 컬러/저 VOC 혼합물 수요 증가

- 신속 리모델링 프로젝트에서의 장식용 콘크리트 오버레이 성장

- 내재 탄소 발자국 감소를 위한 바이오 기반 혼합제 채택

- 시장 성장 억제요인

- 특수 안료, 몰드 및 실러의 높은 초기 비용

- 시멘트 및 안료 공급망 변동성으로 인한 가격 상승

- 인증된 장식용 콘크리트 시공자 부족

- 밸류체인 분석

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 유형별

- 스탬프 콘크리트

- 연마 콘크리트

- 오버레이 콘크리트

- 스테인 콘크리트

- 착색 콘크리트

- 콘크리트 염색

- 기타 유형

- 용도별

- 보도와 진입로

- 파티오

- 수영장 데크

- 바닥

- 벽

- 기타 용도

- 최종 사용자 산업별

- 주거용

- 비주거용

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- 3M

- BASF

- Boral

- CEMEX SAB de CV

- Dex-O-Tex

- Elite Crete Systems

- Heidelberg Materials

- Holcim

- Palermo Concrete Inc

- Parchem Construction Supplies

- PPG Industries Inc

- RPM International Inc.

- Saint-Gobain

- Sika AG

- Subana Technologies Pvt. Ltd.

- Tarmac

- The Euclid Chemical Company

- The Sherwin-Williams Company

- UltraTech Cement Ltd.

제7장 시장 기회와 전망

HBR 25.11.03The Decorative Concrete Market size is estimated at USD 19.48 billion in 2025, and is expected to reach USD 25.56 billion by 2030, at a CAGR of 5.58% during the forecast period (2025-2030).

This sustained expansion reflects a decisive shift in global construction priorities toward materials that marry long-term durability with design versatility, especially as residential remodeling budgets remain elevated and commercial facilities continue to modernize. Heightened post-pandemic home-improvement outlays, an aging housing stock with a median age of 41 years, and growing preference for low-maintenance surfaces are reinforcing demand. In parallel, commercial refurbishments are adopting polished and stamped concrete to meet foot-traffic durability targets, while net-zero building mandates push producers toward bio-based admixtures and low-VOC mixes. Tariffs on imported cement, coupled with volatile pigment supply, amplify cost pressures but also open opportunities for vertically integrated suppliers and innovators in carbon-reduced formulations.

Global Decorative Concrete Market Trends and Insights

Rising Residential Remodeling and Refurbishment Spend Post-Pandemic

Elevated remodeling budgets have shifted toward fewer but higher-value projects, strengthening demand for surface upgrades that combine aesthetics with long service life. Average homeowner spend increased 12% in 2023 despite a brief dip in overall project volume, signaling a willingness to pay for premium finishes that raise property value and support aging-in-place needs. Decorative concrete aligns well because its 20-30-year life span outperforms many alternative pavements, limiting future repair cycles. An aging housing stock motivates extensive outdoor and basement renovations where stamped slabs and polished floors deliver quick visual impact. Mortgage rates trending toward 5.5% by mid-2025 should further unlock renovation funding, amplifying demand throughout the forecast window.

Preference for Stamped Concrete in New-Build Outdoor Living Spaces

Advances in stamping mats and integral coloring have dispelled dated perceptions of stamped surfaces and now enable convincingly natural textures that last beyond two decades when properly sealed. Unit installation costs retain a favorable spread versus quarried stone, enabling contractors to target broader demographic segments. Cool-tone pigments and geometric templates resonate with modern landscaping trends while permeable variants address storm-water mandates in dense urban projects. Integrated LED channels and metallic highlights differentiate premium installations, particularly around pool decks where cooler surface temperatures and slip resistance improve safety.

High Upfront Cost of Specialty Pigments, Molds and Sealers

Decorative concrete commands USD 200-300 per cubic yard against USD 100-150 for standard mixes, a gap driven by expensive iron-oxide pigments, silicone molds, and multi-layer sealing systems. Contractors pass these costs to homeowners and small developers, curbing uptake in price-sensitive regions. Labor premiums also arise because stamped or polished finishes require slower placement rates and specialized finishing skills. Smaller contractors hesitate to purchase proprietary stamp libraries or diamond-polishing equipment, limiting service availability in secondary cities and slowing rural penetration.

Other drivers and restraints analyzed in the detailed report include:

- Net-Zero and Green-Building Certification Pushing Colored/Low-VOC Mixes

- Growth of Decorative Concrete Overlays in Fast-Track Renovation Projects

- Volatility in Cement and Pigment Supply Chains Inflating Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Stamped concrete retained a 40.21% decorative concrete market share in 2024, underpinned by its adaptability across driveways, patios, and commercial plazas. Enhanced tool libraries offer slate, timber, and even integrated logo impressions, enabling contractors to court hospitality and branded retail chains. Polished concrete, while holding a smaller base, is forecast to grow at a 6.19% CAGR to 2030 as facility managers appreciate seamless floors that resist forklift abrasion and ease cleaning protocols. Decorative concrete market size benefits from overlays that extend surface life without structural demolition, and from emerging self-healing capsules that release lime to seal microcracks and prolong service intervals. Overall, diversified type options help suppliers meet both budget and performance briefs, reinforcing the decorative concrete market's resilience.

Continued R&D targets color-fast dyes and rapid-cure sealers that shorten turnover cycles. Colored mixes leverage finer pigment dispersions to avoid streaking, whereas translucent dye systems permit artistic gradients favored in boutique venues. Fiber-reinforced designs alleviate shrinkage cracking, while UV-resistant topcoats guard against fade in open-air entertainment spaces. Collectively, these advances widen use cases and deepen penetration into high-visibility architectural elements, bolstering long-term decorative concrete market growth.

The Decorative Concrete Market Report is Segmented by Type (Stamped Concrete, Polished Concrete, Concrete Overlay, Stained Concrete, Colored Concrete, Concrete Dye, Other Types), Application (Footpath and Driveway, Patio, and More), End-User Industry (Residential, Non-Residential), and Geography (Asia-Pacific, North America, Europe, and More ). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 37.83% of 2024 revenue and posts a leading 6.53% CAGR to 2030, reinforcing its dual role as market leader and primary growth driver. China alone consumed 6.6 gigatons of cement between 2011-2013, dwarfing 20th-century U.S. usage, and still accounts for more than half of global output. Massive housing-relocation schemes and megaprojects such as Indonesia's USD 5 billion industrial park underscore structural demand, while permeable decorative slabs respond to stringent storm-water ordinances in rapidly urbanizing cities. Local producers are scaling low-clinker binders to align with national decarbonization pledges, broadening the product mix and tempering import dependence.

North America faces pronounced cost volatility after 2025 import tariffs but retains growth potential supported by mortgage-rate easing and continued public-sector outlays. An aging housing stock boosts residential resurfacing, while the Bipartisan Infrastructure Law extends opportunities in public plazas and transit hubs. Supply-chain headwinds encourage integrated suppliers to expand captive quarry and terminal capacity, securing raw materials and stabilizing decorative concrete market pricing.

Europe's stringent carbon directives recalibrate specifications toward low-embodied materials, catalyzing uptake of bio-based admixtures and recycled aggregates. Producers investing in waste-heat recovery kilns and bio-char co-firing earn procurement preference under EU Taxonomy rules, reinforcing regional competitive advantages. Meanwhile, Middle East, Africa, and South America register steady gains anchored by urban population growth, though currency volatility and limited installer capacity temper immediate upside potential. Across all regions the decorative concrete market demonstrates capacity to align with local policy imperatives and construction-sector cycles, sustaining a broad demand base.

- 3M

- BASF

- Boral

- CEMEX S.A.B. de C.V.

- Dex-O-Tex

- Elite Crete Systems

- Heidelberg Materials

- Holcim

- Palermo Concrete Inc

- Parchem Construction Supplies

- PPG Industries Inc

- RPM International Inc.

- Saint-Gobain

- Sika AG

- Subana Technologies Pvt. Ltd.

- Tarmac

- The Euclid Chemical Company

- The Sherwin-Williams Company

- UltraTech Cement Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising residential remodeling and refurbishment spend post-pandemic

- 4.2.2 Preference for stamped concrete in new-build outdoor living spaces

- 4.2.3 Net-zero and green-building certification pushing colored/low-VOC mixes

- 4.2.4 Growth of decorative concrete overlays in fast-track renovation projects

- 4.2.5 Adoption of bio-based admixtures to cut embodied-carbon footprint

- 4.3 Market Restraints

- 4.3.1 High upfront cost of specialty pigments, molds and sealers

- 4.3.2 Volatility in cement and pigment supply chains inflating prices

- 4.3.3 Shortage of certified decorative concrete installers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Stamped Concrete

- 5.1.2 Polished Concrete

- 5.1.3 Concrete Overlay

- 5.1.4 Stained Concrete

- 5.1.5 Colored Concrete

- 5.1.6 Concrete Dye

- 5.1.7 Other Types

- 5.2 By Application

- 5.2.1 Footpath and Driveway

- 5.2.2 Patio

- 5.2.3 Pool Deck

- 5.2.4 Floor

- 5.2.5 Wall

- 5.2.6 Other Applications

- 5.3 By End-user Industry

- 5.3.1 Residential

- 5.3.2 Non-residential

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 BASF

- 6.4.3 Boral

- 6.4.4 CEMEX S.A.B. de C.V.

- 6.4.5 Dex-O-Tex

- 6.4.6 Elite Crete Systems

- 6.4.7 Heidelberg Materials

- 6.4.8 Holcim

- 6.4.9 Palermo Concrete Inc

- 6.4.10 Parchem Construction Supplies

- 6.4.11 PPG Industries Inc

- 6.4.12 RPM International Inc.

- 6.4.13 Saint-Gobain

- 6.4.14 Sika AG

- 6.4.15 Subana Technologies Pvt. Ltd.

- 6.4.16 Tarmac

- 6.4.17 The Euclid Chemical Company

- 6.4.18 The Sherwin-Williams Company

- 6.4.19 UltraTech Cement Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment