|

시장보고서

상품코드

1844539

멸균 포장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Sterilized Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

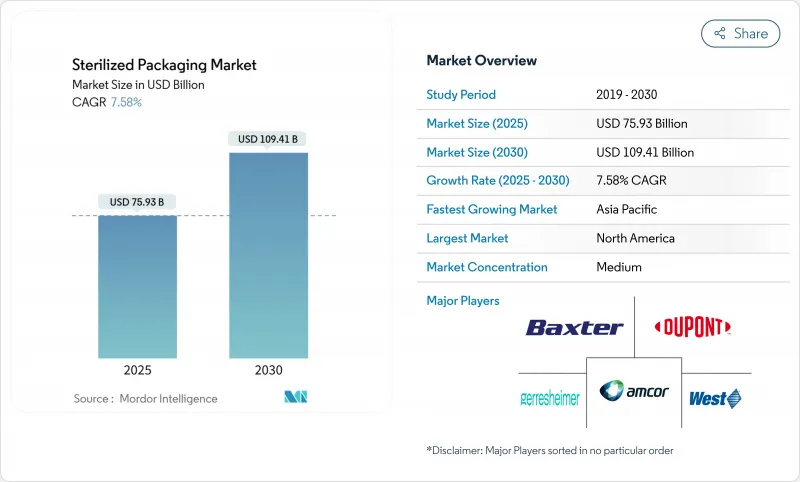

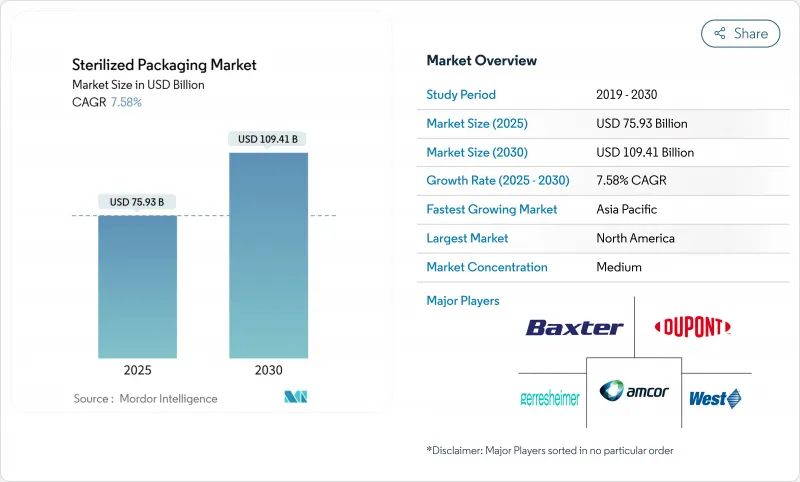

멸균 포장 시장은 2025년에 759억 3,000만 달러에 이르고, 2030년에는 1,094억 1,000만 달러에 달하며, CAGR 7.58%를 나타낼 것으로 예측됩니다.

수요는 세계적인 규제 강화, 생물 제제 제조의 성장, 원내 감염 억제에 대한 압력 증가에 의해 촉진되고 있습니다. 병원 시스템은 단일 사용 팩으로 전환하고 의약품 제조업체는 더 배리어가 높은 형식을 지정하고 장비 제조업체는 리콜 위험을 줄이기 위해 인라인 검사를 통합하려고합니다. EPA(미국 환경보호청)의 새로운 에틸렌 옥사이드(EtO) 배출 규제는 이미 자본을 방사선과 기상의 대체품으로 이동시켰으며, 소재 공급업체는 EU의 PFAS 규제의 다음 파도에 대응하기 때문에 타이벡과 부직포 업그레이드를 급격히 진행하고 있습니다. 세계 기업은 컴플라이언스와 자동화에 필요한 규모를 찾고 통합이 진행되고 있습니다.

세계의 멸균 포장 시장 동향과 인사이트

원내 감염 증가

의료 관련 감염은 미국 병원 환자 중 31명 중 1명이 하루에 감염되어 연간 284억 달러의 손실을 초래합니다. 따라서 병원에서는 중요한 장비의 장벽이 뛰어난 트레이와 멸균 랩의 사용이 의무화되어 있으며, 많은 시설에서는 책임을 줄이기 위해 재사용 가능한 세트를 단일 사용 형식으로 전환하고 있습니다. 단일 사용 멸균 포장 시장 수요는 항생제 내성 유기체에 의해 기존의 세척으로는 불충분 해지고 더욱 높아집니다. 포장 컨버터는 10-6의 무균 보증 수준을 유지하면서 여러 번 ETO 사이클을 견디는 통기성 타이벡 뚜껑 주문이 증가하고 있다고 보고했습니다.

생물 제제 및 주사제의 성장

세계의 생물제제 매출은 2030년까지 8,560억 달러로 향하고 있으며, 주사제 포맷 수요는 미립자를 배출하지 않는 초청정 용기를 필요로 하고 있습니다. 프리필드 주사기 붐을 통해 공급업체는 보다 엄격한 용기 밀폐 시험을 인증해야 하며, 세포 치료 제조업체는 -196℃에서도 완전성을 유지하는 팩이 필요합니다. SCHOTT Pharma의 3억 7,100만 달러를 투자한 미국 주사기 공장은 이러한 치료법을 대상으로 하며 지역 생산 능력 확대가 보다 엄격한 부속서 1 규칙과 어떻게 일치하는지를 보여줍니다.

불안정한 의료 등급 폴리머 가격

의료 등급 수지는 특수 첨가제를 필요로 하고 검증에 시간이 걸리기 때문에 공급업체의 대체가 제한됩니다. 지정학적 혼란과 정유소의 운영 중단은 가격을 급등시키고 이미 비용이 많이 드는 EtO 감소 프로젝트에 직면한 컨버터를 압박하고 있습니다. 여러 지역에서 공급 계약을 체결하고 사내 재활용 능력을 가진 기업은 더 많은 마진을 커버할 수 있습니다.

부문 분석

트레이와 서모폼 팩은 복잡한 기구 세트를 수납할 수 있어 순간적으로 육안 확인할 수 있는 점에서 2024년 멸균 포장 시장에서 26.71%의 점유율을 유지했습니다. 병원은 카운트 인 카운트 아웃 절차를 가속화하고 수술실 지연을 줄이는 투명한 뚜껑을 높이 평가합니다. 맞춤형 캐비티는 제품의 움직임을 억제하고 운송 중 천자 위험을 줄입니다. 블리스터와 앰풀은 2030년까지 연평균 복합 성장률(CAGR)이 9.41%로 가장 급성장하는 제품으로, 오염으로 인해 가치있는 복용량이 손실될 수 있는 단위 용량 생물학적 제형에 의해 지원됩니다.

물집에서 고급 장벽 필름의 추진은 프리미엄화를 보여줍니다. 열성형 라인에 설치된 AI 탑재 카메라는 씰의 무결성을 풀 스피드로 검사해 배치의 수율과 문서화를 향상시킵니다. 파우치, 병, 주입 용기 및 클램쉘은 특정 투여 형태 및 재사용 가능한 기구와 계속 관련이 있지만, 단위 용량 포맷의 보급에 따라 성장은 둔화되고 있습니다. 온도와 방사선 조사를 기록하는 스마트 라벨은 보다 광범위한 디지털화를 반영하여 시험적인 것에서 대규모로 옮겨가고 있습니다.

플라스틱은 강도, 투명성 및 비용이 균형을 이루기 때문에 2024년 멸균 포장 시장 규모의 62.24%를 차지했습니다. 폴리에틸렌, 폴리프로필렌, 환형 올레핀 공중합체는 ETO, 감마선, 전자빔을 견뎌내지만 지속가능성에 대한 규제 증가와 처녀 수지의 인플레이션이 대체를 촉진하고 있습니다. 부직포와 타이벡 기재는 통기성과 섬유 강도가 저잔사 멸균제와의 조합에 도움이 되기 때문에 2030년까지의 CAGR이 9.54%를 나타낼 것으로 예측됩니다.

유리 바이알은 특히 콜드체인의 긴 생물 제제와 같이 약물과 제품의 상호 작용을 0에 가깝게해야하는 경우 필수적입니다. 금속 트레이는 강성 유지 및 차폐 수송을 필요로 하는 정형외과용 임플란트 키트와 같은 작은 틈새를 차지합니다. 생분해성이 중시되는 2차 카톤에서는 판지가 증가하고 있지만, 1차 멸균은 여전히 높은 장벽에 의존하고 있습니다. PFAS의 사용 기한이 가까워짐에 따라 공급업체는 플루오르 수지를 대체하는 플라즈마 코팅 및 산화규소 코팅을 확대하고 있습니다.

지역 분석

북미는 2024년에 멸균 포장 시장 점유율의 33.19%를 차지하며, FDA의 감독과 복잡한 의약품의 상시의 비율의 높이에 지지되었습니다. 대규모 수탁 멸균 네트워크와 주요 수지 제조업체가 공급 안정성을 지원하는 반면, 투자는 EtO 감소와 새로운 전자빔 저장소에 집중하고 있습니다. 벡톤 딕킨슨의 생물학적 제형 부문은 2024년에 10억 달러를 넘어서고, 이 지역이 더 높은 가치의 장비에 기울어져 있음을 부각했습니다.

유럽은 부속서 1의 업그레이드와 PFAS 프리 소재의 조기 채용으로 성숙한 수요로 이어집니다. 독일과 아일랜드에는 세계의 생물 제제 공급망에 공급하는 수많은 충전 마감 공장이 있습니다. EU의 2026년 불소 수지 규제는 대체 코팅의 신속한 인증에 박차를 가하고 유럽의 컨버터를 선발 제조업체에 자리잡고 있습니다. 지속가능성 목표는 재사용 가능한 2차 팩의 순환형 경제 조종사를 뒷받침하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 9.24%로 성장을 지속하고, 중국과 인도가 국내 및 수출 시장용으로 생물학적 제제와 저분자 생산량을 확대하고 있습니다. 각 지역의 규제 당국이 ICH 가이드라인과의 정합화를 진행시켜, 보다 등급이 높은 클린 룸이나 방사선 조사 능력에 대한 투자를 촉구합니다. 고령화가 진행되는 일본에서는 재택치료용 주사기 수요가 높아지고, 한국과 호주는 스마트 라벨의 콜드체인 팩의 테스트 베드가 됩니다. 멸균 포장 시장의 생산 능력을 현지화함으로써 리드 타임을 단축하고 환율을 줄일 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 시장 정의와 조사의 전제

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 원내 감염 증가

- 생물제제와 주사약의 성장

- 세계적으로 엄격한 멸균 규제

- 외래환자 및 재택의료환경 확대

- AI를 활용한 인라인 무균 팩 검사

- 세포 및 유전자 치료의 콜드체인 니즈

- 시장 성장 억제요인

- 불안정한 의료 등급 폴리머 가격

- 에틸렌 옥사이드(EtO) 배출 컴플라이언스 비용

- 의약품 등급의 감마선 조사 능력 한계

- 불소 수지 배리어 필름에 있어서 PFAS 성분 규제 강화

- 가치/공급망 분석

- 중요한 규제 틀의 평가

- 주요 이해관계자의 영향 평가

- 기술적 전망

- Porter's Porter's Five Forces

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

- 거시경제 요인의 영향

제5장 시장 규모와 성장 예측

- 제품별

- 클램쉘

- 파우치

- 병

- 블리스터 및 앰풀

- 바이알

- 트레이 및 열성형 포장

- 정맥 주사 용기 및 백

- 기타

- 재료별

- 플라스틱(HDPE, PP, PET, PVC, 기타)

- 유리

- 금속(알루미늄 호일, 스테인리스 스틸)

- 종이 및 판지

- 부직포 및 타이벡

- 멸균 방법별

- 화학적(에틸렌옥사이드, 오존)

- 방사선(감마선, 전자빔, X선)

- 고온/증기

- 무균 충전 마무리

- 최종 사용자 산업별

- 의료 및 수술 기기

- 제약 및 바이오

- 체외 진단

- 식음료

- 수의학 및 동물 건강

- 기타 산업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장의 집중

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- Amcor plc

- DuPont de Nemours, Inc.

- Baxter International Inc.

- Gerresheimer AG

- SCHOTT AG

- West Pharmaceutical Services, Inc.

- AptarGroup, Inc.

- Tekni-Plex, Inc.

- Sealed Air Corporation

- Sonoco Products Company

- SteriPack Group

- Wipak Group

- Placon Corporation, Inc.

- SGD Pharma

- Becton, Dickinson and Company

- 3M Company

- Berry Global Group, Inc.

- Huhtamaki Oyj

- Sabert Corporation

- Winpak Ltd.

제7장 시장 기회와 앞으로의 동향

- 백스페이스와 미충족 수요(Unmet needs)의 평가

The sterilized packaging market reached USD 75.93 billion in 2025 and is projected to climb to USD 109.41 billion by 2030, expanding at a 7.58% CAGR.

Demand is fueled by stricter global regulations, the growth of biologics manufacturing, and mounting pressure to curb hospital-acquired infections. Hospital systems are switching to single-use packs, pharmaceutical producers are specifying higher barrier formats, and equipment makers are embedding inline inspection to cut recall risks. The EPA's new ethylene-oxide (EtO) emission rules are already shifting capital toward radiation and vapor-phase alternatives, while material suppliers are fast-tracking Tyvek and non-woven upgrades to meet the next wave of EU PFAS limits. Consolidation is picking up as global players seek the scale needed to fund compliance and automation.

Global Sterilized Packaging Market Trends and Insights

Rising Incidence of Hospital-Acquired Infections

Healthcare-associated infections affect 1 in 31 U.S. hospital patients on any day, costing the system USD 28.4 billion annually. Hospitals are therefore mandating higher barrier trays and sterile wraps for critical instruments, and many facilities are shifting reusable sets to single-use formats to mitigate liability. Single-use sterilized packaging market demand rises further as antibiotic-resistant organisms render legacy cleaning inadequate. Packaging converters report growing orders for breathable Tyvek lids that withstand multiple EtO cycles while maintaining a sterility assurance level of 10-6.

Growth in Biologics and Injectable Drugs

Global biologics revenue is moving toward USD 856 billion by 2030, and demand for injectable formats requires ultra-clean containers that do not shed particulates. The prefilled syringe boom is compelling suppliers to certify tougher container-closure tests, while cell-therapy producers need packs that hold integrity at -196 °C. SCHOTT Pharma's USD 371 million U.S. syringe plant targets these therapies and shows how regional capacity expansion aligns with tighter Annex 1 rules.

Volatile Medical-Grade Polymer Prices

Medical-grade resins require specialty additives and lengthy validation, limiting supplier substitution. Geopolitical disruptions and refinery outages have spiked prices, squeezing converters that already face costly EtO abatement projects. Firms with multi-region supply contracts and in-house recycling capacity have more margin cover, whereas single-source buyers risk shortages and expedited-freight expenses.

Other drivers and restraints analyzed in the detailed report include:

- Stringent Global Sterilization Regulations

- Expansion of Outpatient and Home-Care Settings

- Cost of Ethylene Oxide Emission Compliance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Trays and thermoform packs retained a 26.71% share of the sterilized packaging market in 2024 thanks to their ability to nest complex instrument sets and provide instant visual confirmation. Hospitals value clear lids that speed count-in and count-out procedures, reducing operating-room delays. Custom cavities lower product movement, cutting puncture risk in transit. Blisters and ampoules represent the fastest-rising product at a 9.41% CAGR through 2030, supported by unit-dose biologics where contamination can destroy high-value doses.

The push toward advanced barrier films within blisters illustrates premiumization. AI-equipped cameras on thermoform lines inspect seal integrity at full speed, improving batch yield and documentation. Pouches, bottles, IV containers, and clamshells remain relevant for specific dosage forms and reusable instruments, but growth is slower as unit-dose formats gain traction. Smart labels that log temperature or radiation exposure are migrating from trial to scale, reflecting broader digitization.

Plastics still accounted for 62.24% of sterilized packaging market size in 2024 because they balance strength, clarity, and cost. Polyethylene, polypropylene, and cyclic-olefin copolymers withstand EtO, gamma, and e-beam, yet rising sustainability rules and virgin-resin inflation encourage substitution. Non-woven and Tyvek substrates are forecast to rise 9.54% CAGR to 2030 as breathability and fiber strength help them pair with lower-residue sterilants.

Glass vials remain indispensable where drug-product interaction must approach zero, notably for biologics with long cold-chain legs. Metal trays occupy smaller niches such as orthopedic implant kits requiring rigid retention and shielded transport. Paperboard is gaining for secondary cartons where biodegradability is prized, though primary sterility still relies on higher barriers. As PFAS sunset dates approach, suppliers scale up plasma and silicon-oxide coatings to replace fluoropolymers.

The Sterilized Packaging Market Report is Segmented by Product (Clamshells, Pouches, Bottles, Blisters and Ampoules, Vials, and More), Material (Plastics, Glass, Metals, and More), Sterilization Method (Chemical, Radiation, and More), End-User Industry (Medical and Surgical Instruments, Pharmaceutical and Biological, In-Vitro Diagnostics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 33.19% of sterilized packaging market share in 2024, anchored by FDA oversight and a high proportion of complex drug launches. Large contract sterilization networks and leading resin producers underpin supply security, while investment focuses on EtO abatement and new e-beam vaults. Becton Dickinson's biologic-delivery segment surpassed USD 1 billion in 2024, highlighting the region's tilt toward higher-value devices .

Europe follows with mature demand, driven by Annex 1 upgrades and early adoption of PFAS-free materials. Germany and Ireland host numerous fill-finish plants that feed global biologic supply chains. The EU's 2026 fluoropolymer limits spur rapid qualification of alternative coatings, positioning European converters as first movers. Sustainability targets also push circular-economy pilots for reusable secondary packs.

Asia-Pacific posts the fastest 9.24% CAGR to 2030 as China and India scale biologic and small-molecule output for domestic and export markets. Regional regulators are harmonizing with ICH guidelines, prompting investment in higher-grade cleanrooms and radiation capacity. Japan's aging population drives home-care syringe demand, while South Korea and Australia serve as test beds for smart-label cold-chain packs. Localizing sterilized packaging market capacity cuts lead times and cushions currency risk.

- Amcor plc

- DuPont de Nemours, Inc.

- Baxter International Inc.

- Gerresheimer AG

- SCHOTT AG

- West Pharmaceutical Services, Inc.

- AptarGroup, Inc.

- Tekni-Plex, Inc.

- Sealed Air Corporation

- Sonoco Products Company

- SteriPack Group

- Wipak Group

- Placon Corporation, Inc.

- SGD Pharma

- Becton, Dickinson and Company

- 3M Company

- Berry Global Group, Inc.

- Huhtamaki Oyj

- Sabert Corporation

- Winpak Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising incidence of hospital-acquired infections

- 4.2.2 Growth in biologics and injectable drugs

- 4.2.3 Stringent global sterilization regulations

- 4.2.4 Expansion of outpatient and home-care settings

- 4.2.5 AI-enabled inline sterile-pack inspection

- 4.2.6 Cell and gene-therapy cold-chain needs

- 4.3 Market Restraints

- 4.3.1 Volatile medical-grade polymer prices

- 4.3.2 Cost of ethylene oxide (EtO) emission compliance

- 4.3.3 Limited pharma-grade gamma irradiation capacity

- 4.3.4 PFAS scrutiny in fluoropolymer barrier films

- 4.4 Value / Supply-Chain Analysis

- 4.5 Evaluation of Critical Regulatory Framework

- 4.6 Impact Assessment of Key Stakeholders

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Impact of Macro-economic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product

- 5.1.1 Clamshells

- 5.1.2 Pouches

- 5.1.3 Bottles

- 5.1.4 Blisters and Ampoules

- 5.1.5 Vials

- 5.1.6 Trays and Thermoform Packs

- 5.1.7 IV Containers and Bags

- 5.1.8 Others

- 5.2 By Material

- 5.2.1 Plastics (HDPE, PP, PET, PVC, Others)

- 5.2.2 Glass

- 5.2.3 Metals (Aluminum Foil, Stainless Steel)

- 5.2.4 Paper and Paperboard

- 5.2.5 Non-woven and Tyvek

- 5.3 By Sterilization Method

- 5.3.1 Chemical (EtO, Ozone)

- 5.3.2 Radiation (Gamma, e-Beam, X-Ray)

- 5.3.3 High Temperature / Steam

- 5.3.4 Aseptic Fill-Finish

- 5.4 By End-user Industry

- 5.4.1 Medical and Surgical Instruments

- 5.4.2 Pharmaceutical and Biological

- 5.4.3 In-Vitro Diagnostics

- 5.4.4 Food and Beverage

- 5.4.5 Veterinary and Animal Health

- 5.4.6 Other Industrial

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 DuPont de Nemours, Inc.

- 6.4.3 Baxter International Inc.

- 6.4.4 Gerresheimer AG

- 6.4.5 SCHOTT AG

- 6.4.6 West Pharmaceutical Services, Inc.

- 6.4.7 AptarGroup, Inc.

- 6.4.8 Tekni-Plex, Inc.

- 6.4.9 Sealed Air Corporation

- 6.4.10 Sonoco Products Company

- 6.4.11 SteriPack Group

- 6.4.12 Wipak Group

- 6.4.13 Placon Corporation, Inc.

- 6.4.14 SGD Pharma

- 6.4.15 Becton, Dickinson and Company

- 6.4.16 3M Company

- 6.4.17 Berry Global Group, Inc.

- 6.4.18 Huhtamaki Oyj

- 6.4.19 Sabert Corporation

- 6.4.20 Winpak Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-need Assessment