|

시장보고서

상품코드

1844567

제올라이트 분자체 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Zeolite Molecular Sieves - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

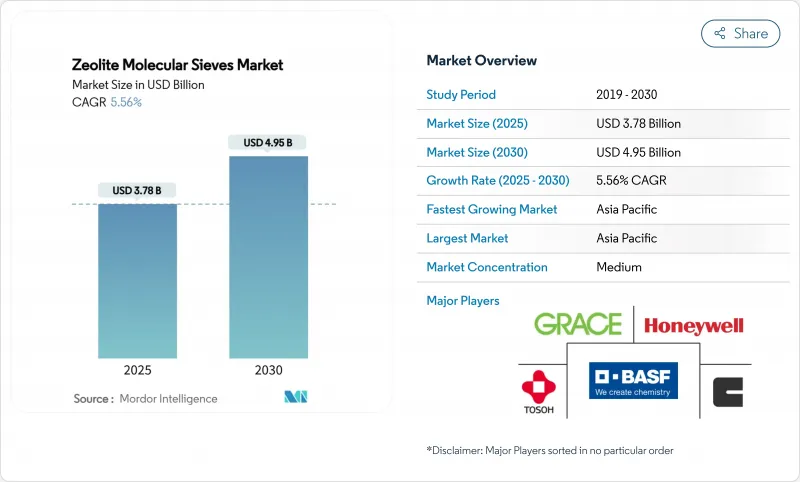

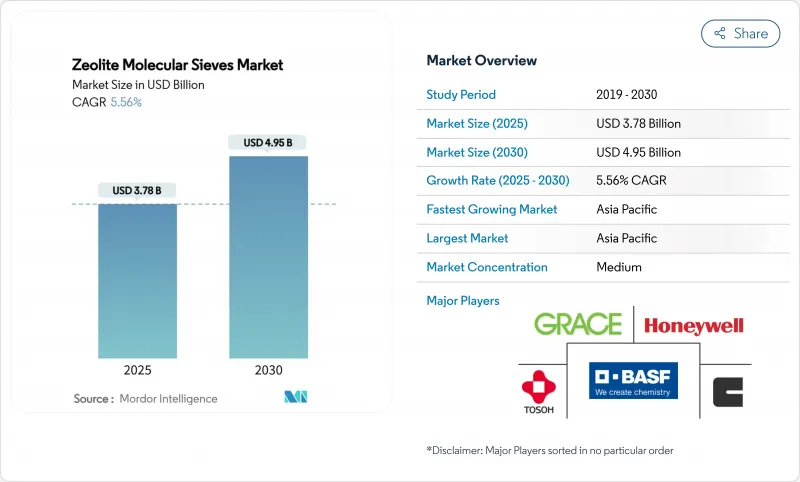

제올라이트 분자체 시장 규모는 2025년에 37억 8,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 5.56%로, 2030년에는 49억 5,000만 달러에 달할 것으로 예상됩니다.

수요 증가는 세제 인산염을 대체하는 환경 규제 강화, 세계 석유화학 콤비나트의 생산 능력 증강, 위생 제품의 이용을 촉진하는 신흥 경제국의 급속한 도시화, 제올라이트 기반의 흡착·촉매 작용에 유리한 저탄소 공업 프로세스의 가속적 추구라는 4가지 구조적인 힘에 지지되고 있습니다. 경쟁사와의 차별화는 기공의 크기, 실리카와 알루미나의 비율, 결정 형태를 특정의 분리나 촉매의 역할에 맞추어 조정하는 독자적인 합성 노하우에 달려 있습니다. 알루미나 및 고순도 실리카 원료의 비용 변동은 마진의 과제가 되고 있지만, 순환형 원료 전략, 특히 석탄 플라이 애쉬 및 기타 산업 잔류물의 전환은 기업의 지속가능성 목표를 지원하면서 원료 위험을 완화하고 있습니다. 탄소 포착과 PFAS 정화의 획기적인 전개는 상업적 프론티어를 확대하고 차세대 환경 시스템에서 활성탄과 아민 용매를 대체하는 실행 가능한 옵션으로 고급 제올라이트 제제를 자리잡고 있습니다.

세계의 제올라이트 분자체 시장 동향과 인사이트

세제의 인산염 금지에 의해 제올라이트로 빌더가 변화

세계의 세제 규제는 부영양화의 위험을 이유로 인산염을 금지하고 있으며, 빌더 수요는 제올라이트 4A로 방향 전환하고 있습니다. 유럽 연합(EU)은 2017년 인산염 사용을 금지하고 연간 250만 톤의 인산염 소비를 줄였습니다. 제올라이트는 현재 분말과 액체 모두에서 그 양의 약 60%를 대체하고 있습니다. 북미에서도 비슷한 규제가 있으며 인도와 브라질에서는 단계적으로 규제가 강화되고 있기 때문에 예측 가능한 수량 성장이 유지되고 있습니다. 제올라이트 4A는 탄산염보다 높은 칼슘 결합능을 나타내므로 경수 지역에서도 세탁 성능을 확보할 수 있습니다. 다국적 세제 브랜드는 제올라이트 빌더를 세계 포트폴리오에 통합하여 기술적으로나 상업적으로 역전할 가능성은 낮습니다. 신흥국은 2027년까지 인산염 프리 규제를 확대할 자세로 제올라이트 분자체 시장의 장기적인 수요 궤도를 강화하고 있습니다.

석유화학 탈수 및 가스 정제 붐

중국, 인도, 사우디아라비아에 걸친 새로운 에틸렌과 프로파일렌의 콤플렉스에 대한 500억 달러를 넘는 투자는 분해가스를 탈수하고 CO2를 100만분의 1레벨까지 제거하는 3A와 4A 분자수 수요를 높이고 있습니다. 세계 규모의 에틸렌 크래커 1기는 초기 충전과 매년 보충으로 500-800톤의 체를 소비합니다. 북미에서의 셰일 가스의 성장은 비재래형 원료의 수분과 산성 가스 부하가 높기 때문에 이 동향을 가속시키고 있습니다. 최근 합성기술의 진보로 물질이송특성이 강화된 보다 큰 제올라이트 결정이 제조되어 재생에너지가 25% 삭감되어 석유화학사업자의 라이프사이클 비용이 절감되었습니다. 그 결과, 제올라이트 분자체 시장은 그린필드 프로젝트와 보다 고순도의 사양을 목표로 한 리노베이션으로부터 증가하는 오프 테이크를 획득하는 태세를 갖추고 있습니다.

세탁용 제제의 효소 및 화학 물질 대체

프리미엄 세제 브랜드는 보다 적은 첨가량으로 동등한 오염 제거 효과를 발휘하는 프로테아제 효소나 리파아제 효소를 선호하게 되어 있어 액체 유형의 제올라이트 함량을 최대 20% 삭감할 수 있습니다. 폴리카르복실산염과 포스폰산염 빌더는 농축액에 쉽게 분산되지만, 제올라이트의 불용성은 가공과 포장을 복잡하게 만듭니다. 액체 세제는 신흥국 시장에서 가장 빠르게 성장하는 카테고리이기 때문에 제올라이트의 사용량은 일류 부문에서 감소할 위험이 있습니다. 그러나 특히 신흥 경제권의 분말 세제와 저가 제품은 경도 제어를 위해 여전히 제올라이트 4A에 의존하고 있으며, 제올라이트 분자체 시장 전체에 미치는 영향을 완화하고 있습니다.

부문 분석

합성 제올라이트 A는 석유화학의 탈수·분리 작업을 위한 세공 직경을 설계하는 정밀한 Si/Al 제어에 의해 2024년에 세계 판매량의 57.89%를 획득했습니다. 비용을 최적화한 수열 합성, 마이크로웨이브 어시스트 합성, 템플릿 프리 합성은 에너지 소비를 35% 삭감하면서 제품의 순도를 계속 증가하고 있습니다. 대조적으로, 천연 클리노프티롤라이트와 모르데나이트 등급은 CAGR 6.12%로 성장하고 있으며, 주로 농업, 악취 방지, 저압수 처리 용도로 성능 대 가격비가 결정의 완성도를 상회하고 있습니다. 튀르키예와 불가리아 천연 광상은 사양에 도달하기 위해 최소한의 이온 교환만을 필요로 하는 광석을 공급하여 30-40%의 비용 우위를 제공합니다. EU의 녹색 거래와 같은 규정은 비 합성 광물에 유리하며 채택을 더욱 촉진하고 있습니다. 미래에 합성 등급은 고압 탈수 및 촉매 작용으로 그 지위를 유지하지만 천연 제올라이트는 환경과 농업의 틈새를 점점 더 주장하고 제올라이트 분자체 시장에서 보완적인 성장 레인을 개척합니다.

제올라이트 분자체 보고서는 원료(천연 제올라이트 및 합성 제올라이트), 최종 사용자 산업(세제, 석유화학 및 정제, 산업 가스 생산, 폐기물 및 수처리, 공기 정화 및 HVAC, 농업 및 동물사료 및 기타 최종 사용자 산업), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 구분됩니다.

지역 분석

아시아태평양은 2024년 세계 매출의 37.56%를 창출했고 CAGR 6.21%를 나타낼 전망입니다. 중국은 에틸렌 크래커와 석탄에서 화학제품으로의 콤플렉스에 대한 투자 선진을 끊고 있으며, 각각 수백 톤의 탈수 분자체를 필요로 합니다. 아시아태평양은 생산 규모, 환경 규범 강화, 대규모 소비자 기반이 융합되어 있으며, 이 지역의 리더십을 견인하고 있습니다. 중국 절강성과 광동성의 에틸렌 프로젝트에서는 수분을 1ppm 미만으로 제거하는 분자체 탈수 유닛이 필요하지만, 현지 폐수 기준에는 암모니아 규제가 부과되어 제올라이트 3차 시스템에 박차가 걸리고 있습니다.

북미는 성숙하지만 기술적으로 풍부한 수요를 보여줍니다. 텍사스의 혈암 가스 처리 공장은 극저온 NGL 회수 전에 수분을 제거하기 위해 3A 분자체를 도입하여 높은 효율과 더 긴 침대 수명을 요구합니다. EPA(미국 환경보호청)의 PFAS 배출에 관한 제안은 퍼플루오로알킬 화합물을 1조분의 1레벨로 포착하는 고실리카 제올라이트의 시험을 가속시켜, 특수 제조업체의 새로운 수익원이 되고 있습니다.

유럽은 지속가능성과 순환성을 선호합니다. 독일과 네덜란드의 공장에서는 상업 규모에서 플라이 애쉬 유래의 제올라이트를 검증해, 버진 광물 루트에 비해 40%의 체적 탄소 삭감을 실현. 중동 및 아프리카는 석유화학의 다양화와 물 부족에 대응합니다. 사우디아라비아의 Vision 2030 수지 설비는 원료 준비를 위한 대형 분자체 타워에 의존합니다. 남아프리카의 광업 부문은 산성 광산 배수의 정화에 크리놉티로라이트를 채택하여 수입 비용을 절감하는 국내 천연 광상의 혜택을 받고 있습니다. 이 지역 개척을 종합하면 제올라이트 분자체 시장의 지리적 캔버스가 확대되고 있는 것을 알 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세제의 인산염 금지에 의한 제올라이트로의 빌더의 변화

- 석유화학 탈수 및 가스 정제 붐

- 엄격한 폐수 배출 규제

- 신흥국에서의 위생 주도의 세제 수요

- 형상 선택성 촉매를 구하는 바이오 정제 변화

- 시장 성장 억제요인

- 세탁 처방에 있어서 효소와 화학물질의 대체물

- 휘발성 알루미나/실리카 원료 가격

- ESG 투자자로부터 의문시되는 고에너지 실적

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 원료별

- 천연 제올라이트

- 합성 제올라이트

- 최종 사용자 산업별

- 세제

- 석유화학 및 정제

- 산업용 가스 생산

- 폐기물 및 수처리

- 공기 정화 및 HVAC

- 농업 및 동물 사료

- 기타 최종 사용자 산업

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- Arkema

- Axens

- BASF

- CLARIANT

- CWK Chemiewerk Bad Kostritz GmbH

- HengYe Inc.

- Honeywell International Inc.

- JIUZHOU CHEMICALS

- KMI Zeolite Inc.

- KNT Group

- KURARAY CO., LTD.

- Luoyang Jalon Micro-Nano New Material

- Sorbchem India Pvt Ltd.

- Tosoh Corporation

- WR Grace & Co.

- Zeochem

- Zeolyst International

제7장 시장 기회와 전망

KTH 25.11.05The Zeolite Molecular Sieves Market size is estimated at USD 3.78 billion in 2025, and is expected to reach USD 4.95 billion by 2030, at a CAGR of 5.56% during the forecast period (2025-2030).

Demand growth is anchored in four structural forces: tightening environmental regulations that substitute phosphates in detergents, capacity additions across global petrochemical complexes, rapid urbanization in emerging economies that drives hygiene product uptake, and the accelerated pursuit of low-carbon industrial processes that favor zeolite-based adsorption and catalysis. Competitive differentiation rests on proprietary synthesis know-how that tailors pore size, silica-to-alumina ratio, and crystal morphology to specific separation or catalytic duties. Cost volatility in alumina and high-purity silica feedstocks poses a margin challenge, but circular feedstock strategies, especially the conversion of coal fly ash and other industrial residues, are mitigating raw-material risk while supporting corporate sustainability goals. Breakthrough deployments in carbon-capture and PFAS remediation are expanding the commercial frontier, positioning advanced zeolite formulations as viable alternatives to activated carbon and amine solvents in next-generation environmental systems

Global Zeolite Molecular Sieves Market Trends and Insights

Phosphate Bans in Detergents Shifting Builders to Zeolites

Global detergent regulations prohibit phosphates because of eutrophication risks, redirecting builder demand toward zeolite 4A. The European Union's 2017 ban eliminated 2.5 million tons of phosphate consumption annually, and zeolites now replace roughly 60% of that volume in both powder and liquid formulations. Similar mandates in North America, along with phased restrictions in India and Brazil, sustain predictable volume growth. Performance advantages compound the regulatory pull: zeolite 4A exhibits higher calcium-binding capacity than carbonates, securing wash performance in hard-water regions. Multinational detergent brands have embedded zeolite builders across their global portfolios, making a reversal technically and commercially unlikely. Emerging economies are poised to expand phosphate-free regulations through 2027, reinforcing the long-run demand trajectory for the zeolite molecular sieve market.

Petrochemical Dehydration and Gas-Purification Boom

Investment exceeding USD 50 billion in new ethylene and propylene complexes across China, India, and Saudi Arabia is elevating demand for 3A and 4A molecular sieves that dehydrate cracked gas and strip CO2 to parts-per-million levels. A single world-scale ethylene cracker consumes 500-800 tons of sieves in initial charging and annual top-ups. Shale-gas growth in North America accelerates the trend, because unconventional feedstocks carry higher moisture and acid-gas loads. Recent synthesis advances have produced larger zeolite crystals with enhanced mass-transfer characteristics, cutting regeneration energy by 25% and reducing lifecycle cost for petrochemical operators. Consequently, the zeolite molecular sieve market is poised to capture incremental offtake from greenfield projects and from revamps that target higher purity specifications.

Enzyme and Chemical Substitutes in Laundry Formulations

Premium detergent brands increasingly favor protease and lipase enzymes that deliver comparable soil removal at lower builder dosage, cutting zeolite content by up to 20% in liquid formats. Polycarboxylate and phosphonate builders disperse easily in concentrated liquids, where zeolite's insolubility complicates processing and packaging. As liquid detergents represent the fastest-growing category in developed markets, zeolite volumes risk erosion in the top-tier segment. Yet powder detergents and value-priced products, particularly in emerging economies, still depend on zeolite 4A for hardness control, mitigating the overall impact on the zeolite molecular sieve market.

Other drivers and restraints analyzed in the detailed report include:

- Stringent Wastewater Discharge Norms

- Hygiene-Driven Detergent Demand in Emerging Economies

- Volatile Alumina/Silica Feedstock Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Synthetic zeolite A captured 57.89% of global volume in 2024 thanks to precise Si/Al control that engineers pore size for petrochemical dehydration and separation tasks. Cost-optimized hydrothermal, microwave-assisted, and template-free syntheses continue to elevate product purity while trimming energy consumption by 35%. In contrast, natural clinoptilolite and mordenite grades are growing at 6.12% CAGR, primarily in agriculture, odor control, and low-pressure water treatment applications where the performance-to-price ratio outranks crystal perfection. Natural deposits in Turkey and Bulgaria deliver ore that requires minimal ion-exchange to reach specification, offering a 30-40% cost edge. Regulatory drivers such as the EU's Green Deal favor non-synthetic minerals, further stimulating adoption. Looking forward, synthetic grades maintain their hold in high-pressure dehydration and catalysis, but natural zeolites increasingly claim environmental and agricultural niches, carving a complementary growth lane within the zeolite molecular sieve market.

The Zeolite Molecular Sieve Report is Segmented by Raw Material (Natural Zeolite and Synthetic Zeolite), End-User Industry (Detergents, Petrochemical and Refining, Industrial Gas Production, Waste and Water Treatment, Air Purification and HVAC, and Agriculture and Animal Feed, Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia Pacific generated 37.56% of global sales in 2024 and is set to grow at a 6.21% CAGR. China spearheads investment in ethylene crackers and coal-to-chemicals complexes, each requiring hundreds of tons of molecular sieves for dehydration duty. Asia Pacific's convergence of production scale, tightening environmental norms, and large consumer bases drives the region's leadership. China's Zhejiang and Guangdong ethylene projects require molecular-sieve dehydration units that remove moisture to below 1 ppm, while local wastewater standards enforce ammonia limits that spur zeolite tertiary systems.

North America exhibits mature but technology-rich demand. Shale-gas processing plants in Texas deploy 3A molecular sieves to strip moisture before cryogenic NGL recovery, seeking higher efficiency and longer bed life. EPA PFAS discharge proposals accelerate trials of high-silica zeolites that capture perfluoro-alkyl compounds at parts-per-trillion levels, an emerging revenue stream for specialty producers.

Europe prioritizes sustainability and circularity. Plants in Germany and the Netherlands validate fly-ash-derived zeolites at commercial scale, delivering 40% embodied-carbon reduction relative to virgin mineral routes. Middle-East and Africa capitalize on petrochemical diversification and water scarcity. Saudi Arabia's Vision 2030 resin capacities rely on large-format molecular-sieve towers for feedstock preparation. South Africa's mining sector adopts clinoptilolite for acid-mine drainage remediation, benefitting from domestic natural deposits that eliminate import costs. Collectively, these regional developments underscore the expanding geographic canvas for the zeolite molecular sieve market.

- Arkema

- Axens

- BASF

- CLARIANT

- CWK Chemiewerk Bad Kostritz GmbH

- HengYe Inc.

- Honeywell International Inc.

- JIUZHOU CHEMICALS

- KMI Zeolite Inc.

- KNT Group

- KURARAY CO., LTD.

- Luoyang Jalon Micro-Nano New Material

- Sorbchem India Pvt Ltd.

- Tosoh Corporation

- W. R. Grace & Co.

- Zeochem

- Zeolyst International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Phosphate Bans in Detergents Shifting Builders to Zeolites

- 4.2.2 Petrochemical Dehydration and Gas-Purification Boom

- 4.2.3 Stringent Wastewater Discharge Norms

- 4.2.4 Hygiene-Driven Detergent Demand in Emerging Economies

- 4.2.5 Bio-Refinery Shift Demanding Shape-Selective Catalysts

- 4.3 Market Restraints

- 4.3.1 Enzyme And Chemical Substitutes in Laundry Formulations

- 4.3.2 Volatile Alumina/Silica Feedstock Pricing

- 4.3.3 High Energy Footprint Questioned by ESG Investors

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Raw Material

- 5.1.1 Natural Zeolite

- 5.1.2 Synthetic Zeolite

- 5.2 By End-user Industry

- 5.2.1 Detergents

- 5.2.2 Petrochemical and Refining

- 5.2.3 Industrial Gas Production

- 5.2.4 Waste and Water Treatment

- 5.2.5 Air Purification and HVAC

- 5.2.6 Agriculture and Animal Feed

- 5.2.7 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Arkema

- 6.4.2 Axens

- 6.4.3 BASF

- 6.4.4 CLARIANT

- 6.4.5 CWK Chemiewerk Bad Kostritz GmbH

- 6.4.6 HengYe Inc.

- 6.4.7 Honeywell International Inc.

- 6.4.8 JIUZHOU CHEMICALS

- 6.4.9 KMI Zeolite Inc.

- 6.4.10 KNT Group

- 6.4.11 KURARAY CO., LTD.

- 6.4.12 Luoyang Jalon Micro-Nano New Material

- 6.4.13 Sorbchem India Pvt Ltd.

- 6.4.14 Tosoh Corporation

- 6.4.15 W. R. Grace & Co.

- 6.4.16 Zeochem

- 6.4.17 Zeolyst International

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessmen

- 7.2 Increasing Demand for Using Green Technologies