|

시장보고서

상품코드

1844591

메타크실렌 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Meta-Xylene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

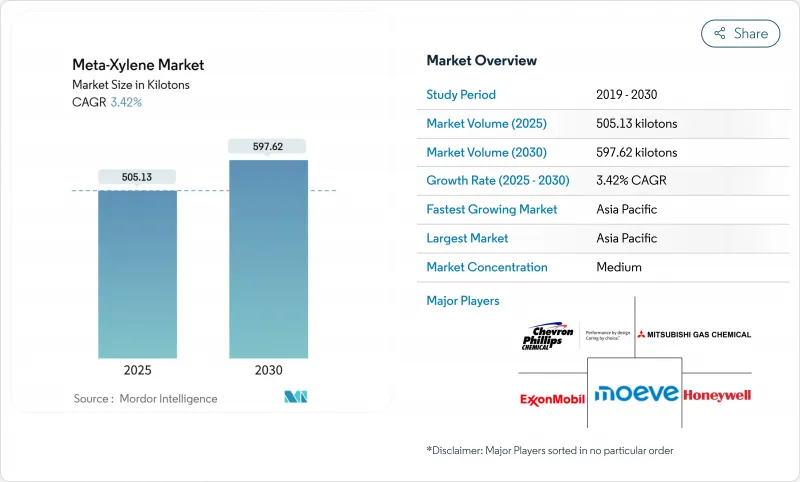

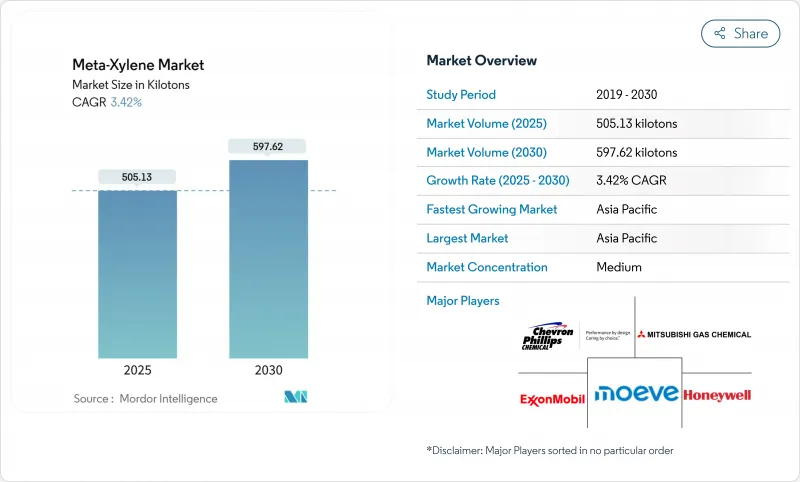

메타크실렌 시장 규모는 2025년에 505.13킬로톤으로 평가되었고, 예측기간(2025-2030년)의 CAGR은 3.42%를 나타낼 것으로 예측되며 2030년에 597.62킬로톤에 이를 전망입니다.

지속적인 PET 및 불포화 폴리에스터 수지(UPR) 소비와 함께 저휘발성 유기화합물(VOC) 및 바이오 기반 코팅 원료로의 전환이 생산량 증가를 뒷받침하고 있으며, 생산자들은 메타자일렌이 이소프탈산의 유일한 원료로서의 역할을 활용하고 있습니다. 중국, 인도, 중동 지역의 통합 방향족 복합체 내 증설로 공급이 수요와 균형을 유지하는 한편, 첨단 추출 기술이 단위 비용을 낮추고 순도 기준을 향상시키고 있습니다. 수요 측면에서는 용매 배출 억제를 위한 규제 압력이 전체 용매 사용량을 감소시키는 동시에 프리미엄 고고형분 페인트에서 메타자일렌의 균형 잡힌 증발 속도 가치를 높이고 있습니다. 원유 가격 변동성이 계속해서 방향족 스프레드에 영향을 미치는 가운데, 다국적 에너지-화학 거대 기업과 지역 선도 기업 간의 진화하는 역학 관계가 경쟁 구도를 재편하고 있습니다.

세계의 메타크실렌 시장 동향 및 인사이트

PET 및 UPR 생산에서의 이소프탈산 수요 증가

이소프탈산은 개질 PET의 열 안정성과 가스 차단 성능을 향상시켜 프리미엄 병, 필름 및 산업용 섬유에 필수적입니다. 자동차 및 전자 제조업체들은 온도가 표준 PET 한계치를 초과할 경우 이소프탈산 개질 PET를 지정하여 메타-자일렌에 대한 수요를 견인하고 있습니다. 혁신 파이프라인은 5-하이드록시메틸푸르푸랄(HMF)과 같은 재생 가능 원료에 점점 더 의존하고 있으며, 상업적 규모에 도달하면 브랜드 소유자들이 탄소 감축 목표를 추구함에 따라 향후 10년 내 바이오 기반 경로가 시장 점유율을 확보할 것으로 예상됩니다. UPR(불포화 폴리우레탄 수지) 분야에서 이소프탈산은 풍력 터빈 나셀 및 해양 복합재의 내식성을 향상시켜 아시아태평양 지역 조선소와 유럽 해상 설비 전반에 걸친 구조용 응용 분야 성장을 뒷받침합니다. 이에 따라 PET와 UPR의 이중 수요가 메타-자일렌 시장 궤적에 가장 강력한 긍정적 영향을 미치고 있습니다.

고고형분/저VOC 산업용 코팅으로의 전환

미국 환경보호청(EPA)의 2024년 유해물질 정보 전달 기준 개정안은 자일렌 유도체에 대한 라벨링 규정을 강화하여, 효과적인 점도 조절을 위해 여전히 메타-자일렌에 의존하는 고고형분 시스템으로 포뮬레이터들을 유도하고 있습니다. 유럽의 탈탄소화 로드맵 역시 저휘발성 유기화합물(VOC) 도료를 장려하여, 메타-자일렌의 중간 수준의 증발 특성을 선호하는 경향 속에서 더 가볍고 빠르게 증발하는 용매로의 대체를 촉진하고 있습니다. 수성 도료는 전체 용매 사용량을 줄이지만, 고급 건축용 및 산업용 유지보수 제품은 응집 보조제로서 메타-자일렌을 계속 사용함으로써 예측 기간 동안 수요를 유지할 전망입니다.

독성 및 가연성 프로파일로 인해 노출 한계가 더욱 엄격해짐

독성물질 및 질병등록청(ATSDR)은 만성 자일렌 노출과 관련된 신경학적 우려를 강조하며, 유럽 규제 기관으로 하여금 8시간 평균 작업장 노출 한계치(TWA)를 낮추는 방안을 검토하도록 촉구하고 있습니다. 강화된 환기 시스템, 방폭 취급 시스템 및 개인 보호 장비 도입은 특히 소규모 또는 독립 시설의 생산 비용을 증가시킵니다. 가능한 경우 코팅제 제조업체들은 대체 용매를 실험하고 있으나, 메타-자일렌의 독특한 용해력 및 가공 특성으로 인해 완전한 대체가 어려워 수요를 완화시키지만 완전히 제거하지는 못하고 있습니다.

부문 분석

2024년 메타-자일렌 시장 규모에서 이소프탈산 생산이 46.17%로 가장 큰 비중을 차지했으며, 이는 고성능 PET 병 및 내식성 UPR 라미네이트 분야에서 해당 부문의 확고한 역할을 강조합니다. 바이오 기반 이소프탈산으로의 점진적 전환은 재생 가능 화학물질이 상업적 적용 단계에 진입함에 따라 원료 조달 구조의 재편을 시사하며, 2030년까지 연평균 6.90% 성장할 것으로 전망됩니다. 유럽과 일본의 초기 도입 기업들은 이미 브랜드 소유자 프리미엄 확보를 위한 대량 균형 인증 절차를 시행 중이며, 아시아 생산자들은 바이오매스 공급 경로 인근에 신규 생산 시설을 건설하고 있습니다.

중기적으로 2,4- 및 2,6-자일리딘 유래 농약·의약품 중간체는 독성학 관련 규제 우려에도 틈새 수요를 유지할 전망입니다. 용매 응용 분야는 절대 톤수 기준 축소되나, 특수 전자제품 및 의약품 세척에 메타-자일렌의 좁은 비등 범위가 요구되는 고부가가치 영역에서는 가치 탄력성을 보인다. 종합하면 응용 분야 구성은 대량 용매 의존에서 고마진 수지 및 특수 화학 용도로 전환되며, 표면적 성장률은 완만하나 전체 수익성은 상승할 것입니다.

메타-자일렌 시장 보고서는 응용 분야(이소프탈산, 2,4- 및 2,6-자일리딘 등), 최종 사용자 산업(건설 및 인프라, 포장, 자동차 및 운송 등), 순도/등급(고순도 MX, 산업용 등급 MX 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류됩니다. 시장 전망은 물량(톤) 기준으로 제공됩니다.

지역별 분석

아시아태평양 지역은 2024년 글로벌 물량의 53.45%를 차지했으며, 원료 유연성과 규모의 경제를 활용하는 중국과 인도의 수직 통합 복합 시설에 힘입어 2030년까지 연평균 5.50%의 성장률을 기록할 것으로 전망됩니다. 중국의 저우산방향족 화합물 허브와 광둥CNOOC-Shell 합작 투자는 각각 지역 자급률을 높여 미국 및 유럽으로부터의 수입 요구를 억제하고 있습니다. 인도의 870억 달러 규모 석유화학 청사진은 2035년까지 국내 자일렌 생산 능력을 550만 톤으로 확대해 다운스트림 폴리에스터, 코팅, 제약 산업군에 원료 공급 안정성을 확보할 계획입니다. 일본과 한국은 중국 수출 증가로 경쟁이 심화되며 구조적 마진 압박에 직면해 고순도 특수제품 및 차별화된 제형으로 전환을 추진 중입니다.

북미는 우수한 분리 기술, 풍부한 셰일 유래 나프타, 방대한 코팅 고객 기반과의 근접성으로 전략적 중요성을 유지하고 있습니다. 그러나 에너지 비용 상승 압력과 강화된 환경 규제 준수로 운영 비용이 증가하고 있습니다. 셰브론이 필립스66의 CPChem 지분을 150억 달러에 인수할 가능성이 있는 것은 기업들이 규모와 원료 통합 혜택을 추구함에 따라 이 지역의 통합 추세를 강조합니다. 멕시코의 신흥 자동차 가치 사슬은 용매 및 수지 수요를 자극하지만 미국 수입에 크게 의존하여 USMCA 관세 안정성의 중요성을 보여줍니다.

유럽은 높은 유틸리티 비용과 엄격한 탄소 정책으로 인해 일반 방향족 화학물질에 대한 신규 투자가 위축되는 등 가장 가파른 운영적 도전에 직면해 있습니다. 유럽 그린딜의 진화하는 탄소국경조정장치(CBAM)는 국내 생산을 부분적으로 보호할 수 있으나 행정적 복잡성을 가중시킵니다. 쉘이 2030년까지 기초화학 사업에서 철수하겠다고 발표한 것은 국제 에너지 대기업들이 자본을 LNG 및 재생에너지로 재분배하는 방식을 대표적으로 보여줍니다. 잔류 유럽 생산사들은 기후 중립 소재에 대한 규제 인센티브를 활용해 바이오 기반 이소프탈산 및 순환형 PET 원료 생산을 강조하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- PET 및 UPR 생산에서의 이소프탈산 수요 증가

- 고고형분/저VOC 산업용 도료로의 전환

- 통합 PX-MX 방향족 복합체 시설의 생산 능력 확대

- 도료 및 코팅 부문 수요 증가

- 자동차 산업 확대

- 시장 성장 억제요인

- 독성 및 가연성 프로파일로 인한 노출 한계 강화

- 원유 가격 변동성이 방향족 스프레드에 미치는 영향

- 자본 집약적 이성질체 분리 기술로 인한 신규 진입자 억제

- 밸류체인 분석

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 업계의 라이벌 관계

제5장 시장 규모 및 성장 예측(수량)

- 용도별

- 이소프탈산

- 2,4- 및 2,6-자일리딘

- 용매

- 기타 용도(농약 중간체 등)

- 최종 사용자 산업별

- 건설 및 인프라

- 포장

- 자동차 및 운송

- 의약 및 농약

- 전기 및 전자

- 순도 및 등급별

- 99.9% 이상 MX(고순도)

- 공업 등급 MX

- 혼합 크실렌 스트림

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- Avantor, Inc.

- Chevron Phillips Chemical Company LLC

- Exxon Mobil Corporation

- Hengli Petrochemical

- Honeywell International Inc.

- JXTG Nippon Oil & Energy

- LOTTE Chemical CORPORATION

- MITSUBISHI GAS CHEMICAL COMPANY, INC.

- Moeve

- Shell Chemicals

- S-OIL CORPORATION

- Suzhou Jiutai Group Co., Ltd.

- Vizag Chemicals

제7장 시장 기회와 전망

HBR 25.11.03The Meta-Xylene Market size is estimated at 505.13 kilotons in 2025, and is expected to reach 597.62 kilotons by 2030, at a CAGR of 3.42% during the forecast period (2025-2030).

Sustained PET and unsaturated polyester resin (UPR) consumption, together with a shift toward low-VOC and bio-based coating ingredients, underpins volume growth as producers leverage meta-xylene's role as the sole feedstock for isophthalic acid. Capacity additions inside integrated aromatics complexes across China, India, and the Middle East keep supply aligned with demand, while advanced extraction technologies lower unit costs and improve purity thresholds. On the demand side, regulatory pressure to curb solvent emissions is simultaneously reducing overall solvent volumes yet elevating the value of meta-xylene's balanced evaporation rate in premium, high-solids paints. As crude price volatility continues to influence aromatics spreads, the evolving dynamics among multinational energy-chemical giants and regional champions are reshaping the competitive landscape.

Global Meta-Xylene Market Trends and Insights

Growing Demand for Isophthalic Acid in PET & UPR Production

Isophthalic acid enhances thermal stability and gas-barrier performance in modified PET, making it indispensable for premium bottles, films and industrial fibers. Automotive and electronics manufacturers specify isophthalic acid-modified PET when temperatures exceed standard PET thresholds, reinforcing pull-through demand for meta-xylene. Innovation pipelines increasingly rely on renewable feedstocks such as 5-hydroxymethylfurfural (HMF); once commercial scale is reached, bio-based routes are expected to capture share within the next decade as brand owners pursue carbon-reduction goals. In UPR, isophthalic acid delivers higher corrosion resistance in wind-turbine nacelles and marine composites, supporting structural applications growth across Asia-Pacific shipyards and European offshore installations. The dual demand from PET and UPR accordingly registers the strongest positive impact on the meta-xylene market trajectory.

Shift Toward High-Solids/Low-VOC Industrial Coatings

The United States Environmental Protection Agency's 2024 Hazard Communication Standard update tightened labeling norms for xylene derivatives, pushing formulators toward higher-solids systems that still rely on meta-xylene for effective viscosity control. Europe's decarbonization roadmap similarly incentivizes low-VOC coatings, driving substitution of lighter, faster-evaporating solvents in favor of meta-xylene's more moderate evaporation profile. Although waterborne paints reduce aggregate solvent volumes, premium architectural and industrial maintenance products continue to incorporate meta-xylene as a coalescent aid, preserving demand through the forecast period.

Toxicological & Flammability Profile Driving Stricter Exposure Limits

The Agency for Toxic Substances and Disease Registry (ATSDR) underscores neurological concerns linked to chronic xylene exposure, prompting European regulators to contemplate lowering the 8-hour TWA occupational limit. Implementing enhanced ventilation, spark-proof handling systems, and personal protective equipment raises production costs, especially for small or standalone facilities. Where viable, coatings producers experiment with alternative solvents, yet meta-xylene's unique solvency and processing characteristics hinder full substitution, tempering but not eliminating demand.

Other drivers and restraints analyzed in the detailed report include:

- Capacity Expansions in Integrated PX-MX Aromatics Complexes

- Increasing Demand from Paints and Coatings Sector

- Crude-Oil Price Volatility Cascading to Aromatics Spreads

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Isophthalic acid production accounted for the largest share of the meta-xylene market size, at 46.17% in 2024, underscoring the segment's entrenched role in high-performance PET bottles and corrosion-resistant UPR laminates. The progressive switch toward bio-based isophthalic acid, projected to grow at 6.90% CAGR to 2030, signals a structural realignment in feedstock sourcing as renewable chemistries enter commercial deployment. Early adopters in Europe and Japan already certify mass-balance routines to capture brandowner premiums, while Asian producers erect greenfield units adjacent to biomass supply corridors.

Over the medium term, pesticide and pharmaceutical intermediates derived from 2,4- and 2,6-xylidine will preserve niche demand despite regulatory concerns around toxicology. Solvent applications shrink in absolute tonnage but exhibit value resilience where specialty electronics and pharmaceutical cleaning require meta-xylene's narrow boiling range. Taken together, the application mix is migrating from bulk solvent dependency toward higher-margin resin and specialty chemical use, elevating overall profitability despite moderate headline growth.

The Meta-Xylene Market Report is Segmented by Application (Isophthalic Acid, 2, 4- & 2, 6-Xylidine, and More), End-User Industry (Construction & Infrastructure, Packaging, Automotive & Transportation, and More), Purity/Grade (High-Purity MX, Industrial-Grade MX, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (tons).

Geography Analysis

Asia-Pacific captured 53.45% of global volumes in 2024 and is forecast to clock a 5.50% CAGR through 2030, driven by vertically integrated complexes across China and India that harness feedstock flexibility and scale economics. China's Zhoushan aromatics hub and Guangdong CNOOC-Shell joint venture each broaden regional self-sufficiency, curbing import requirements from the United States and Europe. India's USD 87 billion petrochemical blueprint seeks to raise domestic xylene capacity to 5.5 million t by 2035, securing raw material availability for downstream polyester, coatings, and pharma corridors. Japan and South Korea confront structural margin pressure as Chinese exports intensify competition, spurring these economies to pivot toward high-purity specialties and differentiated formulations.

North America retains strategic significance through superior separation technologies, abundant shale-derived naphtha and proximity to a vast coatings customer base. However, upward pressure on energy costs and tightening environmental compliance increase operating expenditure. Chevron's potential USD 15 billion acquisition of Phillips 66's CPChem stake underscores the region's consolidation trajectory as companies chase scale and feedstock integration benefits. Mexico's emerging automotive value chain stimulates solvent and resin demand but relies heavily on United States imports, illustrating the importance of the USMCA's tariff stability.

Europe confronts the steepest operating challenges, with high utility costs and stringent carbon policies discouraging fresh investment in commodity aromatics. The European Green Deal's evolving carbon-border adjustment mechanism may partially shield domestic output yet adds administrative complexity. Shell's announcement to exit base chemicals by 2030 typifies how international energy majors reallocate capital toward LNG and renewables. Remaining European producers emphasize bio-based isophthalic acid and circular PET feedstocks, capitalizing on regulatory incentives for climate-neutral materials.

- Avantor, Inc.

- Chevron Phillips Chemical Company LLC

- Exxon Mobil Corporation

- Hengli Petrochemical

- Honeywell International Inc.

- JXTG Nippon Oil & Energy

- LOTTE Chemical CORPORATION

- MITSUBISHI GAS CHEMICAL COMPANY, INC.

- Moeve

- Shell Chemicals

- S-OIL CORPORATION

- Suzhou Jiutai Group Co., Ltd.

- Vizag Chemicals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for isophthalic acid in PET and UPR production

- 4.2.2 Shift toward high-solids/low-VOC industrial coatings

- 4.2.3 Capacity expansions in integrated PX-MX aromatics complexes

- 4.2.4 Increasing demand from paints and coatings sector

- 4.2.5 Expansion of the automotive sector

- 4.3 Market Restraints

- 4.3.1 Toxicological and flammability profile driving stricter exposure limits

- 4.3.2 Crude-oil price volatility cascading to aromatics spreads

- 4.3.3 Capital-intensive isomer separation technology deterring newcomers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Industry Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Application

- 5.1.1 Isophthalic Acid

- 5.1.2 2,4- and 2,6-Xylidine

- 5.1.3 Solvents

- 5.1.4 Other Applications (Pesticide Intermediates, etc.)

- 5.2 By End-user Industry

- 5.2.1 Construction and Infrastructure

- 5.2.2 Packaging

- 5.2.3 Automotive and Transportation

- 5.2.4 Pharmaceuticals and Agrochemicals

- 5.2.5 Electrical and Electronics

- 5.3 By Purity/Grade

- 5.3.1 Greater than or equal to 99.9 % MX (High-Purity)

- 5.3.2 Industrial-Grade MX

- 5.3.3 Mixed Xylenes Stream

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Avantor, Inc.

- 6.4.2 Chevron Phillips Chemical Company LLC

- 6.4.3 Exxon Mobil Corporation

- 6.4.4 Hengli Petrochemical

- 6.4.5 Honeywell International Inc.

- 6.4.6 JXTG Nippon Oil & Energy

- 6.4.7 LOTTE Chemical CORPORATION

- 6.4.8 MITSUBISHI GAS CHEMICAL COMPANY, INC.

- 6.4.9 Moeve

- 6.4.10 Shell Chemicals

- 6.4.11 S-OIL CORPORATION

- 6.4.12 Suzhou Jiutai Group Co., Ltd.

- 6.4.13 Vizag Chemicals

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment