|

시장보고서

상품코드

1844605

총륜구동차 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Automotive All-wheel-drive - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

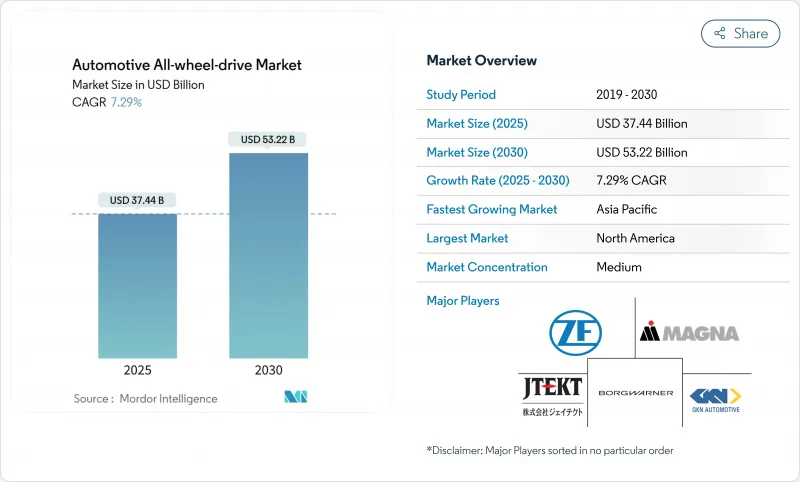

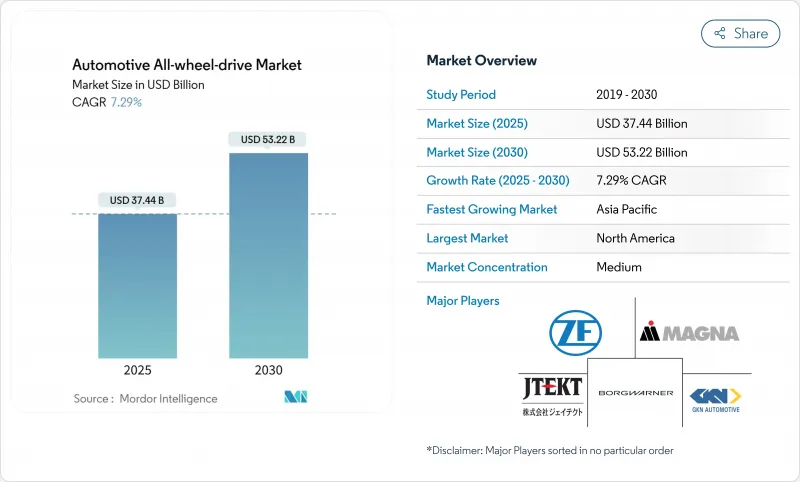

총륜구동차 시장 규모는 2025년 374억 4,000만 달러에 달하고, 2030년에는 532억 2,000만 달러에 이를 것으로 예상됩니다.

안전 의무화 강화, SUV 및 크로스오버의 급속한 보급, 듀얼 모터 전동 드라이브 라인의 경제성 성숙이 이 확대를 지원하고 있습니다. ADAS(첨단 운전자 보조 시스템)는 충돌 회피 성능을 최적화하기 위해 예측 가능한 토크 전달에 의존하기 때문에 OEM은 현재 플랫폼의 초기 단계부터 트랙션 관리 통합을 선호합니다. 또한 전동화는 트랜스퍼 케이스와 샤프트를 소프트웨어 제어 E 모터로 대체함으로써 오랜 기계 비용 부담을 줄여줍니다. 희토류 자석과 파워 반도체를 중심으로 한 공급망의 재구축은 차량당 AWD 비율이 높아짐에 따라 매우 중요해지고 있습니다. AWD를 일회성 하드웨어 기능에서 데이터 구동 성능 향상을 위한 지속적인 수익 채널로 변화시키고 드라이브 라인 하드웨어와 무선 소프트웨어 서비스를 융합시키는 수직 통합 공급업체에 대한 경쟁력의 보상은 점점 높아지고 있습니다.

세계의 총륜구동차 시장 동향과 인사이트

세계 SUV와 CUV 수요 급증

세계 SUV 및 크로스오버 차량의 생산량은 2030년까지 2,800만 대에 이를 것으로 예상되고 있으며, 트랙션 시스템이 옵션에서 기본 패키징으로 전환함에 따라 AWD를 장착하는 비율은 2025년 45%에서 65%로 상승할 것으로 예측됩니다. 구매자는 포장 도로를 주로 주행하는 경우에도 AWD를 심리적 안전 프리미엄으로 간주합니다. 중국 브랜드는 현재 AWD를 시장 경쟁력 있는 기본 가격으로 번들로 삼아 신흥 시장의 과거 비용 장벽을 낮추고 있습니다. OEM은 AWD에 ADAS 스위트를 번들하는 경우가 많으며, 안전성을 강화하고 넷마진을 높이고 있습니다. 소비자 유틸리티 마인드는 연중 수요를 유지하고 총륜구동차 시장을 겨울 계절성에 대한 의존도를 낮추고 있습니다.

전동화에 의한 듀얼 모터 e-AWD의 보급

SAE 테스트에 따르면 듀얼 모터 BEV는 애드온 기계식 AWD를 사용하는 단일 모터 레이아웃보다 에너지 효율이 9% 향상되었습니다. 샤프트와 트랜스퍼 케이스를 제거하면 무게가 줄어들고 정확한 토크 제어가 가능합니다. 상용차 사업자는 유지 보수를 줄이고 전체 차축의 회생 브레이크로부터 이익을 얻을 수 있습니다. 현대의 새로운 하이브리드 플랫폼은 e-AWD가 비용을 절감하면서 ICE와 풀 BEV 아키텍처를 다루는 방법을 보여줍니다.

높은 부품 비용과 연료/에너지 페널티 vs 2WD

기존의 AWD는 아르곤의 시뮬레이션에 따르면 제조 비용에 1,500-3,000달러를 추가해 ICE의 연비를 약 1-2mpg 저하시킵니다. BEV의 항속 거리는 현대 Ioniq 5 데이터시트에서 볼 수 있듯이 듀얼 모터 버전에서는 10-15% 감소합니다. 제조업체 각사는 비용 절감을 위해 AWD를 표준 장비로 하는 경우가 많지만, 이것은 가치 중시의 부문에서는 엔트리 가격을 인상하게 됩니다. 배터리 가격은 계속 떨어지고 있지만 신흥 시장에서는 단기적인 벌금이 판매 장애물이되었습니다.

부문 분석

승용차는 2024년 총륜구동차 시장 점유율의 65.77%를 차지했으며, SUV, 크로스오버, AWD 탑재 세단 증가로 인해 트랙션 매니지먼트가 틈새 옵션에서 주류 기대로 이행한 것을 나타냅니다. OEM은 AWD를 번들 안전성 및 인포테인먼트 패키지와 결합하여 거래 가격을 인상하는 동시에 예측 가능한 토크 전달에 보상하는 규제 테스트 사이클을 만족시킵니다. 소비자는 AWD가 젖은 노면이나 동결된 노면에서 연간 제공하는 신뢰성을 높이 평가하고, 보험사는 그 이점을 보험료의 인하에 반영시키는 경우가 많아, 온난한 지역에서도 채용이 진행되고 있습니다. 또한 프리미엄 자동차는 소프트웨어 정의 토크 벡터링을 사용하여 트림 레벨 간의 라이드 역학을 차별화하고 AWD 능력을 경험적 판매 포인트로 전환하여 더 높은 잔존 가치를 지원합니다.

상용차는 2030년까지 연평균 복합 성장률(CAGR)이 7.96%로 가장 빠르게 확대됩니다. 이는 소화물, 유틸리티 및 긴급 차량이 다양한 로드 및 날씨 조건 하에서 미션 크리티컬한 가동 시간을 보장하기 위해 AWD를 채택하기 때문입니다. 전동 액슬은 트랜스퍼 케이스를 없애 설치를 간소화하고, 유지 보수의 다운 타임을 줄이고, 대도시 중심부에 퍼지는 제로 에미션의 의무에 대응합니다. 함대 텔레매틱스는 전기 AWD가 휠 스핀과 관련된 타이어의 마모를 줄이고 회생 브레이크의 효율을 높이고 초기 가격이 높음에도 불구하고 총 소유 비용을 개선한다는 것을 확인했습니다. 낮은 배출가스 상업수송에 대한 정부의 우대조치와 보다 엄격한 안전감사는 AWD를 향후 차량조달 사이클의 핵심 요건으로 자리매김하여 사양화율을 더욱 가속화시킵니다.

2024년 총륜구동차 시장 규모의 84.25%는 내연 엔진이 차지했지만, 듀얼 모터 레이아웃이 트랜스퍼 케이스의 비용을 삭감하고 토크 정밀도를 향상시키기 위해 배터리 전기 파워트레인이 CAGR 10.11%를 나타낼 전망입니다. ICE 중심 플랫폼은 하이브리드 AWD를 제공하기 위해 전면 또는 후면에 전동 모듈을 통합하는 경향이 강화되어 배출 가스 규제 강화에 대한 투자의 미래를 강화하고 있습니다. 배터리 가격 인하와 정부 인센티브가 함께 총소유비용 격차가 줄어들고 OEM 각사는 주류 가격대에서 AWD 탑재 BEV를 출시하게 됩니다.

연료전지에 대한 노력은 새로운 상업적 가능성을 보여줍니다. BMW가 도요타와 공동으로 2028년에 발매하는 수소 SUV는 장거리 주행 성능과 헤비 듀티나 한랭지용 전동 AWD의 조합을 목표로 하고 있습니다. 듀얼 모터 아키텍처는 소프트웨어로 수익을 창출하는 길을 열고 자동차 제조업체는 성능 업그레이드를 공매하고 있습니다. 카본 페널티로 ICE의 런닝 코스트가 상승하는 시장에서는 이러한 전동화 시스템이 더욱 기세를 늘리고 e-AWD가 트랙션, 효율, 컴플라이언스의 새로운 베이스라인이 됩니다.

지역별 분석

북미는 2024년 총륜구동차 시장의 43.17%를 차지하며 픽업, SUV 및 눈길, 혼합 지형, 보험 등급 우대 조치에 직면하는 함대 부문으로부터 왕성한 수요가 있었습니다. 미국 규제 당국은 AWD와 의무화된 안전 기술을 결합하여 보급을 강화하고 있습니다. 캐나다는 겨울철 트랙션이 기본 기대치이기 때문에 경차 중 AWD 보급률이 가장 높습니다.

아시아태평양은 CAGR 8.55%로 가장 빠르게 성장하는 지역입니다. 중국의 OEM은 AWD를 기존의 이륜구동 경쟁차를 가격으로 낮추는 주류 수출차에 통합하여 비용 효율적인 트랙션에 대한 세계적인 인식을 재구성하고 있습니다. 인도 최초의 대중용 AWD EV인 Maruti Suzuki e-Vitara의 도입은 첨단 드라이브 라인 능력의 민주화를 돋보이게 합니다. 한국에서는 현대자동차와 기아자동차의 포트폴리오 전체에서 e-AWD의 확대가 계속되고 있으며, 일본에서는 하이브리드 AWD의 전통이 세계 전개에 활용되고 있습니다.

유럽에서는 꾸준하지만 그다지 극적인 성장은 보이지 않고, 성능을 유지하면서 유로 7의 배기 가스 목표를 달성하기 위해 전동 AWD가 유력한 루트가 되고 있습니다. 이 대륙의 프리미엄 자동차는 일반 안전 규정 II에 따른 ADAS와 통합된 세밀한 토크 벡터링을 통해 차별화를 도모하고 있습니다. 남미와 아프리카는 인프라 개선과 수입 관세 인하로 인해 AWD 크로스오버 소매 가격이 하락하고 있기 때문에 현재도 소규모로 보급되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계 SUV 및 CUV 수요 상승

- 전동화에 의한 듀얼 모터 e-AWD의 채용

- 충돌 회피 및 트랙션 안전에 관한 규제 강화

- 프리미엄 부문에서 성능 처리로 소비자 이동

- 기후 변화에 의한 OEM의 AWD 표준화

- OTA 대응 소프트웨어 토크 벡터링 아키텍처

- 시장 성장 억제요인

- 2WD에 비해 높은 부품 비용과 연료/에너지 페널티

- e-액추에이터의 자석과 반도체 공급의 병목

- 배터리 EV에 있어서 항속 거리 손실의 우려

- 효율 최적화된 드라이브 라인으로의 자율 주행 변화

- 가치/공급망 분석

- 기술적 전망

- 규제 상황

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 라이벌의 격렬함

제5장 시장 규모·성장 예측

- 자동차 유형별

- 승용차

- 해치백 및 세단

- SUV 및 크로스오버

- 상용차

- 소형 상용차

- 대형 트럭 및 버스

- 승용차

- 추진 방식별

- 내연기관(ICE)

- 하이브리드 전기자동차(HEV)

- 배터리 전기자동차(BEV)

- 연료전지 전기자동차(FCEV)

- 시스템 유형별

- 파트타임/수동 AWD

- 풀타임/자동 AWD

- 전기/e-AWD(듀얼 모터, 쿼드 모터)

- 능동 토크 벡터링 AWD

- 구성 요소별

- 트랜스퍼 케이스

- 차동 장치(센터, 프런트, 리어)

- 커플링 및 클러치 팩

- 프로펠러 샤프트 및 구동축

- 제어 장치 및 소프트웨어

- 판매 채널별

- OEM

- 애프터마켓

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- BorgWarner Inc.

- GKN Automotive(Melrose)

- ZF Friedrichshafen AG

- Magna International Inc.

- JTEKT Corporation

- Toyota Motor Corporation

- Nissan Motor Co. Ltd

- Continental AG

- Eaton Corporation PLC

- American Axle & Manufacturing

- Dana Inc.

- Haldex AB

- Hyundai Motor Company

- Audi AG

- BMW Group

- Mercedes-Benz Group AG

- Schaeffler AG

- Mahle GmbH

- Stellantis NV

제7장 시장 기회와 전망

KTH 25.11.05The automotive all-wheel drive market size reached USD 37.44 billion in 2025 and is expected to reach USD 53.22 billion by 2030, reflecting a steady 7.29% CAGR.

Strengthening safety mandates, rapid SUV and crossover uptake, and the maturing economics of dual-motor electrified drivelines together underpin this expansion. OEMs now prioritize traction management integration from the earliest platform stages because advanced driver-assistance systems depend on predictable torque delivery for optimal crash-avoidance performance. Electrification also removes long-standing mechanical cost penalties by replacing transfer cases and shafts with software-controlled e-motors. Supply-chain re-engineering around rare-earth magnets and power semiconductors is becoming pivotal as AWD content per vehicle rises. Competitive dynamics increasingly reward vertically integrated suppliers that fuse driveline hardware with over-the-air software services, transforming AWD from a one-time hardware feature into a recurring revenue channel for data-driven performance upgrades.

Global Automotive All-wheel-drive Market Trends and Insights

Soaring SUV and CUV Demand Worldwide

Global SUV and crossover output is forecast to hit 28 million units by 2030, and the share fitted with AWD is expected to climb from 45% in 2025 to 65% as traction systems shift from optional to default packaging. Buyers increasingly view AWD as a psychological safety premium even when driving predominantly on paved roads. Chinese brands now bundle AWD with competitive base pricing, lowering the historical cost barrier in emerging markets. OEMs frequently pair AWD with bundled ADAS suites, reinforcing safety credentials and boosting net margins. The utility mindset of consumers sustains year-round demand, making the automotive all-wheel drive market less dependent on winter seasonality.

Electrification-Driven Adoption of Dual-Motor e-AWD

Dual-motor BEVs achieve 9% better energy efficiency than single-motor layouts using add-on mechanical AWD according to SAE testing . Eliminating shafts and transfer cases cuts weight and unlocks precise torque control. Commercial operators benefit from lower maintenance and regenerative braking on all axles. Hyundai's new hybrid platform illustrates how e-AWD bridges ICE and full BEV architecture while containing costs.

Higher BOM Cost and Fuel/Energy Penalty vs 2WD

Traditional AWD adds USD 1,500-3,000 to build cost and reduces ICE fuel economy by roughly 1-2 mpg according to Argonne simulations . BEV range drops 10-15% in dual-motor versions, as demonstrated by the Hyundai Ioniq 5 data sheet. Manufacturers often convert AWD into standard equipment to dilute cost, yet this raises entry prices in value-focused segments. Battery prices continue to fall, but the near-term penalty remains a sales hurdle in emerging markets.

Other drivers and restraints analyzed in the detailed report include:

- Tightening Crash-Avoidance and Traction Safety Mandates

- Consumer Shift to Performance Handling in Premium Segments

- Magnet and Semiconductor Supply Bottlenecks for e-Actuators

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger cars captured 65.77% of the automotive all-wheel drive market share in 2024, illustrating how SUVs, crossovers, and increasingly AWD-equipped sedans have moved traction management from niche option to mainstream expectation. OEMs pair AWD with bundled safety and infotainment packages, boosting transaction prices while satisfying regulatory test cycles that reward predictable torque delivery. Consumers value the year-round confidence AWD offers on wet or icy roads, and insurers often reflect that benefit in lower premiums, reinforcing adoption even in temperate regions. Premium marques also use software-defined torque vectoring to differentiate ride dynamics across trim levels, turning AWD capability into an experiential selling point that supports higher residual values.

Commercial vehicles post the fastest expansion at a 7.96% CAGR through 2030 as parcel, utility, and emergency fleets adopt AWD to ensure mission-critical uptime under varied payloads and weather conditions. Electrified axles simplify installations by eliminating transfer cases, lowering maintenance downtime, and meeting zero-emission mandates spreading across large urban centers. Fleet telematics confirm that electric AWD reduces wheel-spin-related tire wear and enhances regenerative braking efficiency, improving total cost of ownership despite higher upfront prices. Government incentives for low-emission commercial transport and stricter safety audits further accelerate specification rates, positioning AWD as a core requirement for future fleet procurement cycles.

Internal combustion engines still represented 84.25% of the automotive all-wheel drive market size in 2024, but battery-electric powertrains are rising at a 10.11% CAGR as dual-motor layouts erase transfer-case costs and sharpen torque accuracy. ICE-centric platforms increasingly embed electric front or rear modules to offer hybrid AWD, future-proofing investments against tightening emissions rules. Reduced battery prices and government incentives jointly narrow the total-cost-of-ownership gap, prompting OEMs to launch AWD-equipped BEVs across mainstream price bands.

Fuel-cell initiatives indicate fresh commercial potential: BMW's collaboration with Toyota on a 2028 hydrogen SUV aims to pair long-range capability with electric AWD for heavy-duty or cold-weather routes. Dual-motor architectures also open software monetization paths, letting automakers sell performance upgrades over the air. In markets where carbon penalties inflate ICE running costs, these electrified systems gain further momentum, positioning e-AWD as the new baseline for traction, efficiency, and compliance.

The Automotive All-Wheel Drive Market Report is Segmented by Vehicle Type (Passenger Cars and Commercial Vehicles), Propulsion Type (Internal-Combustion Engine (ICE), Hybrid Electric Vehicle (HEV), and More), System Type (Part-Time/Manual AWD, Full-Time/Automatic AWD, and More), Component (Transfer Case, and More), Sales Channel, and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 43.17% of the automotive all-wheel drive market in 2024 with robust demand from pickups, SUVs, and fleet segments that confront snow, mixed terrain, and insurance rating incentives. U.S. regulators coupling AWD with mandated safety technologies reinforce uptake. Canada exhibits the highest AWD penetration among light vehicles because winter traction is a baseline expectation.

Asia Pacific is the fastest-growing region at an 8.55% CAGR. Chinese OEMs embed AWD into mainstream exports that undercut traditional two-wheel-drive competitors on price, reshaping global perceptions of cost-effective traction. India's introduction of the Maruti Suzuki e-Vitara, the country's first mass-market AWD EV, highlights the democratization of advanced driveline capability. South Korea continues to scale e-AWD across Hyundai and Kia portfolios, while Japan leverages hybrid AWD heritage for global deployments.

Europe shows steady but less dramatic growth, with electrified AWD as a favored route to meet Euro 7 emission goals while preserving performance. The continent's premium marques differentiate through fine-grained torque vectoring, integrated with ADAS aligned to General Safety Regulation II. South America and Africa remain smaller today yet illustrate rising adoption on the back of infrastructure upgrades and import duty reductions that lower retail prices for AWD crossovers.

- BorgWarner Inc.

- GKN Automotive (Melrose)

- ZF Friedrichshafen AG

- Magna International Inc.

- JTEKT Corporation

- Toyota Motor Corporation

- Nissan Motor Co. Ltd

- Continental AG

- Eaton Corporation PLC

- American Axle & Manufacturing

- Dana Inc.

- Haldex AB

- Hyundai Motor Company

- Audi AG

- BMW Group

- Mercedes-Benz Group AG

- Schaeffler AG

- Mahle GmbH

- Stellantis N.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Soaring SUV and CUV demand worldwide

- 4.2.2 Electrification-driven adoption of dual-motor e-AWD

- 4.2.3 Tightening crash-avoidance and traction safety mandates

- 4.2.4 Consumer shift to performance handling in premium segments

- 4.2.5 Climate-volatility prompting OEM AWD standardisation

- 4.2.6 OTA-enabled software torque-vectoring architectures

- 4.3 Market Restraints

- 4.3.1 Higher BOM cost and fuel/energy penalty vs 2WD

- 4.3.2 Magnet and semiconductor supply bottlenecks for e-actuators

- 4.3.3 Range-loss concern in battery-EVs

- 4.3.4 Autonomous-driving shift toward efficiency-optimised drivelines

- 4.4 Value / Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.1.1 Hatchbacks and Sedans

- 5.1.1.2 SUVs and Crossovers

- 5.1.2 Commercial Vehicles

- 5.1.2.1 Light Commercial Vehicles

- 5.1.2.2 Heavy Trucks and Buses

- 5.1.1 Passenger Cars

- 5.2 By Propulsion Type

- 5.2.1 Internal-Combustion Engine (ICE)

- 5.2.2 Hybrid Electric Vehicle (HEV)

- 5.2.3 Battery Electric Vehicle (BEV)

- 5.2.4 Fuel-Cell Electric Vehicle (FCEV)

- 5.3 By System Type

- 5.3.1 Part-Time/Manual AWD

- 5.3.2 Full-Time/Automatic AWD

- 5.3.3 Electric/e-AWD (Dual-Motor, Quad-Motor)

- 5.3.4 Active Torque-Vectoring AWD

- 5.4 By Component

- 5.4.1 Transfer Case

- 5.4.2 Differential (Center, Front, Rear)

- 5.4.3 Coupling and Clutch Pack

- 5.4.4 Prop-Shaft and Drive Shaft

- 5.4.5 Control Unit and Software

- 5.5 By Sales Channel

- 5.5.1 OEM-Installed

- 5.5.2 Aftermarket Retrofit

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 South Africa

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 BorgWarner Inc.

- 6.4.2 GKN Automotive (Melrose)

- 6.4.3 ZF Friedrichshafen AG

- 6.4.4 Magna International Inc.

- 6.4.5 JTEKT Corporation

- 6.4.6 Toyota Motor Corporation

- 6.4.7 Nissan Motor Co. Ltd

- 6.4.8 Continental AG

- 6.4.9 Eaton Corporation PLC

- 6.4.10 American Axle & Manufacturing

- 6.4.11 Dana Inc.

- 6.4.12 Haldex AB

- 6.4.13 Hyundai Motor Company

- 6.4.14 Audi AG

- 6.4.15 BMW Group

- 6.4.16 Mercedes-Benz Group AG

- 6.4.17 Schaeffler AG

- 6.4.18 Mahle GmbH

- 6.4.19 Stellantis N.V.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment